2024 Global Healthcare Investment and Financing Analysis Report – Prospectus Summary

In 2024, the capital winter sweeping through the global healthcare investment and financing market entered a critical phase. Limited funds increasingly flowed toward projects with clear market expectations, while conceptual technological innovations no longer attracted strong interest from professional investors or even the general public.

This report, produced by VCBeat, provides an in-depth analysis of over 2,000 global healthcare investment and financing cases in 2024. By integrating global investment and financing data from the past decade, it meticulously portrays the full landscape and subtle shifts of global medical innovation funding in 2024 across multiple dimensions, including sub-sectors, transaction size, frequency, project stage, investing institutions, and geography.

Although innovation remains a central theme in the global healthcare sector, with related initiatives continuing to attract substantial capital investment, institutional investors have shifted their focus from pursuing technological breakthroughs alone to prioritizing projects with higher certainty.

Core Viewpoints

I. The global healthcare industry’s capital-raising capacity stabilized in 2024, showing a slight rebound after a sharp decline in 2023.

II. Financing is dominated by small- and medium-sized transactions with individual amounts below US$100 million; deals exceeding US$100 million account for only 7% of the total.

3. Over an extended observation period, market trading activity remains at historically high levels, causing the average transaction size to approach historical lows; as a result, investment institutions are inclined to adopt more prudent investment strategies.

IV. The deep integration of artificial intelligence and biotechnology is directing mainstream venture capital in the healthcare sector toward innovative biomedical projects.

V. Venture capital is becoming increasingly prudent, favoring innovative companies that strengthen their product lines through asset acquisitions and industry mergers and acquisitions to achieve deterministic growth.

VI. The scale of healthcare IPOs has shrunk again, with some Chinese companies turning to the Hong Kong stock market as a secondary option; healthcare innovation enterprises urgently need to broaden their financing channels and establish more extensive exit mechanisms.

VII. Many regions across China are intensifying efforts to cultivate the biopharmaceutical industry, while the Yangtze River Delta, as a national hub for medical innovation, continues to demonstrate significant locational advantages.

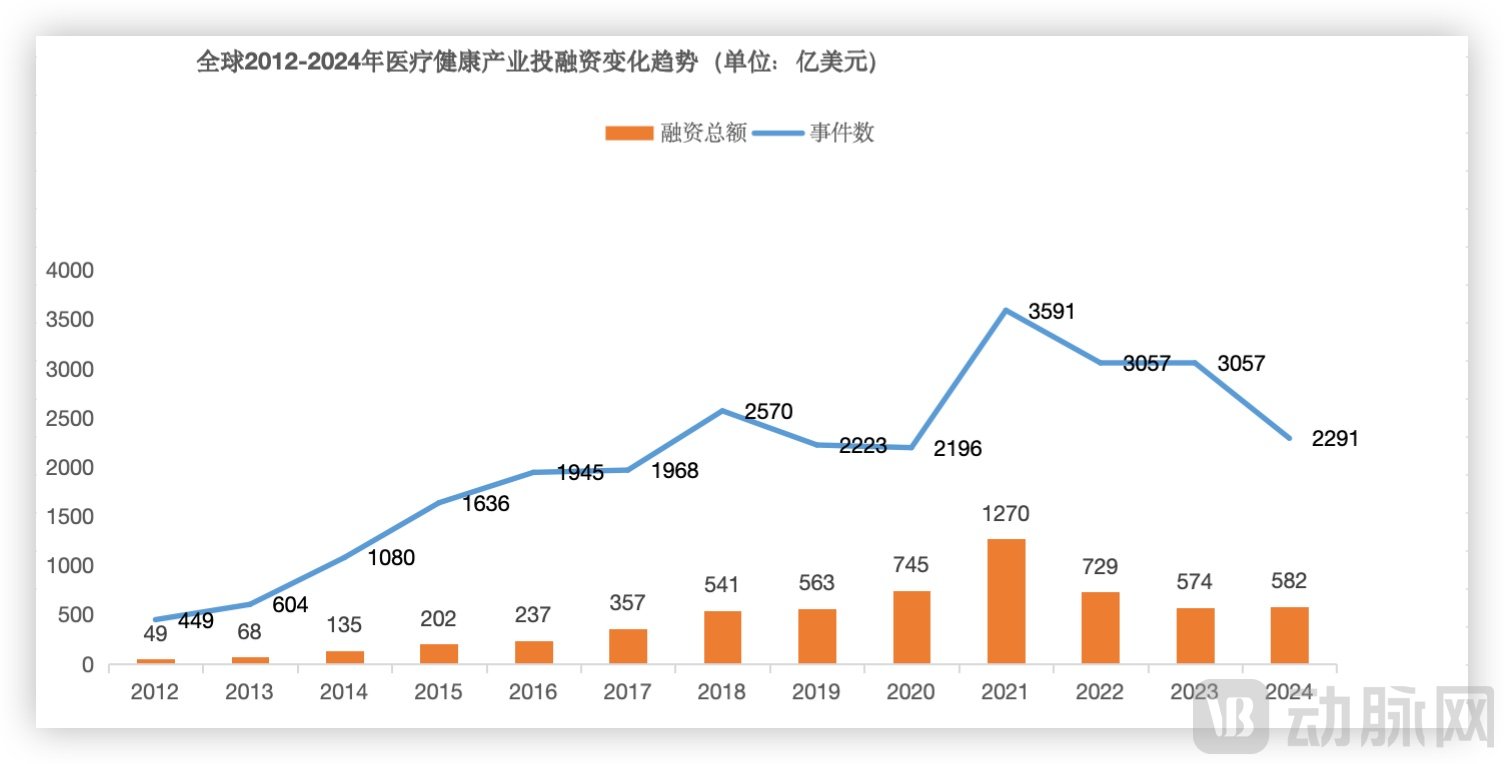

2012–2024 Global Healthcare Industry Financing Trends

Global Healthcare Investment and Financing Stabilizes After Two Years of Decline.

In 2024, a total of 2,291 primary market investment deals were completed globally in the healthcare sector, with cumulative financing reaching $58.2 billion. The total financing amount saw a slight increase of 1 percentage point compared to 2023, but the number of financing events dropped significantly by 25%, from 3,057 in 2023 to 2,291. The capital winter continues.

Global Trends in Healthcare Industry Investment and Financing, 2012–2024; Data Source: VBInsight

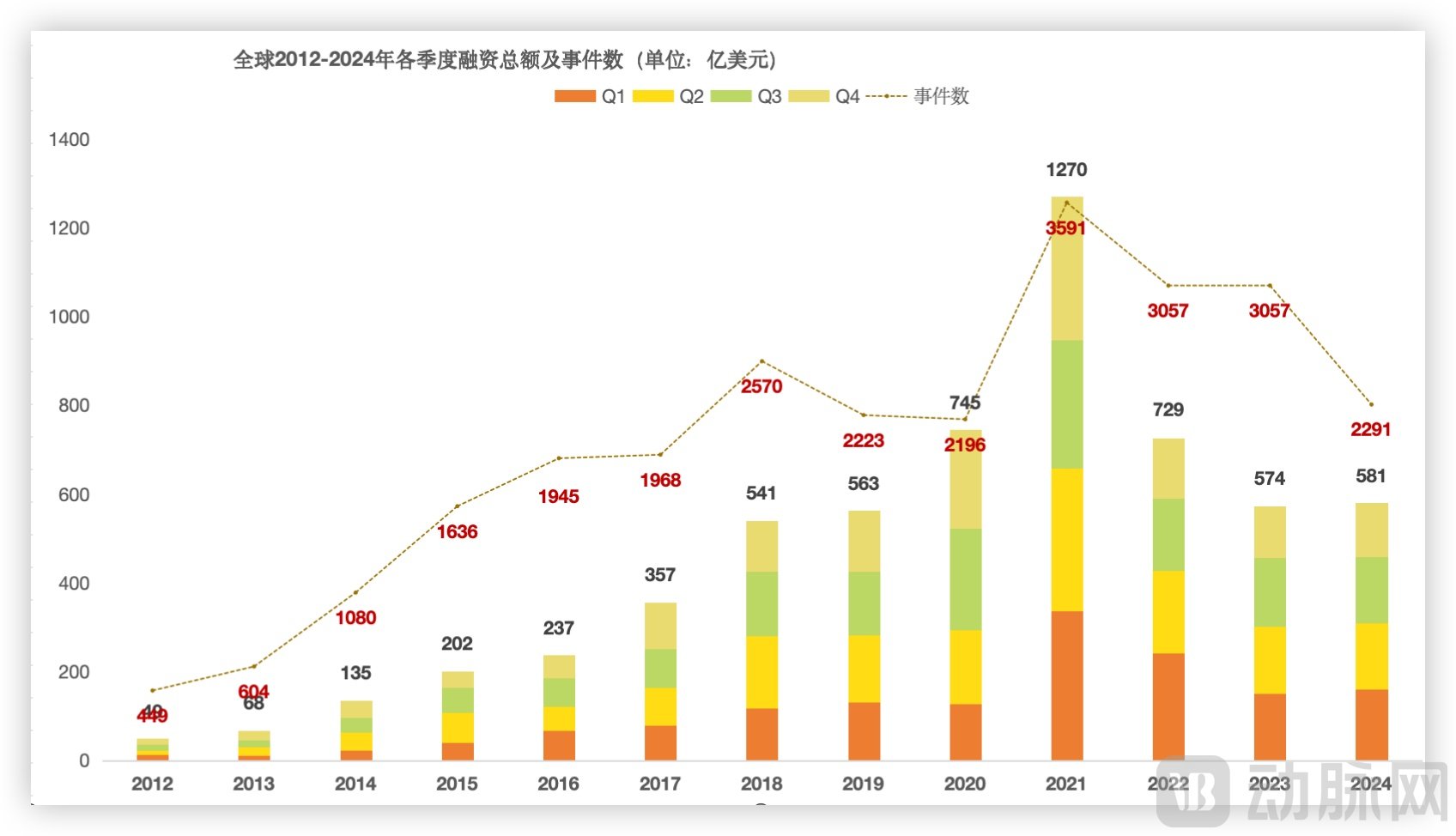

A quarterly review reveals that seasonal fluctuations in global healthcare investment and financing have tended to flatten. Since 2012, primary market investment and financing activities in this sector have often been concentrated in specific quarters, particularly in sub-sectors such as biopharmaceuticals and medical devices, which typically saw clusters of activity in the first and third quarters, thereby driving a corresponding increase in transaction frequency. However, from 2023 to 2024, the correlation between such activities and specific quarters has significantly weakened, further diminishing seasonal disparities in global healthcare primary market investment and financing.

Total Financing Amount and Number of Deals by Quarter Worldwide, 2012–2024; Data Source: VBInsight

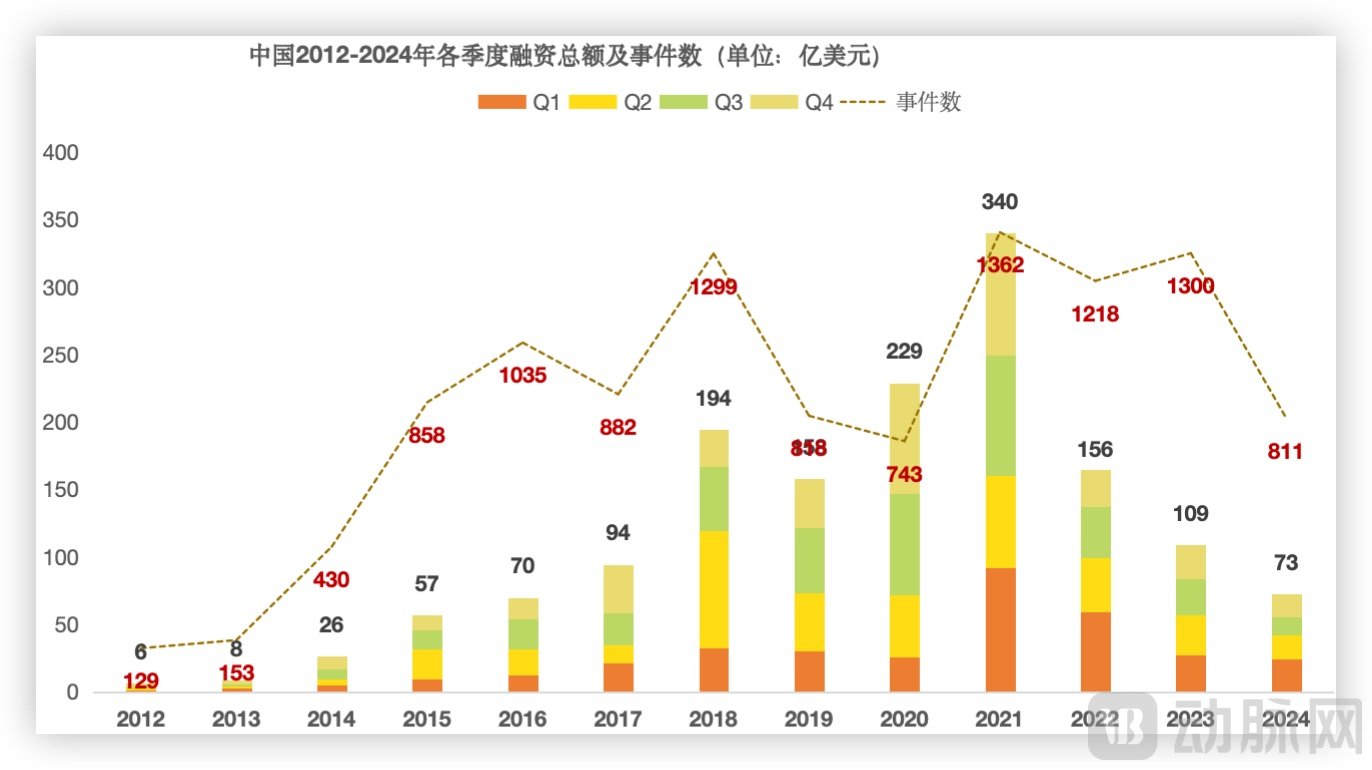

In 2024, the primary market for China’s healthcare industry completed a total of 811 financing transactions, attracting $7.3 billion in capital into innovative explorations. Following the investment and financing peak in 2021, funding in this market has continued to decline. In 2024, the total domestic financing amount decreased by 33% compared to 2023, while the number of financing events also dropped by 37.6%.

Following the cessation of growth in global primary market investment and financing for healthcare, China’s sector has inevitably entered a sustained downturn, with total transaction volumes retreating to levels seen between 2015 and 2016. A comprehensive analysis of global and domestic investment data reveals that the healthcare industry faced the full brunt of a capital winter in 2024. Concurrently, global healthcare venture capital strategies have shifted from prioritizing innovative potential to favoring mature projects with greater certainty. This transition has undoubtedly exerted a widespread impact on healthcare innovation projects worldwide.

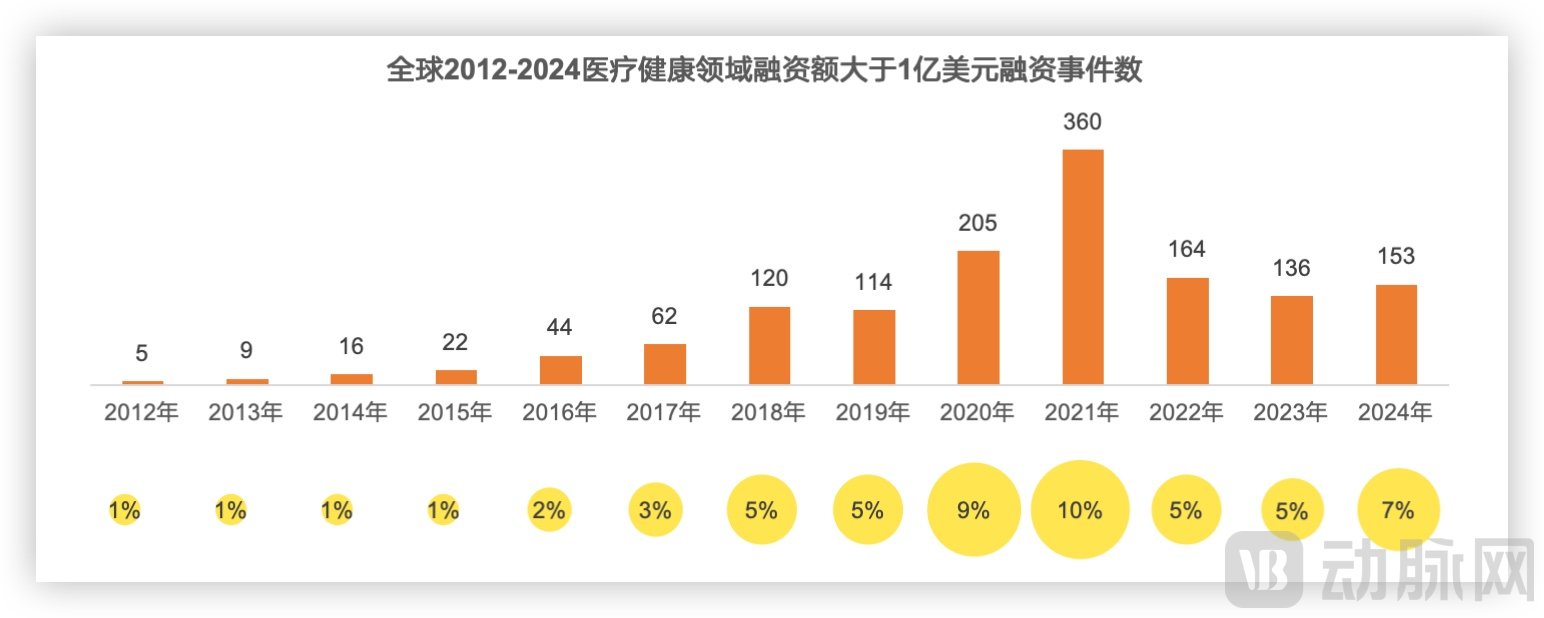

In 2024, the number of large-scale transactions (exceeding $100 million) increased by 12.5%. Globally, there were a total of 153 such financing deals in the primary healthcare market throughout the year, accounting for nearly 7% of all financing events.

After two consecutive years of decline, global primary market financing and investment in healthcare stabilized in 2024. Notably, the number of late-stage financing deals decreased significantly compared to previous years; however, projects with high certainty continued to attract strong interest from investors, even at later stages.

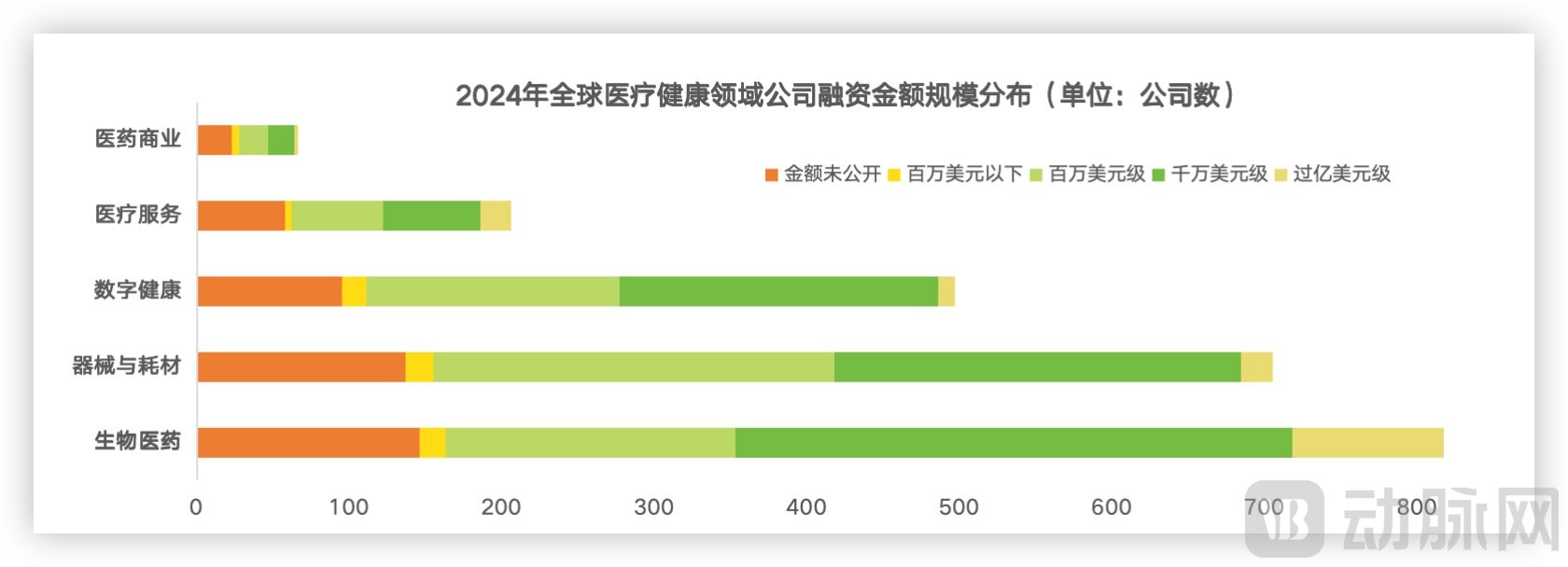

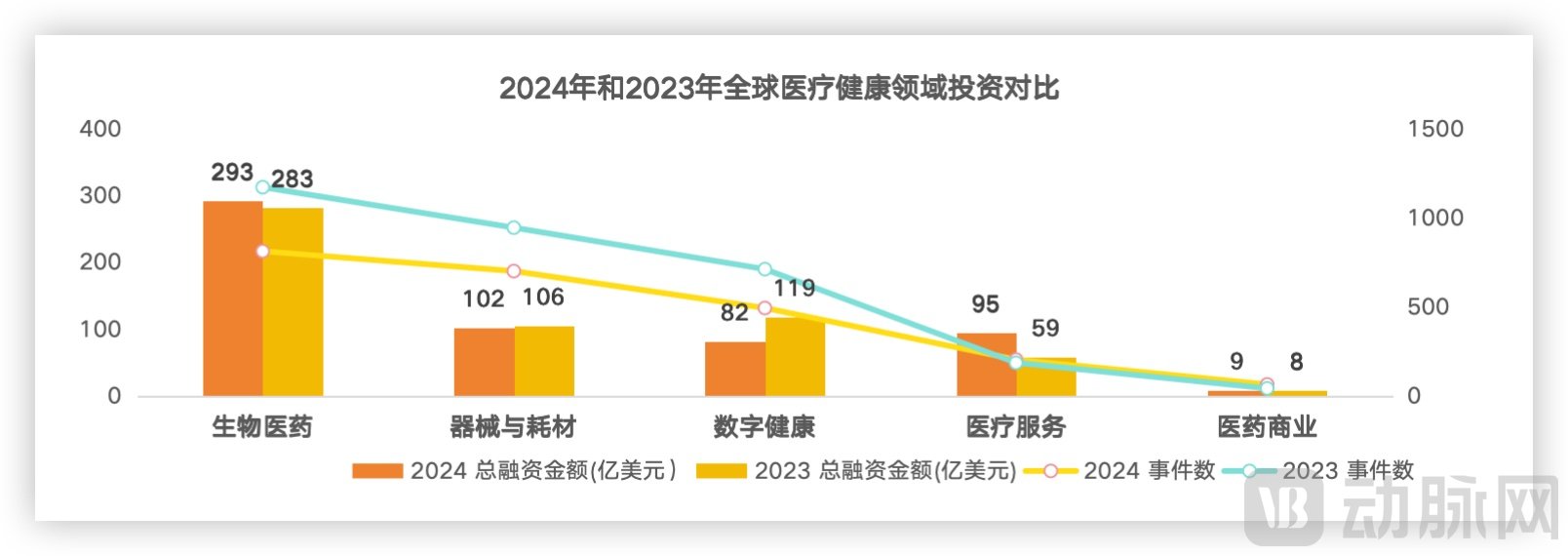

In 2024, biopharmaceutical projects ranked first in both the scale and activity of investment and financing transactions, with medical device and consumable projects following closely. Notably, financing deals exceeding $100 million in the biopharmaceutical sector far outnumbered those in other subsectors, demonstrating a significant lead.

Hot Areas in Global Healthcare Investment and Financing in 2024

Volume Growth and Price Decline in Medical Device Projects; Digital Health Transaction Scale Continues to Shrink.

Compared with 2023, the total financing amount for biopharmaceutical and pharmaceutical commerce projects saw a slight increase in 2024, while the number of transactions rose significantly, leading to a further decline in the average transaction size. This underscores the continued strategy of venture capital funds to pursue early-stage, small-ticket investments in these segments.

Meanwhile, the average deal size for digital health projects has shrunk again compared to 2023. Reviewing investment and financing trends over the past few years, global digital health investment has continued to cool down after the pandemic-driven frenzy. Not only has it become more difficult for early-stage projects to secure funding, but projects in later stages are also facing financing challenges.

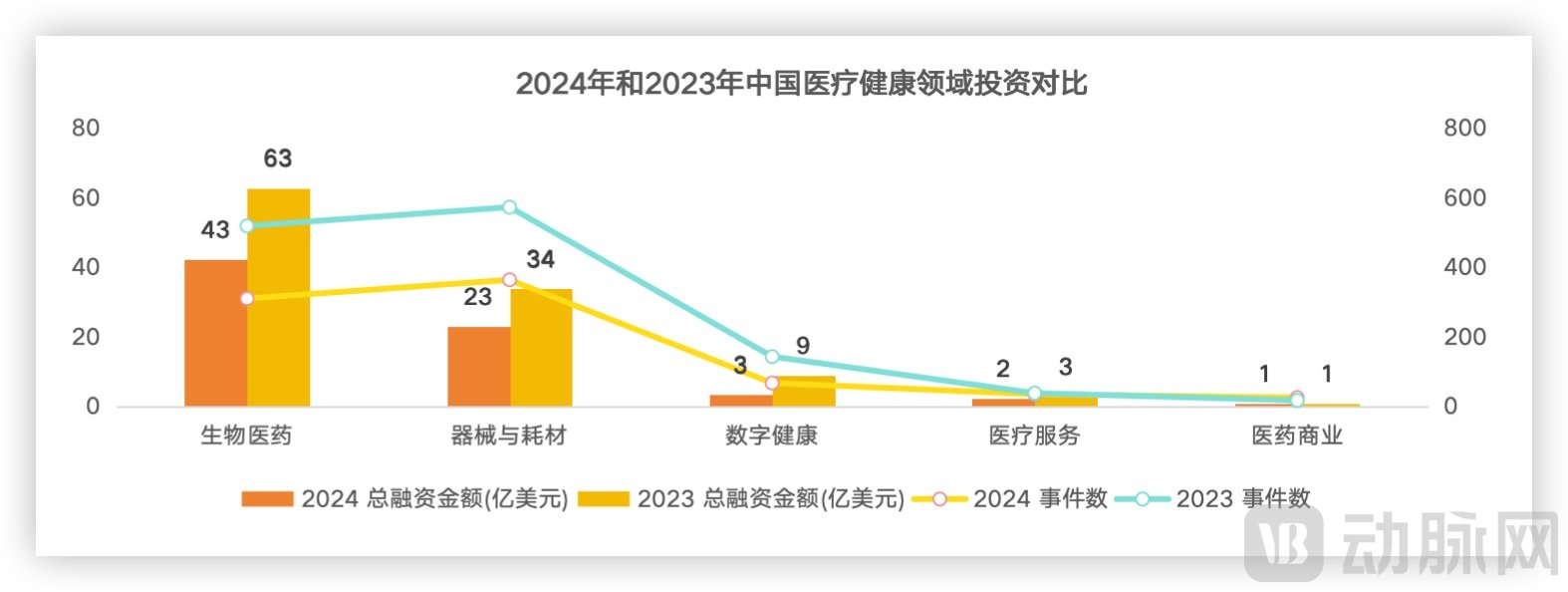

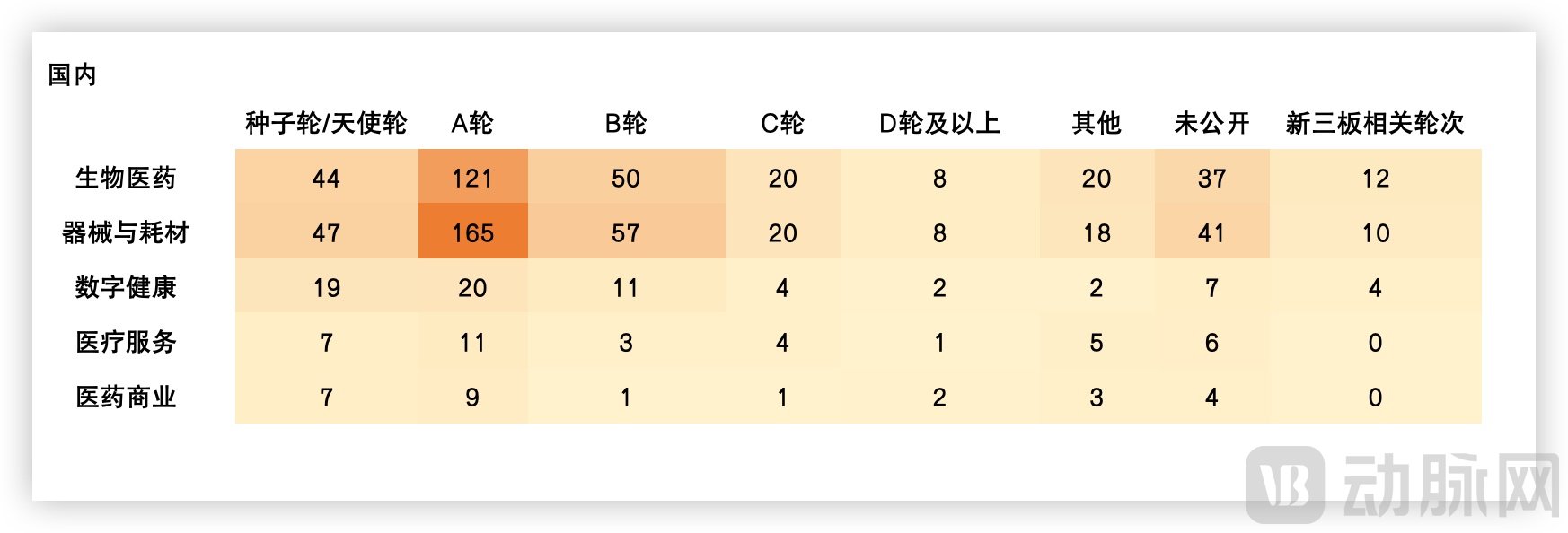

In China, the total investment and financing amounts and transaction frequencies across various sub-sectors in 2024 declined compared to 2023, aligning with global market trends. Notably, the average deal size in China’s sub-sector investment and financing markets decreased more sharply than the global average, highlighting the increasingly cautious stance of investment institutions when making decisions regarding domestic innovative health enterprises.

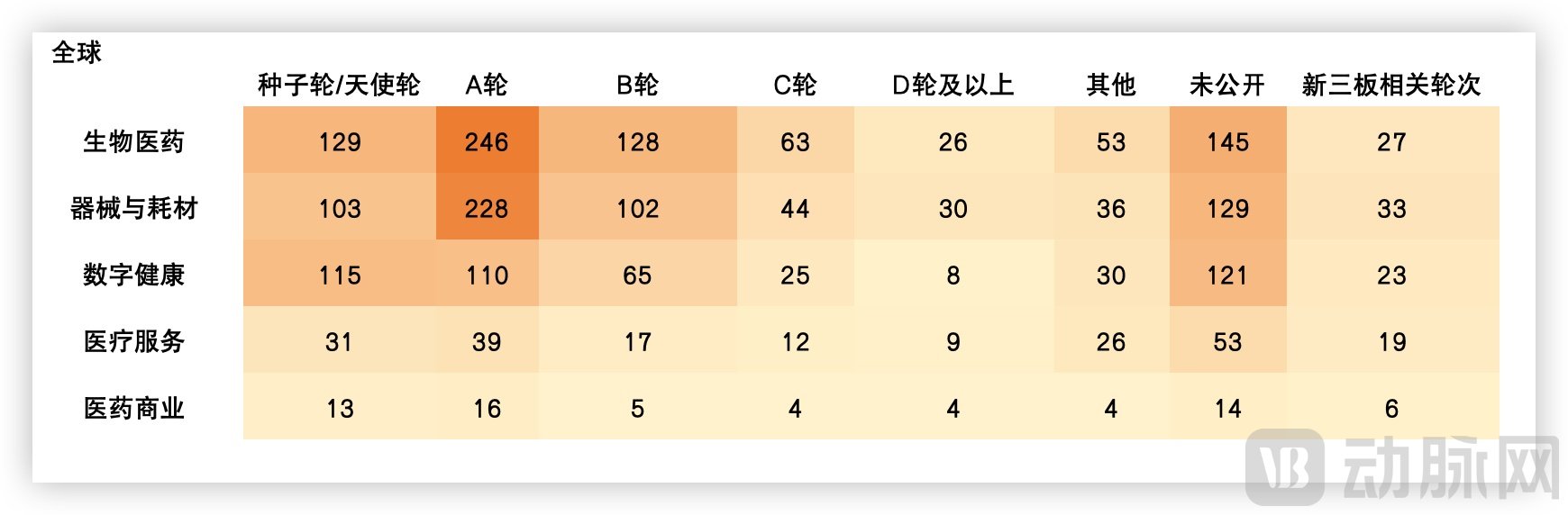

In 2024, within the global primary healthcare market, excluding rounds with undisclosed financing details, investment activity was significantly skewed toward Series A projects, which accounted for a substantial 28% of all transactions. Meanwhile, biopharmaceutical and medical device/consumable projects also saw active trading in Series B and seed rounds. Notably, the biopharmaceutical sector maintained a leading position across all funding stages except for IPOs.

In 2024, among the financing deals completed by global companies in the sectors of biopharmaceuticals, medical devices and consumables, digital health, healthcare services, and healthcare commerce, the proportions with undisclosed funding rounds were 17.7%, 18.3%, 24.3%, 25.7%, and 21.2%, respectively. Constrained by stagnant valuations, an increasing number of domestic innovative enterprises have adopted “+” and “++” round designations.

In China, the distribution of investment rounds in the healthcare primary market in 2024 was similar to that of the global market, with only slightly lower frequencies of seed and angel round transactions compared to the global average.

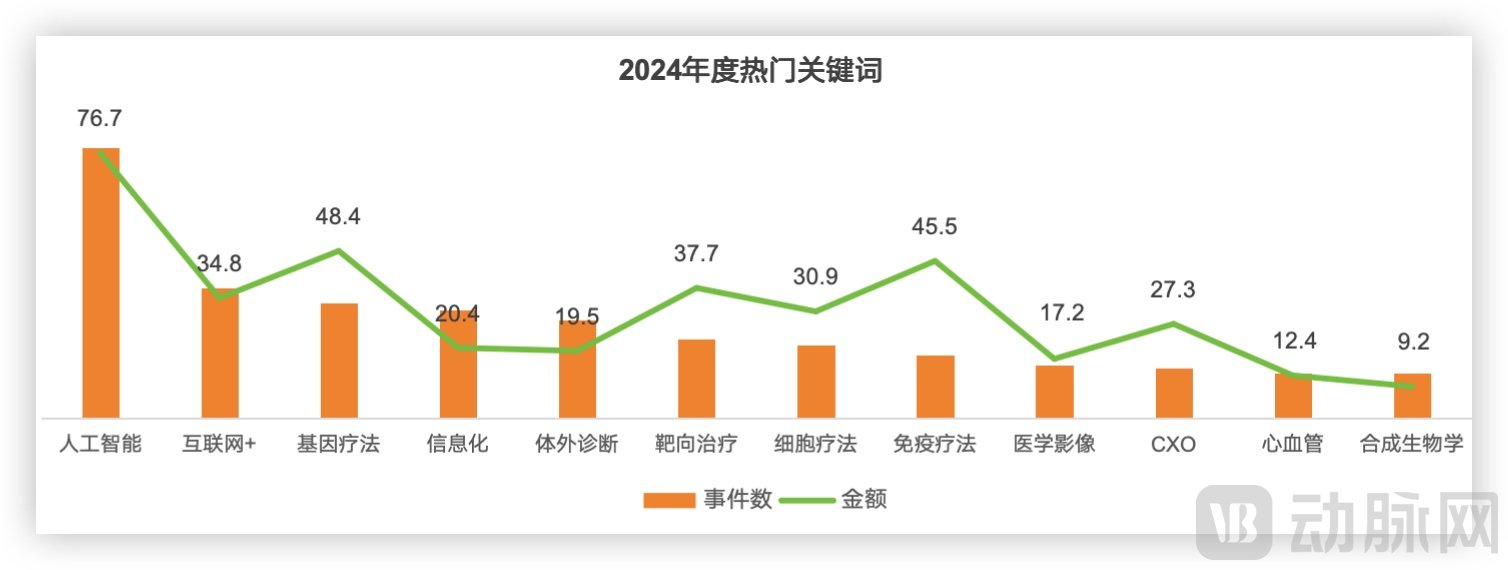

As industry opportunities emerged, artificial intelligence topped the list of hot keywords for investment and financing in 2024, surpassing last year’s “Internet+.” Meanwhile, traditional buzzwords such as Internet+, CGT (Cell and Gene Therapy), informatization, medical imaging, and CXO continue to rank highly in the global healthcare innovation sector. Niche segments that have attracted significant attention since 2021, including digital therapeutics and surgical robots, showed a marked decline in 2024. Notably, with accelerated technological iteration in the global biopharmaceutical field, emerging technologies such as gene therapy and cell therapy are coming to the forefront, becoming new hot keywords in the investment and financing market.

Xaira Therapeutics, which is reshaping drug discovery with its “AI + protein” technology, claimed the top spot globally for healthcare innovation project financing in 2024, securing a $1 billion seed round. In contrast, healthcare service providers, which attracted significant attention in 2023, saw a relatively quieter performance in 2024. Notably, biopharmaceutical companies occupied multiple positions in the top ten rankings.

Top 10 Global Healthcare Industry Financing Deals of 2024 | Data Source: VBInsight

In China, the top 10 annual financing list is dominated by biopharmaceutical projects.

Shenzhen Luye Pharma, ranking first, has over 30 marketed products covering therapeutic areas such as oncology, the central nervous system, cardiovascular diseases, and digestion and metabolism. This investment will provide more ample cash flow for R&D, aiming to upgrade innovative drugs to "best-in-class" and "first-in-class" categories, and strengthen the development of next-generation innovative anticancer drugs.

Top 10 Financing Deals in China’s Healthcare Industry in 2024 | Data Source: VBInsight

Among the top 10 global biopharmaceutical financing deals, AI-driven drug discovery, weight-loss medications, and autoimmune disease therapeutics have stood out. Meanwhile, gene therapy, immunotherapy, and targeted therapy projects have also attracted significant capital interest.

Top 10 Global Biopharmaceutical Financing Deals in 2024 | Data Source: VBInsight

Among these, the biopharmaceutical projects that secured financing are largely focused on cutting-edge biotechnologies, such as gene editing and cell therapy. They are committed to developing highly targeted and efficient therapeutic products aimed at tackling diseases that are difficult to address with conventional therapies, thereby providing patients with innovative treatment options and striving to achieve transcendence and breakthroughs within the industry.

In China, oncology drugs continued to play a significant role in the biopharmaceutical financing deals ranked in 2024.

Top 10 Biopharma Financing Deals in China in 2024 | Data Source: VBInsight

In contrast to U.S. innovation initiatives, which prioritize drug development and biotechnology, China has a larger number of pharmaceutical manufacturers, with many projects focusing on production, sales, and manufacturing. This trend may be attributed to the country’s solid manufacturing foundation and reflects the strong capabilities of China’s healthcare industry in the mid- and downstream segments of the value chain. Achieving continued breakthroughs in upstream innovative R&D would further consolidate China’s position in the global pharmaceutical industry.

In the medical device sector, the total financing volume for the top ten deals globally in 2024 was lower than that in the biopharmaceutical sector; indeed, the largest single financing amount in medical devices did not even rank among the top ten globally in biopharmaceuticals. The two subsectors of brain-computer interfaces and high-value consumables continued to maintain robust growth momentum.

Top 10 Global Medical Device Financings in 2024 | Data Source: VBInsight

Notably, significant achievements have been made in fields such as wearable devices and in vitro diagnostic (IVD) instruments. In particular, the aging population, the rising number of patients with chronic diseases, and heightened health awareness have driven growing demand for precision, convenience, and intelligence in medical devices, thereby fostering innovation and investment in this sector.

In China, Blue Sail Medical (Biosensors) secured the largest financing amount in 2024. The company is primarily engaged in the research and development, production, and sales of cardiovascular and cerebrovascular consumables. Meanwhile, the top two high-value medical device companies on the list led the rest of the projects by a wide margin in terms of financing amounts, which to some extent reflects the current preference of capital for projects with greater certainty.

Top 10 Medical Device Financings in China in 2024 | Data Source: VBInsight

In addition to the three companies listed on the form, several other enterprises—including Medico Technology, Tupai Medical, Saiqiao Bio, Tuge Medical, Waterthene Electronics, Baikelin, Chaoqun Testing, Guozi Robotics, Shenzhen Hannuo, New E Biotech, and Suzhou Elite—also secured financing in the range of RMB 200 million.

In 2024, the number of companies that completed two or more investment rounds decreased to 145, representing a nearly 40% decline from the 238 companies recorded in 2023. In the same year, the number of companies securing more than two financing rounds dropped to 10, down from 20 in 2023, marking a 50% decrease.

Companies That Completed More Than Two Rounds of Financing in 2024, Data Source: VBInsight

From a sector-specific perspective, biomedicine has emerged as the core area for multiple financing rounds; however, the overall funding amount remains relatively low, with only one company securing over $100 million in financing.

Review of Healthcare IPOs Listed in 2024

IPO Pace Slows Further, with U.S. Companies and Capital Markets Becoming the Main Force

In 2024, the pace of global healthcare companies entering the capital markets continued to slow, with only 162 firms completing initial public offerings (IPOs) throughout the year, a 7% decrease from 2023. Among these 162 healthcare IPOs, 106 companies were from the United States, accounting for 65%, while Chinese companies numbered 29, ranking second but representing a 44% decline compared to the 52 Chinese firms that went public in 2023.

2024 IPO Hot Words, Data Source: VBInsight

In 2024, the company that raised the most capital through an initial public offering (IPO) globally was Waystar, a U.S.-based healthcare information technology company. This IPO also marked one of the largest listings in the digital health sector since 2022. Waystar specializes in providing SaaS solutions for revenue cycle management to healthcare providers, aiming to optimize medical insurance reimbursement processes and streamline operations.

Top 10 Healthcare IPOs by Financing Amount Globally in 2024, Data Source: VBInsight

In China, XtalPi ranked first in IPO fundraising amount in 2024. The company successfully listed under Chapter 18C of the Hong Kong Stock Exchange’s new listing rules for specialized and sophisticated technology companies, setting a precedent as the first publicly traded stock in the AI-driven drug discovery sector. In contrast to 2023, when four Chinese enterprises made it into the top ten of the global IPO fundraising rankings, no Chinese company secured a spot in the top ten in 2024. Furthermore, the highest domestic IPO fundraising amount this year was only USD 115 million, which did not even qualify for the top ten domestic IPOs of 2023 (USD 148 million).

Top 10 Healthcare IPOs in China by Financing Amount in 2024, Data Source: VBInsight

Analysis of Active Healthcare Investment Institutions in 2024

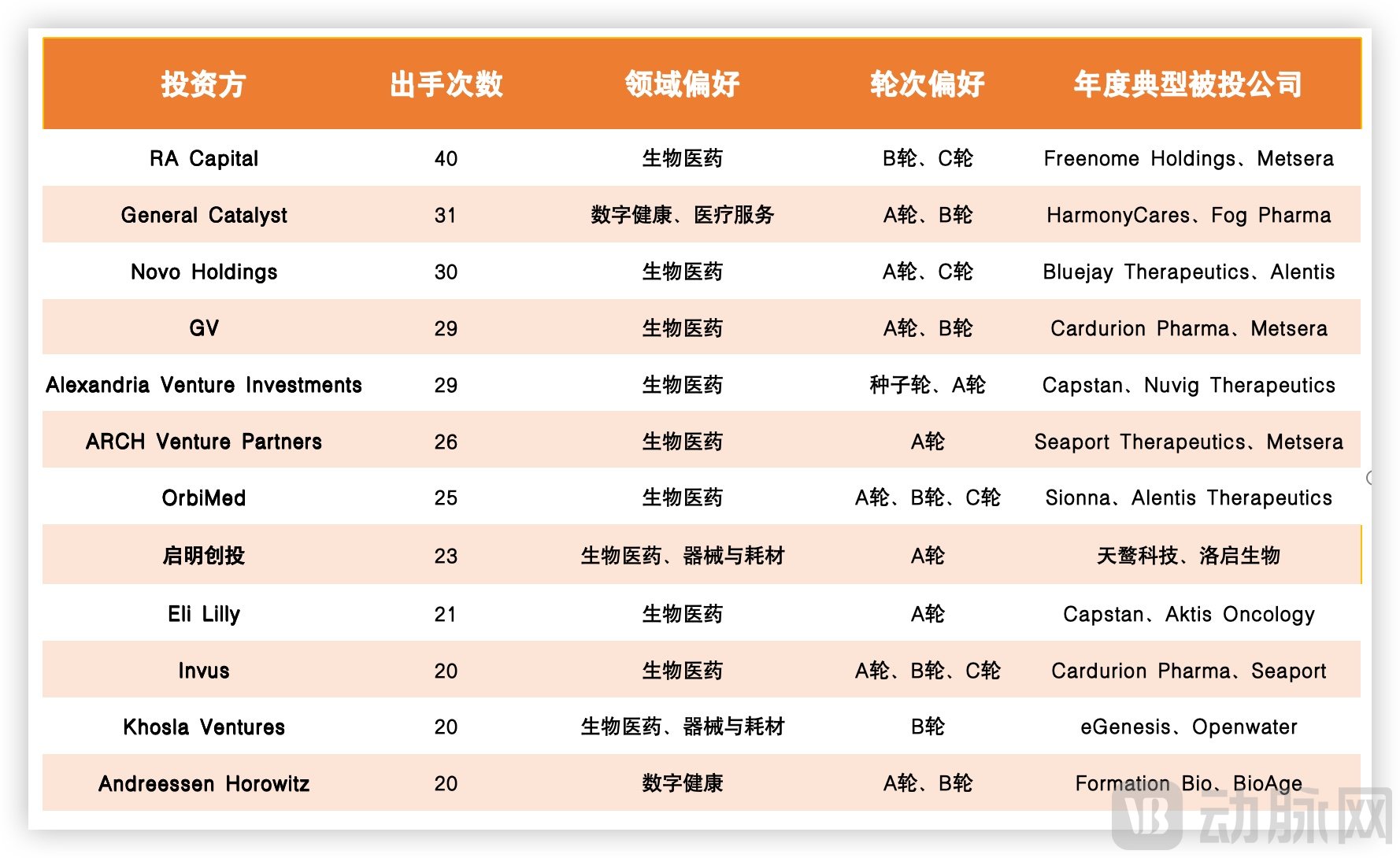

RA Capital has made a total of 40 investments, with biopharmaceuticals drawing the most attention.

In 2024, RA Capital was the most active institution in the global healthcare sector, with a total of 40 investments throughout the year. Notably, it made 33 investments in the first half of the year, while only 7 in the second half. RA Capital clearly favors the innovative drug sector, with a particular focus on antibody drugs and anti-tumor drugs.

Top 10 Most Active Investment Institutions in the Global Healthcare Industry in 2024, Data Source: VBInsight

In recent years, the strategy of investing in early-stage and small-scale ventures, advocated by domestic investment institutions, has not been prominently reflected among globally active investors. Many firms remain keen on companies with stable growth or those already in a relatively mature stage, with some even increasing their stakes in listed companies.

The biopharmaceutical sector remains highly favored by active institutional investors, with only one of the top 10 most active firms having limited exposure. In contrast to previous surges, the digital health sector showed a cooling trend in 2024.

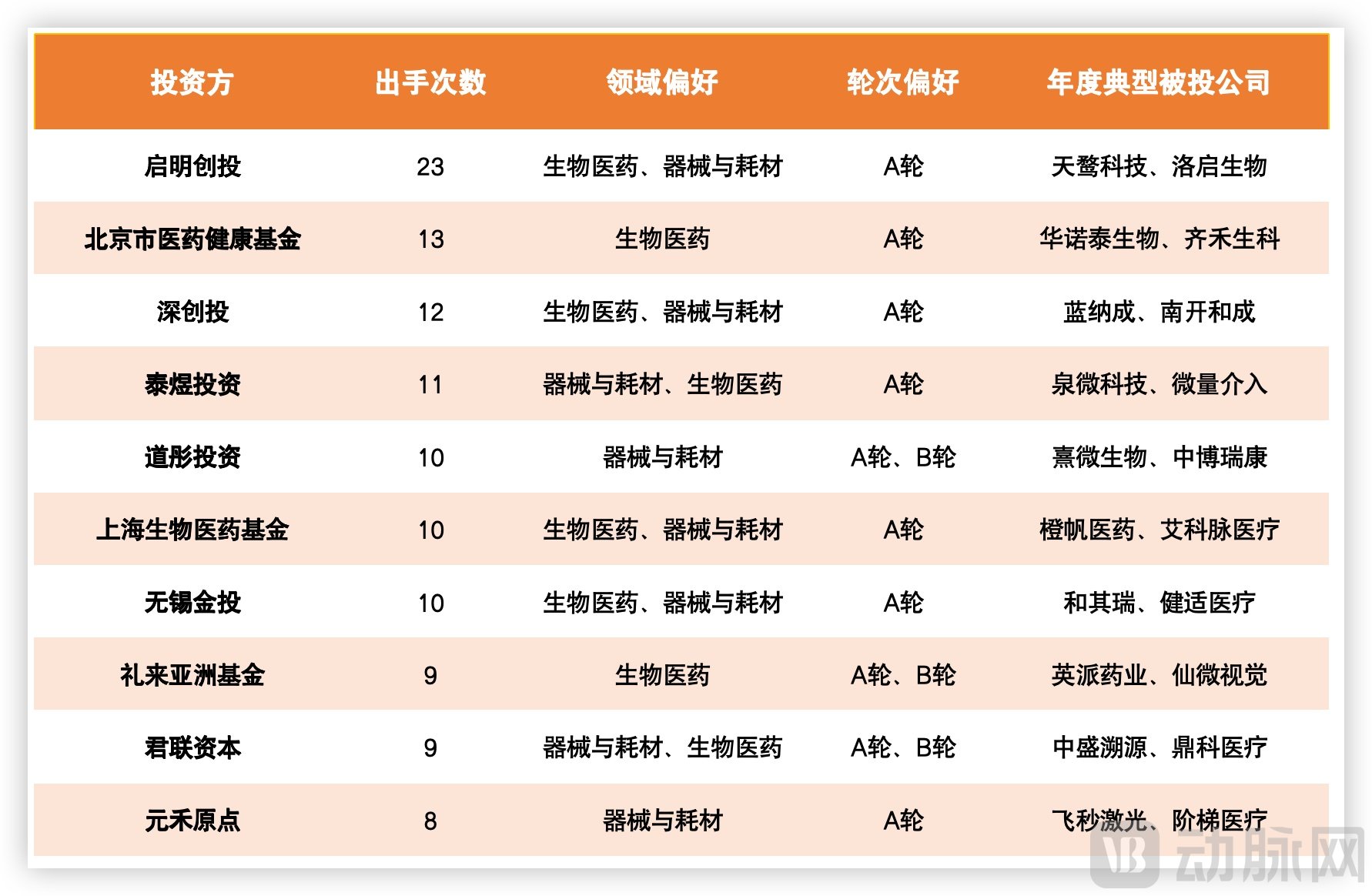

In 2024, leading investment institutions maintained a high level of investment activity. Specifically, Qiming Venture Partners completed 23 investments in the global healthcare market and made additional investments in existing portfolio companies. In contrast, Lilly Asia Ventures and Legend Capital saw their deal counts drop from 20 and 19 in 2023, respectively, to 9 in 2024. Notably, state-owned capital has become a major force in the investment community, with a significant increase in the number of state-owned funds ranking among the top 10.

Top 10 Most Active Investment Institutions in China's Healthcare Industry in 2024, Data Source: VBInsight

Risk-averse strategies have become the core orientation for investment institutions. Diverging from the previous strategy of prioritizing early-stage and small-scale innovative enterprises, mature companies with stable development are more favored by investors in 2024’s capital winter to reduce uncertainty. Compared to the diversified landscape of global healthcare investment deals, domestic investment institutions in China remain focused on the two relatively mature sectors: biopharmaceuticals and medical devices/consumables.

Global Distribution of Hotspots in Healthcare Investment and Financing in 2024

The U.S. remains resilient, while India emerges as a dark horse.

In 2024, the five countries with the highest number of financing deals in the global healthcare sector were the United States, China, the United Kingdom, Switzerland, and Germany, in that order. The United States ranked first with 968 financing deals totaling $39.6 billion. Although the number of deals was slightly lower than in 2023, the total funding amount increased by 13%, indicating a further concentration of capital.

Top Regions for Global Healthcare Primary Market Investment and Financing in 2024 | Data Source: VBInsight

Notably, Germany has surpassed France to break into the global top five. Meanwhile, Switzerland has gradually become the preferred destination for global life sciences R&D and innovation companies to establish their headquarters in recent years, thanks to its globally competitive policy framework, collaborative innovation and translation network, diverse financing channels, and high level of integration with international markets. India now ranks sixth globally, just behind Germany.

In 2024, Jiangsu Province and Shanghai emerged as leaders in China’s healthcare venture capital and private equity sector, completing 164 and 147 financing deals respectively, with total funding amounts reaching $1.375 billion and $1.635 billion. Guangdong Province followed closely behind, with 128 financing deals totaling $1.028 billion. Zhejiang Province and Beijing ranked fourth and fifth, with 112 and 110 financing deals respectively, and cumulative funding amounts of $937 million and $868 million.

Nearly 90% of domestic healthcare financing is concentrated in the aforementioned regions, indicating that medical innovation in China has developed a clustered trend.

During the Spring Festival, VCBeat will release analyses of financing activities and industry status across various healthcare subsectors. Stay tuned.

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please proactively send a message to request it: