The Great Hearing Race: A 12,000-Word Deep Dive into the Current Landscape and Opportunities in China's Hearing Aid Industry

Author: Li Yang, Investment Director at Yuan Yi Capital, Founder of the Stanford Future Healthcare Club.

Yuan Yi Capital was established in 2016 as an early-stage venture capital fund focused on the digital technology sector. The firm currently manages multiple RMB and USD funds, with total assets under management nearing RMB 5 billion.

Special thanks to the following experts for their invaluable guidance in completing this study:

Wan Min, President of the Beijing Hearing Association

Yu Shihu, Founder of Xinsheng Hearing

Mao Huahui, Founder of Ting Gongchang

Xie Bing, Co-founder of Lisheng Hearing Aids

Compared to the decades of experience accumulated by experts in this field, my own learning journey has been relatively brief. Inevitably, there may be inaccuracies; I welcome your critiques and corrections to help me improve.

The global leader in the hearing industry, Switzerland’s Sonova Group, stated in its annual report: “Technologically advanced manufacturing processes are carried out in Switzerland, while the assembly of standard products is completed in Asia.” This statement carries two layers of profound implication.

At the first level, Sonova invests heavily in product R&D and is confident that its technological advancements far surpass those in China. Consequently, it retains advanced technologies and processes exclusively in Switzerland to prevent rapid imitation and overtaking by Chinese competitors. The deeper implication of this strategy is that the Asian market is forced to undertake over 90% of production and assembly work, yet captures only slim manufacturing profits, thereby ensuring Sonova’s sustained high profit margins. This also means that for Chinese hearing aid manufacturers to achieve a breakthrough, it will not be as casually portrayed in most hearing aid project roadshows—where importers are dismissed as vulnerable, or where minor improvements coupled with the “Made in China” label are claimed to enable rapid catch-up amidst competitors’ systematic offensive and defensive layouts. Only by facing facts squarely and acknowledging objective gaps can progress and breakthroughs occur; otherwise, domestic hearing aids will continue to struggle at the bottom of the industry chain.

Hearing care, a sector long monopolized by imports, has witnessed rapid growth in recent years. A cohort of domestic hearing aid manufacturers is striving to break the dominance of the five major overseas giants—Sonova, WS Audiology, GN, Demant, and Starkey—who collectively control over 95% of the global market. What is the current landscape? What are the key challenges? Where do the opportunities lie? We attempt to provide systematic answers to these questions.

On one hand, the core components of hearing aids have long been dominated by imported manufacturers; on the other hand, the primary sales channel for hearing aids—offline hearing centers—has also been cultivated and controlled by these foreign companies for many years. For China’s hearing aid industry, this means not only overcoming “chokepoint” technological challenges but also restructuring distribution barriers that have taken decades to form. In the OTC hearing aid sector, Apple’s AirPods Pro 2 has made a strong entry, offering performance that even surpasses most higher-priced OTC hearing aids, with a price tag of just RMB 1,899. Whether in the offline market for severe hearing loss or the online OTC segment, it is by no means easy for domestic hearing aid entrepreneurs to achieve overtaking on a bend.

As of April 2024, the number of valid hearing aid medical device registration certificates approved in China had reached 262, with the latest figure standing at 279. As of October 31, 2024, the total number of offline hearing aid stores across China had reached 19,397.

We leverage multiple AI agents to programmatically aggregate and analyze relevant industry data, from“Who is manufacturing hearing aids,” “Who is selling offline hearing aids,” and “Who is selling online hearing aids”From three perspectives, this report provides a detailed analysis of the manufacturers behind nationally approved hearing aids, the professional backgrounds of their leaders, the operational status of 19,397 offline hearing aid stores across China, the component composition of in-the-ear (ITE) and behind-the-ear (BTE) models from leading brands, and the current development landscape of online and over-the-counter (OTC) hearing aids. The aim is to systematically address these issues and outline the developmental trajectory of China’s hearing aid industry.

As of April 2024, there were a total of 262 valid hearing aid medical device registration certificates approved in China. Who exactly is manufacturing hearing aids?

I. First, let us examine the distribution of registration types for the 262 hearing aids.

Specifically, there are 112 medical device registration certificates for behind-the-ear hearing aids, 113 for in-the-ear hearing aids, 13 for bone-conduction hearing aids, 20 for body-worn (box-type) hearing aids, and 6 for neck-worn hearing aids, with the specific type unspecified on 4 additional certificates.

It should be noted that all hearing aids are classified as Class II medical devices. The naming conventions and regulatory approaches vary across provincial medical products administrations. For instance, in Hunan Province, a single registration certificate may cover all types of hearing aids; in Jiangsu Province, one certificate may encompass all models; whereas in Shanghai, different models require separate registrations. Additionally, some neck-worn devices are registered under the category of in-the-ear (ITE) hearing aids. For statistical purposes, custom-made hearing aids are uniformly consolidated into the ITE category. Consequently, the total number of medical device registration certificates for the aforementioned categories of hearing aids exceeds the actual count of 262.

In addition,The absolute number of certificates does not directly correspond to a company’s product volume, R&D efficiency, or product performance.Taking the five major importers as examples, Sonova AG of Switzerland holds four medical device licenses, with three registered in Suzhou and one in Shanghai; Demant A/S of Denmark has 22 medical device licenses, all registered in Shanghai; WS Audiology Group, based in Denmark and Singapore, has six medical device licenses registered in Suzhou; GN Group of Denmark has eight medical device licenses registered in Xiamen; and Starkey Laboratories Inc. of the United States has three medical device licenses registered in Suzhou.

II. Next, let us examine the top ten manufacturing addresses associated with these 262 certificates to gain an intuitive understanding of the primary regions involved in hearing aid production.

Although Shenzhen does not host major manufacturing facilities for imported hearing aids, it ranks first by virtue of its exceptionally high density in consumer electronics manufacturing. Xiamen, Shanghai, and Suzhou, which rank second, third, and fourth respectively, are all home to production centers for major imported hearing aid manufacturers. Among them, Xiamen was the earliest production hub for major imported hearing aid brands. Its status as a hearing aid manufacturing center was established starting with GN Group’s Xiamen Ludan Hearing Aid Manufacturing Factory, and later reinforced when Mr. Yu Shihu, founder of New Sound (Xiamen), introduced GN Group’s ReSound China Manufacturing Center while serving as the head of GN Group’s global manufacturing operations.

From this, it can be concluded thatApart from Shenzhen’s unique circumstances, the number of hearing aid manufacturers in other regions has previously depended directly on where major importers established their manufacturing centers.

3. Let’s examine the backgrounds of the leaders of the 94 hearing aid companies outside the Big Five hearing groups

There are 12 companies whose leaders serve as the chairman or president of a listed company.

There are three companies whose founder or second-largest shareholder is a member of the U.S. National Academy of Engineering.

There are two companies whose CEOs are former executives of major hearing aid manufacturers.

Zhangmen operates more than 200 offline chain fitting centers across over four regions.

There are five companies whose CEOs are university professors.

There are 11 companies founded by returnee entrepreneurs.

Detailed Backgrounds of the Heads of 48 Companies

Raphael Michel, founder of the U.S. DTC hearing aid brand Eargo and a 2003 graduate of Stanford University’s Department of Mechanical Engineering, once remarked when he first ventured into the hearing aid market, “When you discuss a new type of hearing aid with investors, it sounds like a tale littered with countless failures along the way. The history of hearing aids is one marked by numerous attempts and repeated failures.” Competition in the hearing aid industry is even more brutal than this statement suggests.

As engineers trained in electronic engineering, after answering the question “Who is making hearing aids?”, we start from first principles to gain a deep understanding of the essence and core value of hearing aids by intuitively analyzing their internal structure. We then explore what is actually being sold when hearing aids are marketed, and who the sellers are.

We purchased behind-the-ear (BTE) and in-the-ear (ITE) hearing aids from leading brands for teardown and reassembly. It was observed that the core electronic components of a hearing aid consist exclusively of: 1. receiver, 2. chip, and 3. speaker. Both the receiver and speaker are sourced externally, with Knowles Electronics, a U.S.-based company, being the leading supplier of receivers and speakers for hearing aids.

Diagram of the Structure of a Behind-the-Ear Hearing Aid

Diagram of In-the-Ear (ITE) Hearing Aid Structure

After consulting specifically with the former CEO of Knowles Electronics (U.S.), I confirmedReceivers and speakers account for a major portion of the production costs for leading hearing aid manufacturers.As imported hearing aid manufacturers primarily rely on self-developed and self-produced chips, thereforeThe performance differences among various imported hearing aids are primarily limited to the chips and the signal processing algorithms embedded within them.

Due toDomestic hearing aid manufacturers currently still primarily procure or custom-develop chips through suppliers such as ON Semiconductor, Nanjing Tianyue, and Shenzhen Muxin., domestically produced hearing aids basically lack self-developed core components at the hardware level; performance differences primarily stem from the tuning of signal processing algorithms on chips. Of course, factors such as casing, ear molds, wearing styles, and the application of artificial intelligence algorithms are also important for hearing aid effectiveness, but they do not constitute absolute performance disparities among different manufacturers' products.

Given the low ratio of hearing aid production costs to sales prices, it is preliminarily inferred thatOne of the core factors determining a product’s selling price is not the cost of the hardware itself, but rather the combined performance of the chip and its onboard signal processing algorithms.

Through studying *Hearing Aid Dispensers: Fundamentals* and *Hearing Aid Dispensers: Professional Skills* (the national Level 3 Hearing Aid Dispenser training materials), it is understood that hearing impairment may result from the combined effects of damage to the auditory nervous system and conductive hearing loss. Age-related hearing loss aligns with the basic characteristics of chronic age-related diseases and degenerative conditions. Furthermore, studies in *Adult Auditory Rehabilitation* indicate that hearing loss can also lead to declines in language and cognitive functions. For neurological disorders or brain science-related diseases, the underlying disease mechanisms are often unclear; consequently, there are no directly corresponding biomarkers or identified root causes at the clinical level, making direct and effective treatment difficult. Therefore, hearing aids are not pharmaceutical agents for treating hearing loss. Moreover, due to the complexity of hearing loss, the primary role of hearing aids is to help patients compensate for their hearing deficits. Thus, selling hearing aids is not merely about providing a hardware product; it requires meticulous effort in the fitting process, along with systematic training to help patients restore their hearing and language functions.The second core factor determining the selling price of a product is professional fitting services and systematic rehabilitation training services.

Consultations with leading industry business experts have revealed that for the same hardware products under a single brand, pricing may vary across regions with different economic development levels, and the product portfolios supplied to these regions may be differentiated.The third core factor determining the selling price of a product is the economic level of the region where hearing-impaired patients reside.

Consultations with senior executives of imported brands in China revealed that payment collection volumes vary significantly among distributors of different scales, leading to corresponding differences in the purchase price discounts they receive.The Fourth Core Factor in Determining Product Selling Price: Sales Volume and Corresponding Purchase Discounts.

Having understood the determinants of hearing aid sales prices, we proceed to answer the following questions: How many hearing aid stores are there in China?Which brand’s hearing aids are sold? Who is the primary owner of the store? What are the professional competencies and sales capabilities of the staff?

We reframed and defined this problem as conducting a comprehensive count of every physically existing hearing aid store on each street across every province, city, district, and county in China. Each store was assigned a unique key, and the data were aggregated to compile a nationwide dataset of hearing aid stores. To achieve this, we leveraged: 1. the latest administrative division codes (adCode) for all districts and counties in China; 2. the Basic Search API from the Amap (Gaode Map) Developer Platform; 3. Llama3.1 Ultra combined with Retrieval-Augmented Generation (RAG) to synthesize industry-specific knowledge about hearing aids; and 4. Python for batch data processing. We systematically enumerated hearing aid stores across all 2,847 districts and counties in China, successfully obtaining contact telephone numbers for 14,600 of these stores. The final output is a comprehensive nationwide dataset of hearing aid stores.

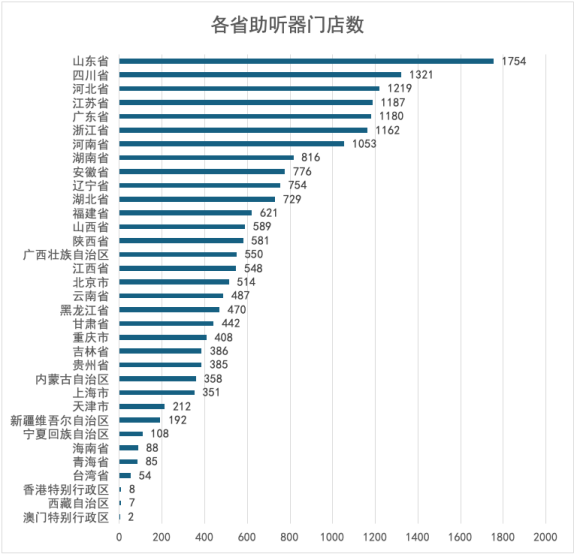

As of October 31, 2024, there were a total of 19,397 hearing aid stores in China.

Which brands’ hearing aids are sold by these 19,397 hearing aid stores?In terms of the number of named storesAmong them, Phonak’s brand influence remains ranked first, Signia has inherited the brand equity of the acquired Siemens Hearing, and both Resound and Oticon have more than 1,000 branded retail stores.

Number of Stores with Imported Brand Naming Rights

According to the founder of a leading hearing aid company, there are four types of sales channels for hearing aids:

(1) The primary channel currently is offline hearing aid stores, accounting for approximately 70%;

(2) The hospital channel accounts for approximately 10%;

(3) Procurement by Disabled Persons' Federations accounts for approximately 10%;

(4) Online sales account for approximately 10%.

Among them,China Disabled Persons' Federation (CDPF)Imported brands account for as high as 95% of procurement,HospitalChannels are primarily dominated by imported brands,Online SalesDomestic OTC brands predominate.Offline Hearing Aid StoresAs the primary sales channel for hearing aids, imported brands account for over 90% of the market share. If semi-finished products supplied by imported brands to leading distributors for assembly or private labeling are included, the market share of imported brands would be even higher than 90%.

Distributor PartnershipIt is a complex, dynamic process that continuously evolves in response to various factors, including pricing policies, the relationship between brand owners and major distributors, changes in professional management personnel at brand companies, the dynamics between major distributors and their internal partners (smaller distributors), and regional user preferences for product adaptation. In this context, the number of stores bearing a brand’s name can serve as an indicator for static analysis of brand influence.

Who is the owner of the hearing aid store?

Using Qichacha, we screened business registrations from 1996 to the present with keywords “hearing aids” and “hearing,” applying the following criteria: 1) presence of an official website, 2) a valid phone number, 3) an official WeChat public account, and 4) status as an independent hearing aid distributor rather than a branch office. This yielded 153 companies, after which we excluded: 1) duplicate registrations arising during mergers and acquisitions-driven expansion, and 2) companies that had already been acquired.

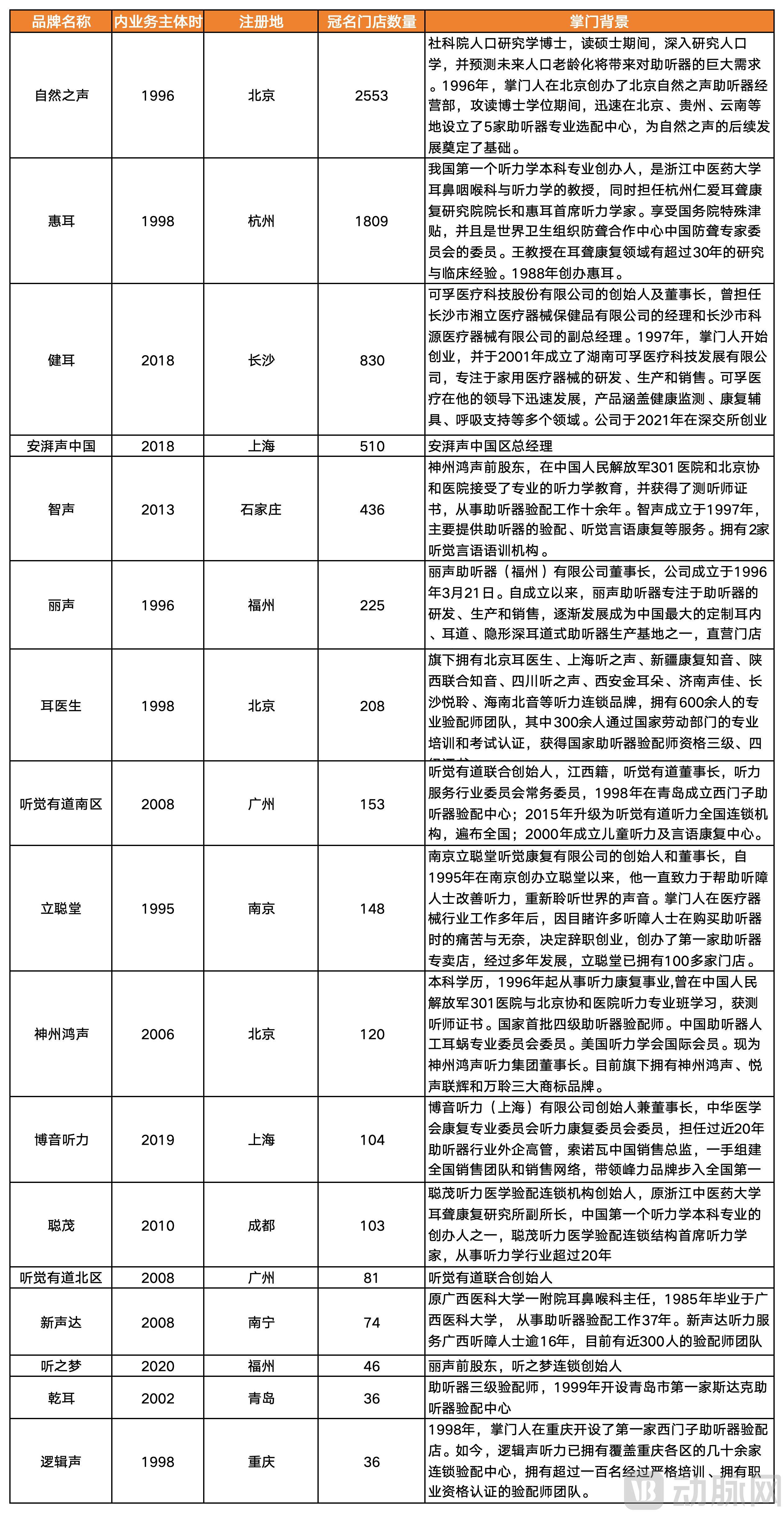

A final selection of 53 distributors was made, among which 17 with more than 30 branded stores were identified as independent and active hearing aid distributors. They are ranked below by the number of branded stores:

(Note: 1. The number of branded stores refers to street-level storefronts featuring the brand name in their signage, reflecting the dynamic equilibrium of brand influence over a period. This figure does not directly equal the sum of company-owned stores and partner stores, as the count of branded stores may be lower due to factors such as newly renovated stores awaiting branding, ongoing M&A transactions, and the continued use of legacy signage from brands like Siemens. 2. Independent distributors’ acquired brands are not listed separately. 3. Discrepancies between registered business entity names and store brand names may result in omissions in brand statistics; please contact me to correct any missing brands. 4. Some brands associated with the above-mentioned distributors are currently undergoing M&A processes.)

By observing the store distribution of major distributors and the evolution of their M&A entities, several interesting phenomena within the industry have been identified:

1. The number of hearing aid stores is positively correlated with regional economic activity and population density;

2. Distributors are typically distributed by city or province. Whether acquiring an imported brand or consolidating among distributors, it is common practice to register a new legal entity in the province of the target brand to facilitate the acquisition;

3. If the M&A is not conducted by a single controlling shareholder, consolidation and division will alternate; mergers, integrations, and post-merger spin-offs have been occurring continuously.

4. Becoming a major distributor requires strong character, balancing external relationships with large manufacturers while managing internal interests. Allocating too little profit leads to the independence of internal partners; allocating too much effectively results in decentralization, rendering the chain operation nominal in name only.

5. The leader of the brand with the greatest influence is a population sociologist, representing the ultimate mastery of strategic momentum and philosophical principles. The leader of the second-most influential brand is a professor who established the nation’s first undergraduate program in audiology, embodying the pinnacle of theoretical expertise and practical technique. The leader of the third-most influential brand is the chairman of a publicly listed company, exemplifying the utmost advantage in resource allocation. The first two leaders have cultivated their presence in the industry for over 25 years, while the latter has been rapidly catching up within just a few short years.

Finally, what are the professional competency and sales proficiency of the dispensing specialists?

After conducting field research on flagship stores and community outlets of leading brands in Beijing’s core business districts, I found that the flagship stores feature highly professional equipment and interior design. Each flagship store is staffed with one store manager (a Level-4 Hearing Aid Dispenser) and two Level-4 Hearing Aid Dispensers, both possessing over six years of dispensing service experience. In contrast, community outlets are equipped with two Level-4 Hearing Aid Dispensers who have transitioned from sales roles in other industries and have only 1–2 years of experience in the field. The compensation level for Level-4 Hearing Aid Dispensers is comparable to that of nurses in first-tier cities. These professionals believe that promotion to Level-3 Hearing Aid Dispenser does not bring a significant salary increase from the company, resulting in limited interest in pursuing certification upgrades.

In China, only a few institutions offer undergraduate programs in audiology. The vast majority of practitioners hold associate degrees and have not undergone systematic clinical training. Compared with their foreign counterparts, they lack a deep understanding of the underlying mechanisms of hearing aid fitting, the neuroscientific basis of hearing loss, signal processing, acoustics, speech rehabilitation, as well as the fundamental structure and function of hearing aids. While their professional appearance, demeanor, and strong sales capabilities are advantageous for expanding store performance and controlling operational costs, it remains questionable whether they provide the optimal experience for patients in terms of fitting, device usage, and rehabilitation outcomes. Under the imperative of sustainable business operations predicated on customer acquisition and conversion, how to further enhance the level of professional services, and at what cost to improve such services and supplement them with rehabilitation training, remains an unresolved issue.

In 2022, the U.S. FDA’s announcement of a new over-the-counter (OTC) hearing aid category sent ripples through the hearing aid market. This chapter provides a detailed analysis of the current development status of online and OTC hearing aids, referencing the U.S. hearing aid classification system.

This study attempts to answer the following five key questions:

1. What are the sales revenue and unit sales volume of online hearing aids?

2. Which platforms, brands, and stores sell hearing aids online?

3. Which manufacturers are the primary producers of online hearing aids?

4. Who are the leaders of online hearing aid brands?

5. How effective are Apple’s over-the-counter hearing aid products delivered via Bluetooth earbuds, and what impact might they have on existing brands?

Research Methods: We aggregated all hearing aid brand stores on mainstream e-commerce platforms, including JD.com, Tmall, Douyin, and Pinduoduo. A comprehensive summary and analysis were conducted on all hearing aid products currently available for sale and their corresponding manufacturers. Using an AI agent tool for e-commerce, we compiled sales revenue and volume data for all brands on the three major e-commerce platforms—JD.com, Tmall, and Douyin—over the past 12 months (from December 2023 to November 2024). Data from Pinduoduo were excluded from the statistics because its group-buying figures do not directly reflect actual sales.

I. What are the sales revenue and sales volume of online hearing aids/OTC hearing aids?

We employed two methods to estimate the sales revenue and unit sales volume of online hearing aids/OTC hearing aids.

Method (1): A summary of sales data from the three major online hearing aid sales platforms—JD.com, Tmall, and Douyin—over the past year (December 2023 to November 2024) reveals thatA total of 1,898,622 hearing aids were sold, with sales revenue reaching RMB 1.58418 billion and an average price of RMB 834. Compared with the same period last year, sales volume increased by 5.89%, sales revenue grew by 33.23%, and the average price rose by 25.83%.

Method (2): Given that e-commerce sales data may contain a certain degree of inflation, sales figures and financial reports from e-commerce platforms are not necessarily reliable. True sales performance should be calculated based on inventory changes and actual consumption of hearing aid chips. Here, we only conducted calculations based on e-commerce data, covering 111 brand stores across the three major online hearing aid sales platforms. We calculated the sales revenue and volume for each store individually and aggregated the results. The findings show that,In the past year (December 2023 to November 2024), these 111 online hearing aid brand stores sold a total of 1,573,661 hearing aids, with sales revenue reaching RMB 1.29576 billion.

Through consultations with leaders of top hearing aid manufacturers, we learned that the return rate for online hearing aids ranges from 30% to 60%. Using an average return rate of 45% for calculation, the actual sales volume of online hearing aids over the past year was approximately 865,513 units, with sales revenue reaching around RMB 712.67 million. This figure aligns with the industry estimates of RMB 600–800 million provided by leading companies, making it reasonable to base projections on the lower end of this range, i.e., RMB 600 million.Accounting for approximately 10% of the hearing aid market.

As can be seen, regardless of the methodology employed, both the sales volume and revenue of online hearing aids demonstrate a certain market size and growth potential.

II. Which platforms, brands, and stores sell hearing aids online?

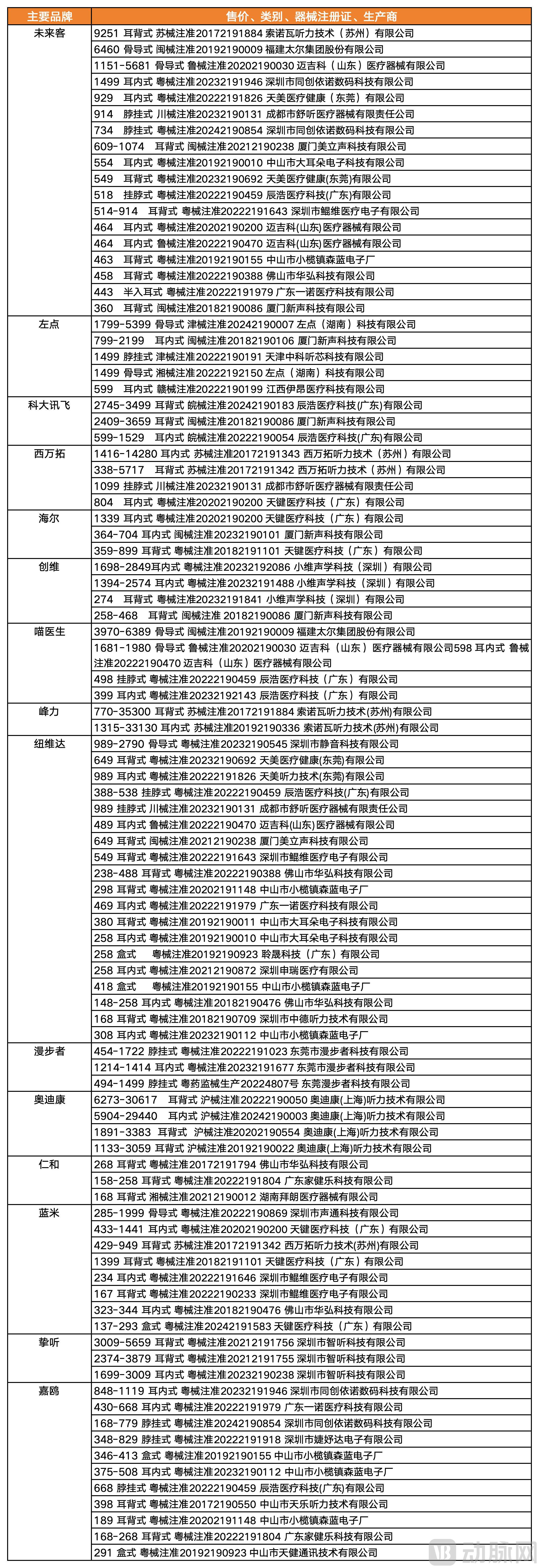

The platforms, brands, and stores for online hearing aid sales mainly include JD.com, Tmall, Douyin, and Pinduoduo. On these platforms, a total of 111 hearing aid store brands are engaged in sales. Among them, 15 store brands achieved sales exceeding RMB 10 million within the past 12 months (calculated based on a more conservative 50% return rate). These brands are ranked in descending order by sales volume as follows:

However, the aggregated e-commerce sales figures do not reflect actual net sales. The ranking based on actual sales differs slightly from the aforementioned order; for instance, the aggregated e-commerce sales of Weilaike and ZuoDian are very close. Currently, two e-commerce hearing aid brands still achieve over RMB 100 million in sales after accounting for returns.

3. Which manufacturers are primarily responsible for producing online hearing aid brands with sales exceeding RMB 10 million?

Among online hearing aid brands with annual sales exceeding RMB 10 million, only seven own their production lines, while the remaining eight adopt an original equipment manufacturer (OEM) model. Regardless of whether they rely on OEM or in-house manufacturing, these brands depend on external procurement for core hardware components such as receivers, speakers, and chips, and have not yet achieved independent research and development of core hardware.

Major Western manufacturers such as Signia, Phonak, and Oticon have long prioritized online hearing aid channels. They have specifically introduced products in the RMB 1,000 range and below RMB 500 to capture the online hearing aid market, achieving tens of millions in sales revenue. This clearly contradicts the claim by many Chinese hearing aid entrepreneurs that these companies neglect their online hearing aid business.

In terms of cost, importers possess proprietary chips that outperform those from ON Semiconductor, thereby largely eliminating the need to procure high-end hearing aid chips from ON Semiconductor at premium prices. (Consultations with ON Semiconductor experts revealed that their R&D investment is significantly lower than that of importers, and their performance still lags behind the proprietary chips developed by importers.) Furthermore, given that the shipment volume of hearing aids for severe hearing loss is currently far greater than that of domestic hearing aid brands, the procurement costs for receivers and speakers are lower than those for domestic hearing aids. Since assembly and production also take place in China, domestically produced online hearing aids hold no production cost advantage over imported online hearing aids. The disadvantage becomes more pronounced as products move toward higher performance and premium segments, whereas there is greater viability in the mid-to-low-end market.

Neck-worn hearing aids are a popular category of online hearing aids, with their core feature being loss prevention. However, since multiple OEM manufacturers can produce them, there are no barriers to entry at the production level. Chinese-made online hearing aids often source from different OEM suppliers, necessitating correspondence with multiple medical device registration certificate series. In contrast, for imported online hearing aids, apart from Shanghai’s regulatory requirements for certification, which differ somewhat from other regions, most products across all price ranges are covered by just two or three certificates. If we adopt the perspective of an import manufacturer’s production manager, is it possible that, in order to further reduce production costs, the core hardware components of different hearing aid series under the same registration certificate are unified, with distinctions between series and pricing achieved solely through algorithmic differentiation? This could represent another layer of competitive advantage, leaving readers and Chinese online hearing aid brands to reflect on this possibility.

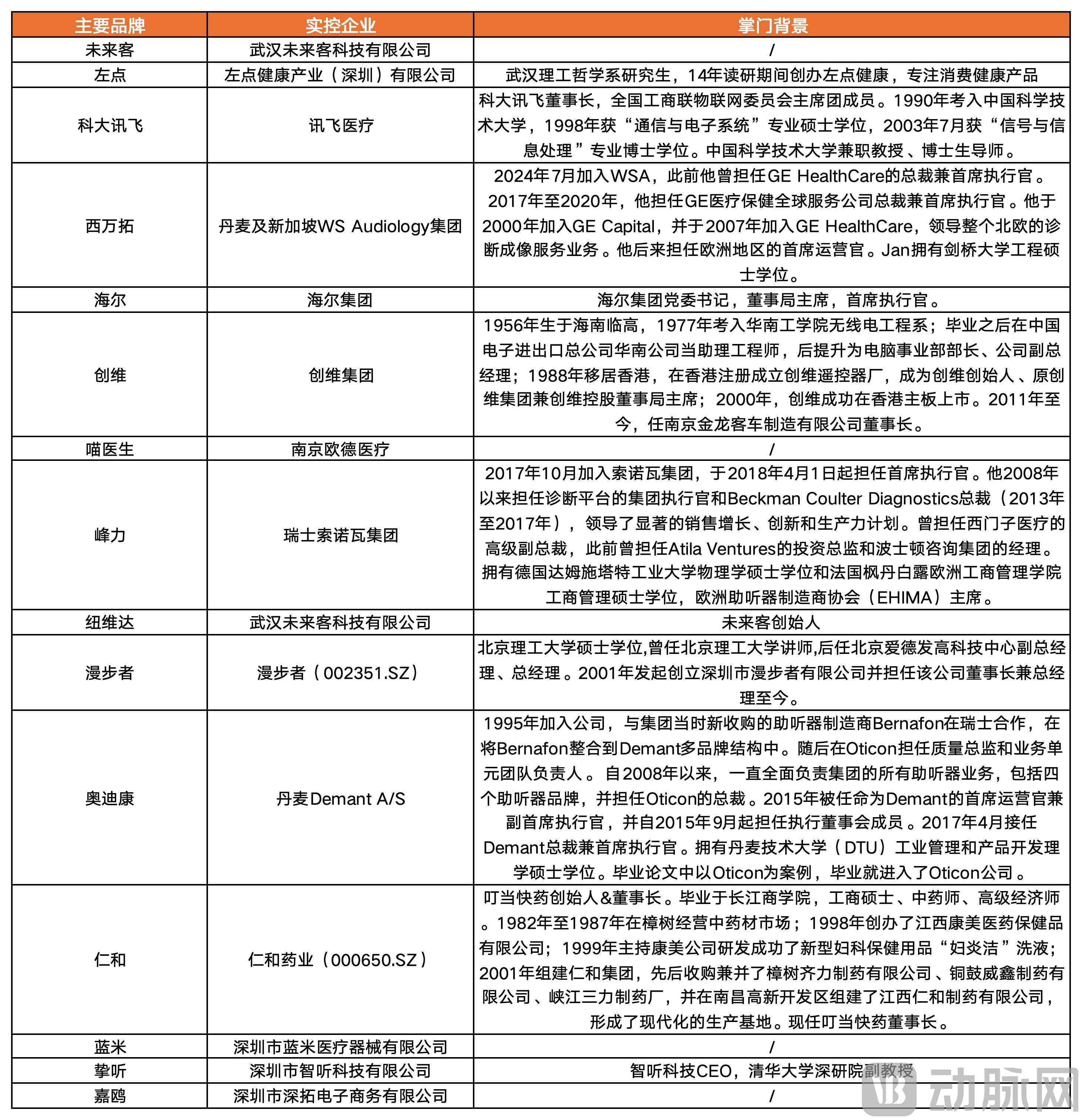

IV. Who are the leaders of online hearing aid brands with annual sales exceeding RMB 10 million?

Among them, eight leading online hearing aid brands are either publicly listed companies or international giants. Headphone manufacturers, AI companies, and consumer electronics firms are actively entering the online hearing aid market.

V. How effective has Apple’s entry into the online hearing aid market via Bluetooth earphones been, and what impact will it have on the industry?

Apple’s AirPods Pro 2, evaluated by internal experts in the field of audiology, have demonstrated performance in addressing mild-to-moderate hearing loss that surpasses the amplification efficacy of most higher-priced OTC/online hearing aids. Currently, the AirPods Pro 2 are priced at RMB 1,899. Compared to the five major hearing aid manufacturers in Europe and the United States, Apple still requires a considerable period to accumulate expertise in the acoustic processing details necessary for severe hearing loss; thus, it is unlikely to make a substantial impact on the market for severe-hearing-loss devices in the near term. Nevertheless, Apple possesses strong capabilities in both proprietary chip development and brand power. By entering the mild-to-moderate hearing loss market through Bluetooth earbuds with integrated hearing aid functionality, Apple is better positioned than online/OTC hearing aid providers to manage user expectations, reduce return rates, and cultivate a future user base for severe hearing loss solutions.

According to data from e-commerce platforms, domestic online sales of Bluetooth earbuds reached 130 million units over the past year, with sales revenue exceeding RMB 21.9 billion—tens of times larger than the market size for online hearing aids. Following Apple’s success in the OTC hearing aid sector, it is poised to significantly squeeze the market share of Chinese-made OTC hearing aids. Will Chinese manufacturers, represented by Xiaomi and known for their strategy of “following rather than leading,” make a major entry into the OTC hearing aid market once Apple has matured both the supply chain and consumer habits?

Existing online hearing aid brands are plagued by high return rates, a lack of professional fitting services, the complete absence of rehabilitation training, and chaotic pricing. How much further must we go to build a truly meaningful domestic online hearing aid brand by reducing return rates through cost-controllable, standardized remote fitting and rehabilitation training services? We shall wait and see.

Despite the hearing aid industry’s current challenges—namely, the difficulty of achieving breakthroughs in core algorithms and the monopoly of chips by overseas giants—the Chinese market holds substantial potential. Entrepreneurship in the hearing care sector requires adherence to the objective laws governing the hearing aid industry as a tangible manufacturing sector, and a clear-eyed recognition that achieving success demands a commitment spanning decades. There is no right or wrong approach, whether one chooses to pursue aggressive, high-intensity growth or opt for modest, sustainable profitability. If, after fully appreciating the strength of competitors and the harsh realities of the industry, you still believe you possess unique competitive advantages and wish to launch a venture in the hearing aid sector—aiming to change the status quo where domestically produced hearing aids account for less than 10% of the market—or if you require the aforementioned data for business promotion purposes, please feel free to contact me (WeChat: leonstanford18).