Gene and Cell Therapy: The Most Capital-Intensive Biopharma Arena Descends Into Fierce Commercial Competition

In the just-concluded2024In [Year], gene and cell therapy remained the hottest investment track in the primary market.

Over $5 billion poured in

In the still relatively quiet2024In the primary healthcare market this year, the gene and cell therapy sector has been particularly striking due to its high level of activity.

According to the VCBeat database,2024year, globally157Gene and Cell Therapy Companies Completed171latest financing round, with cumulative funds raised exceeding51.9$100 million.According to the previously released “2024Annual Report on Global Healthcare Investment and Financing Analysis, in2024In that year, the gene and cell therapy sector was the subsector with the largest total financing amount and the highest transaction activity within the entire healthcare industry.

However, a closer examination reveals that by the time2024In recent years, a significant divergence has emerged in gene and cell therapy financing both domestically and internationally. Judging from the final financing data, primary market investments in gene and cell therapy overseas have been the key driver behind the widening growth gap in this niche sector.

First, in terms of financing pace, primary market transactions for gene and cell therapies overseas have been more active.In China,2024year, with a total of70gene and cell therapy companies have completed75a round of financing transaction, involving an amount exceeding8.1hundred million U.S. dollars. Among them, Leman Bio conducted public financing throughout the year3round, with cumulative fundraising exceeding2000USD 10,000; Yuesai Biotech, Yinzheng Gene, Xinji Pharmaceutical, and Rongze Group have all completed2round of financing.

Relatively speaking,2024In contrast, the overseas fundraising landscape for gene and cell therapy companies was even more robust, with a total of88Home Enterprises Completed96round of financing transaction. Among them,HEPHAISTOS-PharmaFull-Year Public Financing3round, with cumulative fundraising exceeding1200ten thousand U.S. dollars;Vico Therapeutics、Santa Ana Bio、Neurona Therapeutics、Neurenati Therapeutics、Indapta Therapeutics、Brenus PharmaWait6all enterprises have completed2round of financing.

Next is the amount of financing, due to2024Overseas gene and cell therapy companies that secured financing in [year] were mostly mature projects in the mid-to-late stages of their startup lifecycle, corresponding to higher financing amounts.2024Year9Month, a cell therapy company headquartered in California, USAArsenal BioAnnouncement of Completion3.25$100 millionCround of financing was the largest single funding transaction for a gene and cell therapy company in the year, and the only one in this sector to rank among the top annual healthcare financing deals.TOP 10Transactions. In China,2024Year4In May, Shanghai-based cell therapy developer Xinji Pharma announced the completion of its3500USD million, marking the largest financing round in China’s gene and cell therapy sector for the year. Still in itsPre-AXinji Pharmaceutical secured the highest annual funding amount in its financing round, but was pushed out of the global rankings.10...and beyond.

Furthermore, it is worth noting that by2024In recent years, compared with startups relying purely on strong biotechnological capabilities, domestic and international investors have shown a stronger preference for gene and cell therapy companies with distinct clinical or technical attributes.

For example, securing the highest annual financing in the sectorArsenal Bio, is a solid tumorCAR-TA star enterprise in the field. The company’s two co-founders bring robust clinical and medical resources: one is a former liver transplant surgeon who later moved into venture capital, while the other previously served as Vice President of Discovery Oncology and Immunology at Merck Research Laboratories. As for Xinji Pharmaceutical mentioned earlier,2023Founded in 2015, Shanghai Baoshan District Xinji Pharmaceutical, as a directly affiliated institution of the Shanghai Institute of Biological Research, Xinji PharmaceuticalRelying on the Shanghai Institute of Biological Sciences and regions including Zhejiang, Jiangsu, and Shanghai110Collaborations Established with Multiple Grade A Tertiary Hospitals to Open a Green Channel for Clinical Patient Recruitment, with significant advantages in commercial development.

In terms of technical attributes, the aforementioned one secured in the past year3Leman Biotech, which completed its -round financing,AIDistinguished from its peers by its integration with biotechnology. Founded in2021Year Lemang Bio, by the Swiss Federal Institute of Technology in Lausanne (EPFL) Co-founded by Professor Tang Li’s team and XtalPi, focusing on immunometabolic reprogramming (Meta 10)+AIR&D of innovative drugs for tumor immunotherapy in combination.

Of course, even in a year with such fervent financing activity, the funding gap in the gene and cell therapy sector remains significant.2024VCBeat'sCGTPark Walkthrough11the park. During this process, the guests repeatedly mentioned the financing dilemma. One practitioner stated that many opportunities must be pursued proactively and aggressively, as there are few funds available for investment now, yet numerous projects are in need of capital. Another practitioner pointed out that limited resources should be focused on a select pipeline. It is necessary to innovate, but only within limited bounds; differentiation is required, but it must come with certainty. This balance is, in fact, quite challenging.

The Breakout Year of Commercialization

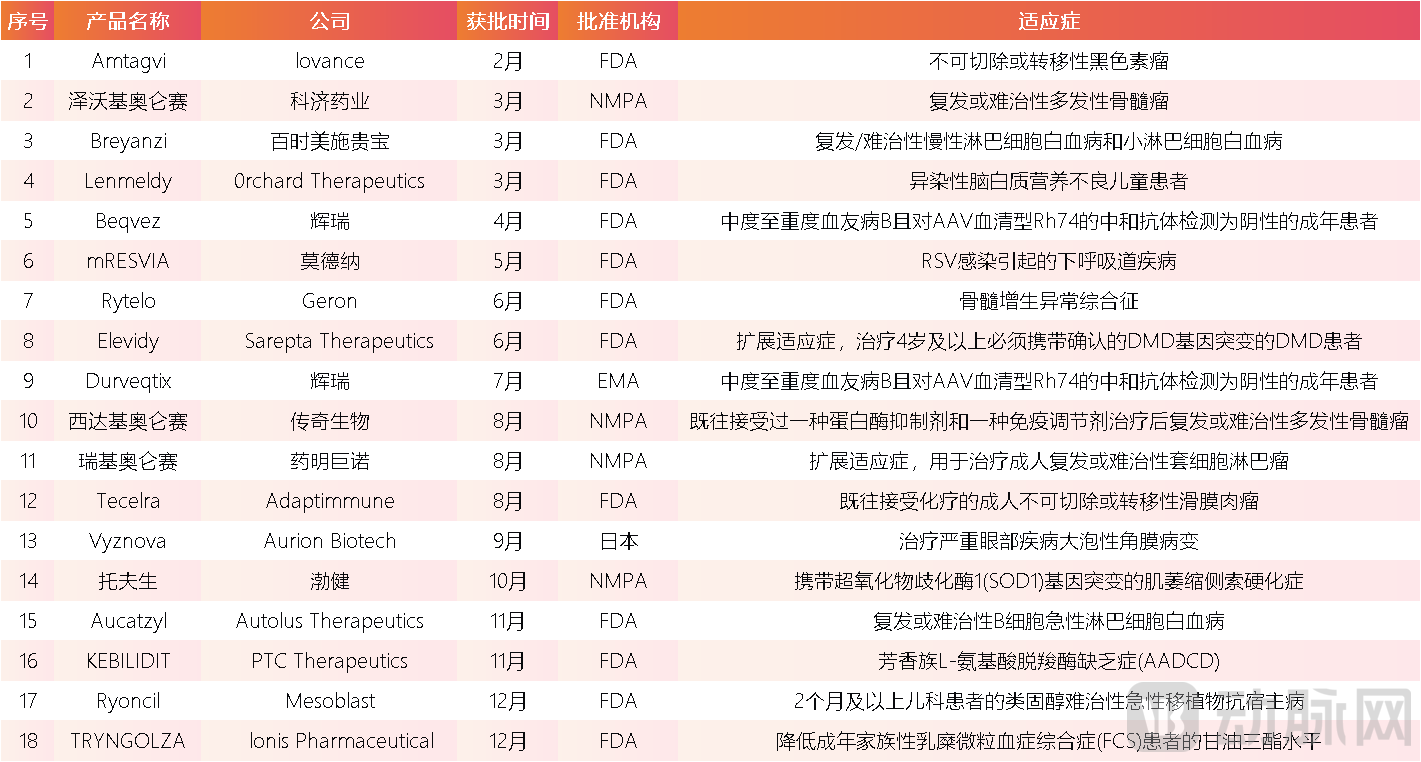

Behind the fervor of primary market financing lies2024In [Year], global gene and cell therapy products achieved significant breakthroughs in rapid succession.This groundbreaking biologic therapy has already provided the only available solutions for many major human diseases. According to incomplete statistics from the Artery Orange database,2024In 20XX, the world's total18gene and cell therapy products approved for market launch, far exceeding2023annual levels. More importantly, it features a number of blockbuster first-in-class new drugs.

2024The first new drug approved for market launch this year is expanding the boundaries of clinical applications for gene and cell therapies into more disease areas.2Month16Day,IovanceThe Company'sAmtagvi(lifileucel) obtained U.S.FDAApproved, it has become the world’s first tumor-infiltrating lymphocyte (TIL) therapy for the treatment of unresectable or metastatic melanoma. Prior to this, patients with unresectable or metastatic melanoma mostly relied on targeted therapy or conventional radiotherapy and chemotherapy to prolong survival. In an international, multicenterII In phase clinical trials,AmtagviMonotherapy for unresectable or metastatic melanoma, with an objective response rate reaching31.4%, which contains8cases of complete remission and40Partial remission in some cases has significantly improved the prognosis for such patients.

3Month14day, Bristol Myers Squibb'sBreyanziAcquiredFDAAccelerated approval for the treatment of relapse/Market Price for Adult Patients with Refractory Chronic Lymphocytic Leukemia or Small Lymphocytic Lymphoma41.03million USD. It is also the first globally approved therapy for the treatment of relapsed or refractory chronic lymphocytic leukemia or small lymphocytic lymphoma.CAR-T Cell Therapy. In Pivotal Multicenter TrialsTranscend CLL004 , the complete remission rate was20%, the overall response rate was45%, among patients who achieved complete response, the median duration of response had not been reached, and the rate of minimal residual disease negativity in the blood was100%, in the bone marrow92.3%。

Furthermore, it is worth mentioning that in2024Year8month, the world's firstTCR-TThe therapy has been approved for market launch. This product, namedTecelraofTCR-TProduct, byAdaptimmuneCompany-developed, byFDAApproved for the treatment of adult patients with unresectable or metastatic synovial sarcoma who have previously received chemotherapy, pricing72.7ten thousand U.S. dollars. All along,TCR-TTherapy is considered to be more thanCAR-TMore advanced cell therapy solutions, but commercialization progress has been very slow.AndTecelra's approval has undoubtedly greatly ignitedTCR-Tenthusiasm for development and investment in the field.

According to statistics from the VCBeat database, as of2024By year-end, the number of gene and cell therapy drugs approved for marketing worldwide had exceeded50...funding. However, judging from post-launch commercial performance, this therapeutic area still has a long way to go before producing a blockbuster drug.

And judging from the already released commercialization data,2024years, except forCilta-cel InjectionIn addition, the sales of most gene and cell therapy blockbuster products remain unsatisfactory. Data shows that,2024Year,Total Sales of Cilta-cel Injection9.63hundred million U.S. dollars, compared to2023Year-over-Year Growth92.7%。andKymriah、Abecmaetc., in2024There was a varying degree of sales shrinkage in the year.

On one hand, a large number of new products are being intensively approved and launched; on the other, their clinical adoption is progressing relatively slowly. A fierce commercial battle in gene and cell therapy seems inevitable. Data show that two domestically produced cell therapy products, relma-cel and zevor-cel, have not delivered breakthrough revenue contributions since their market launch. Data show that,2024In the first half of the year, Relma-cel Injection contributed to revenue8681.510,000 yuan, zevor-cel was soldapproximately60010,000 yuan.

When will the commercialization inflection point occur?

Arrived2025Year,As an increasing number of enterprises and research institutions enter the field, the pipeline of drugs under development and the number of clinical trials continue to grow. The issue of product homogenization is gradually becoming apparent, and the commercialization of gene and cell therapies may descend into a “red ocean” of fierce competition. However, two major bottlenecks that have long constrained these innovative therapies remain unresolved.

On the one hand, gene and cell therapies themselves still carry significant safety risks. This is also a key bottleneck constraining their widespread clinical application.For example, there are risks associated with delivery systems,Commonly Used in Gene Therapy AAV The vector exhibits high affinity for the liver, which may trigger immune system attacks, pose a risk of hepatotoxicity, and lead to chromosomal rearrangements and an increased risk of off-target effects, potentially even causing cancer.For another example, the potential issues arising from editing tools, commonly used in gene and cell therapyCRISPR/Cas9Gene editing tools,The Essence Is ChangeDNASequence, which may generate disordered gene sequences during the body's repair process, carries a high risk of off-target effects and may affect tumor suppressor genes, posing safety concerns.

On the other hand, high costs and expensive pricing limit the patient population that can be covered.Due to the limited technological maturity of gene and cell therapies, the application of such products is restricted to a very narrow scope, and regulatory requirements are exceedingly stringent. Taking gene therapy as an example, viral vector production requires large-scale manufacturing facilities, involves complex production processes, and poses significant challenges in quality control, leading to persistently high costs. Consequently, some gene therapy products are priced exorbitantly due to the high cost of viral vector production. Under current technological conditions, the research and development (R&D) of gene and cell therapies demand substantial investments in capital, talent, and time. The journey from laboratory research to clinical trials and finally to market launch is complex and fraught with risk. Many innovative pharmaceutical companies face financial pressure and the risk of R&D failure, leaving limited room for price reduction from the supply side.

From the payment perspective, such treatments are inconsistent with the coverage positioning of basic medical insurance, making it difficult for them to be included in the National Reimbursement Drug List (NRDL) through standard access channels. Although some commercial health insurance plans and local supplemental insurance schemes (such as “Hui Min Bao”) have covered certain cell and gene therapy products, their scope of coverage, reimbursement levels, and population reach remain limited due to restrictions such as pre-existing condition exclusions and payment caps, failing to adequately meet patient needs.

In a sense, the commercial frenzy surrounding gene and cell therapies may arrive even before the inflection point. However, as the technologies themselves continue to mature and reach a broader patient population, we believe these innovative therapies will become vital clinical treatment tools.