Chinese Pharma Firms Hit the Brakes on Diversification: Asset Sales Surge as Companies Refocus on Core Businesses

WuXi AppTec

New Drug R&D and Production Service Provider

HUTCHMED

Biopharmaceutical Manufacturer

During the recently concluded Spring Festival holiday, the pharmaceutical industry remained active, with nearly all major players offloading their core assets.

Take WuXi AppTec, a CRO giant, as an example. On January 17, 2025, it announced the sale of its U.S. medical device testing business, selling its two major facilities in Atlanta and St. Paul to NAMSA. In fact,This marks WuXi AppTec’s third sell-off in the past month., the previous two transactions involved the cash sale of equity interests in WuXi ATU’s U.S. and U.K. operating entities to Altaris, as well as the divestiture of its vaccine manufacturing facility in Ireland to Merck & Co. for a total consideration of $500 million.

This is not an isolated case; many pharmaceutical companies have recently accelerated their retreat. For instance, HUTCHMED, under Li Ka-shing, announced in January 2025 that it would sell a 45% equity stake for $608 million to divest its traditional Chinese medicine assets. Additionally, at the beginning of the year, SHINVA MEDICAL INSTRUMENT CO.,LTD. again made headlines for offloading hospital assets, formally listing for transfer its 55% controlling stake in Shandong Xinhua Changguo Hospital, with a minimum transfer price of RMB 113 million. Furthermore,Nearly 30 leading pharmaceutical companies, including Luoxin Pharmaceutical, Guangji Pharmaceutical, Weiming Medicine, Tongcheng Pharmaceutical, and Jointown Pharmaceutical, completed their “slimming-down” initiatives during the Spring Festival period.。

New Year, New Outlook: What Industry Signals Are Revealed by the Pharmaceutical Sector’s Collective Divestitures and Spin-offs?

When Diversity Becomes a “Hot Potato”

From the asset sell-offs by domestic pharmaceutical companies during the Spring Festival period,“Selling hospitals” has almost become the common choice. In addition to SHINVA MEDICAL INSTRUMENT CO.,LTD mentioned earlier, several other listed pharmaceutical companies, including Changbao Shares, Jingfeng Pharmaceutical, Humanwell Healthcare, China Resources Sanjiu, and Yibai Pharmaceutical, have recently been transferring their equity stakes in affiliated hospitals.

There are certainly reasons behind this. Taking SHINVA MEDICAL INSTRUMENT CO.,LTD. as an example, the company has repeatedly listed its subsidiary hospitals for equity transfer in recent years, including the sale of an 80% stake in Nanyang Orthopedic High-Tech Zone Hospital in April 2020 and a 70% stake in the West Branch of Zibo Zichuan District Hospital in December 2020. The rationale for these concentrated divestitures is clearly outlined in its annual reports: in recent years, medical services have accounted for less than 10% of SHINVA’s revenue, while capital expenditures have continued to rise. This disparity has directly led to a growth bottleneck. In 2022, in particular, the company’s revenue and net profit growth rates declined by 2.11% and 9.68%, respectively, forcing it to abandon its loss-making medical services segment.

Figure 1. Overview of Hospitals and Healthcare Institutions under Representative Pharmaceutical Companies in 2018

Figure 1. Overview of Hospitals and Healthcare Institutions under Representative Pharmaceutical Companies in 2018

In fact, since the rise of “socially run healthcare” in 2018, domestic pharmaceutical companies have frequently entered the healthcare services sector through acquisitions or by building and merging their own facilities, with the clear objective of cultivating new growth curves. However, ideals often fall short of reality. In the later stages, adjustments to medical insurance policies and changes in the market environment, coupled with the high operational costs of hospitals and prolonged payback periods, have increasingly strained the financial resources of these pharmaceutical companies, leading many to exit the sector in recent years.

From this, it is not difficult to see that,Pharmaceutical Companies’ Diversified Portfolios Are Showing a Significant Trend of Contraction. In fact, besides selling hospitals, other typical manifestations of pharmaceutical companies abandoning diversification include cutting pipelines, terminating non-core businesses, transferring factories, and implementing significant layoffs.

Take WuXi AppTec as an example. In January this year, it divested its overseas assets for the third consecutive time. This move was certainly driven by changes in the international landscape, such as the passage of the U.S. Biosecure Act, which has posed unprecedented challenges to the global pharmaceutical outsourcing industry. Timely divestment not only reduces its risk exposure in the U.S. market but also enables rapid cash recovery, thereby enhancing its resilience against risks.

But on the other hand,WuXi AppTec’s successive divestitures of overseas businesses are, in effect, a move toward “de-diversification.”A set of data precisely substantiates this point. According to the latest annual report, WuXi AppTec’s total operating revenue for the first three quarters of 2024 amounted to RMB 27.702 billion, representing a year-on-year decrease of 6.23%; net profit attributable to shareholders of the parent company was RMB 6.533 billion, down 19.11% year on year. However, after excluding specific commercial manufacturing projects, the company’s revenue would have increased by 4.6% year on year.

This means that it is imperative for WuXi AppTec to “streamline operations and simplify processes.” The reasons behind this are also clear,Amid global economic weakness, market demand has declined significantly while production costs remain high, placing many business segments under severe financial strain. Over time, the mounting economic pressure makes divestiture a viable option to cut losses promptly.。

In fact, the divestment of overseas assets is only one part of WuXi AppTec’s broader retreat; another aspect is reflected in its shareholding reductions. It is reported that WuXi AppTec realized cumulative investment gains of RMB 2.016 billion from the sale of WuXi XDC shares in 2024, accounting for more than 10% of its audited net profit attributable to shareholders of the parent company in 2023. Among this amount, approximately RMB 720 million impacted the company’s net profit for 2024, while approximately RMB 1.297 billion impacted its net profit for 2025.

A Microcosm of the Industry: When Diversification Becomes a Constraint, Even Pharmaceutical Giants Choose to Accelerate Their Exit. In this regard, a partner at Weilai Capital stated, “Operating at a loss is currently the norm for pharmaceutical companies. Three years ago, rapid expansion could still be sustained by financing from both primary and secondary markets. Now, with a downturn across the entire market, continuing with an aggressive, high-spending strategy is clearly unsustainable.”It would be better to divest from the underperforming production and sales lines and focus on R&D, which will provide pharmaceutical companies with greater cash flow to support future business operations.”

Accelerating the Return to the "Main Quest"

At this year’s Tencent Group annual meeting, Ma Huateng, Chairman of the Board and CEO of Tencent, specially"Focus on Core Business"As a keyword in the speech. Looking back at Tencent’s development history, its transformation from a social networking app into today’s business empire is precisely attributable to its maximization of diversified layout. Yet even Tencent, so adept at diversification, has now begun to pause for reflection and gradually shift its focus back to its core businesses.

In fact, “focusing on core businesses” has already become a central issue for the entire industry, and this is especially true in the pharmaceutical sector, which requires substantial investment and has long payback periods. It is reported that in recent announcements by numerous pharmaceutical companies regarding asset divestitures, key phrases such as “optimizing resource allocation,” “improving asset quality,” and “enhancing operational efficiency” have been repeatedly mentioned, with the underlying intent being self-evident.The goal is to gradually divest non-core assets and concentrate more resources on the core business.。

Taking HUTCHMED as a key example, the company, originally a traditional Chinese medicine (TCM) enterprise, has been accelerating its transformation toward innovative drugs in recent years. It has continuously divested its TCM businesses and reinvested the proceeds into advancing its core pipeline. In this regard, HUTCHMED stated, “As the business direction of Shanghai Hutchison Pharmaceuticals differs from HUTCHMED’s core innovative drug business, and given HUTCHMED’s intention to focus more heavily on the innovative drug segment, the company has been exploring ways to convert the potential value of non-core businesses into tangible value in recent years.”

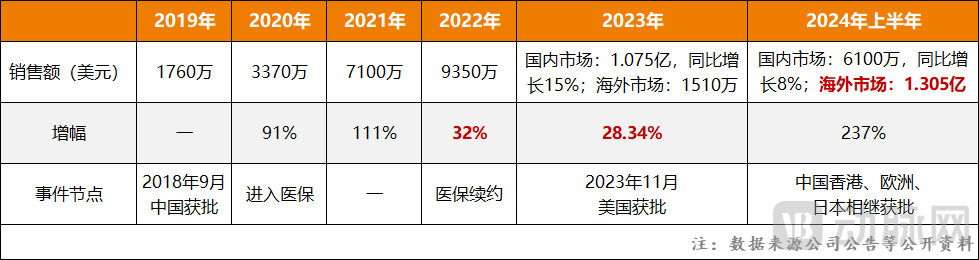

Figure 2. Global Sales of Fruquintinib

Figure 2. Global Sales of Fruquintinib

There are two main reasons for doing so,On the one hand, innovative drugs offer greater growth potential.. In January 2023, Takeda acquired the global rights to HUTCHMED’s fruquintinib for $1.16 billion, after which the drug was rapidly approved and launched in key markets such as the United States, Europe, and Japan. According to projections by authoritative institutions, fruquintinib’s global peak sales could reach as high as $1.5 billion, indicating that HUTCHMED stands to gain substantial revenue from this arrangement.

On the other hand, it is also due to the need to concentrate ammunition to seize market progress.. Currently, HUTCHMED is accelerating the R&D and commercialization of multiple innovative drugs, including savolitinib and surufatinib, all of which require substantial financial support. The divestment of non-core assets serves this purpose well; for instance, the complete exit from its traditional Chinese medicine business brought HUTCHMED an immediate inflow of RMB 4.5 billion, thereby providing it with greater leverage in future competition.

Of course,“Focusing on core business” is not only reflected in the divestiture of non-core assets; the current trend of pharmaceutical companies “selling off subsidiaries” is also a manifestation of this strategy.. It is reported that during the Spring Festival, several listed pharmaceutical companies, including Luoxin Pharmaceutical, Guangji Pharmaceutical, Tongcheng Pharmaceutical, Jointown Pharmaceutical, and Weiming Medicine, chose to sell their subsidiaries. This move not only generates short-term cash flow to alleviate current tight financial pressure but also allows these companies to retain certain high-quality assets, thereby enabling them to seek more breakthrough opportunities in their familiar markets.

In response, a seasoned pharmaceutical industry professional stated, “In recent years,The global economy is facing a major test, with simultaneous tightening in both commodities and currencies, leaving fewer market opportunities for pharmaceutical companies to capture., and at the same time, intense competition within the industry continues to accumulate, leading to continuously rising core requirements for pharmaceutical companies. In light of this, if pharmaceutical companies wish to ensure survival or even achieve sustained growth, focusing on their core business is undoubtedly a smart strategy.Only by continuously strengthening internal capabilities and solidifying the foundational base can one break through first during a bottoming-out cycle.。”

Can You Really Start Running After Losing Weight?

It is not difficult to observe that Chinese pharmaceutical companies are currently divesting assets one after another, essentially to position themselves for the future. However, the ultimate outcome and the extent to which these commitments will be fulfilled remain uncertain. Nevertheless, we can look to multinational corporations (MNCs) that have taken earlier steps for insights.

In fact, long before domestic pharmaceutical companies began to divest assets on a large scale, multinational corporations (MNCs) had already seen undercurrents of change, specifically manifested in aggressive pipeline cuts and continuous adjustments to their global business structures.

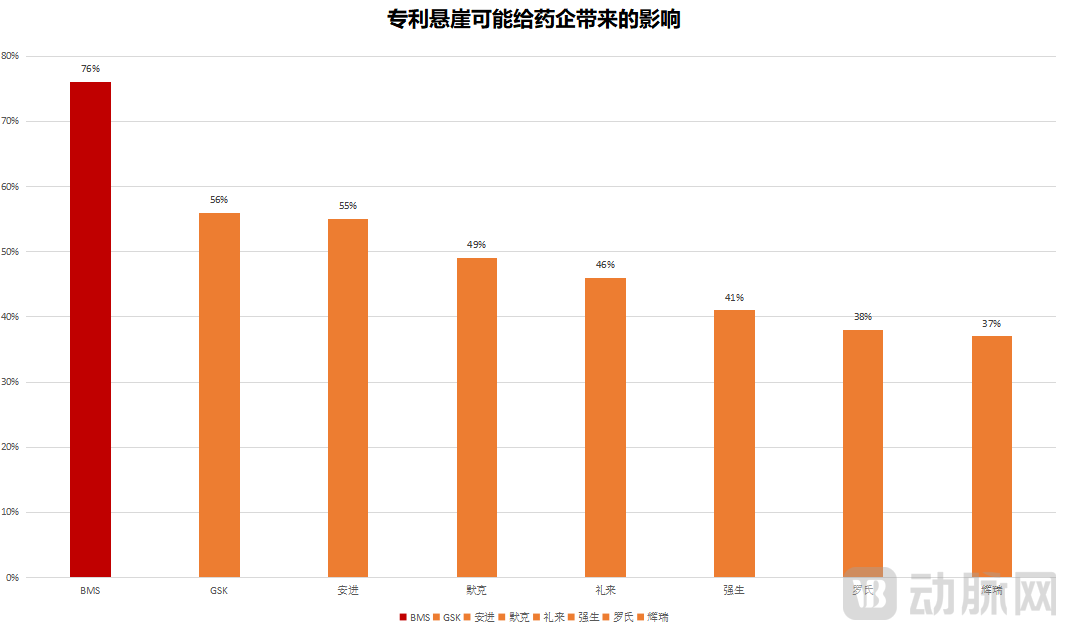

Figure 3. Potential Impact of the Patent Cliff on Pharmaceutical Companies (Source: Bloomberg)

Figure 3. Potential Impact of the Patent Cliff on Pharmaceutical Companies (Source: Bloomberg)

Let’s start with the pipeline. In fact, pruning pipelines is not uncommon for multinational corporations (MNCs). In recent years, MNCs have faced varying degrees of patent challenges. According to Bloomberg’s predictive analysis, the impact of the patent cliff on pharmaceutical companies such as BMS, GSK, Amgen, Merck, Eli Lilly, and Johnson & Johnson could exceed 40% within the next five years. To address this, MNCs have aggressively acquired external pipelines in recent years, which has correspondingly led to more frequent pipeline cuts.

However, a significant departure from previous trends is that multinational corporations (MNCs) are terminating R&D pipelines at much earlier stages, primarily concentrating on Phase I clinical trials and preclinical phases. Taking Bristol Myers Squibb (BMS) as an example, known as the “king of deal terminations,” the company cut nearly 30 R&D pipelines in 2024, with up to 70% of these terminated programs being in Phase I clinical trials or earlier stages. This indicates that,MNCs are currently more sensitive to their pipelines; at the first sign of trouble, such as setbacks in R&D progress, they immediately choose to cut losses. This marks a significant departure from the past, when projects were typically carried through to Phase II/III clinical trials or even until regulatory approval before being terminated.。

Certainly,MNCs’ resolve to withdraw is reflected not only in pipeline cuts but also in the tightening of their global business footprint.。

It is reported that during the Spring Festival, several multinational corporations (MNCs) chose to exit the Chinese market. For instance, UCB sold, divested, and licensed its neurology and allergy business in China to CBC Group, Asia’s largest healthcare-focused specialized asset management group, and Mubadala, an investment company headquartered in Abu Dhabi, for $680 million. Additionally, Kyowa Kirin transferred its shares in Kyowa Kirin (China) Pharmaceutical Co., Ltd. to a newly established special purpose vehicle (SPV), which subsequently transferred all shares of the new entity to Hong Kong-based WJ Pharmaceutical Group for RMB 720 million.

If this is the case in China, an emerging market for innovative drugs globally, then the withdrawal of multinational corporations (MNCs) from other non-mainstream markets is evidently faster and more thorough.

So, what results did MNCs actually achieve after the great retreat? According to the annual report data for the third quarter of 2024,The Top 10 MNCs have shown a significant upward trend in both revenue and revenue growth rate. While overall R&D expenditure, which is directly linked to costs, continues to rise, the proportion of revenue allocated to R&D has slightly declined.. This indicates that multinational corporations (MNCs) have achieved significant results in “cost reduction and efficiency enhancement.” However, this is not absolute; if they fail to seize the appropriate timing for exit, or if their actions lack sufficient rationality and thoroughness, they may instead become further entrenched.

This mirrors the logic currently driving pharmaceutical companies to seek an “exit.” Whether to continue pushing for an IPO, opt for acquisition or merger, or transfer equity stakes requires a comprehensive analysis based on the company’s specific circumstances and evolving market conditions, thereby identifying the path that maximizes its own interests.

But regardless, this wave of asset divestitures by pharmaceutical companies is already sending a key message to the industry:Innovative drug companies, especially those in the early stages, should base their core competitiveness on pipeline innovation rather than on building a complete commercialization system.Therefore, it is a highly pragmatic and rational approach for pharmaceutical companies to divest equity after completing phased research prior to market launch or upon reaching key milestones, or alternatively, to collaborate with or be acquired by partners possessing more robust distribution channels and commercialization capabilities.

Overall, in the current era of increasingly complex market conditions,Pharmaceutical companies need to be more realistic and flexible, promptly embracing the principle of “discard and let go” to maintain stronger cash reserves. Only by staying in the game can they survive the prolonged winter.。

1. “The Hidden Logic Behind WuXi AppTec’s ‘Sell, Sell, Sell’” – Jin Duan;

2. “Amid Frenzied Restructuring, Pharmaceutical Companies Are Selling Off Hospitals” — Saimilan;

3. “Li Ka-shing Exits: Hutchison Pharma Sells for RMB 4.5 Billion” – Investment Circle.