China's First Joint Robotics White Paper Released: Digital-Intelligent Orthopedics Crossing the 'Roche Limit' from Manual to Smart Surgery

Undoubtedly, DeepSeek R1, this “digital nuclear bomb,” has allowed us to tangibly feel how China’s innovative power is deeply penetrating various sectors and rewriting the trajectory of industrial development. The healthcare industry is no exception, as domestically produced surgical robots are gradually breaking the landscape once dominated by foreign technologies.

China boasts fertile ground and vast potential for the development of its robotics industry. However, as patient demand continues to rise, the shortage of high-quality medical resources has become increasingly prominent. On one hand, the number of patients with bone and joint diseases is substantial, exceeding 140 million, which accounts for more than 10% of the total population.1; on the other hand, there is a relative shortage of orthopedic practitioners in China, and it takes 5–7 years and nearly 500 surgeries for a joint surgeon to become proficient.2Surgical culture period.

Joint replacement is the primary treatment for end-stage osteoarthritis, but the clinical efficacy of traditional joint replacement has reached a bottleneck and plateau.The iteration of technologies and tools is the primary means of resolving this contradiction.The advent of orthopedic joint surgical robots marks a shift in surgical practice from traditional “manual” techniques toward precision, minimally invasive, and intelligent approaches. This innovation brings new perspectives and higher-dimensional insights to joint replacement, has become a frontier hotspot in the field of joint surgery, and the application of robot-assisted technology in joint surgeries has become an inevitable trend.

To build industry consensus,National Clinical Research Center for Orthopedics, Sports Medicine and Rehabilitation; Department of Orthopedics, Chinese PLA General Hospital, in collaboration with VCBeat and VCBeat Research Institute, jointly released China’s first panoramic insight and innovation report on joint surgery robots—“White Paper on the Development of the Orthopedic Joint Surgery Robot Industry”。

Over the past year, we have conducted extensive visits across clinical, industrial, research, and capital sectors, interviewing more than 40 leading domestic and international experts in orthopedics as well as representatives from over ten innovative enterprises. This effort has culminated in an in-depth report comprising four major sections and totaling 80,000 words. Herein, we highlight ten core insights from the report to provide reference and valuable perspectives for scholars, policymakers, entrepreneurs, and investors both within and outside the industry.

- 01 -

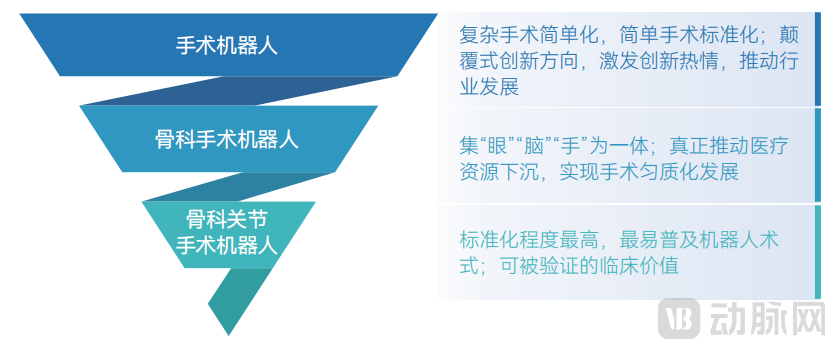

The most widely applied, with the largest cumulative data and the broadest prospects for use

Intelligent Surgical Instruments

Compared with laparoscopic surgical robots, orthopedic surgical robots can significantly reduce the requirements for surgeons’ operative skills, thereby facilitating broader adoption in resource-limited settings such as primary care hospitals and promoting standardization of surgical procedures.

Furthermore, compared with other orthopedic surgical robots, the operational procedures and technical standards for joint replacement surgery are the most standardized, which facilitates the widespread adoption of robot-assisted techniques in the field of joint replacement. As the intelligent surgical tool with the broadest application prospects, joint surgery robots offer four core advantages: 1) preoperative planning and precise intraoperative execution, reducing surgical variability and errors; 2) shortening the learning curve and rapidly enhancing surgical skills; 3) quantifying experience and quality to create a virtuous cycle; and 4) addressing complex cases such as joint revision surgery, thereby improving long-term outcomes.

Figure: Core Clinical Value of Three Types of Surgical Robots, Source: VCBeat

- 02 -

Co-operate!

The Essence of Joint Surgery Robots: Highly Efficient, Intelligent Assistive Tools

Joint surgical robots are primarily used in three procedures: total hip arthroplasty (THA), total knee arthroplasty (TKA), and unicompartmental knee arthroplasty (UKA). The volume of these three major procedures is showing a rapid upward trend. Among them, the annual number of TKA procedures is comparable to that of THA, at approximately 600,000–700,000 cases; the annual number of UKA procedures is less than 100,000 cases, but its growth rate is expected to rise rapidly in the future.3。

However, robot-assisted surgery is not simply about operating the robot, but rather co-operating with it to perform the procedure.Following extensive research, the majority of physicians believe that joint surgery robots, as highly efficient and intelligent auxiliary tools, have broad application prospects. However, over the foreseeable future, they will not completely replace surgeons; rather, they will serve as an extension of the surgeon’s “eyes,” “brain,” and “hands,” assisting in preoperative planning, device registration and matching, intraoperative real-time navigation, robotic arm motion control, and postoperative assessment. Ultimately, through deep collaboration between surgeons and robots, patients will receive superior treatment experiences and outcomes.

Figure: Three Types of Joint Surgical Robots, Data Source: Public Information

- 03 -

Weak initial momentum, strong late-stage surge,

Post-2018, Chinese Enterprises Accelerate Catch-Up Amid Fierce Competition

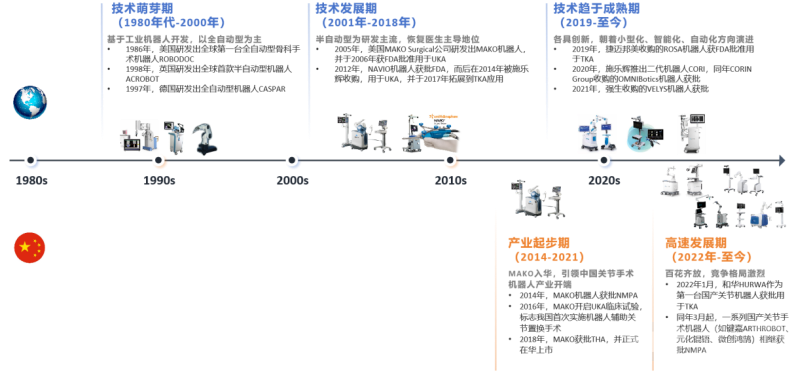

Orthopedic joint surgery robots have been in development for over three decades, which can be broadly divided into three stages: the nascent technology phase (1980s–2000), the technology development phase (2001–2018), and the technology maturation phase (2019–present). Most domestic companies in China entered the market only during the third stage, with relatively insufficient early technological accumulation and market preparation; consequently, the industry’s development lags behind that of overseas markets.

Against the backdrop of the continuously evolving global technological landscape, China has rapidly advanced in fields such as artificial intelligence, mechanical manufacturing, high-performance materials, image recognition, mechanical fabrication, and electronics and electrical appliances, gradually emerging as one of the nations with the most comprehensive technological systems.

Currently, China’s orthopedic joint surgery robot industry is experiencing robust growth, with a significant catch-up trend. The number of approved products has surged from one between 2016 and 2018 to 18 by the end of August 2024. In the future, empowered by domestic large AI models such as DeepSeek, orthopedic joint surgery robots will further enhance their technical capabilities and broaden their application prospects. Meanwhile, as an increasing number of companies worldwide secure market entry, competition is inevitably set to intensify.

Figure: Development History of Joint Surgery Robots in China and Internationally. Data Source: Public Information, Compiled by VCBeat.

- 04 -

Most Chinese enterprises have entered the Series B commercialization validation stage,

Unique Advantages of the Domestic Market Emerge

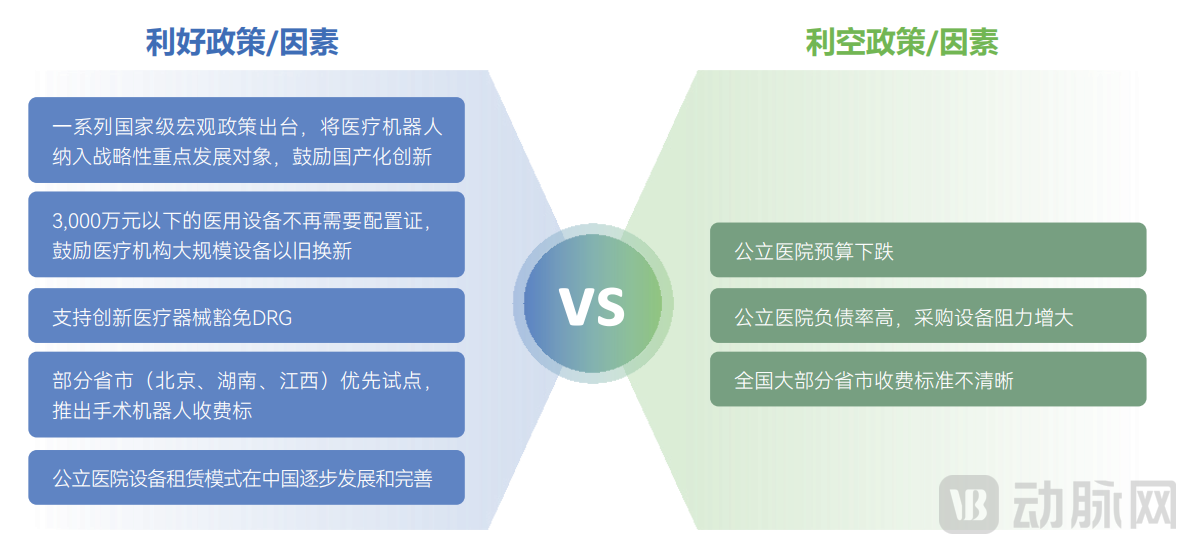

In terms of investment and financing, the global surgical robotics market reached a historical peak in 2021. Since then, most Chinese companies have successively entered the Series B stage of commercial validation after 2022. Regarding market landscape, the overseas surgical robotics market has become relatively stable after years of development. In contrast, the domestic market, leveraging unique advantages such as vast medical demand, a robust supply chain system, and policy support, has become an ideal “fertile ground” for nurturing next-generation robotic systems.

Despite the current shortcomings or resistance in underlying technologies and basic equipment, collaborative innovation models between medicine and engineering, and policy support (review, certification, medical insurance, etc.), as well as the downturn in the global capital market, in the long run,China’s supply chain coordination capabilities and its unique advantages in artificial intelligence and 5G technology will provide strong support for the development of orthopedic surgical robots.This development trend is unstoppable. Once the industry identifies a stable and sustainable business model, it is poised to once again attract significant capital attention, ushering in a new golden age of growth.

Figure: Summary of Favorable/Unfavorable Policies/Factors for Joint Surgery Robots; Data Source: Public Information, Compiled by VCBeat

- 05 -

China's Joint Surgery Robot Market Is Accelerating Its Expansion,

Poised to surpass RMB 1 billion within five years, with long-term prospects exceeding RMB 10 billion

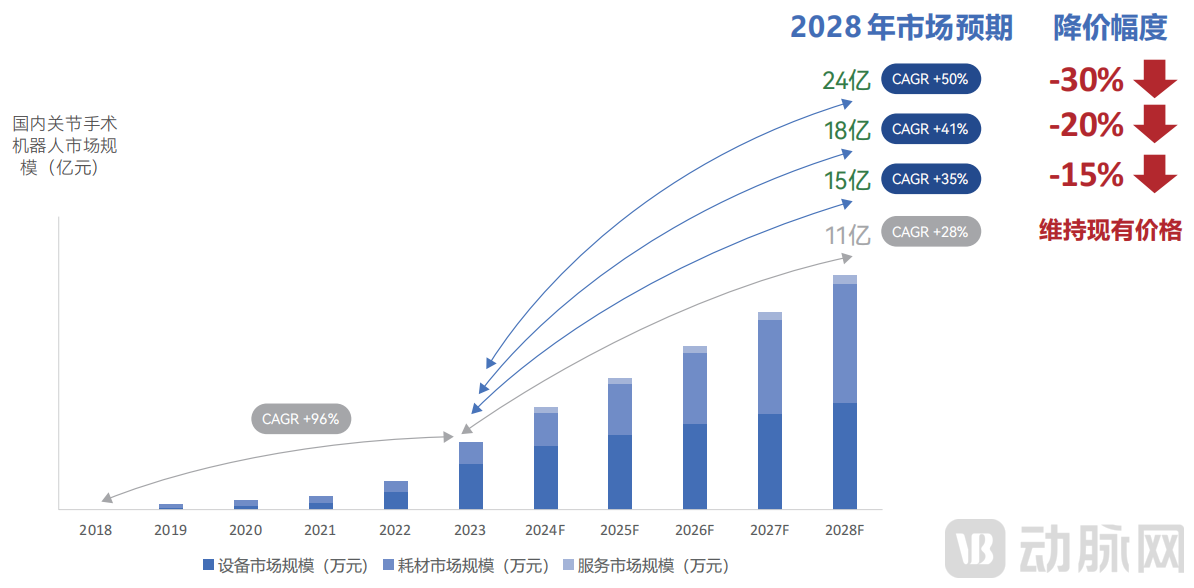

In 2023, the total number of newly installed joint surgery robots in China was approximately 45 units, with the volume of robot-assisted joint surgeries exceeding 15,000 cases. Calculated at ex-factory prices, the overall market size amounted to around RMB 320 million. Assuming stable pricing for surgical robots, the overall market size is projected to surpass RMB 1 billion by 2028.4。

From a long-term perspective,Joint robots are bound to expand beyond large medical centers and gradually become widespread in municipal hospitals and specialized hospitals.After taking into account parameters such as the penetration rate of robotic surgery, the depreciation period of equipment, and the decline in equipment prices, we have calculated thatThe Market Size of Joint Surgery Robots in China Will Approach 13 Billion Yuan。

Figure: Projected Market Size of Domestic Joint Surgery Robots in China, 2018–2028F; Source: VCBeat Estimates

- 06 -

Accelerated approval of domestic products in China over the past three years,

New Installed Capacity on Par with Overseas Markets, with a Clear Substitution Trend

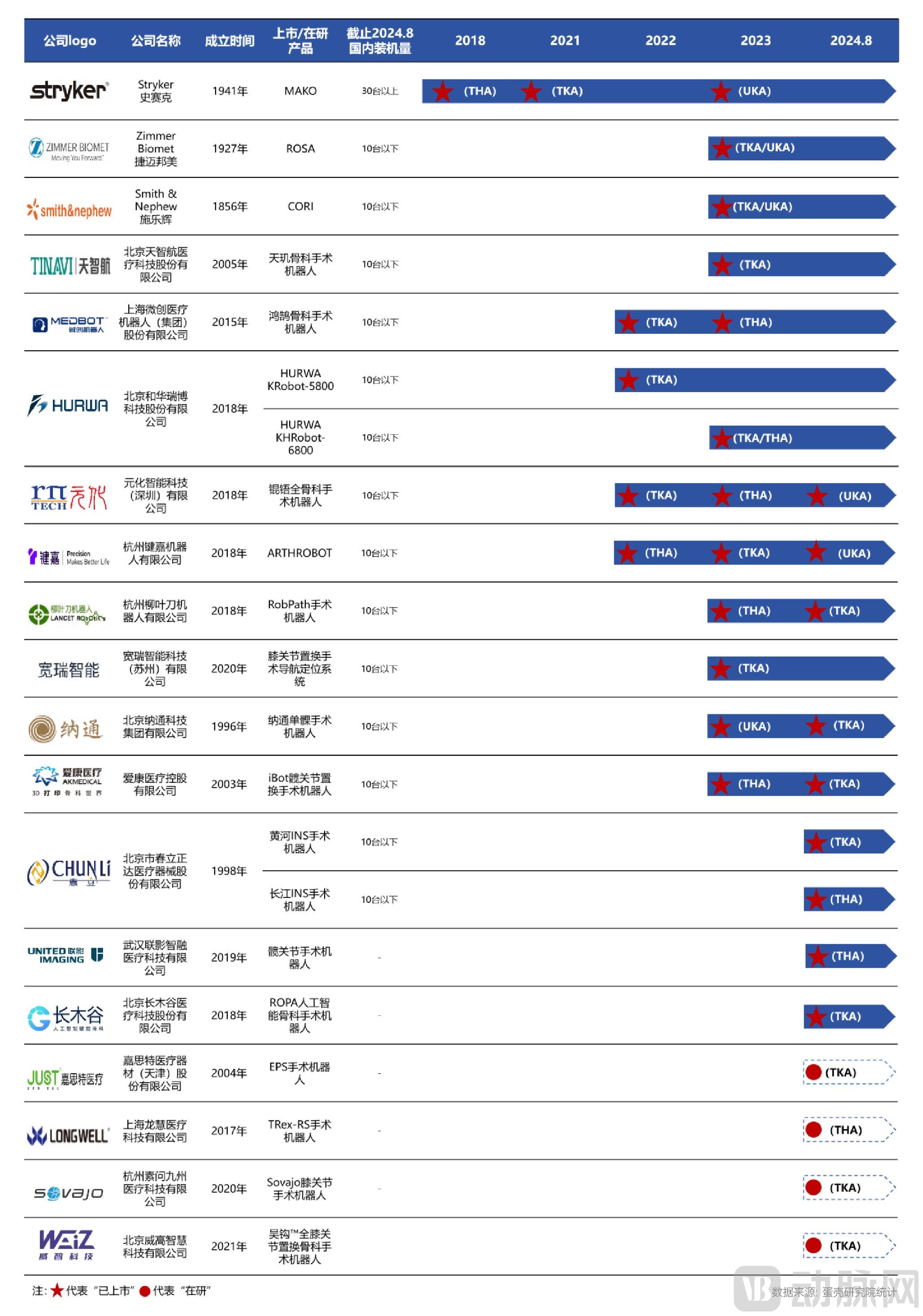

According to incomplete statistics, as of the publication of this article, 19 companies have entered the domestic market for joint surgery robots. Since 2022, related products from Chinese enterprises have entered an accelerated approval phase, with 15 companies having received marketing authorization from the NMPA, while the remaining four are accelerating their product development. In 2023, the number of new installations of domestic brands basically reached parity with overseas brands, indicating rapid progress in commercialization.

However, in 2023, new installations in the market were still dominated by Stryker's MAKO system, accounting for over 50% of the share.5. Due to the higher prices of overseas products, they still account for more than 60% of the market share. However, the market is changing. MAKO has encountered certain obstacles in promotion due to its excessively high pricing (hospital procurement price exceeding RMB 20 million) and its closed-system design (Stryker implants account for less than 10% of the domestic market).

In contrast, most domestic brands adopt open systems, offering greater flexibility for physicians and patients. With more affordable pricing that aligns with the trend of tightening hospital budgets, they are increasingly favored.By 2028, the cumulative installed base of domestically produced products is projected to be roughly on par with that of imported products.

Figure: Competitive Landscape of Major Players and Their Products in the Chinese Market

- 07 -

Each model has its own unique characteristics,

Overseas Industry Leaders Expand Through M&A, While Domestic Companies Focus on Intelligent Innovation

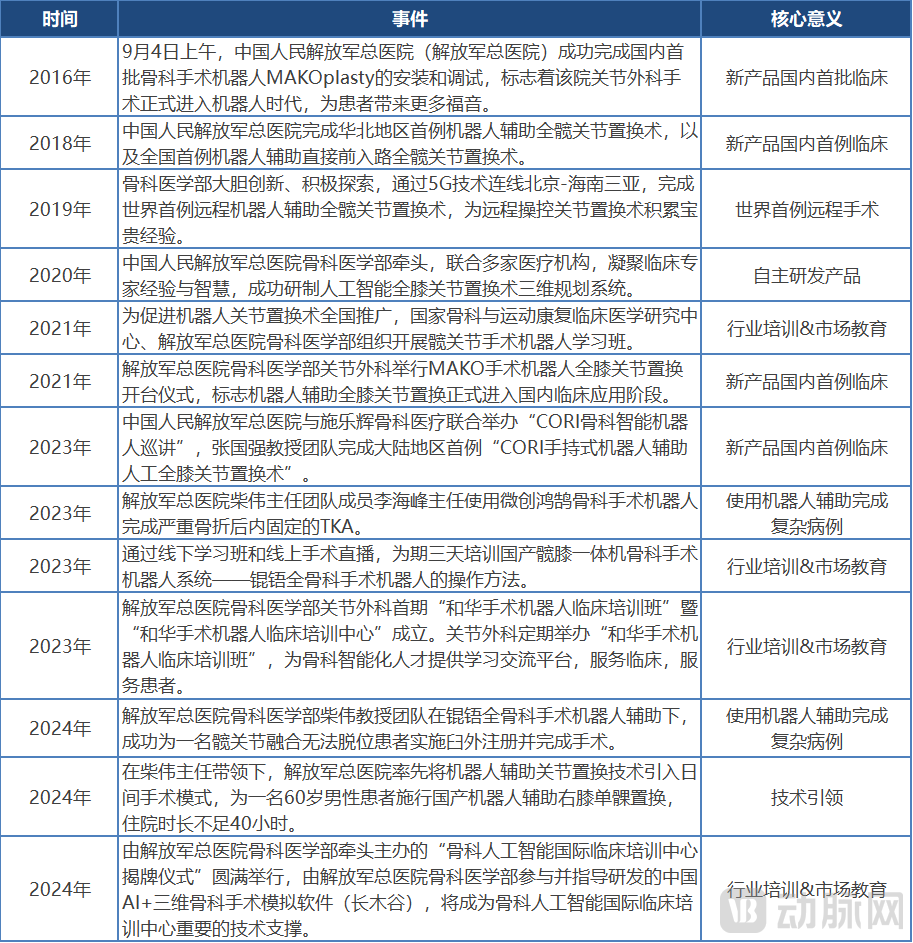

At the corporate development level, overseas companies in the field of orthopedic surgical robots have acquired core technologies through investments and mergers and acquisitions, thereby continuously consolidating and expanding their market advantages. In contrast, the development of domestic enterprises relies heavily on collaborative synergy among healthcare institutions, research entities, government bodies, enterprises, and capital. On the hospital front, the Department of Orthopedics of the Chinese PLA General Hospital and the National Clinical Research Center for Orthopedics and Sports Rehabilitation serve as core representatives and key forces, continuously deepening their efforts in clinical research, application promotion, independent R&D, industry training, and market education for joint surgery robots.

At the product innovation level, overseas joint surgery robots started earlier in robotic arm hardware technology and optical navigation systems, occupying a significant leading and monopolistic position in the industrialization process. Domestic joint surgery robots, however, demonstrate unique advantages in preoperative planning, offering not only higher efficiency and intelligence but also rapid product iteration based on feedback from Chinese clinicians. With the support of AI models such as DeepSeek, Chinese-made joint surgery robots are expected to further enhance their intelligence, decision-making capabilities, and interactive functions, while reducing costs and maintenance complexity. This ability to respond quickly to market demands makes domestic products more competitive in terms of product updates and adaptation to the local market.

Figure: Contributions of the Chinese PLA General Hospital in the field of orthopedic joint surgical robots. Data source: Public information, compiled by VCBeat.

- 08 -

Four Major Product Innovation Trends,

Unveiling the Core Development Directions of Future Joint Surgery Robots

Core technologies cannot be acquired through “purchasing” or “begging”; only innovation can achieve self-reliance and strength. Achieving breakthroughs through the use, R&D, iteration, and innovation of surgical robots is not only a requirement of the times but also a shared goal among clinicians, engineers, and enterprises. Currently, domestic surgical robot products and technologies are exhibiting multi-dimensional innovation trends.

Intelligence and Human-Computer Interaction:AI empowerment will bring new breakthroughs to orthopedic surgical robots. Future research will focus on multi-sensory information fusion, AI-assisted decision-making, adaptive learning, modular and customizable design, and precise control and feedback mechanisms. These advancements aim to achieve more comprehensive and efficient human-robot interaction, enhance the convenience and safety of surgical procedures, and make robots capable assistants for orthopedic surgeons.

Miniaturization and Portability:In the future, equipment miniaturization will be achieved by developing compact, modular robotic arms and integrating cart functionalities. Meanwhile, the setup and teardown processes will be simplified, and the number of supporting personnel required will be reduced, thereby enhancing operational convenience. These advancements will also facilitate the development of high-end smart operating rooms and optimize the surgical environment.

Integration and Multifunctionality:Orthopedic products are advancing toward integration and multifunctionality. For instance, the emergence of “single-platform, multi-procedure” systems has effectively bridged subspecialties such as joint replacement, spinal surgery, and trauma orthopedics, thereby enhancing equipment utilization efficiency and expanding the scope of clinical applications.

Customized Prosthetics:The core development directions are mainly reflected in two aspects. First, leveraging 3D printing technology to customize the design of prostheses used in surgical robots; second, continuously advancing the iterative updates of prosthesis materials to enhance their performance and service life.

Figure: NABRAI Intelligent Operating Room System, Data Source: Public Information

- 09 -

Focusing on Two Major Development Paths,

Fee Structures Are Becoming Increasingly Clear, with a Rising Share of Service-Based Fees

From the perspective of corporate development models, orthopedic joint surgical robot companies can be categorized intoResource-driven and Technology-driven。

Resource-driven enterprises leverage their deep expertise in the field of orthopedic consumables to promote the synergistic development of “consumables + surgical robots.” These companies not only develop a diverse range of joint prostheses but also advance 3D printing and personalized customization technologies, enhancing their competitiveness by building closed-loop systems. Meanwhile, they capitalize on robust supply chains and collaborate with technological forces from other sectors to accelerate product iteration and innovation. Naton Medical is a typical representative of resource-driven enterprises; its extensive accumulation in the field of orthopedic implants and prostheses has enabled it to construct an integrated solution covering artificial joints, surgical robots, and related services.

Technology-driven enterprises focus on breakthroughs in core technologies. Chinese companies, represented by Yuanhua, are continuously innovating in areas such as precision navigation, specialized surgical robotic arms, intraoperative data analysis, and AI-assisted decision-making to promote the intelligent and precise development of surgical robots. Meanwhile, they typically continue to adopt open systems to provide more options for hospitals and patients, thereby differentiating themselves from overseas products like MAKO and accelerating market expansion.

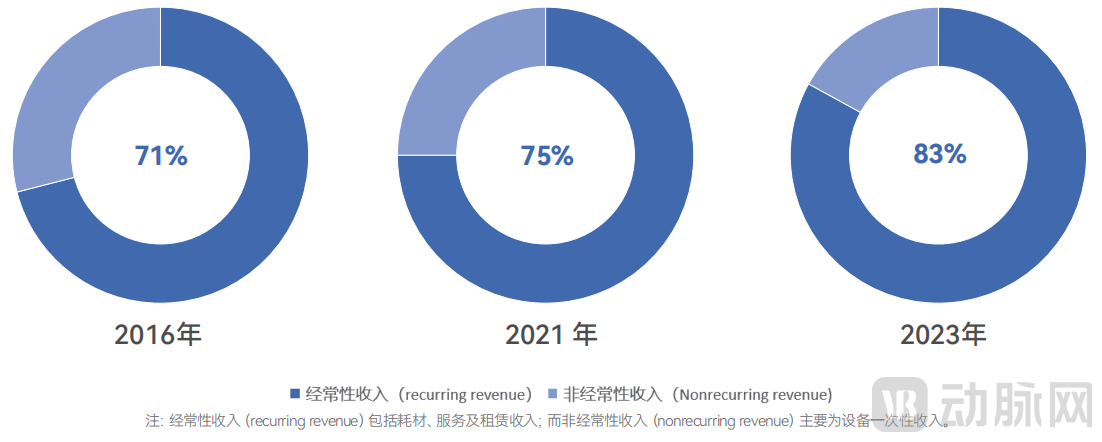

In terms of business model, joint surgery robots can draw on the overseas development paths of the da Vinci and MAKO systems. Currently, the core revenue for domestic manufacturers stems from equipment sales. As the market matures and robot penetration rates increase, the “equipment + consumables + maintenance services” model is expected to become the primary revenue stream for enterprises. Furthermore, with continued market development, the proportion of service-related fees in total corporate revenue is projected to rise further.

Figure: Proportion of Recurring Revenue for Intuitive Surgical, Source: Intuitive Surgical 2023 Annual Report

- 10 -

Insufficient momentum for original innovation, and the review and approval mechanism needs improvement,

Billing Remains the Core Bottleneck

In the process of accelerated industrial catch-up, we have observed a significant trend of "homogenization" in domestic joint surgery robot technologies and products. This issue is closely related to factors such as insufficient motivation for underlying technological innovation among enterprises, imperfect market review and approval policies, and a lack of diversified commercialization pathways.

R&D of Underlying Technologies:Current corporate awareness of intellectual property protection is weak, and investment in basic research is insufficient. Meanwhile, the lack of a relevant surgical evaluation system prevents accurate feedback on patients' quality of life, thereby limiting the promotion and application of surgical robots.

Review and Approval:China has not yet strictly differentiated between “superiority” and “non-inferiority” clinical trials. Joint surgery robotic products that undergo superiority testing are not distinguished from those subjected to “equivalence” or “non-inferiority” testing in terms of approval speed and registration certificate types. This has led to severe homogenization of domestic products, triggered inefficient competition in market promotion, and dampened enterprises’ enthusiasm for innovation.

Market Promotion:Across China, there is no unified pricing model for joint surgery robots, leading to significant controversy over their cost-effectiveness; “reimbursement” remains the greatest challenge at present. Currently, only a few regions such as Beijing, Jiangxi, and Hunan have established clear fee schedules, making it difficult for hospitals to evaluate the return on investment for equipment procurement and resulting in low willingness to pay. Furthermore, overseas companies have secured first-mover advantages in the Chinese market, posing substantial challenges for domestic enterprises in market expansion.

References:

1. Global Health Data Exchange (GHDx) Research Data

2. 2021 Statistical Data from the National Health Commission

3. VCBeat estimates based on expert interviews

4. VCBeat Research Institute's estimates based on research

5. Estimates by VCBeat based on expert interviews

The above is a curated selection from the report. The overall framework of the report is as follows, with a QR code for download attached below:

1. Overview of Robotic Systems for Orthopedic Joint Surgery

1.1 Orthopedic Surgical Robots

1.1.1 Core Components: Control System, Positioning and Navigation System, and Robotic Arm

1.1.2 Major Types: Spine, Trauma Orthopedics, and Joint Surgical Robots

1.2 Orthopedic Joint Surgery Robots

1.2.1 Working Principle

1.2.2 Three Major Surgical Procedures

1.2.3 Different Classifications

1.3 Development History

1.4 Industry Environment

1.4.1 National Policy

1.4.2 Health Economics

1.4.3 Social Trends

1.4.4 Technological Factors

2. Competitive Landscape and Commercial Prospects of Orthopedic Joint Surgical Robots

2.1 Market Drivers

2.1.1 Product Value: Feasibility of the product has been validated by extensive data in overseas markets

2.1.2 Patient Base: Urgently Addressing the Discrepancy Between Surging Surgical Volumes and Physician Shortages

2.1.3 Development Stage: Significant Room for Penetration Rate Growth

2.1.4 Innovative Research: Domestic research in related fields ranks among the highest globally

2.2 Current Status of Investment and Financing

2.2.1 Surgical Robots: Global Primary Market Hits Historic Funding Peak in 2021

2.2.2 Orthopedic Surgical Robots: Highly Favored by Capital, Representing the Sector with the Most Financing Events in the Surgical Robot Field

2.2.3 Orthopedic Joint Surgery Robots: Robust Financing Activity, with Most Companies Now in the Series B Commercialization Validation Stage

2.3 Market Size and Future Growth Potential

2.3.1 Short-Term Market Forecast: The Market Size of Joint Surgery Robots Will Exceed RMB 1 Billion in the Next Five Years

2.3.2 Ideal Market Size: The market is still in its early stages of development, with future potential expected to exceed RMB 10 billion

2.4 Competitive Landscape and Evolutionary Trends

2.4.1 Product Approval Progress: MAKO Takes the Lead, with Domestic Products Accelerating Approval in Recent Years

2.4.2 Domestic vs. International Comparison: Overseas Companies Currently Lead in Installed Base and Sales Revenue

2.4.3 Evolutionary Trends: Supported by National Policies, the Trend of Domestic Substitution Is Promising

3. Insights into Innovation Trends in Orthopedic Joint Surgical Robots

3.1 Core Technological Innovations

3.1.1 “Brain” Preoperative Planning

3.1.2 "Eye" Positioning and Navigation

3.1.3 “Arm” Robotic Arm

3.2 Innovation in Enterprise Development Models

3.2.1 Case Studies of Resource-Driven Enterprises

3.2.2 Case Studies of Technology-Driven Enterprises

3.3 Orthopedic Joint Surgical Robots

3.3.1 Distinctive Development of Domestic and International Robotics Companies and Their Products

3.3.2 Trends in Domestic Product and Technological Innovation

3.3.3 Development Trends in the Business Models of Domestic Enterprises

4. Future Challenges and Expectations for Orthopedic Joint Surgical Robots

4.1 Challenges in the Development of Domestic Joint Surgery Robots

4.1.1 Challenges in the Development of Underlying Technologies and Products

4.1.2 Challenges in Product Review and Approval

4.1.3 Challenges in Product Market Promotion

4.2 Recommendations for the Future Development of Joint Surgery Robots

4.2.1 Build an Integrated Innovation Ecosystem to Support the Accelerated Development of New Quality Productive Forces

4.2.2 Improve the review and approval process to encourage and protect original innovation

4.2.3 Strengthen Market Education and Accelerate Market Promotion

Chai Wei

Director, Department of Joint Surgery, Orthopedics Division, Chinese PLA General Hospital

Science and technology are the primary productive forces, as well as the core driving force behind healthcare transformation.

In recent years, with the rapid development of technologies such as artificial intelligence and mechanical manufacturing, the medical field is undergoing a profound intelligent transformation. Orthopedic surgical robots, which integrate algorithmic control systems, optical navigation systems, and force feedback technology, have become a key force driving orthopedic surgery toward greater precision, minimally invasive techniques, and intelligence, leading surgical procedures away from traditional “manual” operational models.

Compared with traditional orthopedic surgical procedures, the technological breakthroughs of joint surgery robots demonstrate threefold revolutionary value: From a clinical perspective, they enhance surgical precision and safety, provide patients with more precise and personalized treatment plans, improve postoperative recovery quality, and thereby elevate patients’ quality of life; from an educational perspective, they shorten physicians’ learning curves, accelerate the professional development of young surgeons, and consequently drive the overall improvement of technical standards within the industry; from an industrial perspective, their standardized surgical workflows offer robust technical support for the decentralization of medical resources under the tiered diagnosis and treatment system. Moreover, given that joint replacement surgeries are more standardized and proceduralized than other orthopedic procedures, to date,Joint surgery robots can be described as the most perfect application and embodiment of artificial intelligence in the field of orthopedics.

Joint surgery robots are not merely the product of a technological revolution, but also a significant milestone in the modernization of the healthcare system. For medical professionals, they serve as intelligent partners that enhance surgical safety and efficiency; for medical researchers, they act as a convergent platform for multidisciplinary innovation; for policymakers, they provide a powerful lever for the balanced allocation of medical resources; and for innovative capital, they represent a strategic entry point into the trillion-dollar health industry. At present, stakeholders across the medical, research, policy, enterprise, and investment sectors urgently need to join hands, advance collaboratively, deeply integrate all links of industry, academia, research, and application, break down barriers, achieve seamless connectivity, and jointly build a comprehensive health ecosystem. Only in this way can we steadily advance and effectively implement the grand strategic vision of "Healthy China" in the two key dimensions of frontier exploration in "precision medicine" and broad coverage of "inclusive healthcare," thereby laying a solid foundation for the health and well-being of the entire population.

Against this backdrop, the White Paper on the Development of the Orthopedic Joint Surgery Robot Industry has been published. We have compiled this book to comprehensively review and deeply analyze the development history, current status, and future trends in the field of orthopedic joint surgery robots, with the aim of providing highly valuable references for experts and scholars, policymakers, entrepreneurs, and investors both within and outside the industry.

As a clinical practitioner, I would like to share three insights with esteemed seniors, colleagues, and peers: First,The current stage of development in joint surgery robots is akin to the laparoscopic technology revolution at the end of the 20th century, where technological pioneers will have the opportunity to reshape the industry's discourse power system.Second, the precision and stability of domestically produced surgical robots are steadily improving, with a more pronounced trend toward domestic substitution. Third, over the next decade, joint surgery robots will evolve deeply in three directions: intelligence, accessibility, and integration.

However, the path toward intelligent orthopedics is by no means smooth. Critical challenges in core technologies remain to be overcome, requiring interdisciplinary integration, the convergence of diverse research forces, and increased investment in R&D and collaboration. Meanwhile, it is essential to establish and refine a closed-loop system of “clinical problems–technology development–application feedback” to ensure that technological advancements are closely aligned with clinical practice, thereby better serving medical care. Furthermore, the high cost of equipment has deterred many primary-care hospitals from adoption. In the future, costs could be reduced and technology dissemination promoted through process optimization, scaled-up production, and the sharing of R&D outcomes.

Despite numerous challenges, we firmly believe that, driven by strong national policy support and demand spurred by population aging, and through the concerted efforts of research institutions, innovative enterprises, and the investment community, the orthopedic joint surgery robotics industry is poised for broader development prospects.

This white paper embodies the collective wisdom of numerous experts in the field. We extend our gratitude for their selfless sharing of valuable experience, unique perspectives, and profound insights. Our sincere thanks go to all invited editorial board members, committee members, research teams, and the individuals and organizations that provided support during the compilation process.

We are standing at the tipping point of the intelligent orthopedics revolution.We anticipate that this white paper will serve as a catalyst for industry evolution, converging more innovative forces to jointly chart a new blueprint for safeguarding human bone and joint health. In the foreseeable future, as the empowerment by large AI models continues to accelerate, joint surgical robots will transcend the stage of mere task execution, advancing toward intelligent planning and decision-making, thereby achieving comprehensive intelligence in joint surgery.

We look forward to more clinical experts, engineers, investment institutions, and innovative enterprises joining hands to work together in promoting the development of orthopedic joint surgical robot technology, providing patients with higher-quality medical services, and creating greater value for society!

Zhang Hao

Director, Management Center of the National Clinical Research Center for Orthopedics and Sports Rehabilitation

In recent years, amidst the wave of transformation in medical technology, joint surgery robots have undoubtedly emerged as one of the most prominent beacons. From breakthroughs in materials science and in-depth research in biomechanics to the deep integration of artificial intelligence and robotics, digital and intelligent healthcare is reshaping the boundaries of surgical practice. This transformation represents not only a technological leap but also an innovation in medical philosophy—shifting from “experience-driven” to “data-driven” approaches, and from “individualized exploration” to “standardized practice.”

Industry Boom: The Dual Resonance of Technology and Market

Globally, the joint surgery robotics industry has established an ecosystem of collaborative innovation integrating industry, academia, research, and clinical practice. International giants such as Intuitive Surgical, Stryker, and Zimmer Biomet continue to lead the technological frontier, while domestic enterprises like Yuanhua Intelligence and Nato Medical have achieved breakthroughs in core algorithms, precision robotic arms, and navigation systems, gradually breaking the monopoly of imported products. The synergistic effects across the upstream and downstream segments of the industrial chain are becoming increasingly prominent: suppliers of high-precision sensors and intelligent control modules lay the hardware foundation; AI algorithm teams collaborate with clinical experts to optimize decision-making models; and medical institutions feed back into technological iteration through real-world data and clinical studies. Meanwhile, policy dividends are injecting strong momentum into the industry—the National Medical Products Administration’s “green channel” for innovative medical devices is accelerating product launches, pilot programs for insurance coverage of robot-assisted surgeries are gradually expanding, and capital market favor towards medtech companies is providing ample “fuel” for research and development.

Overcoming Challenges: Accumulation and Breakthroughs in the Technology Cycle

The maturation of any disruptive technology follows the cyclical pattern of “trigger—peak of inflated expectations—trough of disillusionment—slope of enlightenment—plateau of productivity,” and joint surgery robots are no exception. Meanwhile, the structural misalignment between technological cycles and economic cycles renders industry trends even more unpredictable. In the early stages of the industry, high costs, complex operational procedures, and limited clinical validation data deterred some medical institutions. At the technical level, issues such as the force control precision of robotic arms, real-time fusion of multimodal imaging, and the safety of human-robot collaboration once became bottlenecks. However, these practical challenges have precisely served as opportunities for technological deepening. In recent years, with low-latency transmission enabled by 5G networks and enhanced edge computing capabilities, the remote collaboration and real-time response capabilities of surgical robots have been significantly strengthened. The optimization of deep learning algorithms has upgraded preoperative planning from “experience-dependent and manual reasoning” to “data-driven and digitally intelligent empowerment.” Furthermore, the widespread adoption of modular design concepts has reduced equipment maintenance costs and lowered the learning threshold. Of greater note is that the industry has shifted from competing on single technologies to “ecosystem building.” Leading enterprises are actively participating in the construction of national intelligent orthopedic bases, such as National Clinical Medical Research Centers. By leveraging scaled, systematic, and efficient industry education, they are accelerating the widespread adoption of joint surgery robot technology, achieving the “externalization of corporate educational costs,” and striving to create a closed-loop market.

The Future Is Here: Dual Anchors of Trends and Confidence

Looking ahead, the development of robotic systems for joint surgery will exhibit three major trends: First, technological integration, where the convergence of AI, the Internet of Things (IoT), and digital twin technologies will enable a closed-loop workflow encompassing “preoperative simulation–intraoperative navigation–postoperative assessment.” Second, the decentralization of application scenarios; as the concept of robotic surgery gains wider acceptance, the cost of domestically produced equipment decreases, and surgical procedures become simplified, robot-assisted surgeries will gradually become prevalent in primary healthcare institutions, which will subsequently emerge as the mainstay of the market. Third, the homogenization of medical care, whereby standardized surgical protocols and remote collaboration allow high-quality medical resources to transcend geographical barriers, helping to address the critical public livelihood issues of difficult and costly access to medical care.

Currently, China is facing the severe challenge of an accelerating aging population and a surge in patients with joint diseases. Statistics show that the demand for knee replacement surgeries will exceed one million cases by 2030, a volume that traditional surgical models can no longer adequately meet. Joint surgery robots, with their advantages of “precision, safety, and reproducibility,” will become the key to breaking this deadlock. Short-term industry fluctuations do not alter the long-term positive fundamentals; intense market competition is accelerating cost optimization and efficiency improvements—this is not only an inevitable law of technological development but also a rigid demand for medical upgrading.

In the Wave of Digital and Intelligent Healthcare, There Are No Bystanders.Whether clinicians, engineers, policymakers, or investors, all must embrace change with a hands-on approach. The White Paper on the Development of the Orthopedic Joint Surgical Robotics Industry is not merely an industry landscape map; it is also a declaration of confidence. It documents the incremental yet far-reaching advances in technology, analyzes the ebbs and flows of the industry, and heralds a healthcare future that is both more efficient and more humane.

Scan the QR code below to contact the assistant and obtain the full report.

(If already added, please proactively contact the assistant)