End of the Burn Rate Era: Internet Healthcare Emerges from Winter with Sustainable Profitability

Recently, with a succession of IPOs and large-scale financing rounds, the spring of internet healthcare has returned.

As the period of policy dividends comes to an end, achieving self-sustaining “blood-making” capabilities and ultimately turning a profit has become the core mission for internet healthcare companies. Among the nine enterprises that have disclosed financial data in the past six months, five have already achieved profitability based on adjusted net profit. For those still unprofitable, losses are gradually narrowing, marking a significant improvement compared with the “cash-burning” deficits of hundreds of millions or even over one billion yuan annually seen in previous years.

Currently, companies are increasingly focusing on their core businesses, divesting operations with low synergy and low gross margins. Leveraging their pivotal role in the out-of-hospital market, newly explored business lines are beginning to show results, and the industry is gradually improving in terms of commercial value.

The notion that internet healthcare can only survive by selling drugs has become a entrenched mindset within the industry. However, an examination of the business structures and revenue sources of various companies reveals that pharmaceutical e-commerce is no longer the sole pillar of scaled revenue for internet healthcare. This is mainly reflected in two aspects:

First, more companies derive their primary revenue from non-pharmaceutical e-commerce.

In the first half of 2024, among Ping An Health’s three major business segments, medical services accounted for 51% of revenue and health services accounted for 47%, demonstrating outstanding performance contribution. In terms of payers and service offerings, Ping An Health provides comprehensive scenario-based medical, health, and elderly care services to F-end clients (integrated financial customers) and employee health management services to B-end clients (corporate customers). Strategic business revenue from the F-end and B-end together accounted for approximately 87.3% of total revenue.

In the business segments of Xikang Cloud Hospital, medical service revenue accounted for 48.9% and health management services accounted for 37.4% in the first half of 2024. Among these, medical services include online consultations, electronic prescriptions, laboratory and diagnostic tests, and telemedicine services provided in regions where the cloud hospital is implemented, using the urban cloud hospital platform as a carrier. Health management refers to employee health management services provided to enterprises, relying on its self-operated medical institutions.

Health Road, which recently went public, has gradually formed two major business segments: health medical services, and enterprise services plus digital marketing services. Among these, the clients of its enterprise services and digital marketing segment include internet platforms, pharmaceutical and healthcare companies, medical institutions, as well as other enterprises and organizations. Health Road provides them with content services, information technology services, and digital marketing services. Over the past two years, this segment has accounted for more than 70% of its total revenue.

Among numerous enterprises, WeDoctor Holdings is exploring a healthcare service payment model based on capitation and value-based care, generating revenue in its Digital Health Community by tying compensation to the effectiveness of member health management. According to its prospectus, in the first half of 2024, WeDoctor Holdings reported continuing operations revenue of RMB 1.818 billion, representing a year-on-year increase of 107.4%. Of this, revenue from health management membership services provided through the Digital Health Community reached RMB 1.032 billion, accounting for 56.8% of continuing operations revenue and serving as the primary driver of performance growth.

Second, among enterprises that currently rely primarily on pharmaceutical e-commerce as their main source of revenue, the proportion of non-pharmaceutical retail income is gradually increasing, or they are continuously expanding their service offerings or service-oriented products.

In recent years, JD Health has achieved steady growth in overall revenue, with service-based revenue (i.e., online platforms, digital marketing, and other services) growing at a faster rate than revenue from pharmaceutical and health product sales, thereby gradually increasing its share of total revenue. In the first half of 2024, service-based revenue amounted to RMB 4.4 billion, accounting for 15.6% of total revenue; in the first half of 2021, three years prior, these figures were RMB 1.9 billion and 13.9%, respectively.

For a company with annual revenues in the tens of billions, such as JD Health, it is impossible for its revenue structure to undergo fundamental changes in the short term; therefore, shifts in revenue composition should be assessed over a longer time horizon.

Alibaba Health continues to upgrade and iterate its healthcare services, providing integrated online and offline medical and health solutions to users across multiple platforms, including Tmall, Taobao, and Alipay. Notably, businesses such as Xiaolu Zhongyi have maintained steady revenue growth, alongside improvements in service quality and gross profit margins.

Fangzhou Jianke has established a Chronic Disease Management Service Center, playing a pivotal role in providing patients with services such as follow-up consultations, prescription counseling, patient education, medication reminders, and medication refill notifications. Over the one-year period ending June 2024, the repeat purchase rate among paying users remained robust at 85.8%.

Dingdang Health leverages its self-developed AI systems, health knowledge graphs, and medical reference databases to assist users in managing their health records and providing Directly Observed Therapy (DOT) medication adherence services. As its services continue to deepen, Dingdang Health is collaborating with medical institutions to explore the establishment of patient and medical service frameworks, offering disease progression management, remote consultations, and health management tailored to diverse user needs.

Driven by multiple factors—including the expansion of O2O medical insurance drug purchases, online price comparison for medicines covered by medical insurance, and the entry of volume-based procurement (VBP) drugs into retail pharmacies—the pharmaceutical retail market is undergoing a profound transformation.

Over the past two years, medical insurance payment for online drug purchases has been rapidly expanded across many regions. To date, Shanghai, Zhejiang, Liaoning, Guangdong, Sichuan, Beijing, and other areas have launched online medical insurance-covered drug purchasing through various forms on internet platforms. Meanwhile, medical insurance bureaus in many parts of China have introduced price-comparison tools for medication purchases, allowing the public to search by drug name to access information such as available pharmacies, prices, and pharmacy locations. In addition, medical insurance authorities are vigorously promoting the availability of volume-based procurement (VBP) drugs in retail pharmacies. With the implementation of these policies, patients can now purchase VBP drugs at retail pharmacies with zero markup.

All these changes revolve around one core factor: drug prices. The public now has more transparent channels to access drug pricing information, enabling them to choose purchasing channels and platforms based on lower prices (and even insurance reimbursement). For pharmaceutical e-commerce platforms and other retailers, price competition for common drugs has become inevitable.

Of course, physical products such as pharmaceuticals and medical devices, as an indispensable part of meeting healthcare needs, will still account for a significant proportion of revenue on many platforms; but it is certain thatThe expansion of non-pharmaceutical retail business will become a key priority.Even in the pharmaceutical e-commerce sector, while price may be the primary factor for patients, it is not the sole consideration. Delivery timeliness and services related to medication safety are also likely to factor into patients’ decision-making. From this perspective, it is essential to build a differentiated and competitive service model centered around products.

Building on established pillar revenue streams, over the past one to two years, numerous companies have also unearthed new high-growth businesses that have become the driving force behind sustained, scalable performance growth; alternatively, long-explored business lines have undergone a qualitative leap following quantitative accumulation, resulting in surging performance.

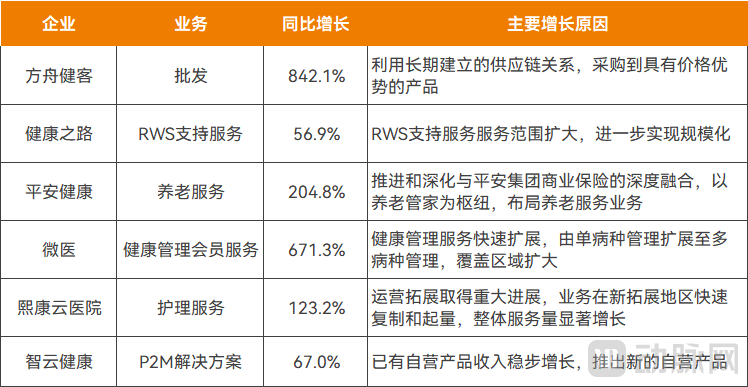

High-Growth Business Segments of Several Internet Healthcare Companies (Based on H1 2024 Data), Source: Company Financial Reports or Prospectuses

Against the backdrop of Ping An Group’s “Integrated Finance + Healthcare and Elderly Care” strategy, Ping An Health has carved out elderly care services as a distinct segment within its managed healthcare offerings. In the first half of 2024, revenue from Ping An Health’s elderly care services surged by 204.8% year-on-year, marking it as a newly added business segment for 2024. Looking ahead, Ping An Health will continue to vigorously develop and expand its home-based elderly care business, while further promoting the deep integration of medical-elderly care services with commercial insurance.

In 2024, Xikang Cloud Hospital also adjusted its business segments, changing from the original cloud hospital platform services, internet medical services, health management services, and smart healthcare products to medical services, nursing services, and health management services. Among these, nursing services, as a new independent segment, saw a year-on-year revenue increase of 132.2% in the first half of 2024. After years of exploration, Xikang Cloud Hospital’s home-based nursing care is currently in a phase of rapid expansion in terms of coverage areas and service offerings.

Furthermore, WeDoctor Holdings’ revenue from health management membership services surged significantly from RMB 134 million in the first half of 2023 to RMB 1.032 billion in the first half of 2024. Benefiting from the significant improvement in diabetes management health indicators achieved by the Tianjin Health Community, WeDoctor Holdings has expanded its capitation and value-based payment models to cover more chronic disease areas, while also extending its multi-disease management service model to additional regions within Tianjin. As of June 30, 2024, the Health Community had covered approximately 900,000 members in Tianjin.

From the perspective of service channels and scenarios, offline channels and home-based settings have become important strongholds for internet healthcare.In the past, internet healthcare platforms have accumulated extensive experience in online service processes, while there remains significant room for growth in offline services and integrated online-offline offerings. On one hand, certain medical services, such as laboratory tests and nursing care, must be conducted in person. On the other hand, amid the trend of population aging, healthcare needs in home settings have become increasingly prominent.

In addition to the performance data already reflected in the related businesses of the aforementioned companies, JD Health has also intensified its offline expansion over the past year or so, particularly by continuously enriching its at-home rapid testing services to complement the laboratory testing component of its online diagnosis and treatment offerings. Currently, JD Health has established a comprehensive library of 396 test items, 147 of which support home sample collection, covering nearly 70% of outpatient and emergency department tests.

Given that internet healthcare platforms have extensively accumulated resources such as patients, physicians, and hospitals, they are particularly critical for pharmaceutical and medical device companies. Leveraging these resources to identify monetization strategies within the pharmaceutical supply chain or to address the in-depth needs of pharmaceutical and medical device enterprises represents one of the key pathways for internet healthcare platforms.

For example, since launching its P2M (Patient-to-Manufacturer) strategy in 2023, Zhiyun Health has seen significant growth in revenue from its P2M solutions. Under this strategy, Zhiyun Health collaborates with pharmaceutical companies to sell proprietary products for which it holds ownership, sales rights, or other exclusive rights, positioning these offerings as an upgraded version of precision marketing. In the first half of 2024, the proprietary products in this business line primarily included Yishujialin and Hetangjing (Dapagliflozin Tablets). Driven by the steady revenue growth of Yishujialin and the launch of Hetangjing, the P2M solutions generated RMB 107 million in revenue, representing a 67% year-on-year increase, and also yielded a certain amount of net profit.

Furthermore, Fangzhou Jianke leveraged its long-established supply chain relationships to aggressively expand its wholesale business in the first half of 2024, driving a significant surge in revenue for this segment.

Health Road, through its collaborations with pharmaceutical and medical device companies, identified their demand for real-world studies. Leveraging its accumulated expertise in medical research and its extensive resources connecting physicians and patients, the company launched its Real-World Study (RWS) support services. These services collect real-world clinical data to observe and analyze real-world clinical evidence, thereby assisting pharmaceutical companies and other entities in researching drugs and other medical products. Since its launch in 2022, the RWS support services have seen continuous growth in customer base, service volume, and revenue, with revenue reaching RMB 268 million in the first half of 2024, a year-on-year increase of 56.9%.

Whether it is the various services oriented toward users or the business layout for stakeholders in the pharmaceutical supply chain, both further indicate that there are new possibilities for the scalable growth of revenue for internet healthcare platforms.

Currently, companies are increasingly focusing on their core businesses and expanding into new business lines that closely align with the needs of industry stakeholders. Some companies have also disclosed that they have optimized their business structures over the past two years by adjusting or divesting businesses with low synergy with their core operations or low gross margins, thereby shedding redundancies to operate more efficiently.

In the current industry landscape, internet healthcare has become an important component of the medical service system for the general public;For the industry, internet healthcare platforms have become hubs connecting various out-of-hospital services and health-related products, deepening collaboration among stakeholders such as medical professionals, pharmaceutical and device manufacturers, and insurers, and even facilitating the reshaping of the out-of-hospital market.

Not only listed companies, but also the development paths of other enterprises have shown the aforementioned trends.

In 2025, Haodf Online officially announced its integration into Ant Group. Alipay will further leverage its platform connectivity to link 800 million patients with 280,000 Haodf physicians. It will also actively promote innovation in the commercial health insurance system, integrating superior innovative pharmaceuticals and medical devices with Haodf’s high-quality services.

Weimai, which recently secured a new round of financing, is also focusing on out-of-hospital care. By providing whole-course disease management, it aims to meet the public’s multi-level, diverse, and personalized healthcare needs, thereby addressing the lack of continuous out-of-hospital services.

From simple online consultations to comprehensive, end-to-end service ecosystems, and from enhancing convenience for patients and physicians to deep integration into the healthcare industry chain, internet healthcare has undergone a long evolution. Although industry enthusiasm has waned in the past two years, leading enterprises have remained steadfast in their original mission to drive innovation in the medical service system. As these companies demonstrate improved profitability and achieve stronger commercial viability, time has provided the most compelling validation.