Aesthetic Medicine Market Defies Capital Winter: Innovation and Investment Surge in 2024

VCBeat’s recently released “2024 Global Healthcare Investment and Financing Analysis Report” notes that both the total financing amount and the number of financing deals for Chinese healthcare companies declined in 2024 compared to 2023, indicating that the global healthcare sector’s capital winter is entering a more severe phase.

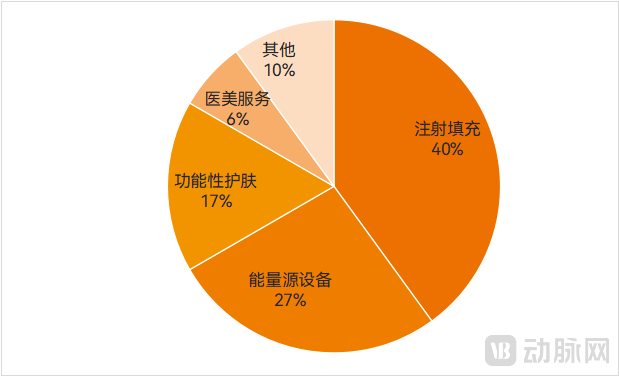

According to data from VBInsight, 2In 2024, there were a total of 30 financing deals in China’s medical aesthetics sector, with the total amount exceeding RMB 1.1 billion. Compared with 2023, investment and financing activity increased rather than decreased. The medical aesthetics industry appears to have remained unaffected by the overall trend in venture capital and private equity.

Specifically, the majority of financing in the medical aesthetics market has gone to upstream companies, with a particular concentration on firms specializing in injectable fillers. Companies focused on energy-based devices have also accounted for a significant proportion of investment and financing activities.

Distribution of Financing and Investment Events in the Medical Aesthetics Sector in 2024, Data Source: VBInsight

The aforementioned report also summarizes the year’s key investment and financing buzzwords, including artificial intelligence, Internet Plus, CGT, and synthetic biology. These terms either encapsulate independent emerging subsectors or describe emerging technologies that intersect with various fields; among the latter, synthetic biology has brought significant disruptive potential to multiple subsectors. In 2024, the medical aesthetics sector saw active investment and financing, with synthetic biology serving as a key enabling technology.

In recent years, injectable fillers have become one of the fastest-growing segments in the medical aesthetics market. End products such as Ellansé, Sculptra, and collagen injections have gained significant popularity, while materials like polycaprolactone (PCL), poly-L-lactic acid (PLLA), and recombinant collagen have rapidly emerged.

More natural and aesthetic injection outcomes, enhanced safety, prolonged duration of effect, greater differentiation in meeting the needs of specific injection sites and individual patients, improved injection comfort, more convenient administration, and lower raw material costs have always been the goals pursued by injectable filler products.Currently, existing products on the market each have their own strengths and weaknesses across these dimensions. Consequently, the industry’s pursuit of superior materials and products has remained unabated, with stakeholders striving to secure greater advantages in these areas.

Since 2024, companies involved in materials such as recombinant collagen, hydroxyapatite, silk fibroin, extracellular matrix (ECM), and polydeoxyribonucleotide (PDRN) have attracted significant capital interest.

2024 Investment and Financing Trends in the Medical Aesthetics Injection and Filler Sector, Data Source: VBInsight

Recombinant collagen was undoubtedly the hottest investment sector in injectable fillers in 2024.

Collagen is classified into dozens of types, such as Type I, Type II, and Type III, based on structure and function, providing structural support to tissues and organs in various parts of the human body. Based on technical principles and structural characteristics, recombinant collagen is categorized into three major classes: recombinant human collagen, recombinant humanized collagen, and recombinant collagen-like proteins. In terms of dosage forms, recombinant collagen can be formulated into solutions, lyophilized powders, gels, sponges, fibers, and more. This diversity at the product level creates vast market opportunities for recombinant collagen.

In 2024, companies such as Junhemeng, Xiangya Bio, Meiliu Bio, and Meishangjie successively secured substantial financing, while Trautec Medical, a developer of recombinant collagen raw materials, was listed on the NEEQ.

Among these companies, Junhemeng and Trautec Medical have overcome technical challenges, achieving significant progress in the research, development, and mass production of recombinant human collagen. After securing a new round of financing, Xiangya Bio will accelerate in-depth R&D and industrialization of its “Huashu” series of recombinant collagen products. Meiliu Bio’s first-generation recombinant humanized collagen offers substantial cost-reduction advantages and has already achieved mass-production capability. Meishangjie combines recombinant collagen with recombinant fibronectin in a microencapsulated format to preserve the biological activity of the collagen.

As a novel material in medical aesthetics, hydroxyapatite has previously been widely used in dentistry, orthopedics, and other fields. Due to its ability to participate in metabolic processes, promote the repair of defective tissues, and exhibit excellent biocompatibility and biodegradability,Since 2024, hydroxyapatite has emerged as a popular material for injectable fillers in medical aesthetics, with Puju Biotechnology, Lingtong New Materials, and Moyang Biotechnology successively securing financing.

Currently, Puju Bio has deployed facial filler products containing hydroxyapatite, while Lingtong New Materials focuses primarily on the R&D of hydroxyapatite microspheres. In 2024, “Youfulan,” a calcium phosphate microsphere-based facial filler under Moyang Bio, made significant progress by obtaining COFEPRIS certification in Mexico for the highest-risk class of medical devices, and is poised to secure China’s first Class III medical device registration certificate for this material.

The proliferation of injectable fillers also includes the emergence of silk fibroin, extracellular matrix (ECM), polydeoxyribonucleotide (PDRN), and others.

In August 2024, Fuxiang Aesthetics, a company primarily focused on the research and development of silk fibroin, completed its Series A financing. In September, Fuxiang Aesthetics entered into a cooperation agreement with GCS, a South Korean medical aesthetics enterprise, for silk fibroin-based aesthetic products. This marked the first license-out of an original Chinese medical aesthetics product to a developed overseas country. The two parties will also jointly develop next-generation silk fibroin-based dermal fillers and skin booster series.

Historically, extracellular matrix (ECM) has been utilized in scenarios such as burn wound repair and patch applications, and its use has now extended into the field of medical aesthetics. Shengzhirun has overcome technical challenges in preparing decellularized matrices from various complex tissue sources and launched a Class III injectable decellularized extracellular matrix (dECM) product, which has completed clinical validation at the Plastic Surgery Hospital of the Chinese Academy of Medical Sciences. In 2024, Shengzhirun completed its Pre-A financing round.

“Salmon Needle” is an emerging product in the medical aesthetics market, with PDRN as its core ingredient. Currently, PDRN-based products have been approved in Italy and South Korea. In China, Jiangsu Wuzhong entered into a partnership with Lilai Technology in 2024, securing exclusive rights to Lilai’s injectable composite solution of sodium hyaluronate and polydeoxyribonucleotide (PDRN). This product is poised to become one of the first Class III medical devices containing PDRN to be marketed in China.

Meanwhile, Ruijiming Biotech, which focuses on the research and development of PDRN raw materials, has completed its Series A financing. The company has successfully developed a synthetic PDRN raw material and achieved successful pilot-scale production.

Many new materials have extensive application scenarios, not only in consumer healthcare but also across various disease areas in serious medical care.From a technical perspective, synthetic biology has played a pivotal role in the innovative iteration of injectable dermal fillers for medical aesthetics, and even functional skincare materials. Many companies, including Xiangya Biology, Junhemeng, Meishangjie, Ruijiming Biology, and Meiliu Biology, have adopted synthetic biology as their foundational technology to help overcome challenges in raw material mass production, efficacy and safety stability, and cost control.

The market for energy-based medical aesthetic devices is experiencing sustained growth. Currently, in addition to dermatology departments in general hospitals and specialized dermatology hospitals, some maternal and child health hospitals and primary healthcare institutions are also investing in the development of photoelectric medical aesthetic projects. Coupled with the rapid emergence of small, boutique physician-founded clinics, this has driven increased demand for equipment procurement. Meanwhile, as regulatory oversight tightens, the market share of non-compliant products is being squeezed, creating room for compliant products to expand.

However, the market for energy-based medical aesthetic devices has long been dominated by imported products, especially high-end equipment, with imported brands having established significant influence among medical aesthetic institutions and consumers.In recent years, a cohort of innovative enterprises in China has grown rapidly, leading to shifts in the market landscape. In 2024, bolstered by capital investment, the localization of energy-based medical devices accelerated.

Investment and Financing in the Energy-Based Device Sector of the Medical Aesthetics Industry in 2024, Data Source: VBInsight

As a typical representative of domestic energy-based medical device manufacturers, Weimai Medical secured four rounds of financing in 2024, with investors including Xiamen Hengxing Group, CDH Baifu, Lizhong Investment, Botanee Group, Chuchang Fund under Jointown Pharmaceutical Group, and Bangqin Capital.

In terms of products, in November 2024, Weimai Medical’s YOUMAGIC high-energy monopolar radiofrequency skin treatment device received Class III medical device approval for the reduction of mild to moderate facial wrinkles. The product is also referred to within the industry as the “domestic Thermage.”

For a long time, Thermage has been the star product among global aesthetic energy-based devices, and after entering China, it became the undisputed gold standard for anti-aging treatments in this field. In recent years, the domestically produced “Ultrasound Cannon” has emerged and can, to some extent, compete with Thermage; however,Constrained by the approved indications in its medical device registration, “Ultrasound Cannon” faced compliance challenges in 2024, which hindered its development progress. Now, with strong support from investors, a compliant “domestic version of Thermage” has been launched. Can it compete on equal footing with imported Thermage? This remains to be seen.

Furthermore, Baifu Laser secured two rounds of financing in 2024. The funds were primarily allocated to the research, development, and regulatory submission of new products; expansion into overseas markets and brand building; initial establishment of domestic distribution channels; as well as capacity expansion and product iteration. It is reported that Baifu Laser currently offers more than 10 core products, which have been exported to over 70 countries and regions. In 2024, Baifu Laser’s intense pulsed light (IPL) therapeutic devices successively obtained medical device certifications from the National Medical Products Administration (NMPA) and the U.S. Food and Drug Administration (FDA).

In fact,2024 was also a year of abundant product launches for various domestically produced energy-based devices.

In addition to intense pulsed light (IPL) therapy devices, which have seen intensive approvals as Class II medical devices, picosecond laser equipment developed by companies such as Fumilei, Ande Optoelectronics, Vishee Medical, Peninsula Medical, and Meidunyi has obtained Class III medical device certification. This marks a significant breakthrough for another category of high-end domestically produced medical aesthetic devices.

In the realm of consumer products, the National Medical Products Administration (NMPA) previously introduced new regulations that classify home-use radiofrequency (RF) beauty devices as Class III medical devices. The implementation of these regulations was originally scheduled for April 2024; however, taking into account factors such as the realities of product development and the need for orderly industry growth, the effective date was ultimately postponed to April 2026. This extension provided ample time for existing products to be registered under the new rules or for companies to adjust their product lines. Nevertheless, some companies moved ahead in 2024: Zongjiang Technology, Yushi Technology, and Shiguang Technology secured the first batch of four Class III medical device certificates for their home-use RF skin treatment devices.

As a large number of products continue to enter the market, the next critical task for domestically produced energy-based medical devices will be to accumulate application case studies, build product reputation, and establish brand image.

A review of investors in the medical aesthetics sector in 2024 shows that industry players such as Botanee, Bloomage Biotech, Mylike Medical, and So-Young have all participated in medical aesthetics investments. As key participants in the medical aesthetics industry chain, these major companies, together with professional investment institutions, are jointly driving industry development and promoting industrial consolidation.

For a long time, insufficient standardization has been a major pain point in the medical aesthetics industry. In recent years, with strengthened regulatory oversight and enhanced industry self-discipline, market compliance has improved. However, issues such as off-label use persist; some products or ingredients are put into clinical application merely after gaining recognition from certain clinicians or being mentioned in expert consensus statements. Taking calcium hydroxylapatite as an example, although no Class III medical device certification for injection and filling has been approved in China to date, products with calcium hydroxylapatite as the primary ingredient have already entered medical aesthetic institutions for injectable use.

In 2025, the investment momentum in the medical aesthetics sector is expected to continue.In January 2025 alone, Huaban Biology, whose core product is agarose-based fillers, completed its first round of financing; Suzhou Meichuang, which focuses on the research and development of expanded polytetrafluoroethylene (ePTFE), closed its Series A+ round; and Onico Medical, a developer of novel energy-source technologies, secured angel funding.

With the support of professional institutions and industrial capital, the research, development, and regulatory submission of innovative medical aesthetics products have received more abundant financial backing, enabling more comprehensive verification of their safety and efficacy. As the number of subsequently approved products increases, the market space for non-compliant products will be squeezed, further advancing the standardization of the industry.