How Peripheral Vascular Intervention Achieves Growth Amid Intensified Volume-Based Procurement

In 2024, there was no safe zone free from centralized procurement in the peripheral interventional field.

As one of the three major vascular intervention markets, the peripheral intervention market refers to the market formed around the interventional diagnosis and treatment of peripheral vascular diseases. Peripheral vessels include the carotid arteries, femoral arteries, and leg vessels, among others.

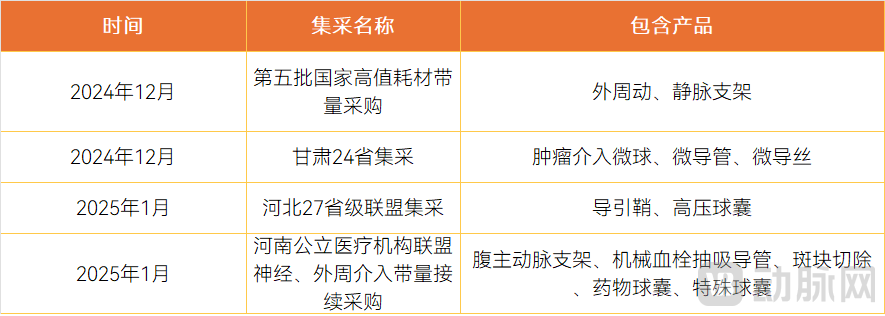

Within less than a month, the field of peripheral interventions has seen the implementation of three large-scale centralized procurement programs. First, the fifth national volume-based procurement (VBP) program for high-value medical consumables was successfully conducted, covering peripheral arterial and venous stents. Subsequently, the centralized procurement initiative involving 24 provinces, led by Gansu Province, was smoothly implemented, encompassing key products such as microspheres for tumor intervention, microcatheters, and microwires. In addition, the results of the Hebei Provincial Alliance’s centralized procurement are imminent, focusing primarily on peripheral guiding catheters. Following the successive implementation of these procurement programs, Henan Province rapidly initiated a follow-up volume-based procurement for neurointerventional and peripheral interventional devices. This procurement round further expanded the scope by including products previously not covered, such as abdominal aortic stents, mechanical thrombectomy catheters, and atherectomy devices.

Recent Volume-Based Procurement in the Field of Peripheral Intervention

Such a high frequency of volume-based procurement (VBP) is rare among other high-value medical consumables. After multiple rounds of VBP, the volume-based procurement for peripheral interventional products has become quite comprehensive.

Historically, the peripheral interventional product landscape featured a wide variety of offerings with relatively low market penetration, leading Chinese enterprises to predominantly adopt a fast-follower strategy in response to overseas innovations. However, with the frequent implementation of volume-based procurement (VBP), profit margins for mature products have been continuously compressed, the time interval between the launch of innovative products and their inclusion in VBP has significantly shortened, and foreign companies have actively participated in the bidding process. This indicates that Chinese domestic manufacturers urgently need to undergo a profound transformation in their development models.

How Will the Successive Volume-Based Procurement Programs for Peripheral Interventions Reshape the Market Landscape?

From the perspective of incremental market growth, referencing the historical implementation of high-value medical consumable procurement, price reductions driven by volume-based procurement (VBP) generally lead to an increase in surgical volumes. Given that the penetration rate of peripheral interventions has remained consistently low, this growth is likely to be even more pronounced. According to IQVIA data, there are approximately 40 million patients with lower extremity arterial disease and around 100 million patients with varicose veins in China, among whom 5 million and 15 million, respectively, are symptomatic. Although the prevalence base for peripheral vascular diseases is substantial, the total annual number of peripheral intervention procedures remains below one million.

Industry experts pointed out: "Many diseases in the field of peripheral intervention are non-fatal, and related surgeries are mostly preventive treatments. In the past, high product prices have limited the improvement of clinical penetration rate to some extent."Referencing the post-volume-based procurement (VBP) market growth observed in coronary stents, neurointerventional devices, and orthopedic artificial joints, surgical volumes generally increased by approximately 30% following the implementation of VBP.Furthermore, from the supply side of surgical services, there is an ample number of medical centers and specialists equipped to perform peripheral interventional procedures. Therefore, it is foreseeable that there will be significant room for increased market penetration of peripheral interventions following the implementation of volume-based procurement.

However, whether the peripheral intervention market can achieve its projected growth remains to be further validated by the market. In addition to volume-based procurement policies, other policies with significant impacts on the industry ecosystem, such as the nationwide rollout of the Sanming healthcare reform model, will also exert multifaceted influences on market growth.”

How Will Intensive Volume-Based Procurement Reshape the Existing Peripheral Intervention Market Landscape? The Shift in the Existing Market Landscape Primarily Centers on the Competition for Market Share Between Foreign and Domestic Companies.

Prior to the volume-based procurement (VBP), the peripheral intervention market was dominated by foreign companies. According to IQVIA data, multinational corporations held approximately 61% of the peripheral intervention market share in 2022, while domestic enterprises accounted for about 39%. So, what changes will occur in the market landscape following the implementation of large-scale volume-based procurement for peripheral interventions in 2024?

Overall, foreign-invested enterprises have actively participated in centralized procurement, with price reductions exceeding expectations, and they continue to maintain their competitive advantage post-procurement.Recent volume-based procurement declaration data clearly indicate that, in the peripheral vascular market, although domestically produced products have begun to emerge, the majority of the market remains dominated by foreign companies.

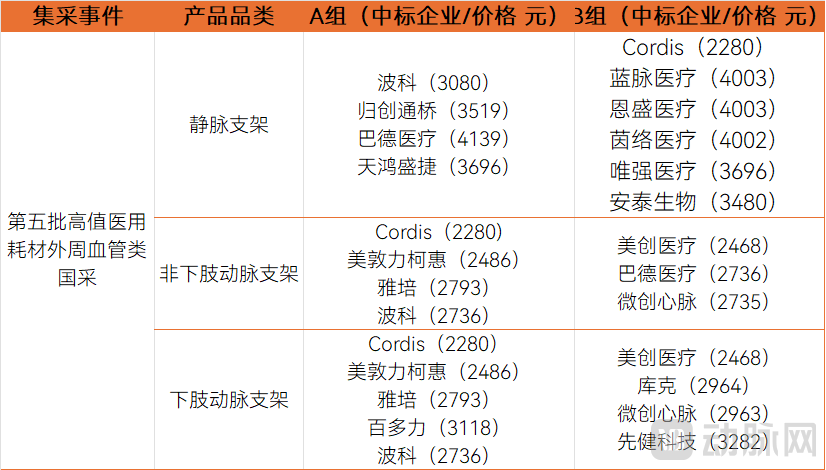

In centralized procurement, foreign companies have reduced prices beyond expectations. During the centralized procurement of peripheral interventions, most multinational corporations actively participated and demonstrated more competitive advantages in pricing. Taking Cordis as an example, in the fifth batch of national consumables procurement, Cordis submitted the lowest bid of 2,280 yuan for its arterial stents, a winning price lower than those quoted by several domestic manufacturers.

Results of the Fifth National Centralized Procurement of High-Value Medical Consumables for Peripheral Intervention

Zhu Chao, Board Secretary of Batai Medical, stated: “In the recent three rounds of centralized procurement for peripheral interventions, a common trend has emerged: foreign companies have shown a clear willingness to reduce prices, thereby driving further downward pressure on the pricing system. Foreign enterprises are adopting defensive strategies to maintain their existing market share. Competition in the established market will become more intense.”

Foreign-funded enterprises have relatively lower prices, while domestically produced products have higher winning bid prices, which indirectly reflects a significant improvement in the competitiveness of domestic products.This indicates that domestically produced products have gained market recognition in terms of product quality."Core domestic enterprises have secured contracted volumes at relatively favorable price levels, while also gaining opportunities to allocate incremental volume. A relatively robust pricing structure implies that domestic firms enjoy greater profit margins to support product quality, R&D investment, and product iteration, thereby fostering a virtuous cycle of development for Chinese manufacturers."

We can also see that in specific markets, such as peripheral guiding sheaths and venous stents, domestic companies are expected to expand their market share through volume-based procurement.Taking peripheral catheter sheaths as an example, in the historical reported volumes for the Hebei Provincial Alliance’s centralized procurement, Cook Medical, the top-ranked company, accounted for 60% of the agreed volume; the second-ranked domestic manufacturer, Batai Medical, accounted for 30%; and the third-ranked Huitai Medical accounted for approximately 15%.

Zhu Chao stated, “After years of iterative refinement, Batai Medical’s guiding sheaths have gained widespread recognition through large-scale clinical use. Through our own efforts, we have already captured a 30% market share, and we are poised to secure over 50% of the market following the implementation of centralized volume-based procurement.”

Whether for foreign-invested enterprises or domestic manufacturers, volume-based procurement is fair to all types of companies, ultimately testing product competitiveness and supply stability. Currently, some products from domestic manufacturers still lag behind top-tier imported products in terms of performance and quality. Therefore, for conventional products, domestic companies need to make efforts in ensuring quality, optimizing manufacturing processes, and driving iterative upgrades.

Wang Yonggang, General Manager of Tianhong Shengjie, stated, “Volume-based procurement essentially places all companies on a level playing field. For domestic enterprises, it lowers the threshold for hospital market access; for multinational corporations, it mitigates the impact of policies promoting domestic substitution. Ultimately, industry competition will return to its core essence, testing quality management systems, supply chain stability, and service reliability.”

Against the backdrop of volume-based procurement (VBP) largely covering peripheral interventional products, domestic companies must pursue sustainable development through a dual strategy: actively embracing VBP to capture a larger share of the existing market, while simultaneously introducing innovative products to unlock growth opportunities in emerging markets.

With Mature Products Such as Stents, Balloons, and Access Devices Subject to Large-Scale Centralized Procurement, What Are the Remaining Innovation Directions in Peripheral Intervention?

First, there is a shift in the concept of innovation: innovation should prioritize listening to clinical practice.

Wang Yonggang pointed out: “After twenty years of rapid development, peripheral intervention has entered a mature phase, and the evolution of treatment concepts will influence surgical approaches. Taking the United States as an example, due to changes in treatment philosophy, the annual number of inferior vena cava filter implantations has dropped sharply, from nearly 130,000 in 2010 to less than 20,000 today. Therefore, product innovation should focus on meeting clinical needs by leveraging the latest materials, technologies, and processes for iterative improvements. We should not merely focus on imitating new overseas products, because if those overseas products encounter problems during clinical trials, domestic companies pursuing imitation-based innovation may find themselves in a difficult position.”

Secondly, innovation in peripheral interventions needs to focus on large indications and the upgrade and iteration of products with higher usage volumes. The population and disease types in the peripheral intervention market are relatively complex, so the product offerings are also more diverse.

Zhu Chao stated, “A larger pond yields bigger fish. Vascular stenosis represents the most prevalent disease category. Although balloons and stents have been included in the volume-based procurement program, this is precisely due to their substantial usage volume. Therefore, the potential of balloon and stent products should not be underestimated in future innovations in peripheral interventions.”

Specifically in terms of products, specialty balloons represent a highly promising direction for development.In the peripheral vascular device tender led by the First Affiliated Hospital of Zhengzhou University in Henan Province, the maximum bid price for constrained peripheral balloons was set at approximately RMB 7,500. This price not only far exceeds the sub-RMB 1,000 prices seen after centralized procurement of conventional balloons, but also represents a significant increase compared to the RMB 3,000–4,000 range for previous-generation specialized balloons (such as scoring balloons and cutting balloons) following their inclusion in centralized procurement. Due to their superior dilation efficacy, specialized balloons are expected to be widely adopted in the future, potentially replacing conventional balloons on a large scale.

Another direction is multifunctional drug-coated balloonsPeripheral interventions featuring drug-coated balloons for "intervention without implantation" therapy represent a key highlight. As first-generation drug-coated balloons have been included in centralized procurement programs in certain provinces, the development of next-generation multifunctional drug-coated balloons has become a focal area of exploration for domestic enterprises.

Among stents, carotid artery stents deserve attention. It is reported that the annual number of surgical procedures for carotid stenosis exceeds 150,000. Currently, no domestically produced products have been approved, and products from importers have not been updated in the past 20 years, with some products already struggling to meet current clinical development needs.

In addition to products with broad indications, tools for treating complex lesions also warrant attention, such as intravascular lithotripsy (IVL) balloons.

Recently, Boston Scientific acquired Bolt Medical, a developer of laser-induced intravascular lithotripsy (IVL) balloon catheters, with an upfront payment of $443 million. IVL technologies include electrohydraulic shockwave and laser-induced shockwave modalities. Shockwave Medical, the leading representative of electrohydraulic shockwave technology, was acquired by Johnson & Johnson for $13.1 billion in 2024. The limitations of IVL in peripheral interventions are that it is only effective for calcified lesions requiring fracture, not suitable for elastic lesions, and involves relatively large outer profile devices. Laser-induced IVL holds promise for addressing these issues.

An industry insider stated, “In theory, laser-source shockwave balloons offer greater advantages. The shockwaves generated by lasers are more stable, whereas those released by electrodes suffer from energy attenuation. Generally, the lifespan of an electrode-based shockwave balloon catheter is limited to only dozens of uses, while the number of uses for laser shockwave balloons is expected to increase, thereby reducing the cost per use of IVL products. Secondly, the design of the electrode structure limits the catheter’s diameter, which may prevent it from passing through many severely stenotic lesions. In contrast, laser-delivering fiber-optic catheters can be made with smaller diameters, improving crossability.”

Despite multiple rounds of centralized procurement in the peripheral intervention market, both foreign and domestic companies have actively participated, underscoring that this segment remains a highly coveted niche. The procurement results clearly indicate that the companies standing out in this market are invariably those demonstrating excellence in quality system construction and product enhancement. The industry reshuffling driven by centralized procurement has fostered more orderly competition. Following this consolidation phase, companies with stable supply capabilities and robust product quality will undoubtedly capture larger market shares, representing an inevitable trend in the future development of the peripheral intervention market.