Jinyao Darrentang Completes RMB 494 Million Divestiture of Loss-Making Commercial Segment to Streamline Operations

Zhongxin Pharmaceutical

TCM Research and Development, Manufacturer

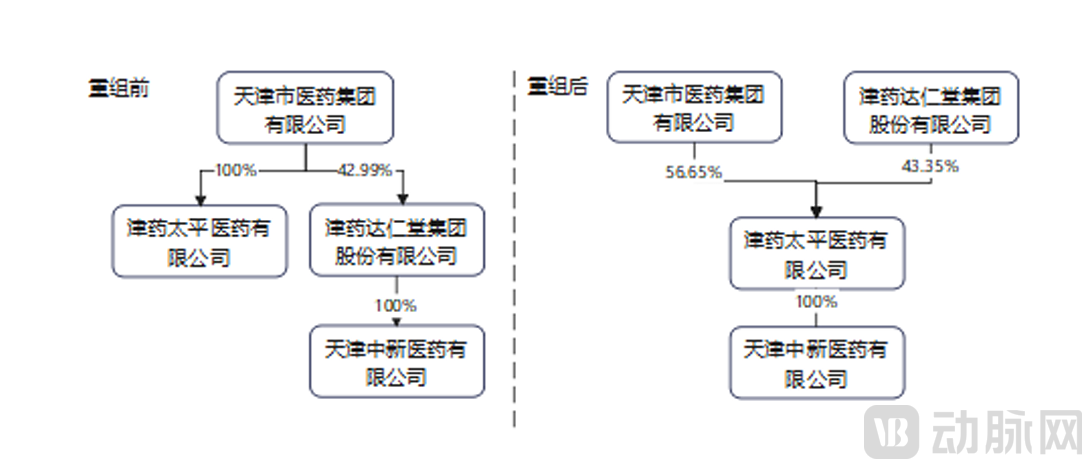

On December 27, Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited issued an announcement stating that it had completed the capital increase in Tianjin Pharmaceutical Holdings Pacific Co., Ltd., which constituted a related-party transaction, with a transaction amount of RMB 493.6177 million.

The transaction involved injecting the entire equity interest of its former wholly-owned subsidiary, Tianjin Zhongxin Pharmaceutical Co., Ltd. (“Zhongxin Pharmaceutical”), into Jin Yao Tai Ping Pharmaceutical Co., Ltd. (“Tai Ping Pharmaceutical”), a wholly-owned subsidiary of the Company’s controlling shareholder, Tianjin Pharmaceutical Group Co., Ltd. (“Tianjin Pharmaceutical Group”), by means of capital increase based on the valuation of such equity interest.

Upon completion of the transaction, Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited and Tianjin Pharmaceutical Holdings will hold 43.35% and 56.65% equity interests in Tianjin Pharmaceutical Holdings Pacific Co., Ltd., respectively; Tianjin Pharmaceutical Holdings Pacific Co., Ltd. will hold 100% equity interest in Tianjin Zhongxin Pharmaceutical Co., Ltd. Therefore, upon completion of this capital increase transaction, Tianjin Zhongxin Pharmaceutical Co., Ltd. will become a wholly-owned subsidiary of Tianjin Pharmaceutical Holdings Pacific Co., Ltd. Tianjin Pharmaceutical Da Ren Tang Group Corporation Limited will no longer hold equity interest in the former but will remain a minority shareholder of both Tianjin Pharmaceutical Holdings Pacific Co., Ltd. and Tianjin Zhongxin Pharmaceutical Co., Ltd.

1Divest the Continuously Loss-Making Pharmaceutical Commercial Segment

In its previous announcement, Zhongxin Pharmaceutical stated that this intra-group asset restructuring transaction was primarily aimed at resolving the issue of horizontal competition between the listed company and its controlling shareholder, thereby enhancing the listed company’s profitability metrics.

The key lies in divesting the loss-making pharmaceutical commercial segment to leverage its economies of scale.

Zhongxin Pharmaceutical’s core business segments comprise pharmaceutical manufacturing and pharmaceutical commerce. The pharmaceutical manufacturing segment, which serves as the primary contributor to profitability, centers on proprietary Chinese medicine producers such as Zhongxin Pharmaceutical, Longshunrong, Leren Tang, Liuzhong Pharmaceutical, and Jingwanhong, supported by ancillary entities including herbal material companies and traditional Chinese medicine decoction piece factories. Its product portfolio spans traditional Chinese medicinal materials, proprietary Chinese medicines, chemical raw materials and formulations, and nutritional health products.

Zhongxin Pharmaceutical boasts a comprehensive product portfolio in the pharmaceutical commerce sector, primarily covering Chinese herbal medicines, processed Chinese herbal slices, proprietary Chinese medicines, chemical raw materials and preparations, biopharmaceuticals, and nutritional health products. Leveraging Tianjin Zhongxin Pharmaceutical Co., Ltd. as its core platform, it manages the distribution of numerous well-known products in the Tianjin region. These include Zhongxin Pharmaceutical’s state-confidential variety Suxiao Jiuxin Wan (Quick-Acting Heart-Saving Pills), state-secret variety Jingwanhong Ointment, TCM-protected variety Zilongjin Tablets, and several varieties with annual sales exceeding RMB 100 million, such as Qingyan Diwan (Throat-Clearing Dropping Pills), Angong Niuhuang Wan, and Qingfei Xiaoyan Wan (Lung-Clearing and Anti-Inflammatory Pills).

The semi-annual report shows that Zhongxin Pharmaceutical’s operating revenue in the first half of 2024 was RMB 3.965 billion, a year-on-year decrease of 3.02%; net profit attributable to shareholders of the parent company was RMB 658 million, a year-on-year decrease of 8.97%; net profit after deducting non-recurring gains and losses was RMB 634 million, a year-on-year decrease of 11.01%; net cash flow from operating activities was RMB 555 million, a year-on-year increase of 353.48%. During the reporting period, basic earnings per share were RMB 0.85, and the weighted average return on equity was 9.49%.

It explicitly states that,The decline in revenue was primarily driven by a year-on-year decrease in income from the commercial segment.— The industrial segment generated RMB 2.62 billion in revenue, a year-on-year increase of 4.25%, while the commercial segment recorded RMB 1.58 billion in revenue, a year-on-year decrease of 14.50%. In fact, the pharmaceutical commercial segment has been operating at a loss for over a year; in 2023, its revenue was RMB 3.724 billion, with a net profit of approximately -RMB 33 million.

The market environment has also been a significant driver behind the challenges faced by its pharmaceutical distribution business, ultimately leading to the decision to divest it.Zhongxin Pharmaceutical stated that the traditional Chinese medicine (TCM) industry is significantly affected by the prices of raw material supplies. Although the year-on-year increase has not been significant in the past year, prices have continued to fluctuate at high levels. In the future, the overall market for TCM materials may continue to experience high-level volatility. Ensuring a stable supply of TCM materials and controlling costs have become operational challenges for the industry in recent years. The Kangmei China TCM Materials Price Index rose from 1,246.17 points in January 2020 to 2,250.73 points in June 2024.

By divesting the low-value pharmaceutical commercial segment that drags down profitability metrics, Zhongxin Pharmaceutical will focus its future financial indicators on the pharmaceutical industrial segment. This strategic shift aims to achieve simultaneous improvements in gross profit margin, net profit, and return-on-assets metrics (such as net profit margin and return on equity), thereby enhancing the company’s cash flow position and accounts receivable turnover efficiency, while significantly reducing bad debt risks associated with the pharmaceutical commercial segment.

Furthermore, the divestiture of its pharmaceutical commercialization business marks a new milestone for Zhongxin Pharmaceutical in continuing its “Three-Year Doubling” plan and accelerating high-quality transformation and development.In 2017, Zhongxin Pharmaceutical, the predecessor of Da Ren Tang, proposed the "Three-Year Doubling" plan, explicitly stating in its annual report: "The company aims to achieve sales revenue exceeding RMB 2 billion for its 11 key flagship products within its major product portfolio, laying a solid foundation for the successful implementation of the 'Three-Year Doubling' plan."

At the shareholders’ meeting, Li Lixin, then Chairman of Zhongxin Pharmaceutical, provided further clarification on the “Three-Year Doubling” initiative: “Operating revenue will grow from RMB 6 billion to RMB 12 billion; net profit will increase from RMB 360 million to RMB 720 million.” Later, the company’s securities affairs representative further confirmed these figures, specifying that they applied exclusively to “revenue from self-operated products within the pharmaceutical manufacturing segment.”

Therefore, Zhongxin Pharmaceutical has proposed a "Product is King" strategy targeting its portfolio of 599 drug approval numbers (including 122 exclusive products), focusing on the "Three Cores and Nine Wings" framework. The "Three Cores" are: establishing Suxiao Jiuxin Wan as the flagship product to build the leading brand for cardiovascular and cerebrovascular medicines in Tianjin; positioning Jingwanhong Ointment as the core product to create the leading brand for wound repair; and leveraging the century-old time-honored brand "Zhongxin Pharmaceutical" to carry premium traditional Chinese medicines, thereby entering the health and wellness sector. The "Nine Wings" refer to promoting the development of specialized product lines in respiratory, digestive, rheumatic and bone pain, urological, women's and children's health, and oncology categories.

Since 2020, Tianjin Pharmaceutical Group has undertaken mixed-ownership reform of state-owned enterprises, which was completed in March 2021. The group has smoothly navigated the subsequent transition period, achieving new highs in industrial marketing sales, pharmaceutical company sales, net profit, and the total market capitalization of its listed companies. Sales of major flagship products under its portfolio, such as Suxiao Jiuxin Wan (Quick-Acting Heart-Saving Pills), have also reached breakthrough levels. Statistics show that Zhongxin Pharmaceutical recorded a compound annual growth rate (CAGR) of 7.58% in total operating revenue and 14.25% in net profit over the past three years.

However, Zhongxin Pharmaceutical delivered mediocre performance in its 2024 semi-annual report. On one hand, as previously mentioned, revenue from the pharmaceutical commercial sector declined; although the pharmaceutical industrial segment achieved a 4.25% growth, it still fell short of the original target of 18%. On the other hand, the company’s self-operated net profit for the first half of this year amounted to RMB 530 million, representing a year-on-year increase of 2%. Nevertheless, due to a decline in investment income, the overall net profit attributable to shareholders of the parent company decreased, dropping by 8.97% year on year.

On September 27, Zhongxin Pharmaceutical announced that the company and its controlling shareholder, Tianjin Pharmaceutical, intend to transfer their respective 13% and 20% stakes in Sino-American SmithKline (SAS) to Haleon (China), with transaction prices of RMB 1.759 billion and RMB 2.706 billion, respectively.Based on a transaction price of RMB 1.759 billion, the estimated impact on the Company’s investment income for the current period is approximately RMB 1.7 billion, and the net profit after income tax for the fiscal year in which the transaction occurs is expected to increase by approximately RMB 1.44 billion.

Sino-American SmithKline (SAS), established in 1987, is jointly held by the multinational pharmaceutical company GlaxoSmithKline, Zhongxin Pharmaceutical, and Tianjin Pharmaceutical Group, with Zhongxin Pharmaceutical holding a 25% stake. The company’s main products include New Contac, Fenbid, Panadol, Tagamet, and Stomil. Affected by the high base resulting from significant performance growth in 2023, SAS’s net profit declined to RMB 421 million in 2024, leading to a year-on-year decrease of RMB 74 million in investment income for Zhongxin Pharmaceutical.

Overall, from exiting low-value pharmaceutical commercial businesses to gradually withdrawing from the OTC and consumer healthcare sectors, Zhongxin Pharmaceutical has consistently pursued “quality improvement, efficiency enhancement, and strengthened returns” by divesting non-core subsidiaries, thereby refocusing on its core traditional Chinese medicine (TCM) business and promoting steady growth in its pharmaceutical industrial performance.

2Resolving Horizontal Competition and Integrating the Commercial Logistics Segment

After Zhongxin Pharmaceutical no longer holds a controlling stake in Tianjin Zhongxin Pharmaceutical Co., Ltd., the issue of horizontal competition between it and its major shareholder, Tianjin Pharmaceutical Group, will be resolved.

One of the key players in this transaction is Taiping Pharmaceutical, formerly known as Tianjin Pharmaceutical Company. After several rounds of restructuring, it is now a wholly-owned subsidiary of Tianjin Pharmaceutical Group and serves as the leading enterprise within the group’s modern pharmaceutical commercial logistics segment. Reportedly, Taiping Pharmaceutical is the largest pharmaceutical commercial enterprise under the Tianjin State-owned Assets Supervision and Administration Commission (SASAC) system. Its business scope mainly includes traditional Chinese medicine patent drugs, chemical raw materials and their preparations, antibiotics, biochemical drugs, biological products, diagnostic agents, and narcotic drugs. Zhongxin Pharmaceutical, on the other hand, operates as the pharmaceutical commercial logistics arm of Zhongxin Pharmaceutical (Da Ren Tang).

Through this internal transaction, the direct controlling equity of Tianjin Zhongxin Pharmaceutical Co., Ltd. will be transferred to Tianjin Pharmaceutical Holdings Pacific Co.,Ltd., achieving integration of resource channels under the same group structure.

In fact, mergers and acquisitions among traditional Chinese medicine (TCM) enterprises have been ongoing in recent years. As a result, 2024 has become a pivotal year for internal structural adjustments aimed at resolving horizontal competition issues.On November 21, China Resources Sanjiu announced that it had entered into an equity transfer agreement with Kunming Pharmaceutical Group, pursuant to which it will sell its 51% stake in Kunming CR Shenghuo Pharmaceutical Co., Ltd. to Kunming Pharmaceutical Group. This restructuring will resolve the horizontal competition between CR Shenghuo and Kunming Pharmaceutical regarding their Xuesaitong soft capsule products, thereby achieving integration of the Panax notoginseng industrial chain and consolidating the market for the flagship Xuesaitong product.

Through internal integration, the pharmaceutical group aims to fully leverage its advantages in products, sales and distribution networks, branding, and supply chain management, with the primary objective of enhancing operational efficiency and boosting revenue returns. The underlying rationale is that, after experiencing rapid growth following mixed-ownership reform, “time-honored brands” have entered a challenging phase characterized by rising prices for traditional Chinese medicinal materials, slowing revenue growth, and limited innovation within their industrial systems.

Is it about exploring the next growth point? Or returning to the continuous deep cultivation of the core traditional Chinese medicine business? This is the choice at hand.

References:

E-Drug Manager - Prominent TCM Leader Divests Business! After Building a Blockbuster Drug Worth RMB 2 Billion, It Chooses to Stay Focused

VCBeat – Nearly 500 Million: Well-Known TCM Enterprise Divests Commercial Segment