Surgical Robotics Endures Its Toughest Year Amid Capital and Commercial Headwinds

Surgical Robots Have Just Emerged from Their Toughest Year.

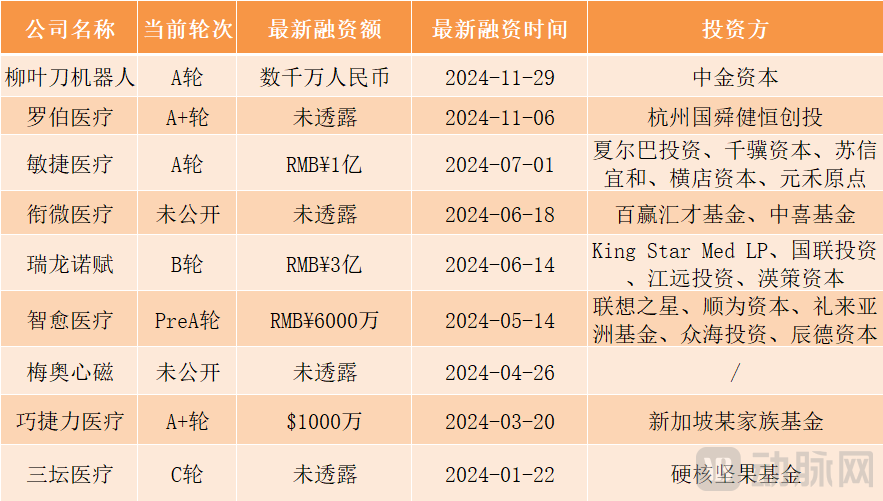

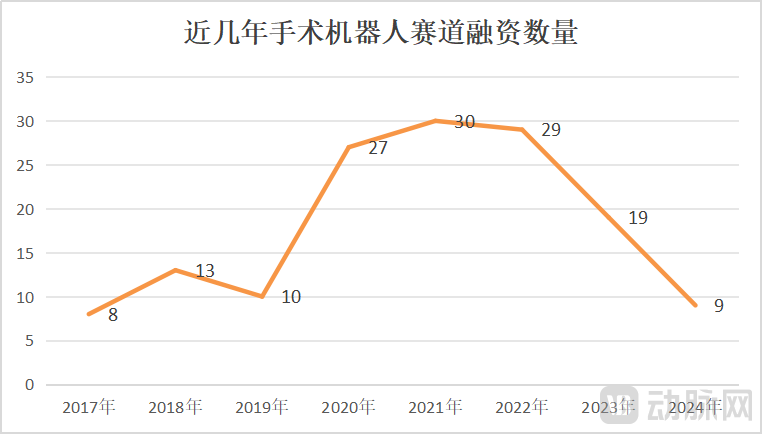

In the capital market, according to the “2024 Global Healthcare Investment and Financing Analysis Report” released by VCBeat, China’s surgical robotics industry completed only nine financing deals in 2024.

Just two or three years ago, surgical robots were a hot favorite in the capital market. For instance, China’s surgical robot industry completed 27 financing rounds in 2020, 30 in 2021, and 29 in 2022. In contrast to the fervor of previous years, surgical robot entrepreneurs found it significantly harder to secure funding in 2024, as the sector suffered a major setback in the capital market.

Despite not being favored by the capital market, the aforementioned surgical robotics companies successfully completed their financing rounds, underscoring their substantial value. According to analysis,In 2024, investment institutions prioritized certainty in their deals, and the surgical robotics sector was no exception.。

A review of these surgical robotics companies that have completed financing rounds reveals that they have all reached specific milestones: Lancet Robot has secured overseas orders for more than 20 units; RaynoBot has completed multi-center, multi-specialty human clinical trials; RoboMD’s gastrointestinal endoscopic surgical robot is nearing regulatory approval; Agile Medical’s laparoscopic surgical robot has completed all surgical procedures required for its urology registration clinical trial; and Zhiyu Medical’s independently developed waterjet surgical robot has entered registration clinical trials.

Emerging fields with less competition are also a key focus for investment firms. Examples include Xianwei Medical’s deployment of super-microsurgical robots and Qiaojieli Medical’s innovative fully flexible dual-arm endoscopic surgical robots.

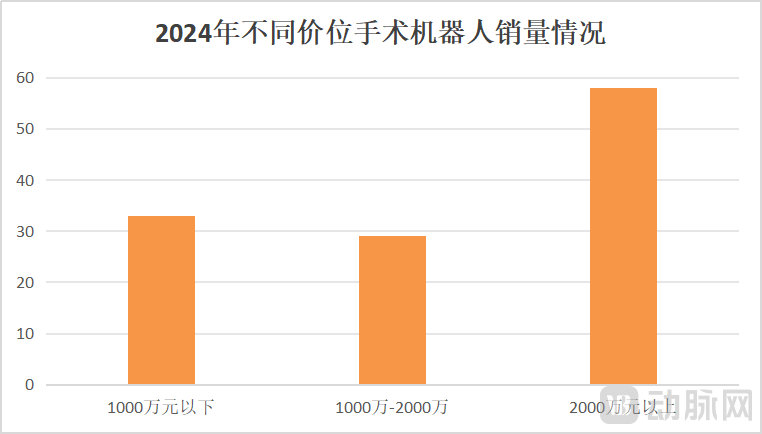

Beyond the capital markets, surgical robots have also encountered headwinds in commercialization. According to public bidding data, over 300 new surgical robot units were installed in China in 2024. Although the number of new installations continued to grow, the procurement market did not see a corresponding significant increase, largely due to a decline in average product prices.

Broadly speaking, in 2024, sales volume increased for lower-priced surgical robots (priced below RMB 5 million), such as neurosurgical and dental surgical robots, while the growth rate slowed for higher-priced products, including laparoscopic and orthopedic surgical robots. As a result, the domestic procurement market for surgical robots did not experience a significant increase despite the rise in overall sales volume.

2024 may have been the most challenging year for domestically produced surgical robots, which faced significant hurdles in capital markets and commercialization. How are Chinese surgical robot companies responding to these challenges? How will the market landscape for surgical robots evolve in 2025?

After a full year of market competition in 2024, surgical robotics companies have gradually come to realize that engaging in aggressive price wars may not be the way forward for the industry.

In 2024, the number of newly installed da Vinci surgical robots, with an average price exceeding RMB 20 million, reached 58 units in China, maintaining its position as the top seller in the domestic laparoscopic surgical robot market. Meanwhile, Chinese-made surgical robots with an average price below RMB 10 million recorded a combined sales volume of 33 units, while those priced at approximately RMB 15 million achieved sales of around 29 units.

This indicates that domestic hospitals in China are less price-sensitive toward surgical robots than previously assumed. Low-priced products do not necessarily achieve high sales volumes, nor do high-priced ones inevitably suffer from low sales. Hospitals place greater emphasis on the performance and quality of surgical robotic systems.

The orthopedic surgical robot market also validates this viewpoint. For instance, Tianzhihang’s orthopedic surgical robots are priced 19% higher than the overall market average, yet they still capture a 50% market share.

Therefore, price wars are not the way forward for the industry; technological competition, innovation-driven rivalry, and differentiation strategies are likely to regain prominence.

Based on research and an analysis of bidding data, medical institutions place greater emphasis on product specifications and performance when procuring surgical robots. For instance, when Taizhou Enze Medical Center procured orthopedic surgical robots, it required that the same equipment system be compatible with total hip arthroplasty, total knee arthroplasty, and unicompartmental knee arthroplasty. As only Stryker’s products met these requirements, the center was able to extend procurement invitations exclusively to Stryker.

For another example, when Ningbo No. 2 Hospital procured an orthopedic surgical navigation and positioning system, four suppliers participated in the bidding. Ultimately, Tuodao Medical, whose bid was the second-lowest in price, successfully won the contract. The bids of the other two suppliers were RMB 4.47 million and RMB 1.95 million lower than that of Tuodao Medical, respectively, but neither was selected.

This is because the products of other suppliers were significantly inferior to those of Tuodao Medical in the commercial and technical evaluation. The commercial and technical evaluation typically involves clinical experts scoring each product based on its functional parameters.

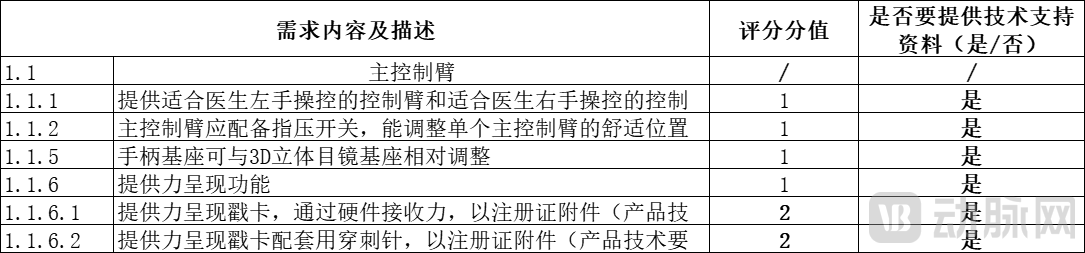

In the field of surgical robotics, evaluation dimensions include: core functions, key technical specifications, master control arms, stereoscopic monitors, control panels, foot pedals, robotic arms, control interfaces, imaging platforms, endoscopes, accompanying services, and after-sales services. The figure below illustrates the requirements and scoring criteria for the master control arm component during the procurement of surgical robots by a medical institution.

(Requirements for the Master Control Arm Component When an Institution Procures Surgical Robots)

Overall, price wars are not the way forward for the surgical robotics industry. Healthcare institutions continue to prioritize surgical robotic systems that offer rich functionality, broad applicability, high cost-effectiveness, and strong innovation.

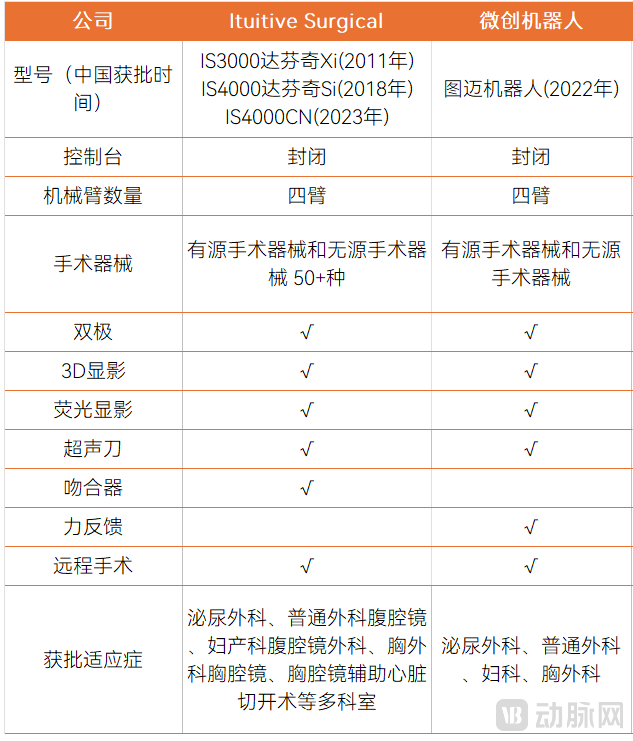

Notably, “domestic production and localization” are no longer exclusive advantages of Chinese surgical robot manufacturers. The da Vinci Surgical System has also become a domestically produced product, with research and development, manufacturing, and training bases established in Shanghai.

In June 2023, the domestically produced version of the da Vinci Surgical System received regulatory approval for market launch in China. In June 2024, Intuitive Fosun announced the inauguration of its headquarters and industrial base in Zhangjiang, Shanghai. This facility is Intuitive Surgical’s largest integrated research, development, manufacturing, and training hub in the Asia-Pacific region.

With the localization of the da Vinci system, industry insiders have estimated, based on bidding and tendering data, that “the market share of the da Vinci surgical robot has increased from 40% in the first half of 2024 to 50% in the second half of 2024.”

In this context, domestic surgical robot companies need to gain a competitive edge through technology, innovation, and differentiation to penetrate the market.

Despite numerous challenges, some domestic brands have achieved growth against the trend.

In 2024, MicroPort MedBot’s Toumai laparoscopic surgical robot secured 39 orders, with commercial installations exceeding 30 units. Domestically, the proportion of Toumai robots installed in leading provincial Grade IIIA hospitals and among China’s top 100 hospitals rose to over 60%, reflecting a steady increase in market share. In overseas markets, Toumai achieved more than 20 commercial orders within just one year.

In addition, the number of clinical surgeries performed using the Toumai surgical robot is growing rapidly. Currently, more than 10 hospitals have each completed over 100 procedures with the Toumai system at single centers, and a few hospitals have even performed nearly 500 commercial clinical surgeries. By comparison, the da Vinci surgical robot, which has been on the market for 20 years, averages over 1,000 procedures per device. (The Toumai surgical robot has been on the market for less than three years.)

In addition to laparoscopic surgical robots, other niche segments of the surgical robot market have also been conquered by domestic companies.

For example, companies such as Yake Smart and Jianjia have made breakthroughs in the oral surgery robot market, with year-on-year sales growth; Baihui Weikang and Huake Jingzhun collectively hold over 80% of the market share in neurosurgical robots; MicroPort Robot’s R-ONE vascular intervention robot has sold eight units; and Aibo Hechuang’s independently developed PANVIS-A cerebrovascular intervention surgical assistance system was approved for market launch in August 2024...

Regarding their remarkable growth against the market trend, companies attribute this success primarily to strong innovation capabilities and superior product performance. For instance, the Toumai surgical robot incorporates force feedback technology—a feature not present in the da Vinci Surgical System—helping surgeons better familiarize themselves with tactile sensations and thereby improving surgical efficiency.

For another example, Yake Wisdom has launched the world’s first autonomous robotic system for dental implant surgery. Its software suite offers comprehensive functionalities, including image visualization, implant planning, surgical guide fabrication, procedural design, robotic motion control, and postoperative assessment. The system features precise robotic arm control, achieving an implant placement accuracy of 0.2–0.3 millimeters, and is capable of operating in confined spaces.

Beyond these commercially available surgical robots, other companies that have not yet reached the commercialization stage are accelerating innovation to enhance their competitiveness. For example, Angtai Weijing has developed and launched the world’s smallest microsurgical robot. Equipped with 7-degree-of-freedom wristed instruments, this robot enables surgeons to perform procedures with greater flexibility, achieving more precise and stable fine manipulation in confined spaces, including suturing. Currently, the robot has entered the animal testing phase.

For example, Fuyi Medical has launched a dual-arm microsurgical teleoperation robotic system capable of performing delicate procedures such as 0.5 mm microvascular anastomosis. The system adopts a dual-arm macro-micro architecture, in which a 7-degree-of-freedom (DOF) serial collaborative arm provides submillimeter precision, while a 6-DOF micromanipulation platform enables micron-level operational accuracy. By integrating these components, the surgical robotic system achieves a multi-DOF design and facilitates the implementation of a remote center of motion module.

Ruolong Nuofu has launched China’s first modular surgical robot. Compared with integrated surgical robots represented by the da Vinci system, this robot offers greater flexibility and degrees of freedom, enabling it to better accommodate diverse surgical requirements. Currently, Ruolong Nuofu’s “Shanhai-1” modular surgical robot has completed patient enrollment in multi-specialty clinical trials.

In fact, in addition to innovation, domestic surgical robot companies have also embarked on the path of global expansion. For instance, in 2024, Edge Medical secured five overseas orders for its laparoscopic surgical robots, MicroPort Robot sold 21 Toumai robotic systems abroad, and Sizhe Rui achieved 11 overseas orders.

As domestic competition intensifies, an increasing number of surgical robotics companies are expected to expand into the global market.

In 2024, the domestic medical device market experienced phased performance pressure due to multiple factors, including a slowdown in tendering and bidding processes and volume-based centralized procurement.

Nevertheless, the industry remains optimistic about a market recovery in 2025.

First, policy support has been further strengthened to promote equipment upgrades. On January 8, 2025, the National Development and Reform Commission and the Ministry of Finance jointly issued the “Notice on Intensifying and Expanding the Implementation of Large-Scale Equipment Upgrades and Consumer Goods Trade-In Programs in 2025,” which proposes increasing the funding scale supported by ultra-long-term special treasury bonds for equipment upgrades in key sectors, intensifying interest subsidies for equipment upgrade loans, accelerating the assessment and diagnosis of existing equipment as well as project reserves, and strengthening financial support.

Previously, in July 2024, the National Development and Reform Commission (NDRC) and the Ministry of Finance issued the “Several Measures on Intensifying Support for Large-Scale Equipment Renewal and Trade-In of Consumer Goods,” arranging approximately RMB 300 billion in ultra-long-term special treasury bond funds to promote large-scale equipment renewal and the trade-in of consumer goods.

As funds related to the medical equipment renewal policy are disbursed and projects in certain regions begin implementation, the medical equipment market is expected to see an overall recovery.

Secondly, the suppressed demand resulting from the slowdown in tendering and bidding activities has been released, and hospital procurement has returned to normal. Previously, the outbreak of the anti-corruption campaign in the healthcare sector led to the suspension or postponement of many tendering and bidding projects. As the market stabilizes, tendering and bidding activities by medical institutions across various regions are gradually resuming. With the release of pent-up demand, the medical equipment market is poised for explosive growth.

Tendering and bidding data indicate that in the first half of 2024, the surgical robot procurement market declined significantly due to multiple factors. However, in the second half of the year, as tendering and bidding activities returned to normal, the number of newly installed surgical robots in China increased by 46.34% year-on-year in the third quarter of 2024. Demand is expected to further expand in 2025.

Third, the liberalization of configuration permits has expanded the surgical robot market. In June 2023, the National Health Commission released the "14th Five-Year Plan for the Configuration of Large Medical Equipment," which plans to configure 3,645 units of large medical equipment nationwide, including 117 Class A devices and 3,528 Class B devices. Since laparoscopic surgical robots were reclassified from Class A to Class B devices in 2018, the planned number of configuration permits has increased significantly, with an additional 225 units added during the 2018–2020 period and 559 units added under the 14th Five-Year Plan.

As the management of configuration certificates is gradually relaxed, the installed base of surgical robots is expected to continue growing.

Finally, the approval of more innovative surgical robots has boosted market activity. As a new wave of surgical robot products gains regulatory approval, relevant companies will intensify their academic and brand promotion efforts, heightening competition and further invigorating the market.