Global Healthcare M&A Retreats in 2024 Amid Strategic Shifts, But Signs of Recovery Emerge in Early 2025

$86.6 billion vs. $41.8 billion.

This is a comparison of the total value of the top 5 global annual M&A transactions in 2023 and 2024, which also indirectly reflects the state of industry mergers and acquisitions in 2024.

Although global mergers and acquisitions (M&A) in the healthcare sector were frequent in 2024, reaching record highs in certain niche segments, many industry giants sought to drive revenue growth and optimize their therapeutic areas and technology portfolios through strategic M&A, aiming to cope with intensifying market competition and rapid technological iteration. However, a closer examination reveals that major M&A deals, once common, have significantly decreased, suggesting underlying concerns beneath this bustling surface.

In short, buyer companies have begun to flexibly adjust their M&A strategies in response to changing economic conditions, with a greater emphasis on cost control. Against this backdrop, the divestiture and sale of business lines has emerged as a major trend in the healthcare industry in 2024, exemplified by Edwards Lifesciences’ sale of its critical care business to Becton Dickinson (BD). Through this transaction, BD strengthened its product portfolio in smart connected care, while Edwards Lifesciences refocused on its core area of structural heart disease.

Although M&A transactions in 2024 faced numerous challenges, several large-scale deals in early 2025 have brought new hope to the industry.

Compared with 2023, large-scale M&A transactions in the healthcare industry decreased significantly in 2024.

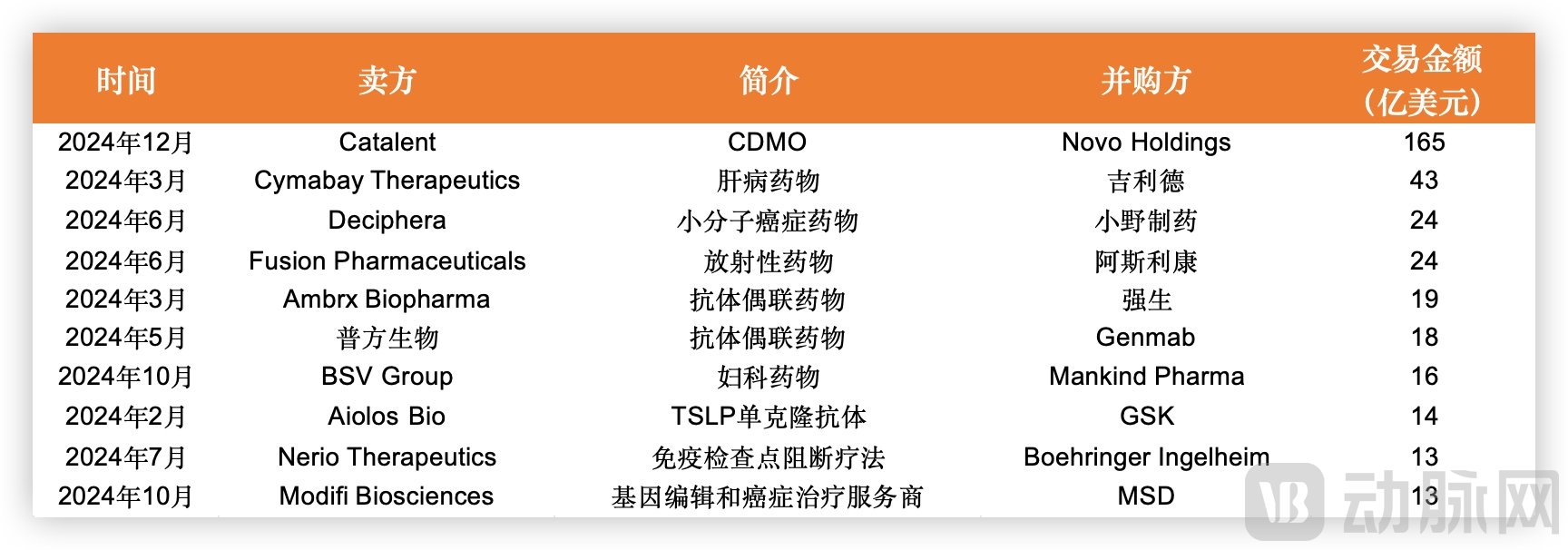

In 2024, although the healthcare industry saw several high-value M&A transactions, the total number of deals declined significantly compared to 2023. Novo Holdings, the majority shareholder of Novo Nordisk, claimed the top spot for deal value in 2024 by acquiring CDMO giant Catalent in an all-cash transaction worth $16.5 billion, followed closely by Johnson & Johnson’s $13.1 billion acquisition of Shockwave Medical.

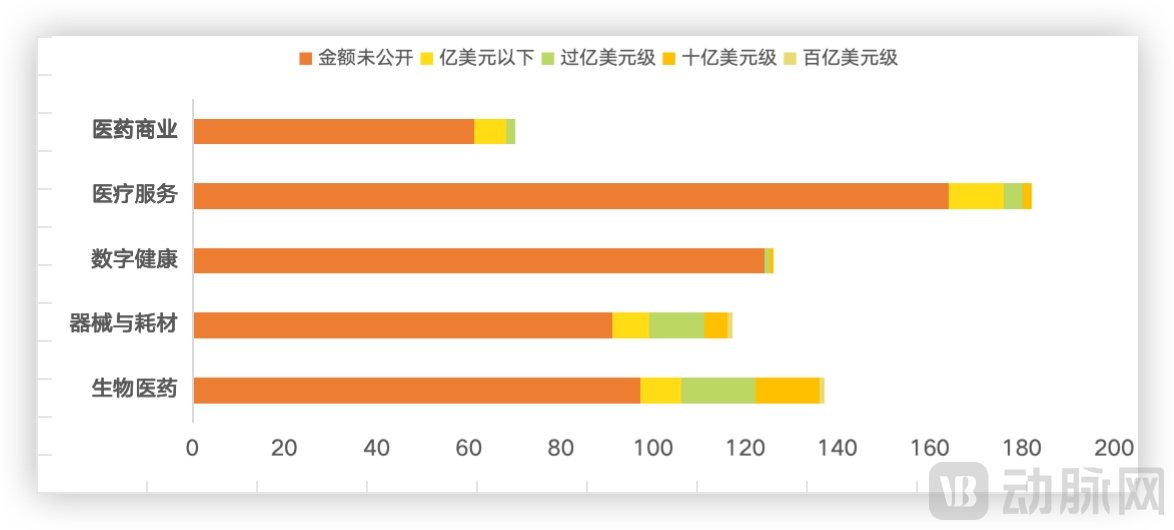

Distribution of Global M&A Transaction Values in the Healthcare Sector, 2024; Source: VBInsight

Although the healthcare services sector recorded the highest number of M&A transactions by volume, its overall transaction value lagged behind that of the biopharmaceutical and medical device/consumables sectors. Nevertheless, in terms of deal activity, consumer healthcare projects capable of generating stable revenue remain a key factor attracting acquirers. In particular, for companies pursuing scaled operations, acquiring locally established and mature enterprises offers a shortcut to growth. Furthermore, given the importance of specialized medical services within the healthcare system and their market appeal, specialized healthcare institutions have also become prominent targets for M&A transactions.

Overall, the total value of M&A transactions in 2024 decreased compared to 2023. In terms of deal size distribution, small- and medium-sized M&A deals predominated, with the most frequent transaction values falling in the range exceeding USD 100 million. The biopharmaceuticals and medical devices & consumables sectors remained the most closely watched subsectors, accounting for approximately 90% of the total transaction value. This concentration is also partly attributable to the higher volume of disclosed transaction data in these two fields.

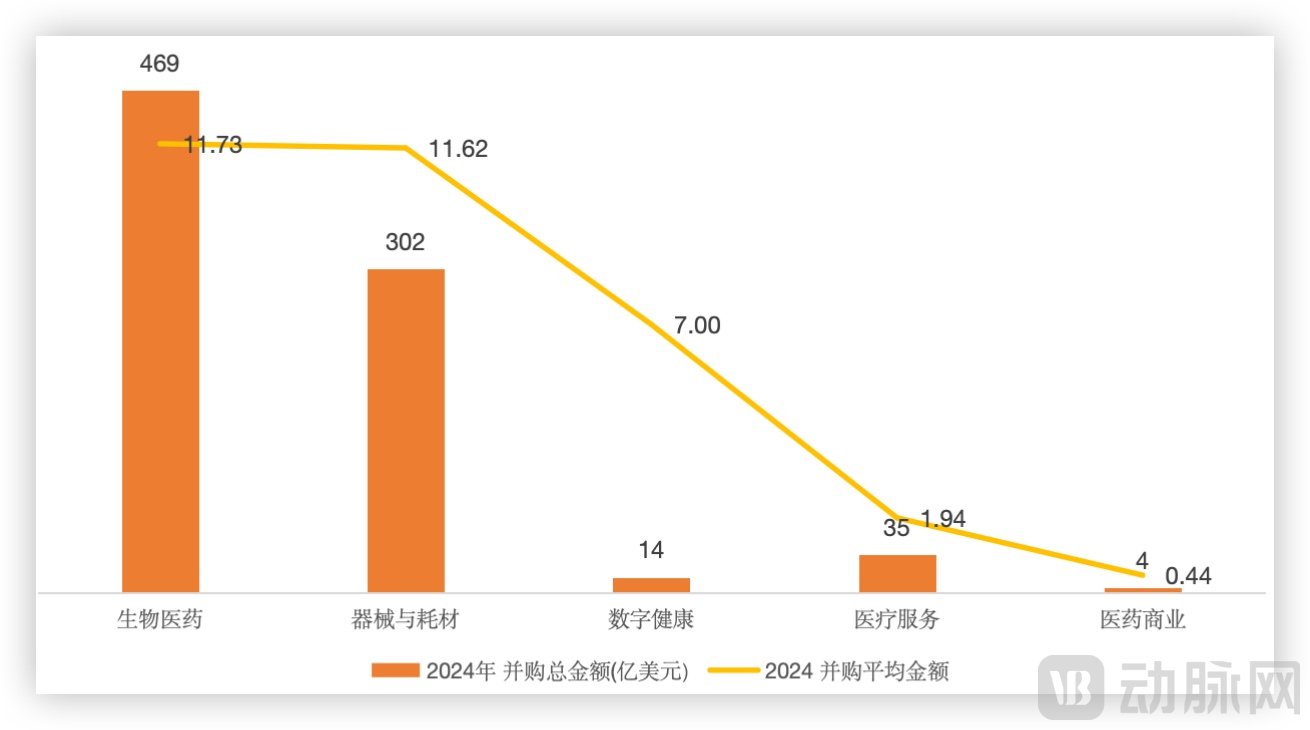

M&A Value and Average Deal Size in Healthcare Subsectors, 2024; Source: VBInsight

Excluding transactions with undisclosed amounts and analyzing the remaining deals reveals that the top three subsectors by average transaction value are biopharmaceuticals, medical devices and consumables, and digital health. Notably, although the total M&A transaction value in medical devices and consumables was approximately 36% lower than that in biopharmaceuticals, their average transaction values were nearly identical.

From a geographic perspective, the United States remains the industry’s center, with 67% of M&A transactions involving U.S. companies. Although China ranks second, its share is only 8.2%, marking a significant gap; the United Kingdom, in third place, accounts for roughly half of China’s share. Overall, the landscape continues to be characterized by a tripartite dominance among the United States, Europe, and China.

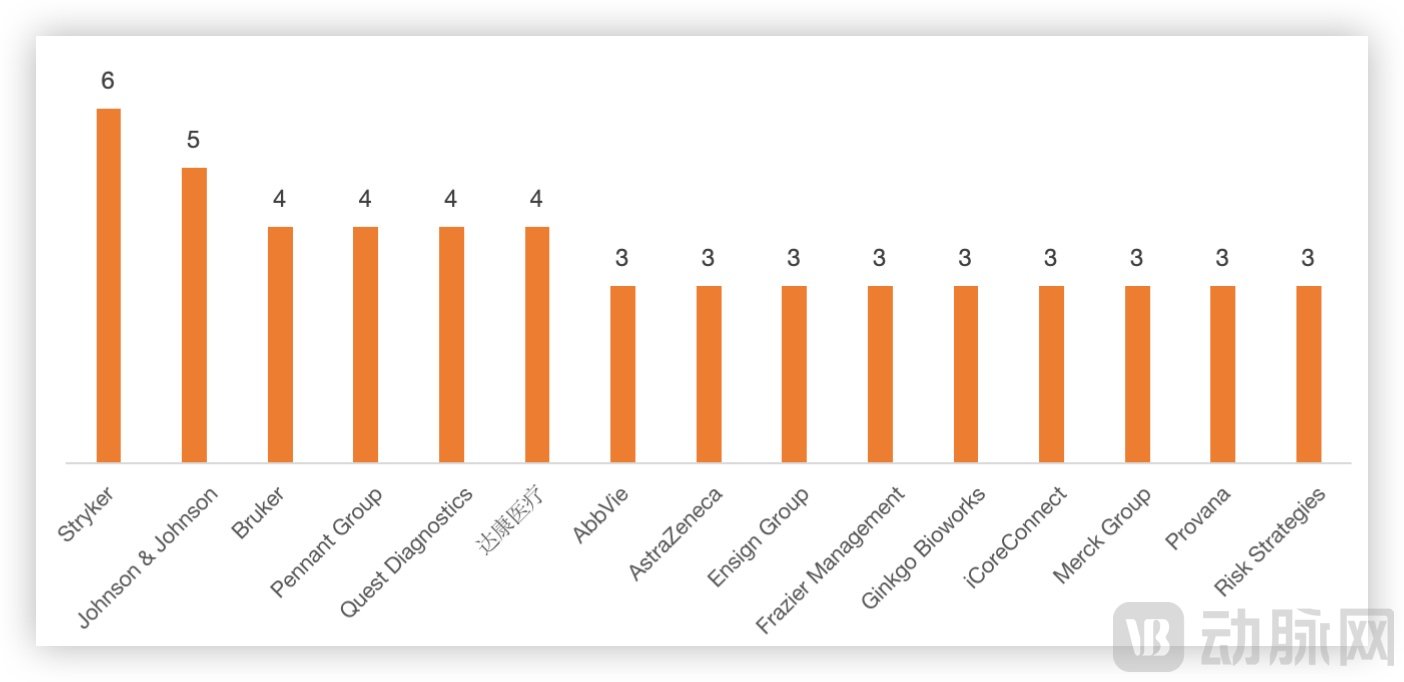

Companies That Made Multiple M&A Moves in 2024, Data Source: VBInsight

Large multinational corporations remained the primary driving force behind mergers and acquisitions in the healthcare industry in 2024.

Stryker, the global leader in orthopedics and medical devices, executed six acquisitions. Close behind, Johnson & Johnson also carried out multiple mergers and acquisitions in 2024, spanning various fields such as cardiovascular disease treatment device developers (Shockwave Medical) and gene therapy developers (Proteologix). These M&A activities demonstrate the strategic intent of multinational corporations to consolidate their leading position in the medical technology sector and further expand their market share by integrating global resources.

Of course, there are other transactions worth noting, such as Sichuan Harmony Shuangma Co., Ltd.'s cross-industry acquisition of Jianyuan Pharmaceutical.

Sichuan Shuangma, a company born out of the traditional construction industry, has demonstrated not only the strategic layout of domestic enterprises in anticipation of promising prospects in the biopharmaceutical sector through cross-industry investments, but also the emphasis placed by local companies on high-end technology R&D and innovation. Moreover, cases of achieving technological breakthroughs or market expansion through mergers and acquisitions are becoming increasingly common. For instance, Beauty Farm’s acquisition of Nailier enabled it to instantly gain approximately 200 directly operated stores, further expanding its market presence in the fields of medical aesthetics and health management.

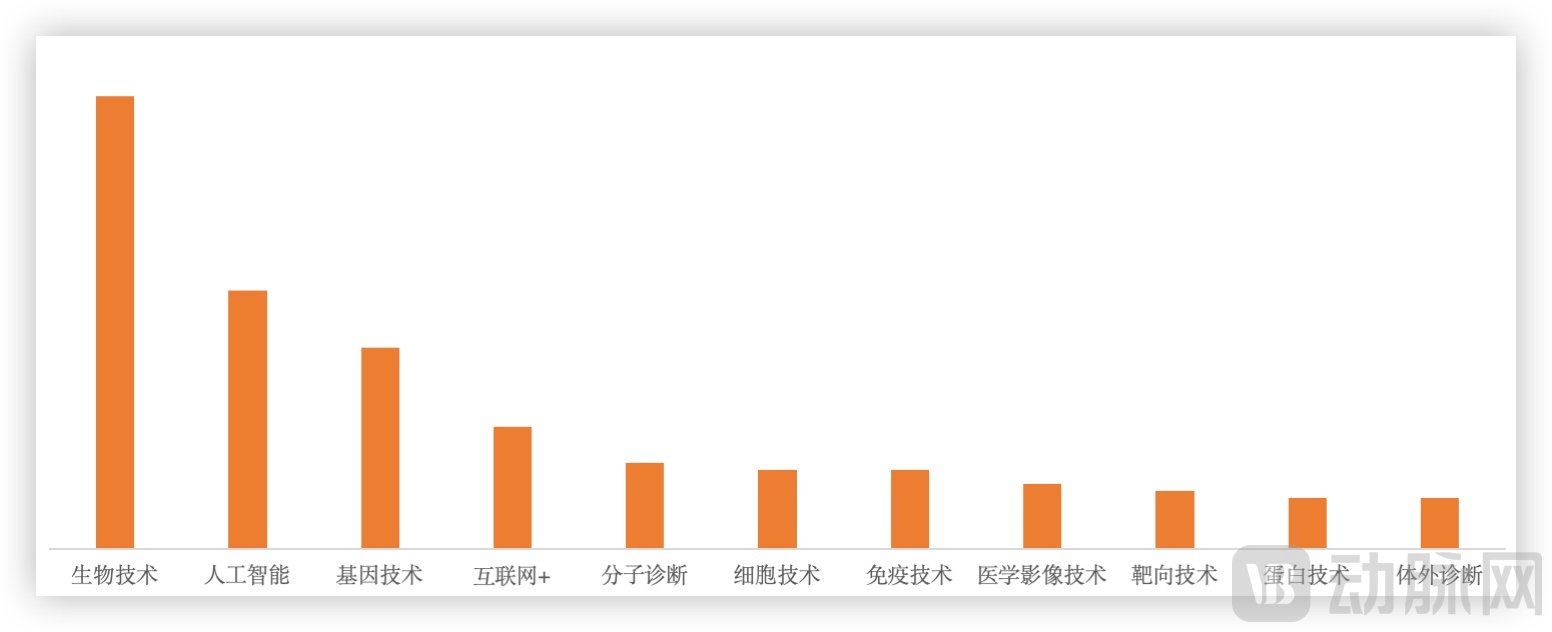

Hot Keywords for M&A in the Healthcare Industry in 2024, Data Source: VBInsight

As can be seen, the data is similar to that in VCBeat’s 2024 Investment and Financing Report: in 2024 M&A transactions, niche sectors such as artificial intelligence (AI), cell and gene therapy (CGT), and medical imaging saw significant increases compared to previous years. In particular, the AI sector experienced another wave of heightened interest in 2024, with companies and investors across the board increasing their commitments. Following the widespread popularity and breakout success of China’s DeepSeek during the Spring Festival holiday, it is easy to anticipate that AI will continue to remain at the forefront of market trends in 2025.

Top 10 Healthcare M&A Deals of 2024, Data Source: VBInsight

Overall, most M&A targets in 2024 demonstrated significant advantages in technological innovation.

For instance, Shockwave Medical, acquired by Johnson & Johnson at a significant premium, is a company dedicated to the development of medical devices for cardiovascular disease treatment. Its innovative Lithoplasty technology effectively minimizes damage to healthy tissue and enhances therapeutic outcomes. Such technology-driven innovators have become hot targets in the M&A market, reflecting the industry’s strong focus on and demand for cutting-edge technologies.

Biopharmaceuticals was one of the most concentrated sectors for M&A activity in 2024, accounting for approximately 60% of the total transaction value.

On the other hand, the capital winter in the biopharmaceutical industry continues. According to PwC data, the number of mergers and acquisitions (M&A) transactions in the global pharmaceutical and life sciences sectors decreased by 8% year-on-year in 2024. Data from the London Stock Exchange also shows that M&A activity in the global pharmaceutical industry has reached its lowest level in nearly a decade.

Top 10 M&A Deals in the Global Biopharmaceutical Sector in 2024, Data Source: VBInsight

Overall, M&A transactions in the biopharmaceutical sector in 2024 exhibited the following characteristics:

I. The overall transaction amounts are relatively small, with buyers aiming to supplement their pipelines; many multinational corporations (MNCs) are trending toward deals valued at under $5 billion.Among the Top 10 M&A Deals in the Global Biopharmaceutical Industry in 2024, compiled by VCBeat, well-known multinational corporations (MNCs) such as Pfizer, BMS, AbbVie, and Roche were notably absent.

II. Biotech Companies in Their Early Development Stage Are More Popular.According to incomplete statistics, the proportion of acquired companies in Phase III clinical trials or commercialization stages in 2024 decreased by approximately half compared to 2023. Multinational corporations (MNCs) are more risk-sensitive in the current macroeconomic environment; even when taking risks, they prefer to invest smaller amounts in emerging fields to strategically position themselves for the future.

III. From the perspective of therapeutic areas, oncology and autoimmune diseases are the absolute dominant sectors in mergers and acquisitions within the biopharmaceutical industry.From the perspective of niche sectors, ADCs, radiopharmaceuticals, and TCEs were the hottest tracks in 2024.

Specifically, the oncology sector remains a hotbed for innovative drugs, with various new therapies continually emerging, including cell and gene therapy (CGT), antibody-drug conjugates (ADCs), bispecific and multispecific antibodies, and radioligand therapies. Emerging companies in these niche segments have become targets for mergers and acquisitions by multinational corporations (MNCs).

Take Johnson & Johnson as an example. As ADC drugs have gained validation, the company has intensified its strategic investments in this area in recent years. From previous technical platform collaborations with Mersana and Duoxi Biologics, to the business development deal with LegoChem Biosciences, and culminating in the nearly $2 billion full acquisition of Ambrx, these moves all underscore Johnson & Johnson’s strong commitment to ADCs.

In addition to ADCs, the radioligand therapy (RLT) sector is also experiencing significant momentum.

Following Novartis’s success, competitors’ interest in radiopharmaceuticals has grown steadily, with substantial capital inflows and continuous pipeline expansion. A case in point is AstraZeneca’s $2.4 billion acquisition of Fusion, which not only boasts multiple radiopharmaceutical candidates in development but also possesses the capability to manufacture clinical-grade GMP radioactive doses. For AstraZeneca, a newcomer to this field, such an acquisition target is highly attractive.

The application of bispecific/multispecific antibodies in the field of oncology is also a key strategic focus for multinational corporations (MNCs).

Taking Merck’s $680 million acquisition of Harpoon as an example, although the transaction price was double Harpoon’s closing share price on that day, the deal was actually quite cost-effective. This merger not only enabled Merck to acquire a highly promising DLL3/CD3 antibody currently in clinical development, but also incorporated Harpoon’s multiple trispecific antibody platforms, particularly the next-generation ProTriTAC and TriTAC-XR trispecific antibody platforms capable of specific activation within the tumor microenvironment, thereby allowing Merck to rapidly enter the TCE (T-cell engager) sector.

Notably, TCEs are not only making significant strides in oncology but also show strong promise in the field of autoimmune diseases, with TCE assets emerging as a hot focus for business development (BD) in 2024.

For instance, Candid Therapeutics, which was established only a few months ago in the second half of 2024, acquired two domestic innovative TCE biopharmaceutical companies and subsequently entered into TCE collaborations with three other enterprises—Nona Bioscience, Biocytogen, and Ab Studio—within a short period. Multinational corporations (MNCs), including GSK and Merck & Co., have also reached agreements with Chinese biotech firms regarding TCE products; however, these MNCs have opted to advance the TCE pipelines from Chinese biotechs, originally intended for oncology indications, into clinical trials for autoimmune diseases.

Coupled with a series of mergers and acquisitions in the first half of 2024—including Novartis’ $250 million acquisition of Calypso in January; Regeneron’s acquisition of 2seventy bio in April; Johnson & Johnson’s spending of over $2 billion to acquire two autoimmune biotech companies in May; and Asahi Kasei’s announcement of its $1.06 billion acquisition of Calliditas—these moves all reflect the emphasis multinational corporations (MNCs) are placing on the autoimmune disease sector.

From an industry development perspective, the M&A landscape in 2024 was not optimistic. The absence of mid-to-large-scale deals in the $5 billion to $10 billion range reflects a lack of confidence in the overall growth of the sector.

In 2024, the global medical device industry witnessed over 100 M&A transactions, with a total value exceeding $30 billion.

In the medical device industry, which comprises numerous niche segments, these segments are typically small in scale and exhibit low technological generalizability. Global giants in the medical device sector are reluctant to engage directly in development; instead, they opt to acquire technologies that have already undergone clinical validation. This approach is exemplified by companies such as Johnson & Johnson, Medtronic, and Boston Scientific.

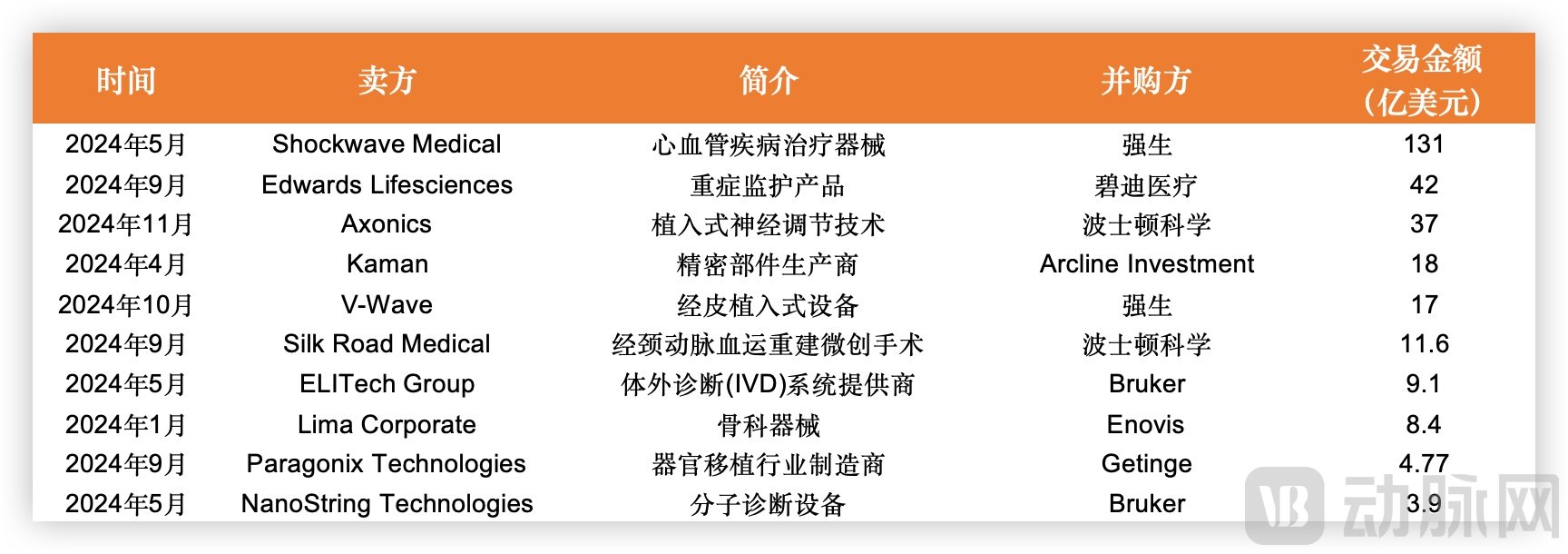

Top 10 M&A Deals in the Global Medical Devices and Consumables Sector by Value in 2024, Source: VBInsight

Therefore, we can analyze the strategic intentions of these multinational giants and their impact on industry development through these mergers and acquisitions.

In April 2024, Johnson & Johnson acquired Shockwave for $13.1 billion to expand its business in the fields of coronary artery disease and peripheral artery disease. The addition of Shockwave provides strong complementarity and support to Johnson & Johnson’s existing Abiomed cardiac recovery solutions and Biosense Webster electrophysiology technologies. Subsequently, in October, Johnson & Johnson completed the acquisition of V-Wave, a manufacturer of atrial shunt devices, for $1.7 billion. The integration of V-Wave will enable Johnson & Johnson to offer more diverse and effective treatments for heart failure, addressing the unmet needs of approximately 800,000 patients with heart failure with reduced ejection fraction (HFrEF) annually.

Subsequently, in September, Boston Scientific completed its acquisition of Silk Road Medical for $1.16 billion. Silk Road Medical is a medical device company that pioneered new approaches to stroke prevention and the treatment of carotid artery disease through Transcarotid Artery Revascularization (TCAR), a minimally invasive procedure. The integration of the TCAR platform strengthens Boston Scientific’s vascular technology solutions.

The domestic market is no exception. In January 2024, Mindray Medical announced the acquisition of a 24.61% stake in Hytech Medical, a medical device company listed on the STAR Market, for RMB 6.65 billion through “agreement-based transfer plus the waiver of voting rights by the original actual controller,” thereby securing control over Hytech Medical. Through this transaction, Mindray Medical will enter the cardiovascular sector.

It is evident that the cardiovascular and cerebrovascular sector has become a key arena for medical device innovation worldwide. Currently, the treatment of cardiovascular and cerebrovascular diseases is gradually transitioning toward precision and personalization. With the continuous emergence of various innovative technologies, industry giants are significantly increasing their financial investments to address their own shortcomings and ensure they maintain a leading position in the fiercely competitive market.

Moreover, Stryker’s multiple M&A activities in 2024 were particularly noteworthy. According to incomplete statistics, through a series of acquisitions, Stryker has significantly strengthened its strategic layout in various fields, including chronic low back pain, artificial intelligence, soft tissue fixation, neurointervention, and joint consumables. Regarding this series of “combination punches” by Stryker, its CEO pointed out during the earnings conference that although these M&A transactions were not large in scale, they played a crucial role in complementing the company’s business.

It is evident that by leveraging mergers and acquisitions (M&A), medical device giants can rapidly keep pace with the iteration of new technologies, thereby optimizing their strategic layouts. Meanwhile, M&A effectively facilitates rapid market entry and enables swift global expansion. Furthermore, M&A helps refine supply chain systems, making corporate ecosystems more robust and diversified.

Looking Back at 2024: M&A Activity in the Healthcare Sector Remained Frequent, Yet Deal Sizes Trended Downward. This phenomenon may reveal the predicament currently facing the industry. On one hand, sellers are gripped by panic amid a capital winter, with companies under immense pressure from investors seeking exits; on the other hand, buyers have grown increasingly cautious, placing greater emphasis on risk assessment, leading to widening valuation gaps between the two parties.

By 2025, the situation may change as a wave of mergers and acquisitions in the healthcare industry is emerging.

Johnson & Johnson announced in early 2025 its $14.6 billion acquisition of Intra-Cellular Therapies, a company focused on the central nervous system (CNS) sector; Stryker announced the acquisition of Inari Medical for nearly $5 billion; and Boston Scientific also announced in early 2025 that it would acquire the remaining shares of Bolt Medical for $664 million. These moves may signal that more blockbuster mergers and acquisitions will emerge in 2025.