Even the Aesthetic Medicine Upstream Sector Is Now Fiercely Competitive!

The medical aesthetics industry, once deemed “highly lucrative,” has faced significant challenges in recent years: intense price and marketing competition has become the norm for mid-tier service providers, with even publicly listed companies struggling to achieve profitability.

Consequently, starting in 2021, capital flocked to shift its focus, sparking a financing boom in the upstream segment of the medical aesthetics industry. This surge propelled multiple companies to successful initial public offerings (IPOs), creating notable business success stories such as the “Three Musketeers of Medical Aesthetics,” the “Moutai of Medical Aesthetics,” the “Collagen Myth,” and the “Year One of Regenerative Aesthetics.”

However, in 2024, the upstream sector of the medical aesthetics industry also began to feel the pressure of intense competition.

It began with product proliferation. From the official NMPA approval of AestheFill, a poly-L-lactic acid-based biostimulator under South Korea’s Regen Biotech (Lizhen), introduced by Jiangsu Wuzhong Pharmaceutical, to Bloomage Biotechnology securing China’s second Class III medical device registration certificate for composite solutions, and further to the successive approvals of Galderma’s Sculptra and Proyouth’s Proyouth Baby Face, new aesthetic medicine products launched in 2024 were largely extensions of existing categories, with no significantly differentiated product directions emerging in the market.

Next comes price competition. In 2024, prices in the upstream segment of the medical aesthetics industry also began to decline. For instance, competition has become exceptionally fierce for hyaluronic acid, one of the most popular materials in the upstream supply chain. Taking Imeik, the industry leader, as an example, the average unit price of its flagship Hi-Ti series has continued to drop: according to data from Miaotou, it has fallen from a peak of 384 yuan in 2021 to around 330 yuan.

In the face of increasingly fierce industry competition, how can upstream players in the medical aesthetics sector break through in the post-hyaluronic acid era? What possibilities lie ahead in 2025?

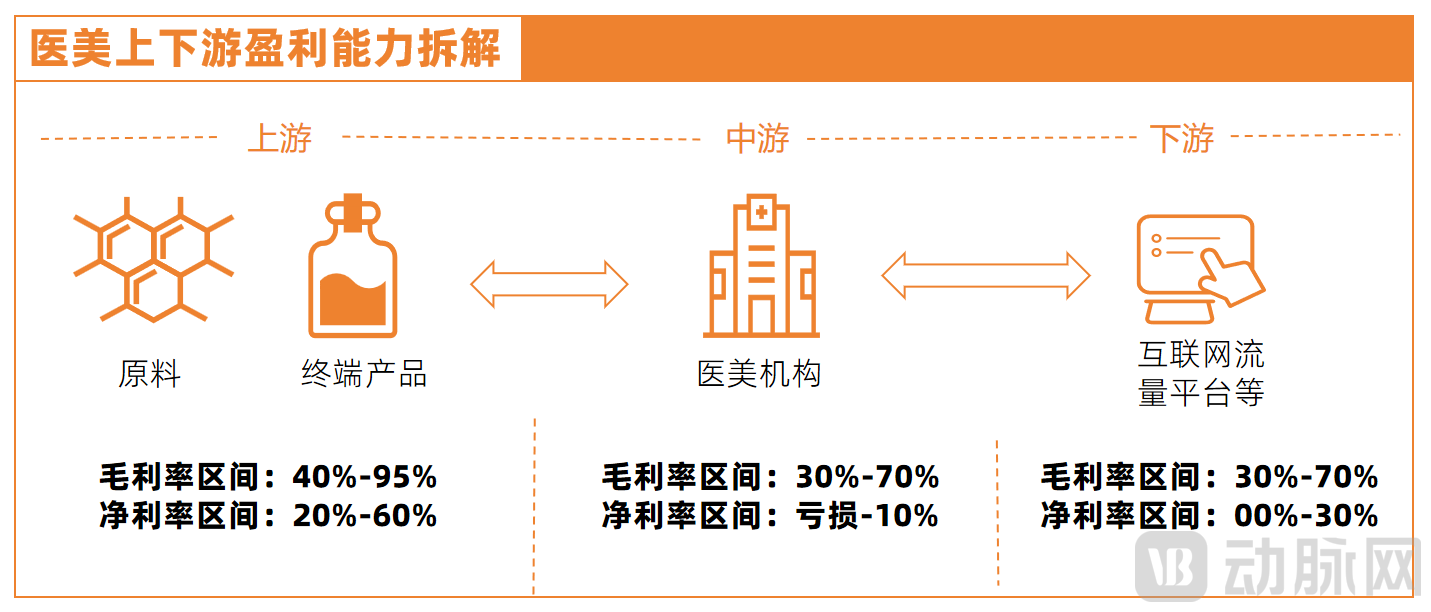

“The upstream players feast on meat, the downstream ones sip the broth, while those in the middle can’t even gnaw on the bones.” This was once the most apt metaphor for the survival conditions across various segments of the medical aesthetics industry chain.

▲Graphic by VCBeat

Specifically, the upstream sector primarily consists of product R&D and supply companies represented by Imeik, Bloomage Biotech, Haohai Biological Technology, and Giant Biogene. Leveraging their relatively scarce products, these companies hold the greatest bargaining power within the industry chain. The midstream sector is dominated by medical aesthetic service providers such as Ruili Medical Aesthetics, Langzi Shares, and Huahan Shares. This segment faces intense competition and possesses relatively low bargaining power within the overall industry chain. The downstream sector comprises channel providers led by platforms like So-Young, Gengmei, Meituan, and Tmall. As internet platform-based enterprises, they control massive traffic volumes and occupy an intermediate position in terms of bargaining power within the industry chain. This industrial structure has consistently enabled the upstream medical aesthetic sector to enjoy exceptionally high gross profit margins.

At present, the era in which upstream players “feast on the meat” is drawing to a close.

“The industry barriers in the upstream segment of China’s medical aesthetics sector, created by “approval thresholds,” are diminishing.“Cheng Li (a pseudonym, at the interviewee’s request), Vice President of Investment at a well-known biomedical fund, told VCBeat, ‘The National Medical Products Administration maintains stringent review standards for Class III medical devices, resulting in a slow approval process. This has kept competition in upstream categories relatively limited over the past few years, allowing companies to command higher pricing premiums and achieve strong profitability. However, as more products gain approval, competition is intensifying.’”

Data provides insights into the approval speed of products. Taking regenerative aesthetic injectables as an example, four products were approved in 2024: Jiangsu Wuzhong’s AestheFill (“Tongyan Zhen”), Galderma’s Sculptra, Shandong Guyuchun’s Suyanzhen·Zhenhao, and Prellen’s Prellen·Tongyan. With these approvals, the total number of regenerative aesthetic injectable products approved in China has reached seven.

The recombinant collagen sector is also characterized by intense competition. According to data from Meiyexinweidu, there are currently 753 medical device registration certificates for “recombinant collagen,” with 485 newly approved in 2024 alone, accounting for a striking 64.41%.

Not only that,Products awaiting approval are also coming in quick succession.It is understood that multiple companies, including Hanggai Biotech, Sihuan Pharmaceutical, and Xihong Biotech, have established R&D pipelines for regenerative products, which are expected to receive regulatory approval for market launch in 2025 and subsequent years.

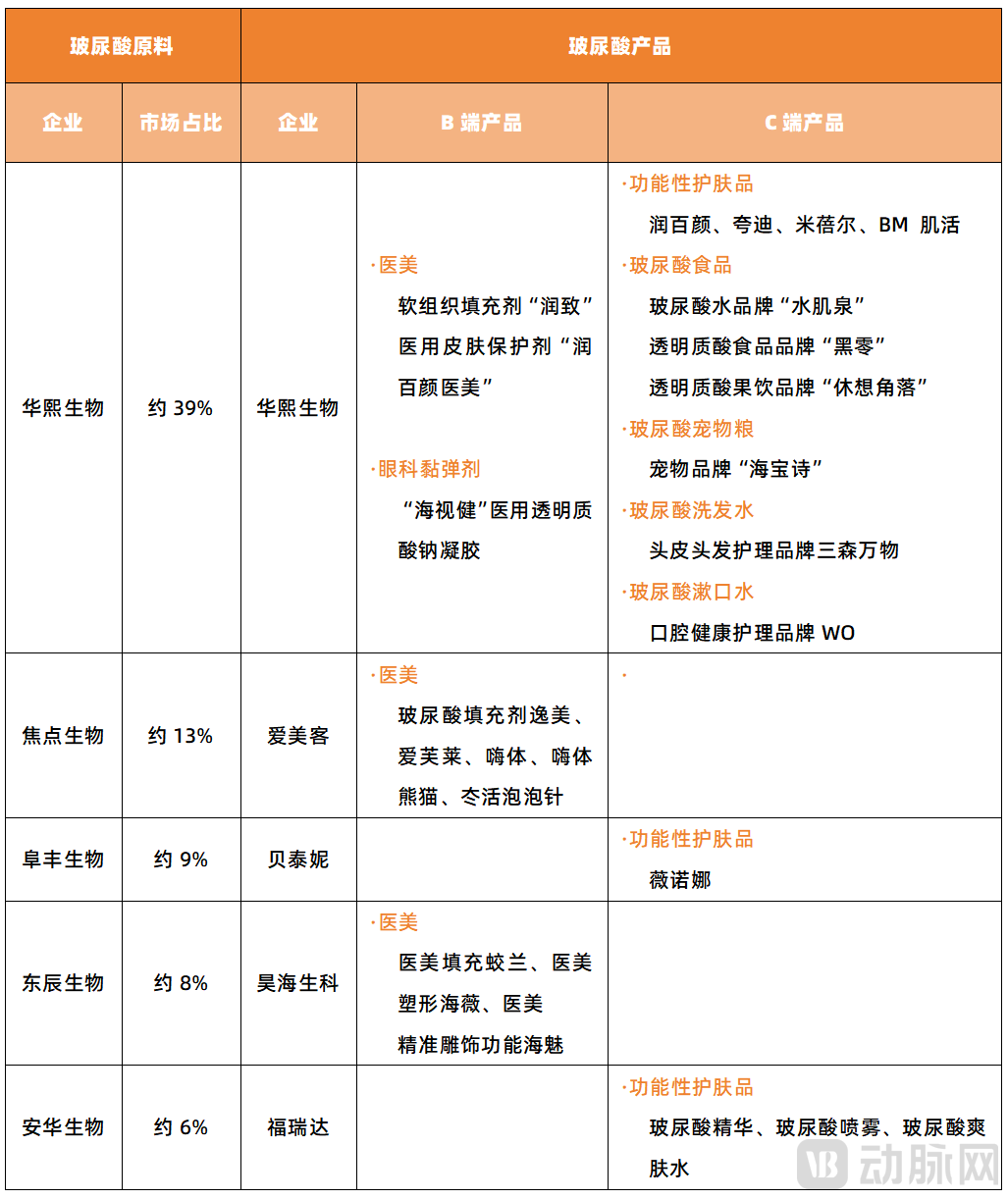

Not only are regenerative medical aesthetic injectables facing fierce product competition, but hyaluronic acid, the hottest single product in the medical aesthetics industry, has long entered a red ocean: in 2024, the number of approved hyaluronic acid-related device products exceeded 70.Companies are pulling out all the stops in exploring application scenarios for hyaluronic acid, pushing the boundaries of possibility to new extremes., including but not limited to its application in functional skincare products, food items, shampoos, mouthwashes, and other products.

▲ Hyaluronic Acid Product Portfolios of Select Companies | Chart by VCBeat based on public data

More players are also entering the botulinum toxin market. In March 2024, Merz Aesthetics’ Xeomin® received approval, becoming the fifth botulinum toxin product available in the Chinese market. Soon after, companies such as Imeik, Huadong Medicine, and Fosun Pharma are poised to reap the benefits of their investments, signaling that fierce competition in the botulinum toxin sector is imminent. Meanwhile, the once-buzzing field of recombinant collagen has been following a similar trajectory over the past two years.

Meanwhile,“The ‘one certificate, multiple products’ model has further intensified competition.”What Is “One Certificate, Multiple Products”? It refers to the marketing strategy of packaging products under different specifications and brands while sharing a single medical device registration certificate, thereby saving on certification costs. This means that the number of medical aesthetic products available on the market far exceeds the number of approved certificates.

For example, the Class III medical device product approved for Imeik, “cross-linked sodium hyaluronate gel containing poly(L-lactic acid-co-glycolic acid) microspheres,” is available in specifications including 0.5 mL, 0.75 mL, 1.0 mL, 1.5 mL, 2.0 mL, 2×0.5 mL, 2×0.75 mL, and 2×1.0 mL. Among these, the product packaged as two 0.75 mL syringes per box is marketed as “Ruba Angel,” while the one packaged as two 1.0 mL syringes per box is marketed as “Rusheng Angel.”

Furthermore, under the pressure of survival, medical aesthetic service providers implemented more aggressive price-cutting promotions in 2024, transmitting this downward pricing pressure upstream. This has, to some extent, suppressed product prices for upstream enterprises and accelerated the trend of hyper-competition.

It is worth noting that in recent years, medical aesthetics service providers have accelerated their OEM (original equipment manufacturer) layouts—commonly known as “private labeling”—to expand their profit margins, thereby intensifying competitive challenges in the relevant product markets. VCBeat previously reported in its article “The Great Melee in Medical Aesthetics” that service providers such as Mylike, Yestar, Langzi Medical Aesthetics, and Huamei each have multiple customized products of their own.

It is precisely against this industry backdrop thatDomestic upstream medical aesthetics companies have seen a continuous decline in performance growth.According to the financial reports of listed companies, Imeik, a leading player in the medical aesthetics industry, saw its revenue grow by 13.53% year-on-year in the first half of 2024, significantly lower than the over 30% growth rate recorded in previous years; Haohai Biological Technology’s revenue growth rate declined from 32.61% in 2021 to 6.97%; while Bloomage Biotechnology continued the downward trend seen in 2023, with a year-on-year revenue growth rate of -8.61%.

How to Break Through Involution Has Undoubtedly Become an Urgent Issue for Upstream Companies in the Medical Aesthetics Industry

To break free from intense competition, it is imperative to identify differentiated pathways or seize new market growth opportunities. Thus, within the existing pipeline,Expanding product indications is one of the problem-solving strategies for innovative enterprises.

Taking botulinum toxin as an example, this product was previously limited to facial aesthetic applications. In October 2024, Allergan Aesthetics officially announced that the U.S. FDA had approved the indication for its botulinum toxin product, BOTOX® Cosmetic, to “temporarily improve the appearance of moderate to severe vertical bands (platysmal bands) between the chin and neck.” This marked the first approval of a botulinum toxin product for use outside the face, thereby opening up new market opportunities.

In China, a review of the NMPA website reveals that BOTOX® Cosmetic has been approved for four indications: first, for the treatment of blepharospasm, hemifacial spasm, and related focal dystonia in patients aged 12 years and older; second, for the temporary improvement of moderate to severe glabellar lines associated with corrugator and/or procerus muscle activity in adults aged 65 years and younger; third, for the temporary improvement of moderate to severe lateral canthal lines (crow’s feet) in adults; and fourth, for the temporary improvement of prominent or very prominent masseter hypertrophy in adults.

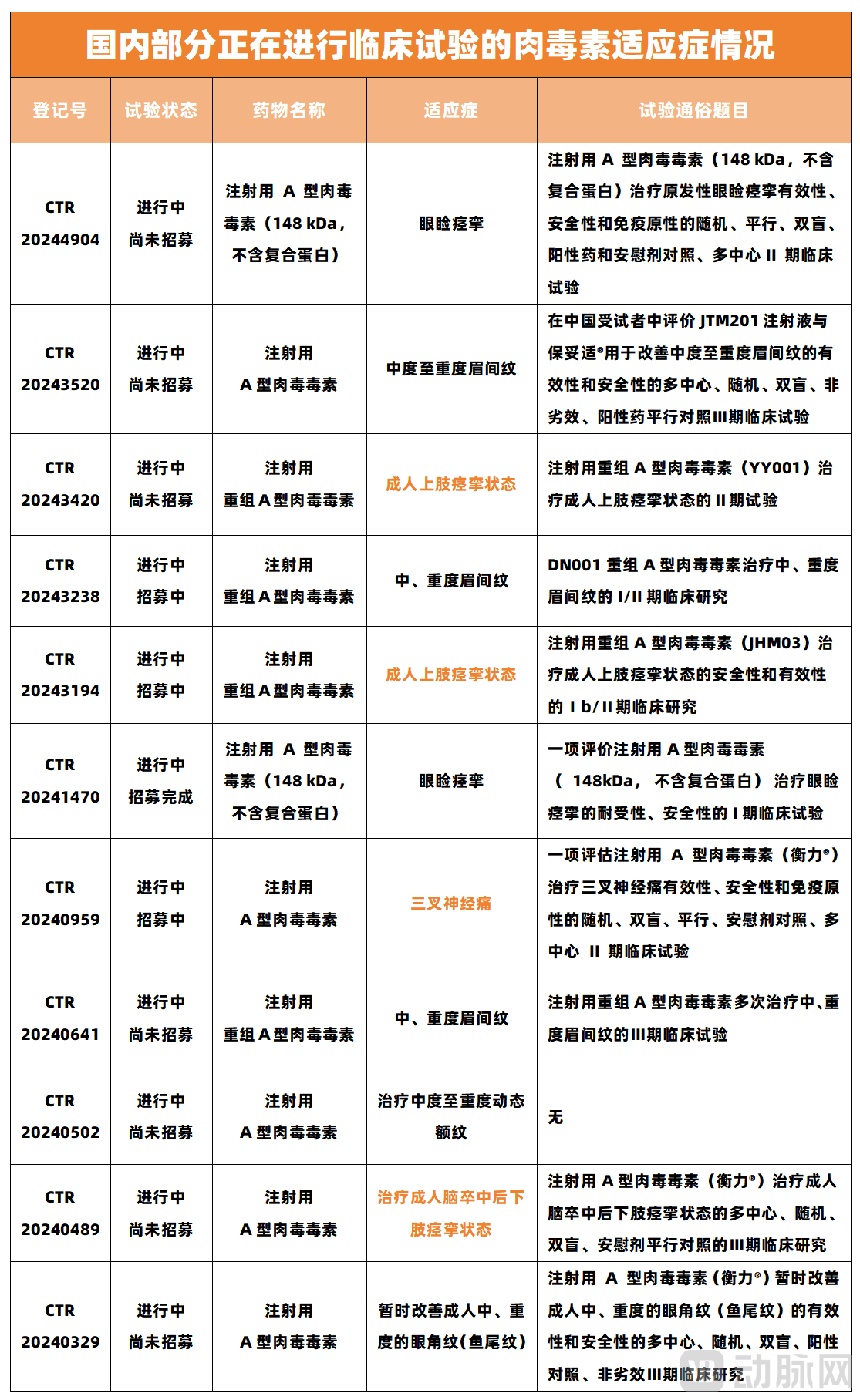

Beyond this, the industry is actively exploring indications for botulinum toxin beyond medical aesthetics, including serious medical conditions and the weight-loss drug market (to alleviate “Ozempic face”). For instance, JHM03, an injectable recombinant type A botulinum toxin under Junhemeng Biologics, targets the treatment of upper limb spasticity in adults after stroke. In September 2024, Junhemeng announced that the clinical study of JHM03 for upper limb spasticity in post-stroke adults had enrolled its first subject, with approval imminent.

▲Source: Drug Clinical Trial Registration and Information Publicity Platform

Taking Sculptra as an example, an institutional investor specializing in consumer healthcare recently told VCBeat that the pricing of Sculptra will undergo a repricing process as the competitive landscape continues to evolve. “Therefore, if there are breakthroughs in existing indications and injection dosages in the future, there may be greater potential for market share and pricing. For instance, Lanluma, recently acquired overseas by Huadong Medicine, is a product that breaks through the current indications of Sculptra.”

“Over time, existing products are increasingly revealing numerous issues. If new products can “address the root causes,” they can secure a competitive edge through continuous optimization.“Cheng Li, Vice President of Investment at the aforementioned biopharmaceutical fund, cited botulinum toxin as an example. In the past, related products generally suffered from pain points such as short duration of efficacy, low purity, and narrow indications. Late-entering companies that conduct R&D targeting these issues can also become key to breaking through in the market.”

Meanwhile, as competition in the Chinese market intensifies,Seeking overseas markets is becoming a new practice for many innovative enterprises.Taking Bloomage Biotech, which expanded its overseas business at an early stage, as an example, the company has successively launched its Runzhi series of hyaluronic acid products in markets such as Thailand and Russia amid intensifying domestic competition in recent years, achieving sustained sales growth.

According to Bloomage Biotech’s financial report, the company’s domestic revenue experienced negative growth in 2023, while its overseas business grew by approximately 20%. In the first half of 2024, overseas revenue accounted for 17% of the total.

Targeting potential market opportunities, a cohort of innovative companies is accelerating their global expansion. For instance, in the collagen sector, Trauer Medical entered into a strategic cooperation agreement with DKSH in April 2024 to introduce its recombinant collagen products to the U.S. market; in November of the same year, Jinbo Bio and Meibo Bio sequentially announced that their respective products had received regulatory approval in Vietnam.

It is evident that innovative enterprises can break free from intense domestic competition only by either expanding product indications and addressing issues with existing products, or by expanding from the domestic market to the international stage.

In recent exchanges with medical aesthetics industry professionals, VCBeat learned that listed companies, new entrants, and investors alike are eagerly anticipating the emergence of new medical aesthetics materials comparable to hyaluronic acid.

"In the medical aesthetics industry,"Material innovation is the key to creating the next generation of “blockbuster products.”“Cheng Li stated, ‘The future of medical aesthetics will be dominated by innovations in materials and applications.’”

Taking aesthetic injectables as an example, due to differences in the degradation cycle, physical properties, firmness, and microstructure of various materials, products based on different materials vary significantly in their intended injection depths and design directions for aesthetic outcomes: generally, firmer materials are suitable for deep-layer injection and localized contouring, while softer materials are appropriate for superficial injection to treat fine lines or provide large-area volumization.

Therefore, amid the ongoing intense competition among upstream players in the medical aesthetics industry and the increasingly refined demands of aesthetic seekers, new materials and solutions have become critical factors determining whether the industry can achieve substantial growth.

Some industry experts believe that hyaluronic acid has become a saturated market, collagen is entering its maturity phase, while polymers such as polylactic acid and polycaprolactone are experiencing rapid growth, offering substantial market potential and numerous opportunities. Beyond these materials, promising candidates like hydroxyapatite, agarose, and extracellular matrix components are currently garnering significant attention.

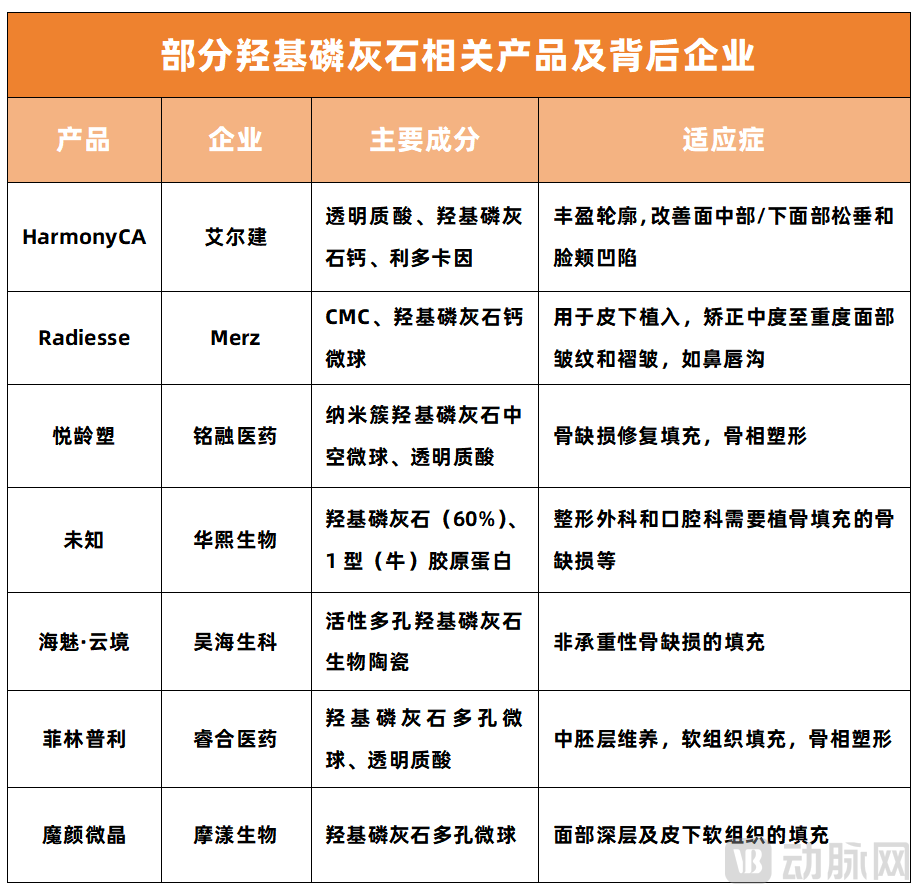

WithHydroxyapatiteAs an example, this material is a naturally occurring mineral whose degradation occurs through hydrolysis and osteoclastic enzyme activity, gradually breaking down into calcium ions and phosphate ions. This slow degradation process allows the effects of hydroxyapatite fillers to last for an extended period, typically between 6 and 24 months, offering longer-lasting efficacy compared with current regenerative materials, which generally maintain their effects for approximately 6 to 12 months.

It is understood that multiple innovative companies, including Allergan, Moyang Biology, GeneScience Pharmaceuticals, Haohai Biological Technology, Merz (Germany), and Bloomage Biotechnology, have entered the field of hydroxyapatite materials and are accelerating their efforts to secure the first compliant Class III medical device certification in China for hydroxyapatite-based injectable fillers used in facial soft tissue augmentation within the medical aesthetics sector.

▲Source: FDA, NMPA

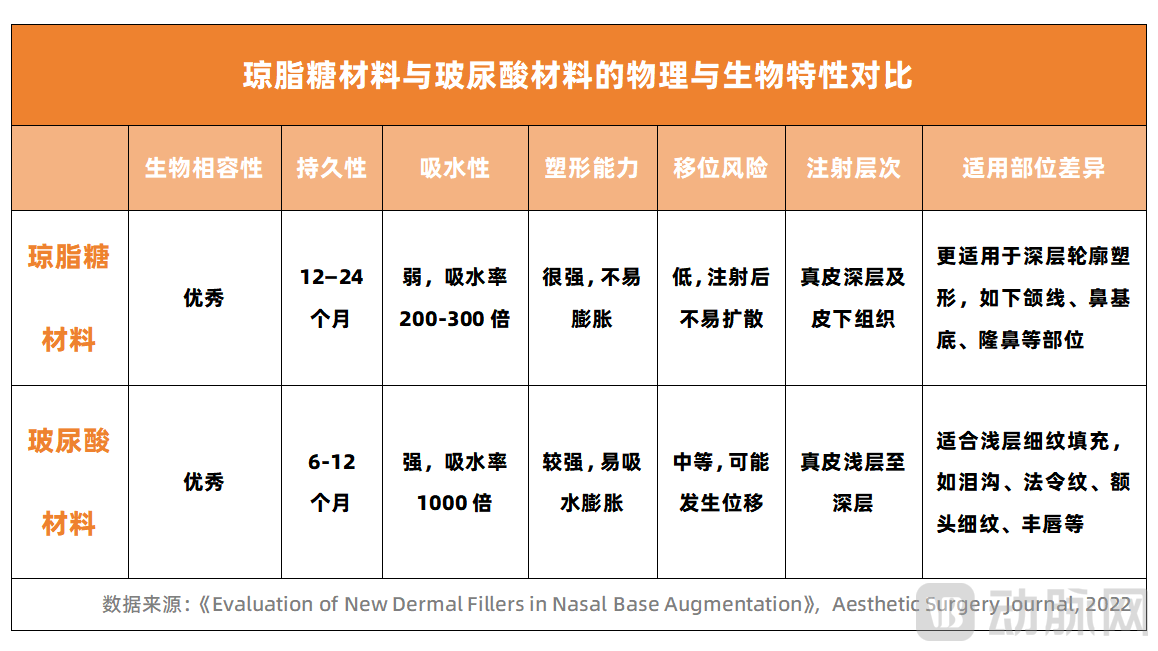

RevisitAgarose Materials. As a natural polysaccharide extracted from seaweed, it has a simpler structure and composition, higher purity, and its biosafety has been extensively validated through experiments. It is precisely due to its unique physical and chemical properties that agarose is demonstrating significant potential in medical aesthetic applications.

Currently, innovative companies such as Advanced Aesthetic Technologie, Lonza, Bio-Rad Laboratories, Beirong Biotech, and Huaban Biotech are engaged in the research, development, and marketing of agarose products. Their aim is to develop more high-performance agarose products suitable for the medical aesthetics field by improving agarose extraction and purification processes.

In December 2024, the "Agarose Gel for Injection" submitted by Beirong Biologics was classified as a Class III medical device. Its agarose injection AG15 is the second agarose-based injectable worldwide and has now entered the clinical trial phase.

NextExtracellular Matrix, which refers to the non-cellular component of tissues outside the cells. It serves as the environment in which cells reside and constitutes a sophisticated and organized network structure. The main components of the extracellular matrix include collagen, elastin, fibronectin, laminin, vitronectin, tenascin, and others. This material can support and maintain the morphology and function of tissues, while also influencing cellular behavior.

As the primary component of the extracellular matrix, collagen stimulates regeneration at both the cellular and molecular levels. Spanning the dual concepts of “recombinant collagen” and “regeneration,” it is regarded by many industry experts as a novel material with broad application prospects in the future medical aesthetics industry.

Certainly, the validation process for new materials requires a long cycle. It demands that all parties involved continuously address challenges throughout the entire journey—from translating scientific achievements into clinical trials, to refining the product for the market—while enduring prolonged periods of cost outlays and revenue fluctuations. This is an arduous endeavor.

Therefore, this process requires close collaboration between innovative enterprises, research institutions, and regulatory agencies to jointly inject new vitality into the sustainable development of the medical aesthetics industry, fostering the emergence of more widely accessible blockbuster products derived from innovative materials for beauty seekers.