Medical Aesthetics Regenerative Sector Welcomes a 'Game-Changer': First Compliant Class III Certificate Set to Land

Recently, another new material is being fiercely snapped up by capital.

First, in November,Moyang Biotech Announces Nearly RMB 100 Million in Series B+ Financing, which boasts the core product “Magic Crystal Microcrystalline,” a calcium hydroxyapatite-based facial filler for injection, is poised to secure China’s first regulatory approval in the field of injectable soft-tissue facial fillers for medical aesthetics. Recently,Lingtong New Materials Announces Completion of Multi-Million Yuan Angel Financing Round, which focuses on the research and development of hydroxyapatite microspheres, aiming to break the long-standing monopoly held by foreign entities in this technological field.

Beyond the capital markets, the product side has also been abuzz recently. On December 18,Giant Biogene’s Bone Repair Material Officially Approved as Class III Medical Device, the inorganic component of this material is hydroxyapatite particles, which are key to its filling and restorative functions. Looking back to September this year, Allergan’s (a subsidiary of AbbVie) product HArmonyCa successfully completed registration testing in China and is poised to commence clinical trials. It is reported that the product has already obtained EU CE certification and was officially launched in Hong Kong earlier this year. Its core ingredient is calcium hydroxyapatite (CaHA) microspheres, with primary efficacy in facial filling and skin tightening and lifting.

It is not difficult to find that,“Hydroxyapatite”It has been repeatedly mentioned, and it is precisely one of the regenerative new materials currently attracting significant attention in the industry. Originally widely used in orthopedics and dentistry, it is now also shining brightly in the field of medical aesthetics regeneration and is expected to spark a new technological revolution.

Cross-Industry Entry: Another “Dark Horse” Emerges in the Regenerative Medicine Sector

2021 was hailed as the “Year One of Regenerative Aesthetics” in China’s medical aesthetics industry. That year, a number of regenerative products received regulatory approval in China, including Huadong Medicine’s Ellansé (CMC+PCL), Changchun Saint-Bioma’s Sculptra-like filler (PLLA), Imeik’s modified PLLA+HA filler, and Jinbo Bio’s recombinant humanized type III collagen lyophilized fibers. These products achieved rapid commercial success following their approvals.

Figure 1. Seven regenerative products currently approved for marketing in China

Figure 1. Seven regenerative products currently approved for marketing in China

Taking Huadong Medicine’s “Girl Needle” as a key example, its sales revenue reached RMB 1.05 billion in 2023 and continues to exhibit rapid growth. This has undoubtedly provided new insights for the medical aesthetics industry, which is currently facing a growth bottleneck. Consequently, over the past one to two years, a variety of emerging materials have flooded into the field of regenerative medical aesthetics, primarily includingPoly-L-lactic acid (PLLA), Polycaprolactone (PCL), Polydeoxyribonucleotide (PDRN), Polynucleotide (PN)etc. These new materials have already given rise to a range of mature products.

However, exploration has not ceased. This year alone, four regenerative medical aesthetic products have been centrally approved for market launch, and recently, industry attention has gradually shifted toward hydroxyapatite (HAP). As the primary inorganic component of human and animal bones, hydroxyapatite can participate in metabolic processes within the body and promote the repair of defective tissues. Furthermore, due to its certain hardness and strength, it has historically been mainly applied in orthopedic and dental scenarios, with core products including artificial bone preparations, dental implants, and restorative materials.

Figure 2. Mechanism of action after facial injection of hydroxyapatite (Image source: MCU)

But its potential extends far beyond this. Because after subcutaneous injection,Hydroxyapatite can drive the regeneration of type I and type III collagen, elastin, and proteoglycans, while also exhibiting excellent biocompatibility and biodegradability., making it an ideal regenerative material with significant application value in anti-aging, skin tightening, and facial contouring.

Although domestic exploration in this field has only just begun, the United States had already approved the use of hydroxyapatite in medical aesthetics and plastic surgery as early as 2006. For instance, the renowned“Radiesse”, having been launched earlier in Europe and the United States and widely applied in the field of medical aesthetics than PLLA (poly-L-lactic acid/Sculptra) and PCL (polycaprolactone/Ellansé), Radiesse also has a significantly larger number of users globally compared to PLLA and PCL.

There are, of course, reasons for this. In fact, compared with mainstream regenerative products currently on the market, hydroxyapatite is more favorably regarded by industry professionals. ThisOn one hand, this is due to its origin; as the primary inorganic component of human bones and teeth, it exhibits excellent biocompatibility., after injection into the dermis, it can stimulate the rapid generation of collagen and elastic fibers in the skin, thereby achieving skin tightening and lifting effects.

In addition, as a naturally occurring mineral, hydroxyapatite degrades through hydrolysis and osteoclastic enzyme activity, gradually breaking down into calcium ions and phosphate ions.This slow degradation process allows the effects of hydroxyapatite fillers to last for an extended period, typically between 6 and 24 months.. In contrast, the current duration of effect for regenerative materials is approximately 6 to 12 months, whereas hydroxyapatite evidently offers a longer-lasting efficacy.

Another major feature is reflected in the induction method,Hydroxyapatite induces regeneration, which is an active physiological process in the human body, thereby maximizing efficacy while minimizing tissue damage.In response, the founder of a medical aesthetics company remarked, “Most products currently on the market work by stimulating regeneration, which is a passive process rather than an internally driven active one. While this approach may yield short-term efficacy, prolonged use leads to tissue wear and tear, significantly compromising long-term outcomes. In contrast, induced regeneration is an active process that leverages the body’s own endogenous components, which are readily recognized and support cellular adhesion and growth, ultimately leading to tissue formation. This entire process occurs without causing irritation or triggering immune responses, thereby offering superior efficacy and safety.”

"Skirting the Edge" of an IPO: Can It Really Help a Company Stand Out?

It is reported that nearly 200 hydroxyapatite products have been approved in China, but all approved indications are centered around the two major application fields of orthopedics and dentistry.Hydroxyapatite approved for aesthetic medicine indications remains unavailable at this stage.. Nevertheless, the market has moved ahead of the curve; currently, numerous products have already entered circulation in the medical aesthetics sector, with nearly all of them achieving a doubling of their performance in 2024.

This is, in effect, a form of “borderline” conduct, namelyLeverage existing Class III medical device certifications for serious medical applications, extending them into the aesthetic medicine sector to accelerate product market launch.. Specifically, for hydroxyapatite, the product may have originally been approved for orthopedic or dental applications, but it can also gain market approval by expanding its indications to the medical aesthetics field.

For instance, a certain marketed Product A received approval as a Class III medical device as early as 2017, with its indicated use defined as “repair or filling of bone defects caused by various etiologies; repair or augmentation of soft tissues caused by various etiologies, such as orbital implant placement following enucleation or evisceration.” At first glance, this appears to have some relevance to medical aesthetics; however, its indications are primarily centered on orthopedic applications and have no direct connection to facial filling or reconstruction.

The same holds true for marketed Product B, which received its Class III medical device approval in 2015 with indications and intended uses limited to “filling non-load-bearing bone defects,” having no relevance whatsoever to medical aesthetics, facial filling, or restoration. Coincidentally, however, both Products A and B were launched as aesthetic medicine brands at the end of 2021, a year widely regarded as the “Year of Regenerative Aesthetics.” Their keen market insight and strong execution capabilities enabled both products to rapidly garner positive market feedback.

According to industry insiders, as hydroxyapatite continues to expand and explode in the field of medical aesthetic regeneration, nearly ten more hydroxyapatite-based medical aesthetic brands are expected to enter the market over the next two years, following the same logic. So, how long will this period of opportunity last?

This issue must be examined from two dimensions. If the sole objective is to make quick profits, such “gray-area” tactics can clearly achieve that goal, as they allow companies to bypass cumbersome and lengthy approval cycles, rapidly capture market share, and generate profits in a more cost-effective manner. In fact, currently, not only in the field of hydroxyapatite but also in other areas of regenerative medical aesthetics materials, similar “gray-area” practices are prevalent. However, this does not necessarily imply a negative connotation.Even for botulinum toxin, currently the most popular treatment, its approved indications lag behind the scope of its current clinical applications.。

Furthermore, it is undeniable that “edge-ball” marketing can, to a certain extent, facilitate the rapid market adoption and promotion of new materials. For instance, hydroxyapatite has not only gained prominence in the medical aesthetics sector through Products A and B, but also attracted greater interest from enterprises and capital, thereby driving industry development.

Of course,If one wishes to establish the application of hydroxyapatite in the field of regenerative medicine as a sustainable long-term business, regulatory compliance is clearly the only viable path forward.. The logic behind this is not merely that it can be sold in compliance with market regulations; the most fundamental reason lies in its superior efficacy and higher safety profile. This is because it is approved specifically for indicated conditions, allowing for targeted product design, which differs significantly from simply repurposing existing products for medical aesthetic indications.

In fact, this is precisely the significance of the strengthened regulatory oversight in the medical aesthetics sector in recent years. For any new material seeking to enter this field,Compliance remains the critical final step to its ultimate market success.。

The Market Is Eagerly Awaiting the First Compliant Class III Medical Device Certificate

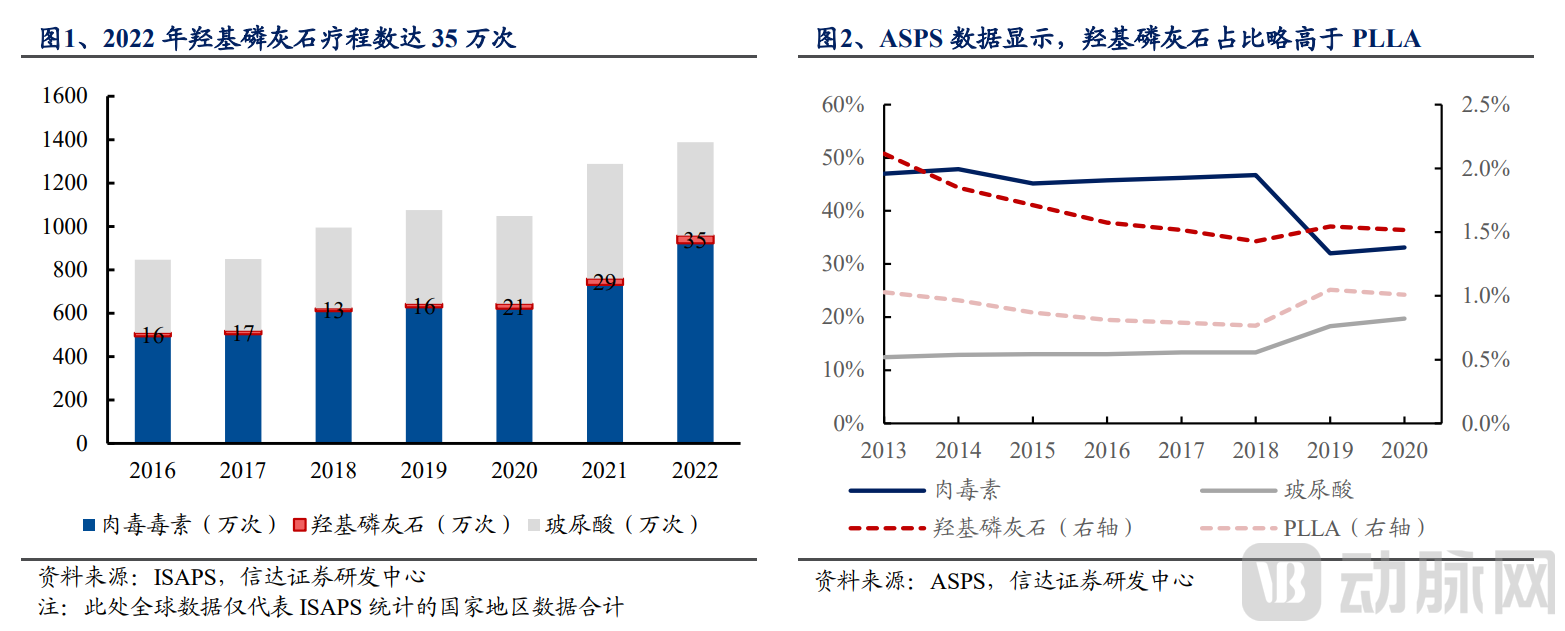

According to ISAPS data, the total number of hydroxyapatite treatment procedures in its surveyed countries and regions reached 350,000 in 2022, a year-on-year increase of 21%. The five-year compound annual growth rate (CAGR) from 2017 to 2022 was 16%, higher than the respective five-year CAGRs of 13% for botulinum toxin and 6% for hyaluronic acid. This indicates that hydroxyapatite possesses greater growth potential. According to a market research report by Bizwit Research & Consulting LLP, the global hydroxyapatite market size was RMB 19.279 billion in 2023,It is projected to reach RMB 26.2 billion by 2029.。

Figure 3. Number of Hydroxyapatite Treatment Sessions and Market Share (Source: Cinda Securities)

This is undoubtedly a huge incremental market. To this end, includingAllergan, Moyang Biology, GeneScience Pharmaceuticals, Haohai Biological Technology, Merz (Germany), Bloomage BiotechNumerous domestic and international companies are actively preparing to compete for the first compliant Class III medical device approval in China for hydroxyapatite-based injectable fillers used in facial soft tissue augmentation within the medical aesthetics sector.

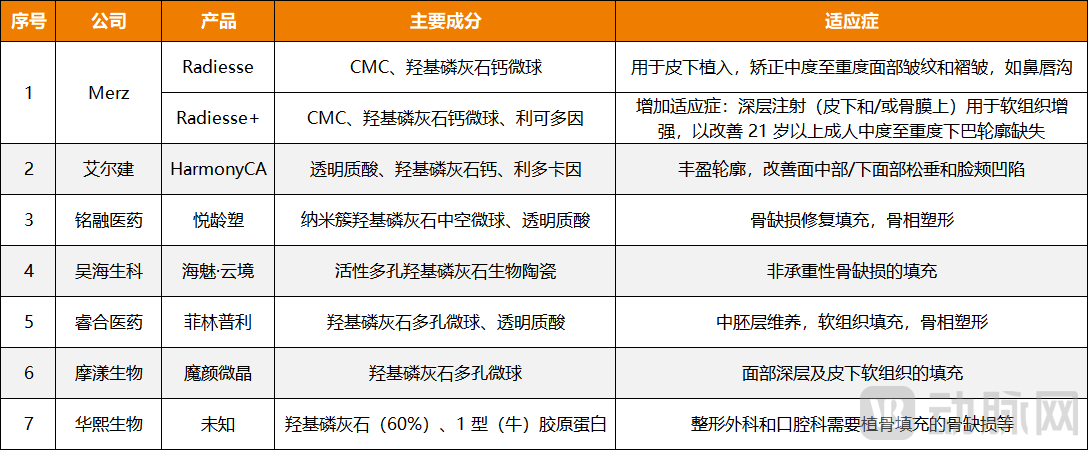

Figure 4. Major Hydroxyapatite Products in the Medical Aesthetics Sector (Source: FDA Official Website, National Medical Products Administration)

Figure 4. Major Hydroxyapatite Products in the Medical Aesthetics Sector (Source: FDA Official Website, National Medical Products Administration)

Taking Merz’s Radiesse as an example, it received FDA approval for market launch in 2006, with indications including the nasolabial folds and jawline contouring. In 2019, Radiesse made its initial attempt to enter the Chinese market, but ultimately failed. In 2023, Radiesse made a comeback, officially launching registered clinical trials in China for the indication of “correcting moderate to severe nasolabial fold wrinkles.” Reportedly, Radiesse has 18 years of clinical history overseas and is considered the pioneering product of calcium hydroxylapatite in the medical aesthetics field.

Next, focus shifts to Allergan’s HArmonyCa. In September this year, it successfully completed registration testing in China and is poised to commence clinical trials. Reportedly, HArmonyCa is a premium dual-action hybrid injectable filler designed to provide immediate volumizing effects while stimulating collagen regeneration. Currently, HArmonyCa is marketed in Europe and other regions, and its FDA clinical trials are underway.

In China, product development is progressing rapidly for Moyang Biotechnology’s core product, “Moyan Microcrystal.” As an injectable calcium hydroxyapatite facial filler, it is particularly suitable for filling deep facial layers and subcutaneous soft tissues, with effects lasting up to 18 months. Currently, this product is in the stage of responding to supplementary requests for registration, positioning it as a strong contender for the first domestic regulatory approval. Additionally, Haohai Biological Technology’s “Hai Mei Yun Jing” has entered clinical trials for a new indication in rhinoplasty, with its market launch imminent.

So, who will ultimately come out on top? It is difficult to draw a definitive conclusion at present, because, in essence,Existing products show no significant gap, with nearly all players still starting from the same baseline.。

To this end, a senior investor in the medical aesthetics sector remarked, “In the current aesthetic medicine market, hydroxyapatite injectable products are predominantly formulated as a combination of 'space-occupying agents' and hydroxyapatite microspheres. Their approved indications are primarily for deep-to-mid-layer injection-based contouring, with a focus on 'bone-like anti-aging.'’; therefore, the differences are not significant. They merely involve varying combinations of dosage, concentration, and microsphere particle size, with more detailed categorization based on applicable anatomical sites and therapeutic effects.Therefore, who will cross the finish line first still depends on the selection of specific indications and the advancement of clinical progress.”

Furthermore, calcium hydroxylapatite (CaHA) has its limitations. For instance, it is not suitable for mild to moderate wrinkles and can only be administered via deep injection. Moreover, unlike hyaluronic acid fillers, which can be dissolved with hyaluronidase if the outcome is unsatisfactory, CaHA cannot be reversed; in cases of suboptimal results or nodule formation, patients must wait for the material to be naturally absorbed and metabolized. This irreversibility represents a significant drawback related to its longevity. Therefore, as companies compete to launch the first compliant product, it is crucial to effectively balance factors such as indication scope, injection techniques, and consumer concerns.

But in any case, an established fact has become increasingly clear:The Market Is Poised to Welcome the Arrival of a New “King”。

1. “Hydroxyapatite Track: The Next Windfall in the Regenerative Field?” – Cinda Securities;

2. “A Subtle Shade of Gray in the Aesthetic Medicine Market: The Dilemma of Hydroxyapatite” — Casual Talk on Medicine and Aesthetics;

3. “Aesthetic Medicine Regenerative Materials Hit the ‘Fast-Forward Button’” — STAR Market Daily