Global Cardiovascular Financing Analysis: Structural Heart Disease Emerges as the Top Investment Magnet

In 2024, among the numerous subsectors of medical devices, the cardiovascular sector attracted the highest number of financing deals.

As the leading cause of death worldwide, cardiovascular disease (CVD) is expected to impose an increasingly heavy disease burden. According to a study published in the European Journal of Preventive Cardiology, the global burden of CVD will continue to rise from 2025 to 2050, primarily driven by global population aging. In this context, the crude mortality rate for CVD is projected to increase rapidly, with the escalating burden largely attributable to atherosclerotic diseases.

Moreover, the cardiovascular field is a global hotspot for medical device innovation. Currently, the treatment of cardiovascular diseases is evolving toward precision and personalized medicine, with various innovative technologies emerging in rapid succession.

Against this backdrop, VCBeat conducted an in-depth statistical analysis of the distribution of financing in the medical device sector in 2024.

According to VBInsight data, global financing activities in the cardiovascular sector demonstrated robust momentum in 2024, with a total of 61 financing deals recorded. Among these, 35 deals occurred in China, accounting for approximately 57.4%, while 26 deals took place overseas, representing about 42.6%. An in-depth analysis of the data reveals that the higher number of domestic financing events underscores the strong vitality and significant potential of China’s cardiovascular sector at its current stage of development. However, despite the relatively lower number of financing deals abroad, competition in the international cardiovascular landscape remains fierce, with leading technological standards. Overseas markets benefit from profound scientific research accumulation, advanced R&D systems, and mature market operation models, making their innovative capabilities still worthy of close attention.

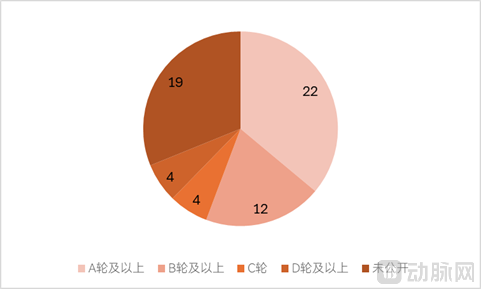

Distribution of Financing Rounds in the Cardiovascular Field in 2024

From the perspective of funding round distribution, early-stage financing dominates.A-round and above financings were the most frequent, totaling 22 instances, followed by B-round and above financings with 12 instances. This indicates that investors prefer to make early-stage investments, particularly at the A- and B-round stages. Late-stage financings were less common, with both C-round and D-round and above financings occurring only 4 times each.

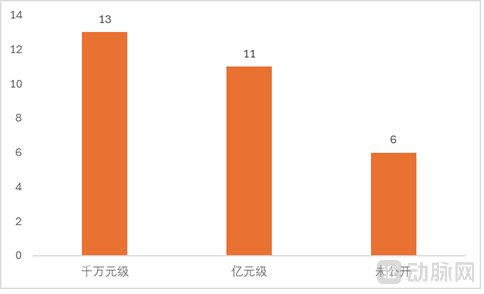

In terms of the distribution of financing amounts, domestic cardiovascular sector financing exhibits a multi-tiered structure. There were 13 financing deals in the tens-of-millions-of-yuan range, 11 in the hundreds-of-millions-of-yuan range, and six with undisclosed amounts. The number of deals in the tens-of-millions-of-yuan range was relatively high, accounting for nearly half of the total. This indicates that a considerable number of startups or early-stage, smaller-scale enterprises in the cardiovascular field are receiving capital injections. These companies may be at a critical stage of technological research and development.

Distribution of Financing Amounts for Cardiovascular Events in China

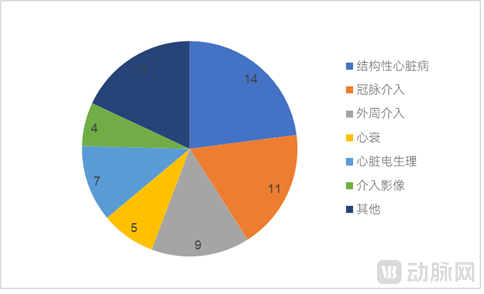

The breakdown of global cardiovascular financing deals in 2024 by subsector shows that structural heart disease led with 14 financing events, followed by coronary intervention and peripheral intervention with 11 and 9 deals, respectively. Cardiac electrophysiology, heart failure, and interventional imaging accounted for 7, 5, and 4 financing events, respectively, while an additional 11 deals fell under other subsectors.

Distribution of Financing Sub-sectors in the Cardiovascular Field

Structural Heart Disease

Structural heart disease attracted the highest number of financing events, indicating strong capital interest in its technological innovation and market potential. The number of financing deals in this field was comparable between China and overseas markets.Abbott’s CEO once stated, “Structural heart is one of the most attractive areas in the medical technology field and a rapidly growing segment within Abbott’s business.”

Financing in the field of structural heart disease is primarily driven by innovative technologies in the mitral and tricuspid valve sectors. The complex anatomical structures of the mitral and tricuspid valves, coupled with diverse interventional treatment strategies, create significant opportunities for product and technological innovation. Companies securing funding have developed products including interventional repair systems for mitral and tricuspid valves, as well as robotic systems for valvular surgery.

Currently, the market for mitral and tricuspid valve interventions is dominated by Abbott and Edwards Lifesciences. Abbott’s MitraClip is used for the treatment of mitral regurgitation, while its TriClip is indicated for tricuspid regurgitation. Edwards Lifesciences markets the PASCAL system for mitral and tricuspid valve repair, as well as the EVOQUE tricuspid valve replacement system. Due to the limited availability of surgical interventions, there is substantial demand for interventional therapies in patients with mitral and tricuspid valve diseases. Both companies have reported rapid growth in their respective product lines. According to reports, Abbott’s structural heart disease business generated $2.25 billion in sales in 2024, representing a year-over-year increase of 15.5%. The majority of this revenue was driven by MitraClip, although Amplatzer Amulet (a left atrial appendage occluder) and TriClip also demonstrated strong growth performance.

Companies in the field of structural heart disease that have secured financing are showcasing several key innovation trends in their products, primarily reflected in reducing procedural complexity, expanding indications, achieving precise positioning, and developing novel valve materials.

Coronary Intervention

In the field of coronary intervention, there is a large patient population, and various innovative technologies for addressing complex diseases have garnered significant attention. For instance, microvascular obstruction (MVO) in acute myocardial infarction affects approximately 50% of patients, a proportion far higher than that of the no-reflow phenomenon. MVO can lead to dysfunction of the heart and other organs. Traditional coronary angiography can only visualize stenosis and occlusion in large vessels, offering limited capability for assessing microvasculature.

CorFlow Therapeutics has developed an intraoperative diagnostic and drug delivery platform for MVO. CorFlow detects MVO using sensor-equipped guidewires and algorithmic systems, and following diagnosis, locally delivers therapeutic agents to the microvascular system.

Intravascular lithotripsy (IVL) has also garnered significant attention in percutaneous coronary intervention. Currently, traditional treatments for calcified vascular lesions have certain limitations. For instance, passive interventional devices such as cutting balloons and scoring balloons are primarily suitable for mild to moderate calcified lesions; they cannot effectively address calcified deposits within the coronary intima and submedial layers, and may cause damage to healthy vessel walls. Although atherectomy is a primary method for treating severe calcified lesions, it mainly improves intimal calcified plaques and is ineffective against deep calcified lesions beneath the intima. Furthermore, it carries a high risk of vascular perforation, target lesion revascularization, and myocardial infarction.

In contrast, IVL has demonstrated favorable efficacy and a higher safety profile in the management of moderate to severely calcified lesions. It is currently the only device capable of effectively treating deep vascular calcification by precisely delivering acoustic pressure waves to the calcified sites, thereby fracturing or loosening intravascular calcified plaques, restoring vascular compliance, maintaining patency, and achieving coronary vessel remodeling.

Johnson & Johnson acquired Shockwave, the world’s first company to provide intravascular lithotripsy (IVL) technology, for as much as $13.1 billion in 2023. This large-scale acquisition fully demonstrates Johnson & Johnson’s strong recognition and confident optimism regarding the future development prospects of IVL technology.

However, current intravascular lithotripsy (IVL) systems still have many areas for improvement in practical applications, which precisely provides valuable development opportunities for other innovative companies. Specifically, existing balloon catheters have significant design flaws; they are often bulky and cumbersome, which to some extent affects their ease of operation and flexibility. Meanwhile, the high cost of using existing products imposes a substantial financial burden on both healthcare institutions and patients.

In light of the aforementioned issues, developing IVL products with improved lesion-targeting deliverability, lower usage costs, and more stable energy output has become a key direction for innovation-driven companies in this field.

Peripheral Intervention

Among the various domains of interventional therapy, pulmonary embolism (PE) in peripheral interventions has garnered significant attention. Pulmonary embolism, particularly acute high-risk PE, is often associated with high mortality rates, underscoring the urgency and challenges inherent in its treatment.

Currently, there are various interventional techniques for the treatment of acute high-risk pulmonary embolism (PE), such as catheter-directed thrombolysis (CDT), mechanical thrombectomy, catheter-based aspiration thrombectomy, and thrombus removal. However, these existing technologies have revealed numerous issues in practical application, primarily centered on high procedural complexity, relatively low therapeutic efficiency, and difficulty in achieving standardized operations. To some extent, this has limited their widespread clinical adoption and efficacy.

In recent years, Inari Medical’s FlowTriever system has garnered significant attention in the field of pulmonary embolism treatment. The FlowTriever system features a unique design concept, utilizing a large-bore structure with self-expanding nitinol discs that mechanically engage thrombi within the pulmonary arteries. During aspiration through the large-bore catheter, the nitinol discs can flexibly retract into the catheter lumen, thereby extracting the captured thrombi out of the body.

Notably, the FlowTriever system is currently the only interventional device specifically designed for the treatment of large-volume thrombi. This innovative mechanical thrombectomy approach offers significant clinical advantages by rapidly recanalizing occluded vessels. Timely restoration of blood circulation effectively improves patient outcomes, significantly shortens hospital stays, and delivers a superior healthcare experience.

Electrophysiology

In the financing landscape of the electrophysiology sector, Pulsed Field Ablation (PFA) technology continues to play a pivotal driving role. Compared with traditional radiofrequency ablation and cryoablation techniques, PFA technology demonstrates superior performance. It not only offers enhanced safety and efficacy but also enables more precise ablation of target myocardial tissue, significantly minimizing damage to surrounding healthy tissue.

As the commercialization of pulsed field ablation (PFA) technology accelerates, the competitive landscape of the electrophysiology industry is undergoing profound reshaping. Boston Scientific has rapidly emerged in the electrophysiology market with its superior PFA products, becoming a focal point of industry attention. The global commercialization of PFA technology is gaining momentum, demonstrating strong growth potential.

In 2024, driven by the innovativeness of pulsed field ablation (PFA) technology and its vast market potential, multiple Chinese companies operating in this sector secured financing by leveraging their technological advantages and market strategies.

Cardiac Interventional Imaging

All financing in the field of cardiac interventional imaging originates from within China, primarily driven by the trend of domestic substitution. As the treatment of cardiac and vascular diseases moves toward greater precision, precise interventional imaging products are being increasingly widely applied in the management of these conditions. Intracardiac echocardiography (ICE) and intravascular ultrasound (IVUS) are two representative technologies. Among these, the ICE sector leads in financing activity.

Currently, intracardiac echocardiography (ICE) in China is primarily applied in the field of electrophysiology, where atrial fibrillation treatment constitutes the dominant application, followed closely by left atrial appendage closure. Compared to the ICE utilization rate of over 90% in electrophysiology procedures in the United States, China’s ICE penetration rate is only one-tenth that of developed countries, fully demonstrating the significant growth potential inherent in the Chinese ICE market.

In the domestic intracardiac echocardiography (ICE) market, foreign brands currently hold a dominant position, while Chinese-made products account for a relatively small market share. However, it is encouraging to note that domestic enterprises have achieved significant breakthroughs in key ICE technologies. For instance, through continuous innovation and optimization in the design and manufacturing of ultrasound probes, Chinese companies have enhanced probe precision and stability. Substantial progress has also been made in optimizing image processing algorithms, greatly improving image clarity and diagnostic accuracy. These breakthroughs in core technologies have significantly boosted the performance and quality of domestically produced ICE devices. For Chinese enterprises, those that master core ICE manufacturing processes and advanced algorithms, as well as those with strong product iteration capabilities enabling rapid adjustments and optimizations in response to market demands and technological advancements, are more likely to gain capital recognition.

Looking ahead, the cardiovascular market boasts broad development prospects and is filled with opportunities. At the technological level, cardiovascular technologies are continuously advancing toward precision and personalization. As domestic attention to cardiovascular diseases continues to increase, the release of medical demand will drive further expansion of the cardiovascular market. Moreover, with innovations in key technologies and improvements in product performance and quality by domestic enterprises, Chinese medical device brands will gradually strengthen their influence and are poised to emerge as significant players in the global cardiovascular market.

Reference Article:

Tian Hongyan | Hotspots and Challenges in the Diagnosis and Treatment of Acute Pulmonary Embolism — Chinese Journal of Vascular Surgery

Abbott expects to launch first PFA device outside of the US this year——medtechdive