Radiology AI: Dawn of a New Era – Prospectus Summary

UNITED IMAGING

Artificial Intelligence Medical Product Developer

DeepWise

Developer of Artificial Intelligence Medical Imaging Diagnosis System

A Seemingly Unremarkable Year, Yet Imaging AI Shines in the Spotlight at Year-End.

In December 2024, United Imaging Intelligence completed a RMB 1 billion financing round, pushing the valuation of its imaging AI business above RMB 10 billion. On the eve of the New Year, DeepWise secured another RMB 500 million in funding, marking another significant step forward for the established AI enterprise.

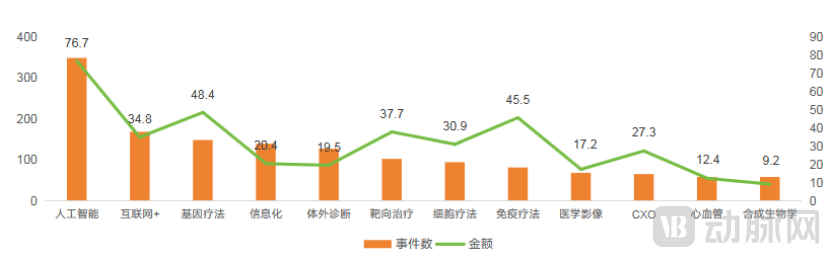

The soaring enthusiasm for financing in the field of medical artificial intelligence has played a significant role in the rise of this niche sector. According to data from the "2024 Global Medical and Health Industry Capital Report," there were over 300 financing deals in medical AI in 2024, with total funding reaching approximately RMB 7.67 billion—far exceeding other sectors—and driving the development of imaging AI.

Meanwhile, the relentless efforts of industry pioneers have also been crucial. After a decade of accumulation, AI in medical imaging has come very close to realizing its original vision.

Hot Keywords for Global Healthcare Industry Investment and Financing in 2024

Deconstructing the New Drivers Behind AI Imaging Financing: Three Key Dimensions

First, in the area of medical insurance. In November 2024, the National Healthcare Security Administration released the “Guidelines for Project Initiation on Pricing Items for Radiological Examination Services (Trial),” which sent shockwaves through the industry.

Policy interpretation articles state that the new project establishment guidelines will uniformly arrange an "AI-assisted diagnosis" extension item under the main category of radiological examinations. Hospitals utilizing artificial intelligence for assisted diagnosis shall apply the same pricing level as the main item, without charging separately in addition to the main item.

In short, the issuance of this project guideline can be regarded as a significant endorsement of the clinical application value of artificial intelligence.

Although direct charging for relevant applications is not currently feasible, once the threshold of being included as an “add-on item” is crossed, imaging AI has the potential to rapidly achieve the “per-case fee” model initially envisioned by companies—provided that comprehensive health economics evidence can be subsequently supplied—thereby generating stable, scalable revenue.

Next is the R&D direction. In the past, independently developing an AI-based medical imaging product required a lengthy cycle. Developers needed to assess hospital requirements, identify disease types with sufficient patient volume that matched their technical capabilities, and then seek collaborations with hospitals to obtain legally compliant data. This data was then cleaned, de-identified, annotated, and categorized to create training datasets, ultimately enabling the development of corresponding models.

Throughout this process, enterprises must devote substantial time and effort to establishing hospital partnerships, cleaning and annotating data, and training and fine-tuning models, which significantly drives up the R&D cost of individual AI solutions.

Now that we have entered the era of large models, new-generation unsupervised learning algorithms can perform delineation and segmentation tasks for various types of imaging data and disease lesions at low cost and high efficiency, significantly reducing the amount of data required for model training.

More importantly, health data, as a new type of asset, officially began trading in public hospitals in 2024.

In mid-October, Shanghai General Hospital secured 18 data product listing certificates in a single application. These include multimodal datasets commonly used in AI-assisted diagnosis, such as pulmonary nodules, diabetic retinopathy, CT-derived fractional flow reserve (CT-FFR), and breast ultrasound, as well as disease-specific datasets covering spermatogenic disorders, acute leukemia gene mutations, and transplantation prognosis.

In November of the same year, Xuanwu Hospital of Capital Medical University completed the asset rights registration and transaction for its carotid artery stenting dataset (comprising 2,550 records at the time of registration) at the Beijing International Big Data Exchange (hereinafter referred to as “Beijing Data Exchange”). According to Xuanwu Hospital, the relevant dataset will be applied to the research and development of domestically produced carotid artery stents, helping healthcare institutions gain a more precise understanding of cerebrovascular diseases in the Chinese population.

For imaging AI, health data trading has brought unprecedented positive impacts.

Under the previous R&D model centered on enterprise-hospital collaborations, medical imaging AI companies needed to frequently communicate with hospital physicians to ensure that cooperation processes were reasonable and compliant. This model not only resulted in relatively low R&D efficiency but also often required sharing intellectual property rights of AI algorithms with hospitals, thereby hindering subsequent commercialization efforts.

Now that health data has been assigned a market price, the relationship between enterprises and hospitals has shifted from partnership to buyer-seller dynamics. Companies can not only accurately estimate the R&D costs of imaging AI and efficiently execute AI training plans, but also effectively price imaging AI developed in collaboration with hospitals. This facilitates the repurchase of AI intellectual property rights by enterprises, thereby mitigating potential risks in subsequent sales processes.

Finally, there is the product form. Following the traditional AI development approach focused on single diseases, imaging AI can gradually cover all medium- and high-volume disease types. However, the spectrum of diseases that humans may suffer from is extremely broad; there are over 200 diseases affecting the lungs alone, and more than 1,000 neurological disorders, far exceeding the combined capabilities of existing AI companies.

In the era of large imaging models, companies no longer need to prioritize throughput or pursue disease-specific breakthroughs in isolation. Empowered by LLMs and advanced algorithms, they can conduct comprehensive cross-modal and cross-anatomical training, achieving true artificial intelligence capable of diagnosing like physicians.

As “data,” the core element of artificial intelligence, becomes a tradable commodity, the biggest obstacle facing the medical AI industry is removed. In this new AI era, we will inevitably see more tech companies entering the healthcare sector, accelerating the transformation toward an era of digital and intelligent medicine.

So, what kind of medical imaging AI companies can stand out in the new AI era?

Before transaction volumes in the health data market reach scale, evaluating imaging AI still requires focusing on their product layout logic and commercial innovation capabilities.

Looking back at 2024, the combined impact of anti-corruption campaigns in the pharmaceutical and healthcare sectors and the increasingly prominent trend of centralized procurement for medical equipment halted the decade-long price surge in medical imaging devices. Although policy catalysts such as the “adjustment to the configuration permit catalog” and “trade-in programs” were introduced, the market’s response lagged, resulting in limited recovery momentum. Consequently, it is unlikely that the sector will recapture its past glory in 2025.

Under these circumstances, the traditional sales models of medical imaging AI companies are no longer sustainable. Consequently, nearly every leading player in the field is seeking its own breakthrough strategy. For instance, ShuZhun Intelligence has heavily invested in the technically challenging and less crowded domain of AI-powered ultrasound, successfully developing AI models for ultrasound imaging of all major human organs. DeepWise has delved into hospital data centers to assist healthcare institutions in assetizing their imaging and textual data. UNITED IMAGING has released foundation models, transforming the R&D paradigm for imaging AI. Infervision has leveraged medical imaging to expand into the surgical domain, shifting from AI-assisted diagnosis to parallel AI-driven diagnosis and treatment. Shukun Technology has targeted device intelligence, achieving deep integration of software and hardware through its self-developed ultrasound solutions.

From a current perspective, each choice corresponds to a visible market. If the quality of products or solutions can be ensured, there is hope to open up considerable new markets. In 2025, they need to take advantage of favorable policies and quickly find effective business models within their own new layouts to survive through the darkness before dawn.

As trading in the health data market becomes the norm, differences among various business models will diminish, and companies will need to establish new core competencies.

At that time, whoever possesses sufficient cash flow, identifies genuine clinical needs with the greatest speed and precision, and rapidly develops effective algorithms will break through the deadlock in this protracted competition and emerge as the undisputed leader.