2024 China Innovative Drug & Supply Chain White Paper: Record-Breaking Year as License-Out Upfront Payments Surpass R&D Financing for the First Time

2024: China’s Biopharmaceutical Industry Enters a Recovery Phase of Bottoming Out and Rebounding. Although capital remains cautious and IPOs continue to tighten, the warm sun has pierced through the winter chill, spreading its warmth!

The development of antibody-drug conjugates (ADCs) and bispecific/multispecific antibodies is undoubtedly one of the hottest topics in current pharmaceutical innovation. Although the key to developing highly efficacious and low-toxicity new drugs lies within infinite permutations and combinations, rational design strategies honed by historical experience have significantly accelerated this process. Before the next blockbuster drug emerges, China’s pharmaceutical industry has already made a significant impact through its robust engineering-driven innovation capabilities and high efficiency.

2024 was a special year. In this year,Chinese Innovative Drug Companies' License-Out Deal Amounts and Number of Transactions Hit New Highs, with Total Upfront Payments($3.16 billion)Exceeded Innovative Drug R&D Financing in the First Year($2.71 billion)!Multiple Deals Feature Massive Upfront Payments “Rivaling IPOs.” Not Only Are MNCs Actively Pursuing Acquisitions, but Domestic Innovative Drug Companies Are Also Aggressively Acquiring Innovative Assets,20% Innovative Drug AssetsMergers and AcquisitionsTransaction Amount Accounts for Half of the Trillion-Yuan Total Transaction Volume!Meanwhile, NewCo has surged in popularity, with six consecutive transactions involving a total sum exceeding $8 billion.

Where Does China’s Biotech Sector Stand at This Stage? Perhaps Source Innovation Is Not the Best Answer; Truly Addressing Unmet Clinical Needs and Delivering Compelling Clinical Data Are.

A Review of 2024: Cumulative Developments in China’s Innovative Drug and Supply Chain Sectors from January to OctoberOver 300 financing deals, more than 200 business development (BD) transactions, the issuance of over 200 national policies, and clinical pipeline advancements in nearly 100 products within hot sectors are worthy of attention.To gain insights into industry developments and grasp future trends, VBInsight, in collaboration with over 10 investment institutions and biotech founders, has conducted a detailed review and analysis of the year’s hotspot events for the benefit of the industry.

CHAPTER 1. 2024 in Numbers: Hitting Bottom and Rebounding, the Industry is Accelerating its Recovery

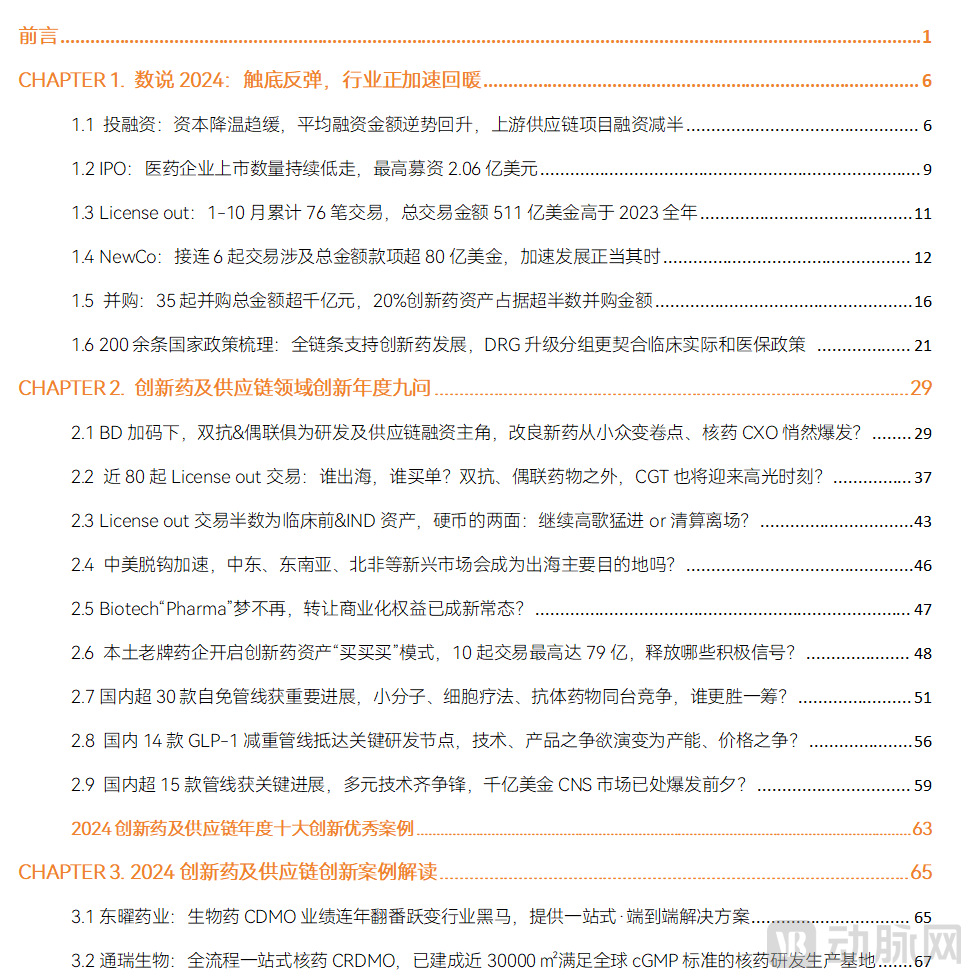

The cooling trend in primary market investment and financing has slowed, with the average financing amount rising against the tide to 2022 levels. According to incomplete statistics from VBInsight, the total financing amount in China’s innovative drug and supply chain sectors from January to October 2024 reached $4.206 billion, approximately two-thirds of the 2023 total ($6.159 billion).

Figure 1. Overview of Total Financing Amount and Number of Financing Events in China’s Innovative Drug and Supply Chain Sectors, 2020–2024

Data Source: VBInsight

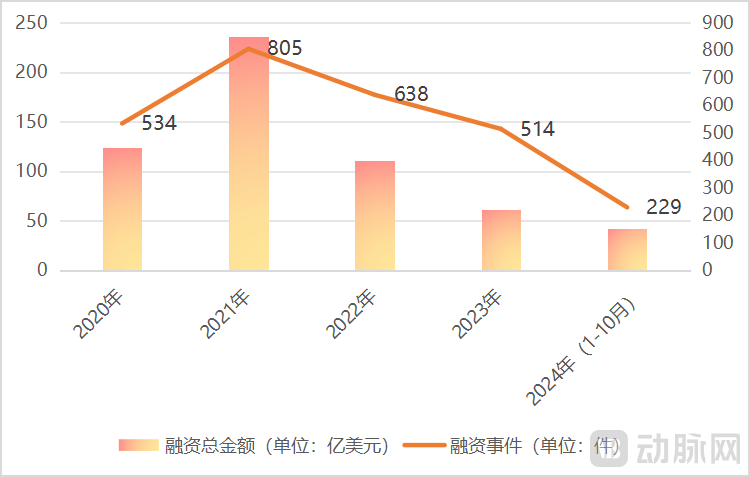

In terms of the average financing amount and the number of financing events,From January to October 2024, there were 229 financing events in China’s innovative drug and supply chain sectors, with an average financing amount of $18 million, surpassing the sector’s average financing level in 2022.

Figure 2 Overview of Average Financing Amounts and Number of Financing Events in China’s Innovative Drug and Supply Chain Sectors, 2020–2024

Data Source: VBInsight

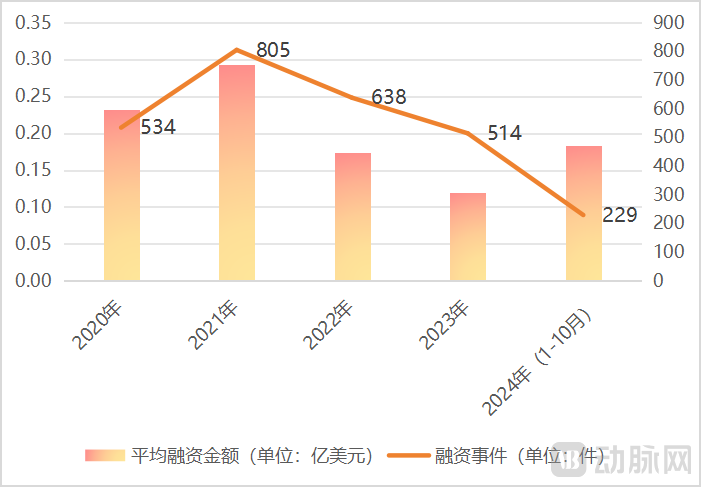

Compared with 2023, the total financing amount for the innovative drug supply chain dropped sharply in 2024. According to incomplete statistics from VBInsight,From January to October 2024, financing in the innovative drug supply chain amounted to RMB 8.99 billion, approximately half of the RMB 19.43 billion raised for innovative drug R&D during the same period.In 2023, the total financing amount related to the innovative drug supply chain reached RMB 30.14 billion, which was not significantly different from the RMB 36.33 billion raised for innovative drug R&D during the same period.

Figure 3: Overall Performance of Investment and Financing in R&D and Supply Chain of Domestic Innovative Drugs in China from January to October 2024

Data source: VBInsight

From January to October 2024, there were 77 financing events related to the innovative drug supply chain, with an average financing amount of RMB 117 million. During the same period, there were 150 financing events related to innovative drug R&D, with an average financing amount of RMB 130 million.

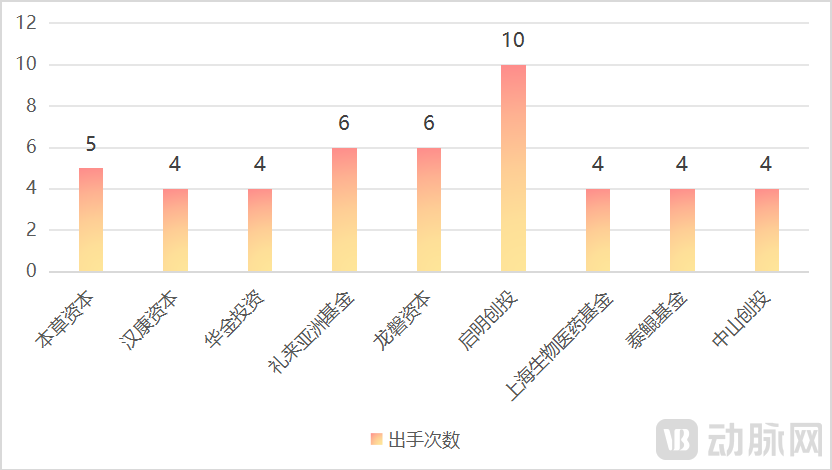

From January to October 2024, the top 10 most active investment institutions in the innovative drug and supply chain sectors were Qiming Venture Partners, Lilly Asia Ventures, Longpan Capital, Bencao Capital, Hankang Capital, Huajin Investment, Shanghai Biomedical Industry Fund, Taikun Fund, and Zhongshan Venture Capital.

Figure 4: Top 10 Investment Institutions by Number of Deals in Domestic Innovative Drugs and Supply Chain Investments, 2024

Source: VBInsight

VBInsight has conducted a non-exhaustive review of the projects invested in by the top three most active investment firms in 2024, for industry reference.

Figure 5: Projects Invested by the Top 3 Institutions with the Highest Number of Deals in Innovative Drugs and Supply Chain Investments, 2024

Source: VBInsight

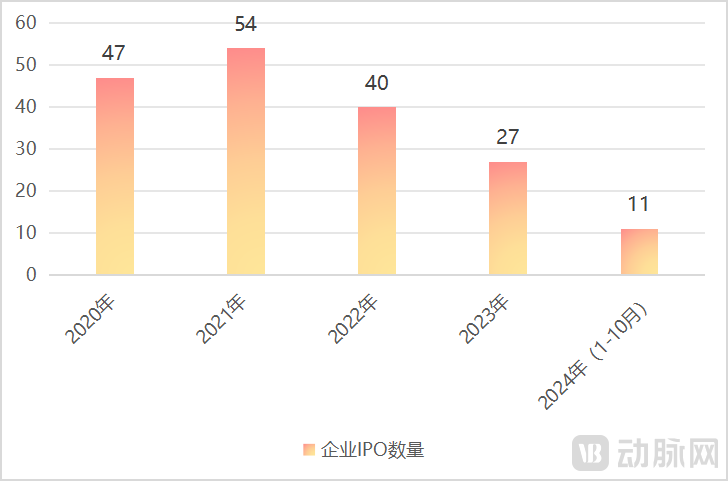

The number of IPOs for innovative drugs and supply chains hit a record low in 2024. According to incomplete statistics from VBInsight,From January to October 2024, there were only 11 initial public offerings (IPOs) in the innovative drug and supply chain sectors, including 6 IPOs related to innovative drug R&D and 5 IPOs related to the innovative drug supply chain.

Figure 6 Changes in the Number of IPOs in the Innovative Drugs and Supply Chain Sector, 2020–2024

Data Source: VBInsight

Among them, only one pharmaceutical company raised over RMB 1 billion in public offerings: Kangpei Biotech, which raised USD 206 million, marking the largest biotechnology IPO in China for the year. According to public information, Kangpei Biotech specializes in the development of new drugs for medical aesthetic injections and diseases related to fat metabolism. Its two independently developed novel drugs—the oral weight-loss drug CBW-511 and the local lipolytic injection CBL-514—have entered clinical trials. In October 2024, the company announced the completion of Phase 2b clinical trials of CBL-514 for local fat reduction, with unblinding results expected in the first quarter of 2025.

Figure 7 Overview of Domestic IPOs in the Innovative Drug and Supply Chain Sectors from January to October 2024

Source: VBInsight

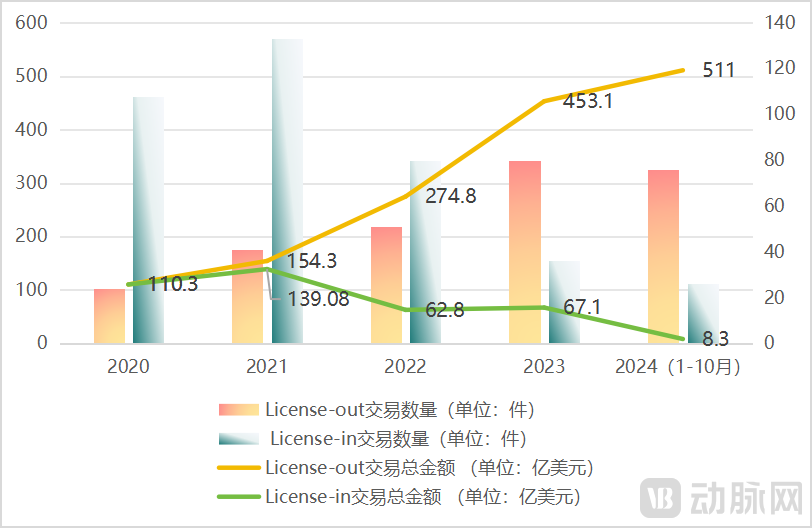

In 2024, according to incomplete statistics from VBInsight,A total of 76 license-out transactions occurred in China’s innovative drug sector, three times the number of license-in transactions (26) during the same period.

Figure 8 Overview of License-In/Out Transactions in the Past Five Years

Data Source: MedPartner, VBInsight

In terms of transaction amount,From January to October 2024, the total upfront payments for license-out transactions amounted to approximately $3.16 billion, with the total transaction value reaching $51.1 billion, surpassing the full-year total for license-out transactions in 2023.

It is quite thought-provoking that, from January to October 2024Upfront Payment Amount for License-Out Transactions($3.16 billion)has already exceeded the total amount of financing for innovative drug R&D during the same period(19.43 billion yuan, approximately 2.71 billion US dollars).

The fervor surrounding NewCo transactions needs no elaboration. According to incomplete statistics from VBInsight,From January to November 2024, a total of six NewCo transactions occurred, involving a total transaction amount of $8.23 billion and total upfront payments of approximately $200 million.

Figure 9 Overview of NewCo Transactions in 2024

Data source: Public reports, VBInsight

Current Market StageHotter NewCo pipelines include autoimmune-related drugs, metabolic disease drugs, and TCE bispecific/multispecific antibodies.According to industry insiders, subsequent NewCo transactions involving domestically produced ADC products will be disclosed in due course, and some frontier fields, including CGT, are also exploring the possibility of establishing NewCos.

From the perspective of the clinical stage of NewCo's transaction assets,Preclinical IND to Phase I/IIa trials dominate the deal flow.

Currently, whether multinational corporations (MNCs), U.S. dollar funds, or domestic funds and local pharmaceutical companies, are all actively exploring the potential for developing NewCo transactions. Some investors have pointed out that,NewCo is highly likely to become one of the predominant models for Sino-foreign collaborations in recent years.

Dr. Liu Dan, Managing Partner at Pivotal bioVenture, pointed out that three dimensional factors are driving this trend: Unlike conventional asset divestitures, the NewCo model ultimately yields a new entity with strong overseas characteristics—a purely foreign company primarily operating in the U.S. market. This provides an acceptable framework for pharmaceutical collaboration between China and the United States, particularly against the backdrop of multifaceted U.S. restrictions on China’s biopharmaceutical industry.

Secondly, the fund investors introduced in the NewCo partnership model are predominantly institutions characterized by “high reputation, strong professionalism, and deep resources.” These entities are highly adept at managing complex transactions and can provide substantial support in empowering the new company’s management as well as facilitating subsequent financing rounds.

Finally, new companies established under the NewCo model will have greater opportunities for survival and more strategic options if they secure substantial financing. For instance, they can acquire new pipeline assets to balance operational risks and returns; leveraging the extensive experience and resources of investors and the management team, they can develop more mature and actionable exit strategies.

In mature markets such as Europe and the United States, mergers and acquisitions are the primary channel for corporate capitalization.

Amid tighter domestic IPO regulations and supportive policies for mergers and acquisitions (M&A)—such as the successive introduction of the “Nine National Guidelines” and the “Six M&A Measures”—M&A has gradually become the preferred exit route alongside IPOs.

Additionally, central state-owned enterprises and state-owned assets are also exerting efforts, with multiple M&A funds already established.Recently, the Shanghai Municipal Government announced the establishment of a RMB 10 billion M&A fund for the biopharmaceutical industry, aiming to complete a number of representative merger and acquisition deals by 2027.

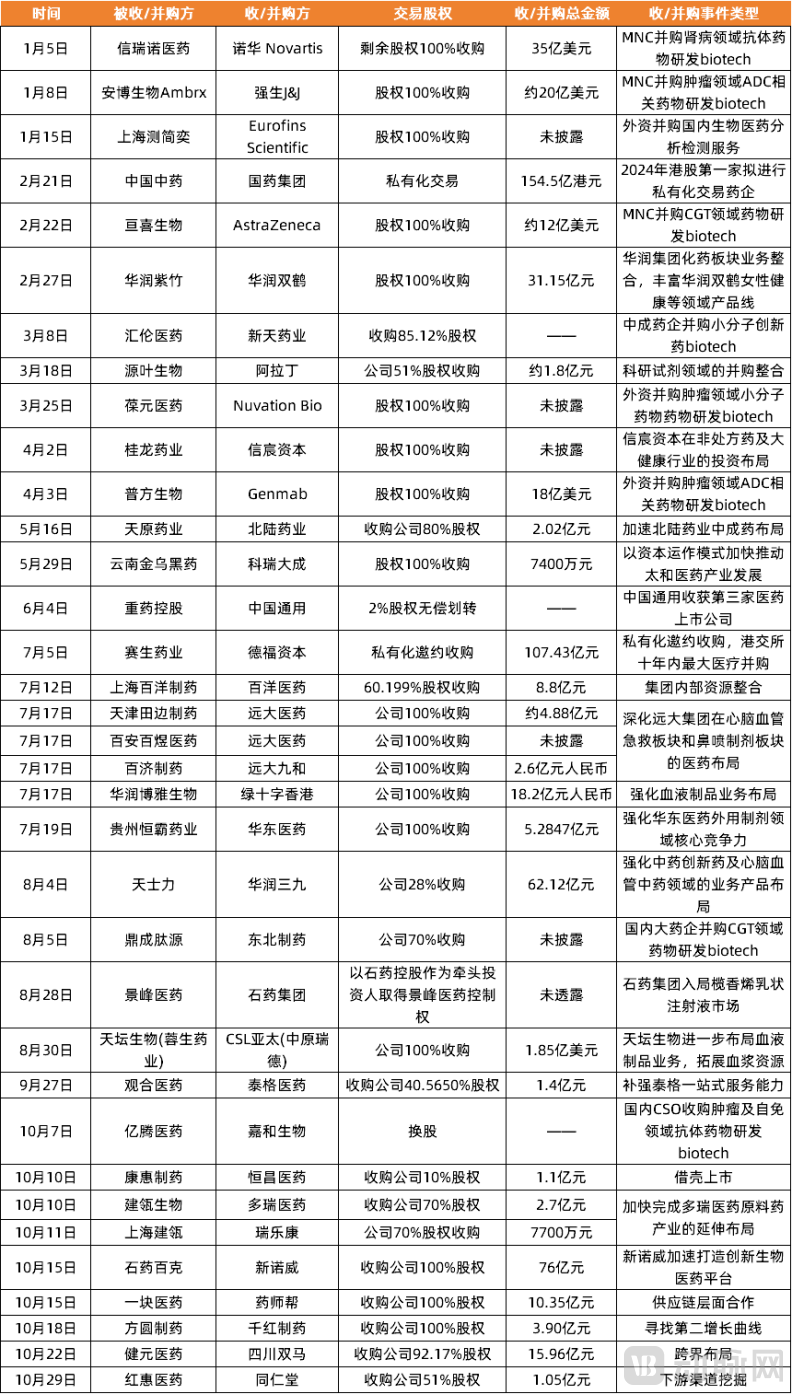

A total of 35 M&A transactions in China's pharmaceutical industry involved a cumulative transaction value exceeding RMB 100 billion (RMB 112.58 billion).

Figure 10 Overview of M&A Transactions in the Pharmaceutical Sector in 2024

Source: VBInsight

It can be clearly observed that,Mergers and acquisitions are predominantly characterized by absorption and integration across the industrial chain.

Notably, the trend of acquisitions involving innovative drug assets became pronounced in 2024—Of the 35 M&A transactions, 10 involved acquisitions of innovative biotech companies. Six deals (19.4%) disclosed transaction amounts, totaling RMB 68.82 billion, which accounted for 61.1% of the total value of all 31 M&A transactions with disclosed amounts.In other words, the acquisition of innovative drug assets, accounting for 20% of the total, represented over half of the total M&A value.

Large multinational pharmaceutical companies are the primary drivers of M&A activity for innovative biotech firms.Six M&A deals of innovative drug biotech assets led by large multinational pharmaceutical companies involved a total amount of RMB 61.03 billion, accounting for 88.7% of the total disclosed M&A value.M&A deals for innovative drug biotech assets led by state-owned pharmaceutical enterprises involve relatively small transaction amounts.

Figure 11 Transactions Involving the Acquisition of Innovative Drug Biotech Assets in 2024

Data source: VBInsight

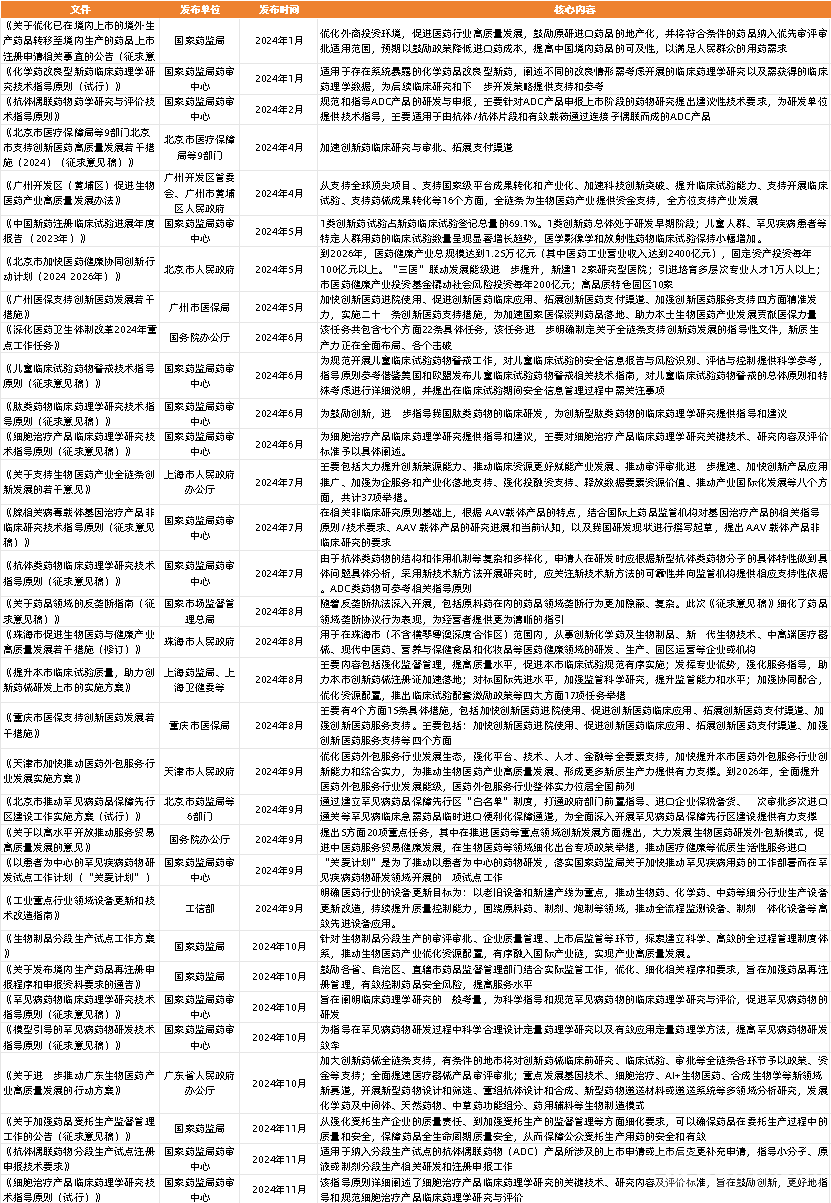

According to incomplete statistics from VBInsight,As of the end of November 2024, more than 200 national-level policies related to the pharmaceutical industry were issued in China, while nearly 1,000 relevant policies were released at the provincial level. VBInsight has selected key policies for systematic review and interpretation.

Figure 12 Overview of Key National Policies in the Biopharmaceutical Sector in 2023

Data Source: Collected and compiled from public news channels, VBInsight

Including:

1. At the national level, the 2024 Government Work Report released in March has charted the course for the long-term development of the biopharmaceutical industry, laying out detailed arrangements and strategic plans across multiple dimensions, including overall industrial development, coordinated reform of healthcare, medical insurance, and pharmaceutical sectors (the “Three Medical Linkages”), R&D innovation, intellectual property protection, and investment.

2. Policies supporting the innovative drug development across the entire value chain are being progressively implemented from the national level to local jurisdictions, thereby promoting high-quality development of the biopharmaceutical industry.

3. The pilot program for segmented manufacturing will have a positive impact on the entire industry chain, including improving the R&D efficiency and market supply capacity of innovative drugs, increasing demand for CRO and CDMO services, and enhancing the supply security capability for biological products.

4. Continued attention and focused support for pediatric drugs and orphan drugs.

5. In terms of medical insurance, the Diagnosis-Related Group (DRG) payment grouping scheme has been upgraded to version 2.0, with groupings that better align with clinical practice and the direction of medical insurance policies.

6. In popular niche sectors such as chemically modified new drugs, antibody-drug conjugates (ADCs), peptide-based therapeutics, and cell and gene therapy (CGT), the government has formulated multiple policies to promote and regulate industry development.

CHAPTER 2. Nine Key Questions on Innovation in Innovative Drugs and the Supply Chain Sector

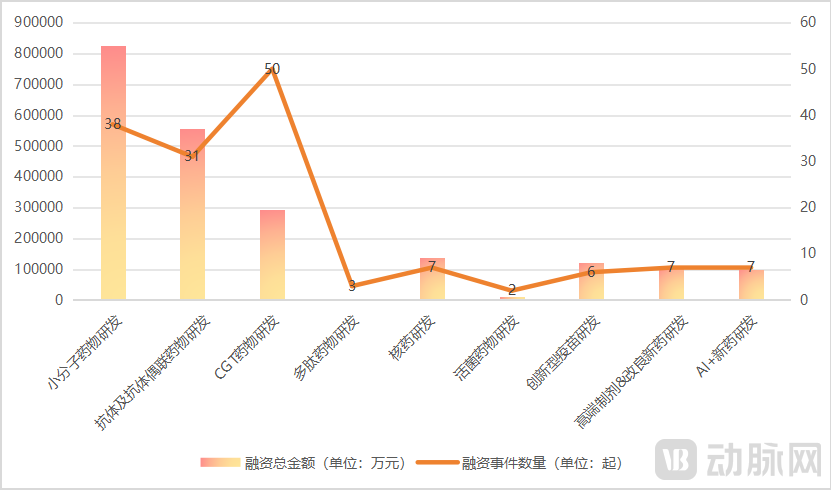

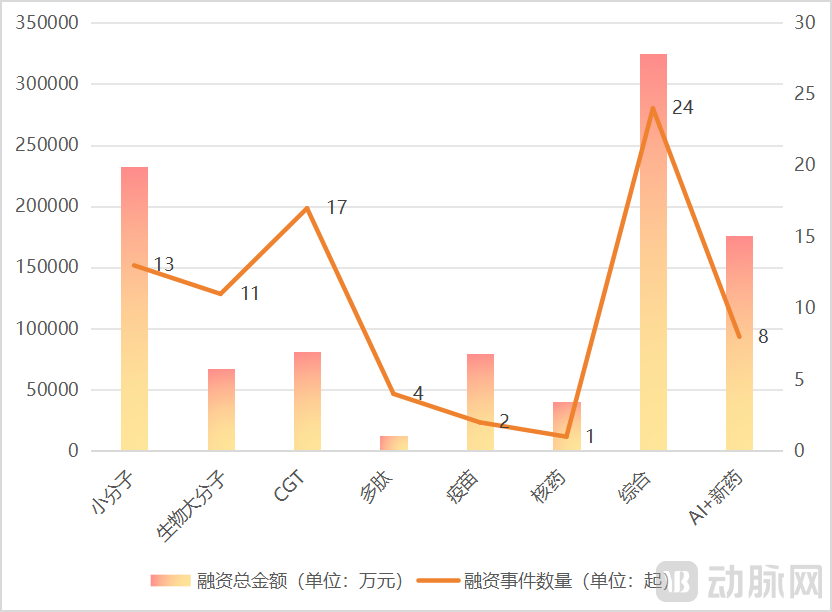

Continuing the 2023 financing trend, January–October 2014 in the innovative drug R&D sectorThe sectors attracting the most capital remain the relatively mature and stable fields of small-molecule drugs (RMB 8.251 billion) and antibody and antibody-drug conjugate (ADC) R&D (RMB 5.577 billion).

Figure 14 Total Financing Amount and Number of Financing Deals in Various Sub-sectors of Innovative Drug R&D, January–October 2024

Data Source: VBInsight

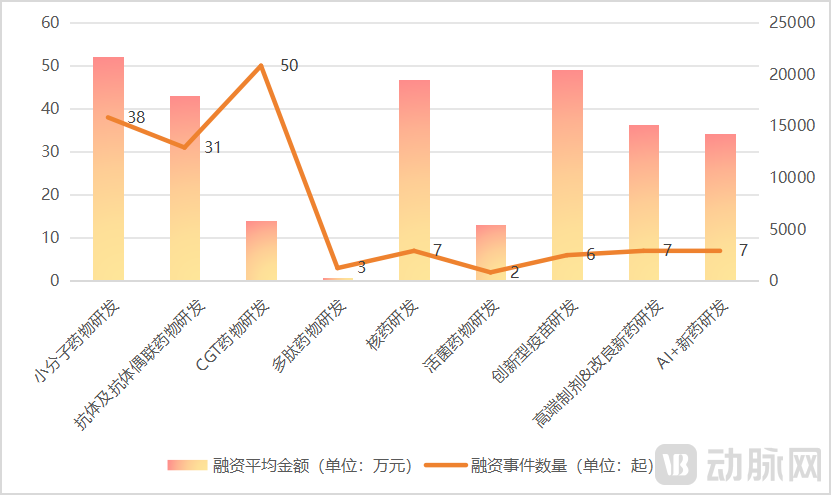

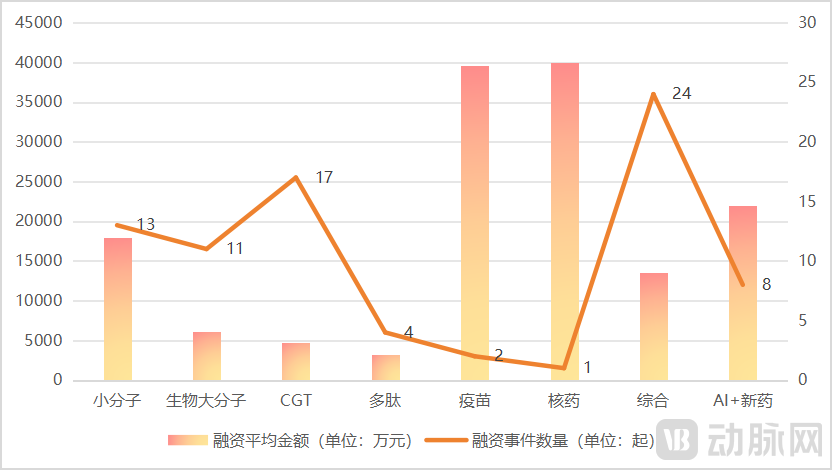

In terms of average financing amount, except for the fields of small-molecule drugs and antibodies and antibody-drug conjugates,RadiopharmaceuticalsThe sector continues to demonstrate strong capital-attracting capabilities: seven financing deals totaled RMB 1.364 billion, with an average financing amount of RMB 195 million.Innovative VaccinesThe sector has seen a total of six financing rounds, raising RMB 1.23 billion.

Figure 15 Average Financing Amount by Sub-sector in Innovative Drug R&D, January–October 2024

Data Source: VBInsight

It is also worth noting thatHigh-End Formulations & Improved New DrugsR&D Track. There were seven related financing events, with a total funding amount of RMB 1.06 billion. Dr. Liu Fei, founder of Minovate Pharmaceuticals, pointed out that Class II improved new drugs were once a very niche segment in China, but in recent years, a large number of companies have entered this field. While the market for me-too generic drugs was highly saturated in previous years, the current moment presents a favorable entry point.

Furthermore,Class 3 drugs and high-barrier Class 4 generic drugs also harbor significant opportunities. The combined development model of 2.2+2.4 may also represent a future pathway for growth.

The top 20 financings in the innovative drug R&D sector broadly reveal capital’s investment preferences in 2024.

Figure 16 Top 20 Financings in the Innovative Drug R&D Sector, January–October 2024

Source: VBInsight

Bispecific Antibodies and Conjugated DrugsThe fervor in business development has also extended to financing; from January to October 2024, financing in the innovative drug R&D sectorAmong the Top 20, six companies are engaged in the R&D of bispecific antibodies and antibody-drug conjugates, with a total financing amount of RMB 3.579 billion.

Figure 17 Financing Distribution of the Top 20 Innovative Drug R&D Projects (Financing Amount in CNY 100 Million)

Data source: VBInsight

Small-Molecule Drug Field, PROTACs, etc.Innovative technological pathways, accompanied by breakthroughs in international clinical trials, have gained favor with investors.CGT field,With de-risked druggability, significant room for indication expansion, and clear administration advantagesSmall Nucleic Acid DrugsRemains a key focus of capital attention.Vaccine Sector,As an “additive” that enables vaccines to more effectively elicit the body’s immune response, adjuvantsNovel Vaccine AdjuvantsGarnering market attention and leading new trends in vaccine research and development.

Supply Chain:Comprehensive supply chain enterprises secured the highest number of financing deals, totaling 24, with a cumulative amount of RMB 3.249 billion. Three companies completed initial public offerings (IPOs), including XtalPi, a technology company driving innovative drug discovery through computation; Taimei Medical, which provides digital operational services for pharmaceutical R&D, pharmacovigilance, pharmaceutical marketing, and market access; and Fangzhou Jianke, which focuses on advancing internet-based chronic disease management services.

Other supply chain enterprises that have secured substantial financing in the primary market include DTiPharma, which provides drug delivery technology services for small-molecule and nucleic acid therapeutics; InnoStar Bio, which offers preclinical safety assessment studies to pharmaceutical companies; and Xinji Pharma, a comprehensive provider of pharmaceutical R&D services.

Figure 18 Total Financing Amount and Number of Financing Deals in Subsectors of the Innovative Drug Supply Chain, January–October 2024

Data source: VBInsight

Secondly, supply chain enterprises that provide services/products for small-molecule drug R&DA significant number of financing rounds (13) were completed, with total funding reaching RMB 2.328 billion; among them, Haisheng Pharmaceutical, engaged in the R&D and production of human and veterinary active pharmaceutical ingredients (APIs) and intermediates, achieved an initial public offering (IPO).

The listing of XtalPi and the $100 million financing round secured by DTAI Pharma have significantly boosted fundraising performance in the AI-driven new drug supply chain sector. From January to October 2024, eight financing deals in this sector raised a total of RMB 1.758 billion.

Figure 19: Average Financing Performance in Sub-segments of the Innovative Drug Supply Chain, January–October 2024

Source: VBInsight

In terms of average financing amount, the nuclear medicine and innovative vaccine supply chain sectors have shown outstanding performance.In March 2024, MiDu Bio, a CRDMO service provider for radiopharmaceuticals, completed a financing round of nearly RMB 400 million. Recently, TongRui Bio also secured a substantial Series A+ financing round exceeding USD 100 million in November.

Amid the capital winter, the strong fundraising appeal of nuclear medicine CRDMO service providers may be attributed to two factors: the industrial development background and the companies’ own competitive advantages.

On one hand, the booming development of radiopharmaceuticals has propelled the growth of the radiopharmaceutical R&D supply chain.

On the other hand,Companies such as Tongrui BiopharmaProviding one-stop CRDMO services for radiopharmaceuticals, spanning from early-stage R&D to commercial-scale manufacturing and including downstream logistics and distribution, this model aligns perfectly with the strong CXO demands of numerous radiopharmaceutical developers, particularly given the capital-intensive nature of the industry and the current climate of tightened investment.Furthermore, in the non-radiopharmaceutical sector, radiopharmaceutical CXOs can also provide molecular imaging CRO and companion diagnostic development services to conventional pharmaceutical companies, as well as validation services for assessing the druggability of new drugs targeting innovative targets.

Overall, the cooling of the capital market in the innovative drug R&D sector has directly impacted the supply chain industry. Financing for the innovative drug supply chain in 2024 saw a significant decline compared to 2023, with only 14 financing deals exceeding RMB 100 million recorded from January to October.

Figure 20: Top 20 Financings in the Innovative Drug Supply Chain Sector, January–October 2024

Data source: VBInsight

Notably, the situation of CXOs in certain segments of the secondary market differs significantly from that in the primary market. Taking biologics CXOs as an example, the boom and vigorous R&D activity in antibody-drug conjugate (ADC) projects have directly translated into growth for the CXO service industry. According to incomplete statistics from VBInsight, listed CDMOs that were among the first to enter this field, such as WuXi XDC, TopAlliance Biosciences, and Haoyuan Chemexpress, have all achieved rapid performance growth in their corresponding business segments in recent years, sending positive signals.

WuXi XDC, the leading contract research, development and manufacturing organization (CRDMO) for antibody-drug conjugates (ADCs), reported a 67.6% year-on-year increase in revenue for the first half of 2024, reaching RMB 1.665 billion; its net profit surged by 175.5% year-on-year to RMB 488 million. Allergan Pharmaceuticals (Suzhou) Co., Ltd. (TopAlliance Biosciences) recorded CDMO/CMO business revenue of RMB 140 million in 2023, representing a 94% year-on-year growth. In the first half of 2024, the company’s CDMO/CMO revenue reached RMB 114 million, up 144% year-on-year, while net profit amounted to RMB 31.56 million, marking a turnaround from loss to profit and establishing it as a dark horse in the biologics CDMO market.

The frequent out-licensing of projects by innovative biotech companies to overseas markets signifies that the R&D capabilities of domestic innovative pharmaceutical enterprises have gained recognition from foreign pharmaceutical companies, making Chinese innovative drug assets a crucial source for multinational pharmaceutical corporations to sustain their innovation capacity.

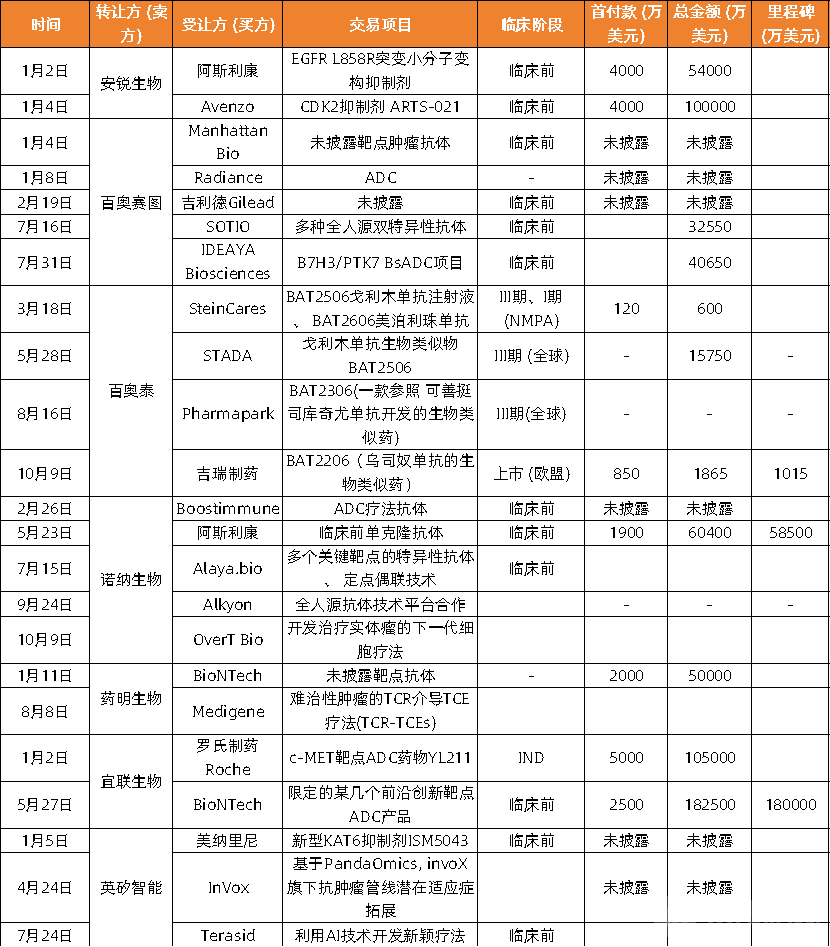

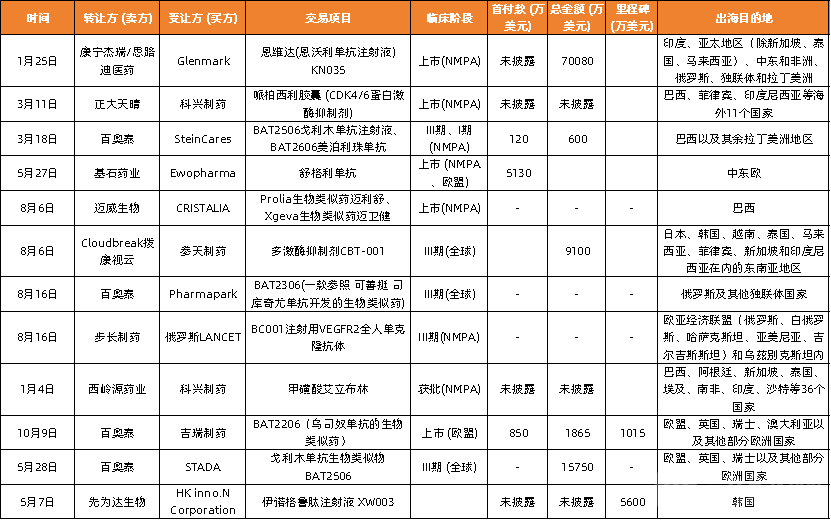

From the perspective of buyers in license-out deals, multinational corporations (MNCs) are undoubtedly the main players.According to VBInsight statistics, the total value of 24 related transactions involving MNCs accounted for 55.4% of the total value of License-out transactions;The upfront payment amount for the relevant transactions accounted for 71.5% of the total upfront payments for all License-out transactions.

Figure 21 License-out Deals Involving Chinese Innovative Pharmaceutical Companies with Major MNCs in 2024

Data sources: Public reports, VBInsight

Seller's Perspective,Biocytogen, Bio-Thera Solutions, ArriVent Biopharma, Nona Bioscience, WuXi Biologics, Yilian Biotech, and Insilico Medicine are all star enterprises in license-out collaboration deals.

Figure 22: In 2024, Nearly 10 Chinese Innovative Pharmaceutical Companies Engaged in Two or More License-Out Transactions

Data Source: Public Reports, VBInsight

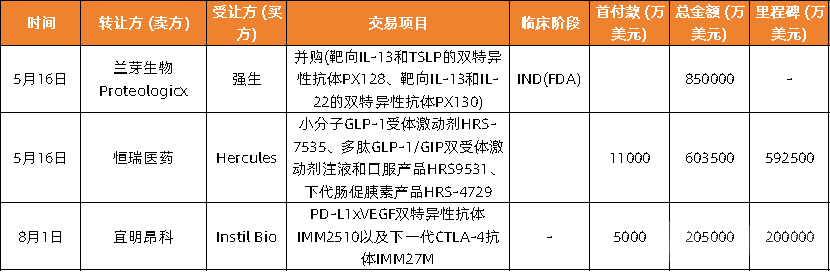

In terms of total transaction value for license-out deals, Lan Ya Biotech, Hengrui Medicine, and ImmuneOnco took the top three spots.

Figure 23 Top 3 License-out Deals by Total Value in 2024

Source: Public reports, VBInsight

In terms of upfront payments for license-out deals, Regor Pharmaceuticals, Tongrun Biopharma, and Mingji Biologics rank in the top three.

Figure 24 Top 3 Upfront Payments in License-out Deals in 2024

Data Source: Public reports, VBInsight

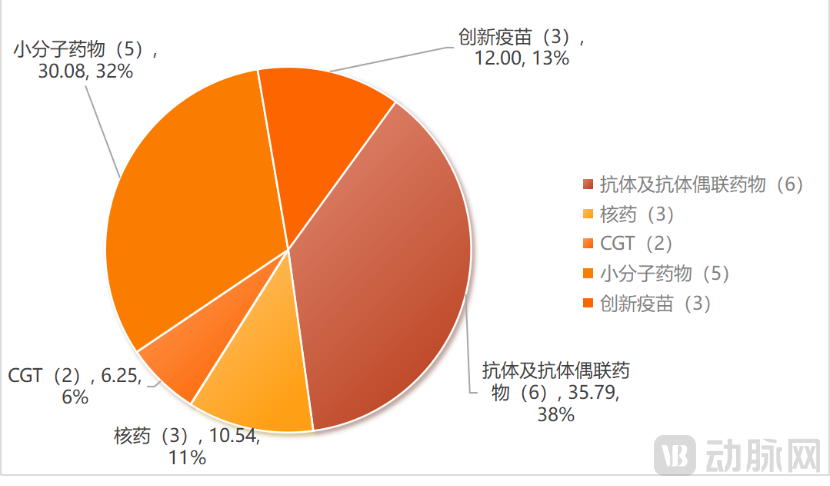

In terms of the types of drugs involved in transactions, the majority of license-out deals are focused on areas such as antibodies and antibody-drug conjugates (ADCs), as well as cell and gene therapy (CGT) products.

Among the 76 license-out transactions that occurred from January to October 2024, half (38 deals) involved antibodies and antibody-drug conjugates (ADCs), with bispecific antibodies and ADCs being the predominant categories.A total of nine license-out transactions involved bispecific antibody drugs, with their upfront payments accounting for 66.2% of the overall license-out transactions for antibody and antibody-drug conjugate (ADC) therapies.

Figure 25 License-out Transactions Related to Bispecific Antibody Drugs in 2024

Data Source: Public Reports, VBInsight

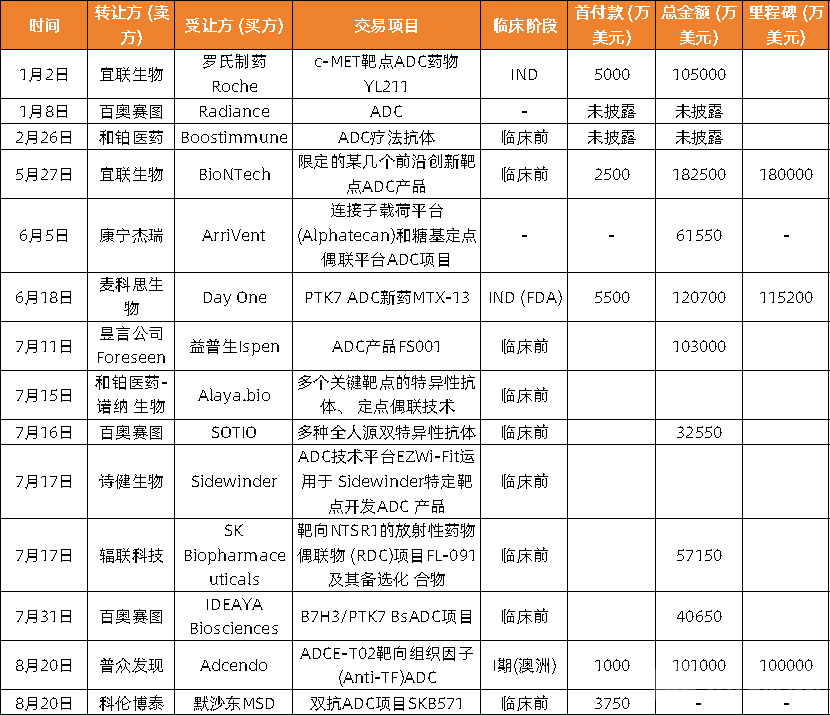

A total of 14 license-out deals related to ADC drugs,Accounting for 36.8% of the total number of license-out transactions related to antibody-drug conjugates (ADCs).

Figure 26 License-out Transactions Related to ADC Drugs in 2024

Data Source: Public Reports, VBInsight

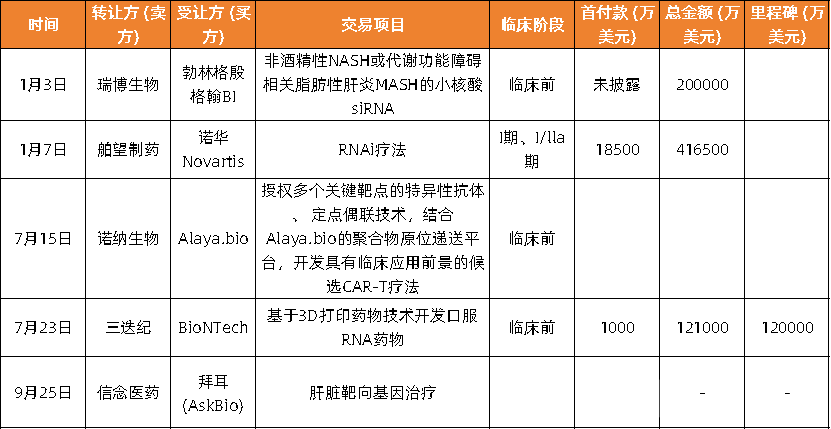

The CGT drug sector also delivered noteworthy performance in 2024: from January to October 2024, a total of five license-out transactions were completed in the CGT field.With the two early-year business development (BD) deals for overseas expansion of small nucleic acid drug pipelines—between Ribo Life Science and Boehringer Ingelheim, and between Shuwang Pharmaceutical and Novartis—Chinese small nucleic acid drugs have successfully broken the ice in going global. Notably, the upfront payment in the Shuwang Pharmaceutical–Novartis deal reached as high as $185 million.Following in the footsteps of ADCs and antibodies, cell and gene therapy (CGT) has emerged as another niche segment of innovative drug development in China that has gained global market recognition, holding promising prospects for the future.

Figure 27: License-out Transactions Related to CGT Therapeutics in 2024

Data Source: Public reports, VBInsight

The rapid momentum of license-out deals among Chinese innovative pharmaceutical companies is the result of joint efforts by both buyers and sellers.

On one hand, multinational pharmaceutical companies have increasingly recognized the R&D capabilities of Chinese pharmaceutical firms from the buyer’s perspective.On the other hand, given the current domestic industrial landscape, a successful license-out deal is not only regarded as a powerful tool for securing financing during the capital winter but also serves as an exit route for certain pharmaceutical companies’ executive teams and related investors.

License-out deals featuring high transaction values and substantial upfront payments (at least over $100 million) indicate that the innovator’s drug development capabilities have been recognized by multinational corporations (MNCs), thereby facilitating easier access to financing. Furthermore, although industry consensus has not yet been reached, license-out transactions are, to some extent, regarded as an exit strategy.

Some notable successes include Henlius Pharmaceuticals’ $1.3 billion license-out deal with Novo Nordisk in 2023—although later-stage pipeline progress fell short of expectations, resulting in no additional milestone payments.An upfront cash payment of approximately USD 800 million enabled the relevant shareholders to achieve substantial investment returns.

Although for most investment institutions,Compared with previous IPOs, exits achieved through business development (BD) transactions such as license-out deals have generally yielded less-than-ideal results., likely merely at the break-even level.

Therefore,Licensing out non-core assets to indirectly validate a pharmaceutical company’s R&D capabilities, while simultaneously introducing cash flow to support the development of its core pipeline through business development (BD) deals, represents a shared vision across the industry.Lixin Pharma has entered into multiple license-out deals with companies including AstraZeneca, Turning Point Therapeutics, and Merck & Co. However, the innovative drug assets licensed out were non-core pipeline candidates, so these transactions do not affect its future development prospects.

Figure 28. Selected Clinical Pipeline of Liminopharma

Source: Limin Pharma official website

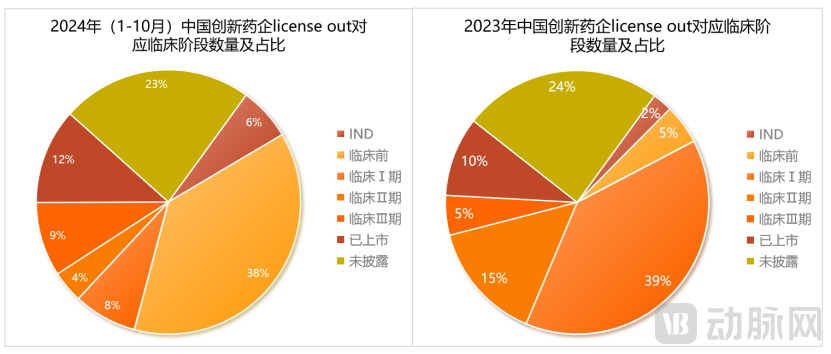

From the perspective of the clinical stages of pipelines involved in license-out transactions, the proportion of preclinical and IND-stage assets is increasing. In 2023, preclinical and IND-stage assets accounted for 7% of license-out deals; this figure rose to 44% in 2024.If judged solely by the number of disclosed clinical-stage pipeline assets, this ratio would be even higher.

Figure 29 Changes in Clinical Stages Corresponding to License-out Transactions by Chinese Innovative Pharmaceutical Companies, 2023–2024

Data source: Meibo Bidi, VBInsight

Industry insiders stated that,The Phase I clinical stage, or the period immediately preceding clinical trials, is the most suitable stage for business development (BD) within a drug pipeline, as this is when capital exerts the greatest leverage.

For sellers, amid the capital winter,For promising preclinical assets that lack the resources to advance into clinical trials, monetization through license-out deals is a sound strategy.For buyers, preclinical assets with preliminary validation data also offer a higher cost-performance ratio.

Accelerated Global Expansion of Marketed Drugs: Beyond Europe and the US, Chinese Pharmaceutical Companies Target Emerging Markets in the Middle East, Southeast Asia, and North AfricaAccording to incomplete statistics from VBInsight, 14 drugs were intensively exported overseas through CSO collaborations from January to October 2024.

Figure 30: In 2024, Domestically Listed Drugs Intensified Their Global Expansion

Data sources: public reports, VBInsight

Compared with the European and American markets, which impose stricter requirements on drug efficacy and safety and are less price-sensitive, emerging markets such as the Middle East, Southeast Asia, and North Africa—characterized by large populations, vast market potential, and high price sensitivity—have become key regions for the international expansion of drugs approved in China.

However, some primary market investors have pointed out that, as many Chinese innovative pharmaceutical companies still prioritize the North American market and domestic clinical needs during project initiation and development, certain listed innovative drug assets exhibit low compatibility with emerging markets. Given market access in emerging economies and the influence of complex factors such as local production and transportation conditions,In the coming years, North America and China will remain the preferred markets for Chinese biotech companies, particularly for early-stage projects, when initiating development based on clinical needs.

It has become the new norm for biotech companies with marketed products to transfer commercialization rights.In 2024, a growing number of biotech companies, including those with the potential to evolve into biopharmaceutical enterprises, are intensively abandoning independent commercialization in the Chinese market.Domestic biotech firms are returning their focus to product and R&D, while it is becoming an industry consensus that large pharmaceutical companies leverage their established in-house sales teams and channel resources to handle commercialization.

From January to October 2024, according to incomplete statistics from VBInsight, there were a total of 16 cases of Biotech companies transferring commercialization rights to domestic pharmaceutical enterprises, involving a total disclosed transaction amount of RMB 7.29 billion and an upfront payment amount of RMB 860 million.

Figure 31 Overview of Commercialization Rights Transfers from Biotech Firms to Domestic Pharmaceutical Companies in 2024

Data source: Public reports, VBInsight

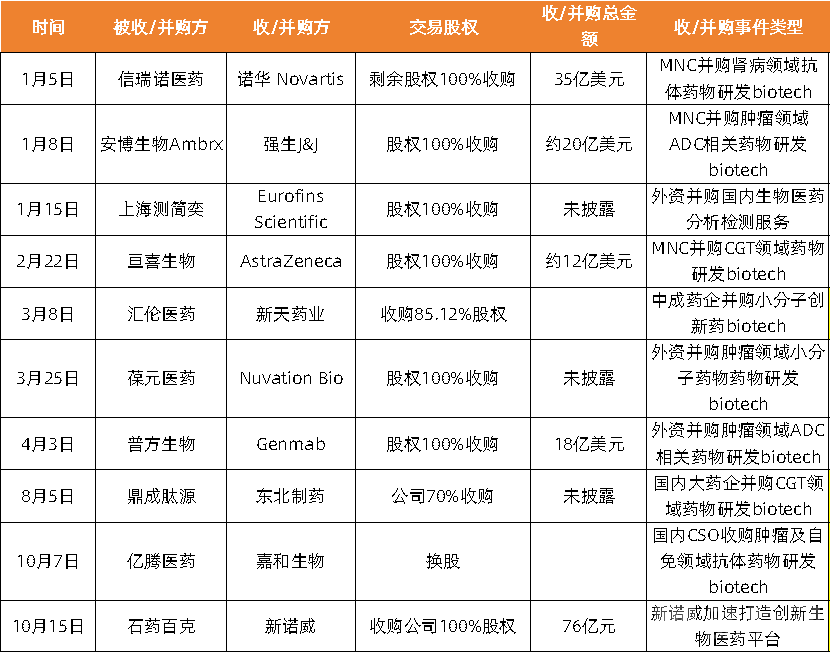

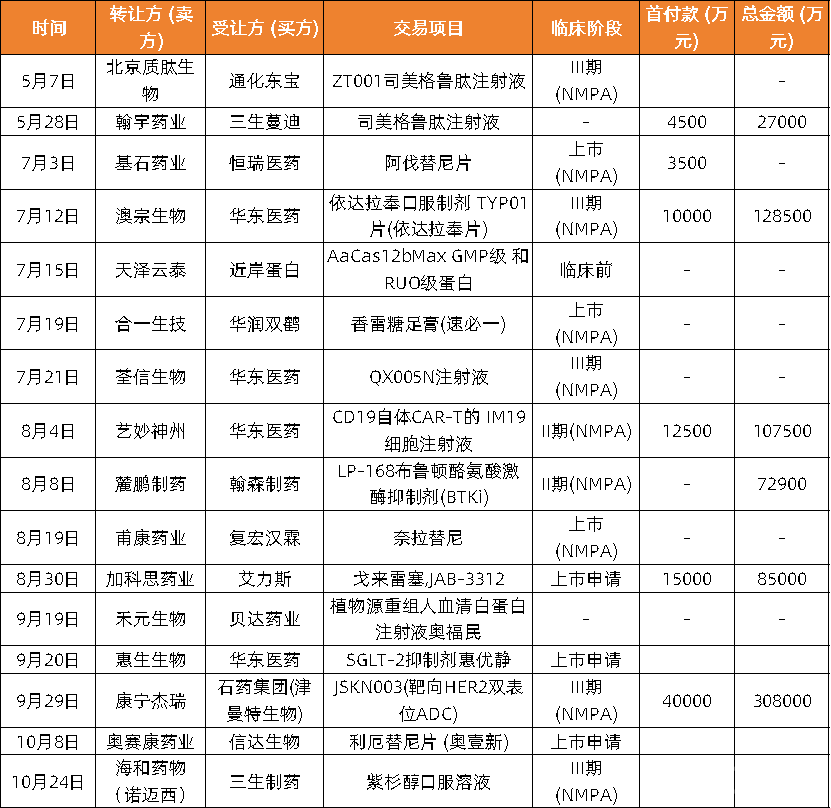

In the ongoing wave of mergers and acquisitions in 2024, besides the frequently disclosed M&A transactions by multinational corporations (MNCs), many established domestic pharmaceutical companies with substantial capital reserves are also accelerating their strategic layouts.

AsXintian PharmaceuticalAcquired an 85.12% equity stake in Shanghai Huilun Pharmaceutical to achieve a dual-drive strategy of “traditional Chinese medicine + chemical drugs”;Xinnuowei Invests RMB 7.6 BillionAcquiring 100% equity of CSPC Baike to accelerate the development of a more competitively advantageous innovative biopharmaceutical platform; one of the “four major legacy pharmaceutical companies”Northeast PharmaceuticalProposed acquisition of a 70% equity stake in Dingcheng Peptide Source, a biotech company specializing in TCR-T therapy R&D, for RMB 187 million; it was also stated that, following the successful completion of the acquisition, ample funding would be allocated for scientific research and translational development, with “no upper limit.”

In terms of licensing transactions for pipeline assets, domestic pharmaceutical companies have also made active attempts.For instance, the long-established listed pharmaceutical company Salubris Pharmaceuticals secured exclusive licensing rights for Yaotang Biopharma’s base editing drug “YOLT-101” in a transaction valued at over RMB 1 billion. Other similar deals include pipeline licensing and technical collaborations between domestic pharmaceutical companies and biotech firms in areas such as small nucleic acid drugs and mRNA vaccines.

Figure 32 Pipeline Licensing Deals and M&A Transactions Between Domestic Pharmaceutical Companies and Biotechs

Data source: Public reports, VBInsight

However, overall, most established pharmaceutical companies remain relatively conservative in their strategic positioning within the innovative drug sector. This is closely tied to the inherent organizational culture and resource endowments of their teams, as the deployment of innovative drug assets indeed carries substantial risk.

Taking Salubris Pharmaceuticals’ in-licensing of Yaotang Biologics’ pipeline as an example, while it appears to be an acquisition of cutting-edge base-editing drugs, key considerations included the drug’s indication within Salubris’ familiar cardiovascular disease domain—enabling pipeline synergy—and the clinical validation of similar foreign-targeted drugs. Additionally, Yaotang Biologics’ distinct advantages and patent portfolio in delivery systems are indeed noteworthy. Meanwhile, Huilun Pharmaceutical, acquired by Xintian Pharmaceutical, boasts robust self-generated cash flow and solid profitability.

Objectively speaking,For the foreseeable future, MNCs will likely continue to dominate acquisitions of local biotech firms and licensing of pipeline assets. However, the new strides made by domestic pharmaceutical companies, coupled with positive feedback from later-stage development and accumulated experience, will undoubtedly serve as a significant positive catalyst for major domestic pharmaceutical enterprises in their acquisition of innovative drug assets.

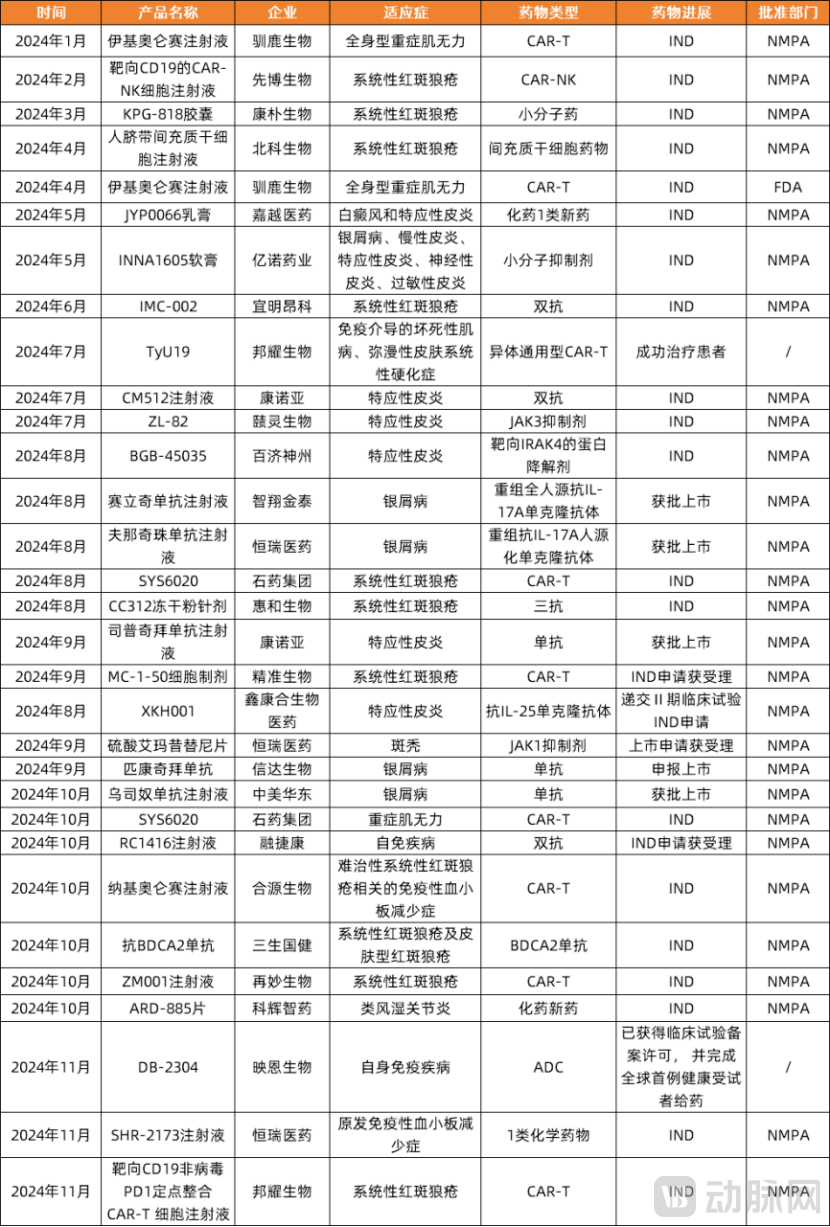

In 2024, research and development in the autoimmune field was in full swing. According to incomplete statistics from VBInsight, as of November 20, 2024, more than 30 autoimmune drugs in China had reached key clinical milestones. Various therapies, including CAR-T, stem cell therapy, antibody-drug conjugates (ADCs), bispecific antibodies, and trispecific antibodies, have flourished in the autoimmune space, with indications covering systemic lupus erythematosus, atopic dermatitis, psoriasis, vitiligo, alopecia areata, myasthenia gravis, and other diseases. Among these clinical pipelines that have achieved milestone progress, three points are worth noting.

Figure 33. Autoimmune Disease Pipeline with Milestone Progress in 2024

Data source: Public reports, VBInsight

First is the issue of target clustering and homogenization of indications.Autoimmune drugs developed against popular targets such as IL-4R, IL-17A, IL-12, IL-23, and TSLP have been launched globally. In China, more than ten companies are pursuing each of these high-profile targets. This target clustering has led to homogenization of indications, with most pipelines in the autoimmune field currently focusing on atopic dermatitis, psoriasis, rheumatoid arthritis, and systemic lupus erythematosus. Moreover, the majority of these investigational pipelines are already in Phase II or Phase III clinical trials, pointing to intense future commercial competition.

Secondly, there is an urgent need for long-acting products in the field of autoimmune diseases.Autoimmune diseases are typically not fatal. Given their limited financial capacity and price sensitivity, patients in China cannot allocate substantial economic resources to treating autoimmune conditions as they might for cancer. Consequently, there is a greater need for long-term, safe, and affordable therapeutic products for autoimmune diseases.CAR-T therapy and other innovative approaches are being introduced into the field of autoimmune diseases, holding promise for delivering long-acting treatments such as “one-shot efficacy” to patients with autoimmune conditions.Among the pipelines that achieved clinical milestone breakthroughs in China in 2024, nine were autoimmune CAR-T pipelines, accounting for nearly half of the total.

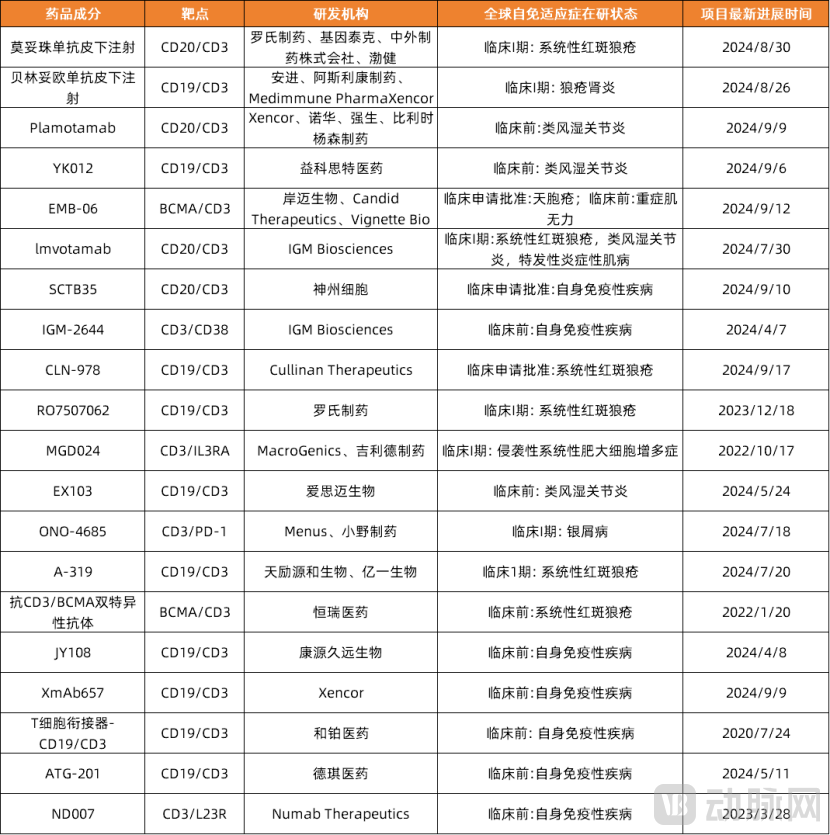

Finally, the rise of T cell engager (TCE) technology in the field of autoimmune diseases is also noteworthy.In 2024, the industry witnessed intensive acquisitions of TCE bispecific antibody assets. According to incomplete statistics from VBInsight, TCE-related pipeline transactions accounted for five out of six NewCo deals in 2024. On the clinical front, more than 20 actively developed TCE drugs worldwide are currently undergoing clinical studies for autoimmune diseases, primarily focusing on target combinations such as CD3×CD19, CD3×CD20, and CD3×BCMA.

Figure 34 Global TCE Bispecific Antibodies in Development for Autoimmune Diseases

Data source: VBInsight

As the global obese population increases, demand for novel glucose-lowering and weight-loss medications—such as GLP-1-based therapies (including GLP-1 receptor agonists, GLP-1R/GIPR dual agonists, and GLP-1R/GCGR dual agonists)—is also on the rise.

In the global market, GLP-1-related weight loss products are currently dominated by Novo Nordisk and Eli Lilly. In China, Novo Nordisk’s patent for semaglutide is set to expire in 2026, with numerous domestic generic drug manufacturers already positioning themselves in this sector and poised to enter the commercialization phase.As of November 20, 2024, four GLP-1R and GLP-1R/GIPR products have been approved in China.

Figure 35 GLP-1 Products Currently Approved for Weight Management

Data sources: Public reports, VBInsight

Clinical Stage,China has an even larger pipeline of GLP-1-based weight-loss therapies. According to publicly available data, more than 56 GLP-1 products are currently undergoing research for weight-management indications in China, with 55% of them having advanced to Phase II or III clinical trials, marketing application submission, or market approval stages. This indicates that competition in the domestic GLP-1 weight-loss segment will intensify further over the next two to three years.

Figure 36 Current Progress of GLP-1 Products in China for Weight Loss Indications

Data sources: Public reports, VBInsight

In 2024 Only(Data as of November 20, 2024),As many as 16 GLP-1-based weight-loss drug candidates in China have achieved milestone progress.(including products approved for market by Novo Nordisk and Eli Lilly). In addition to already approved products, the most advanced candidate is Mazdutide from Innovent Biologics, whose marketing application for weight management indications was accepted by the NMPA in February 2024. It is the first GLP-1R/GCGR dual agonist globally to file for marketing approval and is poised to become the first domestically produced dual-target weight-loss drug.

Figure 37 GLP-1-related weight loss products with milestone clinical advancements in China in 2024

Data sources: Public reports, VBInsight

Against the backdrop of Novo Nordisk’s Wegovy and Eli Lilly’s Zepbound, the GLP-1 weight-loss sector has set a high bar from the outset, meaning that subsequent competitors will need toDemonstrates advantages in efficacy, safety, convenience, and other aspects, will it be able to possess the strength to compete with Novo Nordisk and Eli Lilly.Oral administration, dual-target novel GLP-1 drugs, and exploration of combination therapies are key areas of focus for major pharmaceutical companies in their upcoming strategic plans.

Furthermore, as various companies’ products gradually enter the market, there is also a substantial demand for production capacity of GLP-1-based therapies. It is foreseeable that once competition in technology and products reaches a certain stage, in the near future,The GLP-1 Weight Loss Sector Will Face Competition Over Production Capacity and Pricing.

According to incomplete statistics from VBInsight, as of November 11, 2024,More than 15 drug candidates in the CNS field achieved significant progress in China in 2024, with indications covering neurodevelopmental disorders, psychiatric disorders, neurodegenerative diseases, and rare diseases such as amyotrophic lateral sclerosis (ALS); drug types include both traditional therapies such as monoclonal antibodies and small-molecule drugs, as well as emerging therapies including cell therapy, gene therapy, stem cell therapy, and nucleic acid-based drugs.

Figure 38: Chinese CNS Pipelines Reaching Key R&D Milestones in 2024

Data source: Public reports, VBInsight

Industry experts have pointed out that,The fragmented and diverse landscape of indications in the CNS field may be attributed to two factors.: First, each specific indication within the central nervous system (CNS) therapeutic area encompasses a large patient population, and effective treatments are currently lacking for most of these conditions. Second, driven by various factors—including high-profile social events, significant advancements in blockbuster drugs, and heightened regulatory attention—the CNS disease field is experiencing a boom in development activity.

Although the CNS pipeline presents a landscape where traditional and emerging therapies each account for half of the field, but from the perspective of traditional clinical application and regulatory approval,Small-molecule drugs still account for the majority.Qian Hua, Senior Vice President of Business Development and Strategic Alliances at Yisi Bio, stated that since current academic and clinical understanding of CNS diseases largely remains rooted in the classical perspective of receptors, small-molecule drugs hold a distinct advantage in terms of the feasibility of developing receptor modulators.

In practice, it is an industry consensus that the development of central nervous system (CNS) therapeutics is highly challenging and associated with high clinical failure rates. Bao Yanghuan, founder of Pubaisi Biotech, stated that unlike oncology diseases, where most tumors present with well-defined lesions at specific stages, most CNS disorders involve multi-target and multi-mechanistic pathways, leading to greater complexities in pipeline development and clinical patient recruitment. Currently,CNS diseases still face challenges such as unclear mechanisms, a lack of reliable animal models, and significant drug toxicity and side effects.

Drug combinations, improved dosage forms, drug-device combinations, medical devices, digital therapeutics, and diagnostic testing methods with novel intellectual property rights will constitute a blue ocean for CNS development; even in the context of the AI era, there is substantial demand for intelligent solutions such as human-computer interaction workstations and apps.CNS Diseases: A Field with Great Potential and Promise

Drawing on an analysis of industry innovation logic and corporate practical initiatives, this white paper presents a list of the year’s outstanding innovation cases, with detailed interpretations of selected cases provided in subsequent chapters.

The above is an excerpt from the main content of the report. Scan the QR code on the poster.Scan the code to access the full report.

Report Contents