Inpatient Costs Hit a Decade-Low, Disrupting Commercial Health Insurance Logic

The effects of healthcare insurance payment method reforms and medical cost containment are becoming increasingly significant.

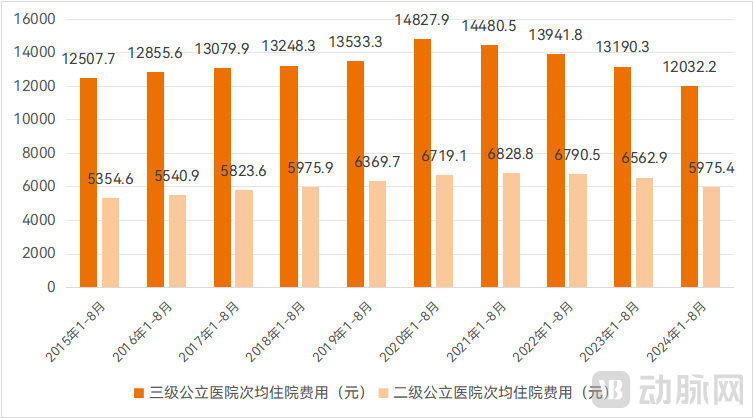

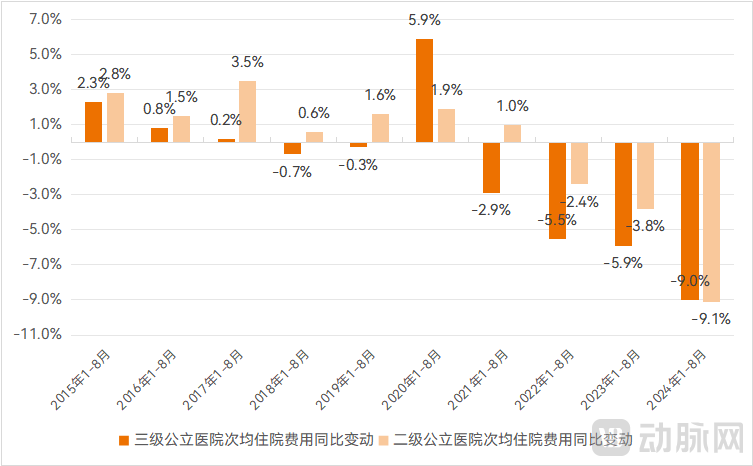

Official data show that from January to August 2024, the average hospitalization cost per visit at public tertiary hospitals across China was RMB 12,032.2, representing a 9.0% year-on-year decrease (at comparable prices). This marks the largest decline in a decade, with the average cost per hospitalization falling below the level recorded during the same period ten years ago.

From the payer’s perspective, reduced inpatient costs can alleviate the financial burden on both public health insurance funds and individual patients. However, the situation is not so straightforward for commercial health insurers. Underlying these cost reductions are changes in inpatient medical service processes, service offerings, and the utilization of pharmaceuticals and consumables, which may render existing coverage provisions of health insurance policies ineffective.

As inpatient costs hit record lows, how can health insurance redefine its role within the multi-tiered medical security system? This is an urgent issue for the industry to address.

Under the influence of a series of measures from the new healthcare reform, the average cost per hospitalization has gradually decreased in recent years.

According to data released by the National Health Commission, from January to August 2024, the average hospitalization cost per visit at tertiary public hospitals across China was RMB 12,032.2, the lowest level in a decade and even slightly lower than that of the same period in 2014. This figure represents a 9.0% year-on-year decrease compared to the same period in 2023 (at comparable prices), marking the largest decline in ten years.

Meanwhile, the average inpatient cost per visit at secondary public hospitals showed a similar downward trend, with a year-on-year decrease of 9.1% from January to August 2024 (at comparable prices).

Changes in the Average Hospitalization Cost per Visit in Public Hospitals over the Past Decade, Data Source: National Health Commission

Change in Average Inpatient Cost per Visit at Public Hospitals over the Past Decade (Adjusted for Comparable Prices), Data Source: National Health Commission

Of course, the possibility of “unbundled hospitalizations” in medical institutions cannot be ruled out. However, an overview of the changes in the number of discharges from public hospitals in recent years shows that the overall level has remained stable, with no significant abnormal increase. In addition, the average outpatient cost per visit at public hospitals has also shown a downward trend, making it difficult to conclude that inpatient costs are being shifted to outpatient services.

The majority of medical expenses are incurred during hospitalization. Reducing the average cost per hospital stay not only alleviates pressure on the basic medical insurance fund but also lessens the financial burden on patients. As an important component of China’s multi-tiered healthcare security system, what changes will commercial health insurance undergo?

Among the two major branches of commercial health insurance, disease insurance—represented by critical illness insurance—primarily triggers benefits upon the occurrence of a covered disease, whereas medical insurance provides coverage based on the occurrence of medical services.The reduction in the average cost per hospitalization is a result of changes in treatment protocols, as well as the use of pharmaceuticals and medical consumables, thereby making it highly correlated with medical insurance.

Taking the popular "Million-Yuan Medical Insurance" products within the medical insurance category as an example, these plans typically feature several key characteristics: coverage is primarily focused on inpatient medical care; sum insured amounts reach up to several million yuan; and 100% reimbursement is provided for expenses exceeding the deductible (usually set between a few thousand yuan and 10,000 yuan) after social medical insurance payments. Some plans also cover new therapies and specialized innovative drugs included in a specified formulary.

In the past, million-yuan medical insurance plans served as an effective supplement to basic medical insurance for certain high-cost diseases. However, as the average cost per hospitalization has decreased, two issues have emerged. First, policyholders’ out-of-pocket expenses after basic medical insurance reimbursement may fail to meet the deductible threshold, rendering them ineligible for claims. Second, the reduction in medical costs is closely tied to the use of drugs and consumables procured through centralized volume-based procurement. If hospitals do not utilize new specialty drugs, the practical value of the corresponding coverage clauses in medical insurance products is significantly diminished.

In recent years, the growth rate of premium income for medical insurance has surpassed that of critical illness insurance, with its share of total health insurance premiums steadily increasing. Since January 2025, dozens of life insurance companies have successively disclosed their annual claims reports. Overall, the scale of medical insurance claims has continued to rise, with the number of paid claims far exceeding those for critical illness insurance.

Given the pivotal role of medical insurance in the health insurance market, reforming health insurance with a focus on medical insurance is imminent under the overarching trend of controlling medical costs.

Traditional medical insurance policies condition payouts on the occurrence of medical services, with coverage primarily focused on in-hospital treatment and the direct management of diseases. Currently, however, medical insurance is expanding beyond hospital settings, extending its scope to areas outside conventional disease treatment.

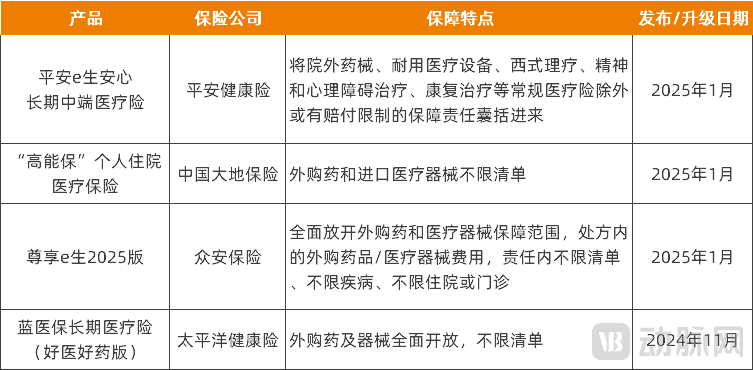

One of the most notable trends is that more medical insurance plans are adding coverage for externally purchased drugs and devices not restricted to a specific formulary.

In fact, in recent years, an increasing number of medical insurance products have incorporated coverage for specialty drugs dispensed outside hospitals to meet the demand for expensive medications required in the treatment of critical illnesses. The formulary of covered specialty drugs has been gradually expanding, growing from dozens to over a hundred, with some plans now covering more than 200 such drugs. Following the widespread implementation of Diagnosis-Related Group (DRG)-based payment systems, restrictions on in-hospital medication use have tightened further, necessitating more comprehensive out-of-hospital drug coverage to address diverse medication needs.Products, including million-yuan medical insurance and mid-end medical insurance, are gradually incorporating coverage for externally purchased drugs and medical devices not restricted to specific formularies.

In November 2024, Pacific Insurance launched the “Blue Medical Insurance Long-term Medical Plan (Premium Drugs and Devices Edition),” which provides comprehensive coverage for externally purchased drugs and medical devices without being restricted to a specific formulary.

In January 2025, ZhongAn Insurance launched the “Zunxiang E-Sheng 2025” million-yuan medical insurance plan. This product iteration comprehensively expanded coverage for externally purchased drugs and medical devices. Expenses for prescription-based externally purchased drugs and medical devices are covered without restrictions on formularies, diseases, or care settings (inpatient or outpatient), and no separate deductible applies.

Recent Medical Insurance Products with Waived Liability for Externally Purchased Drugs and Devices, Source: Public Corporate Information

Another manifestation is that, from the perspective of disease intervention, medical insurance products are significantly expanding their coverage, extending from treatment to rehabilitation.

Typically, medical insurance focuses solely on disease treatment, with rehabilitative care falling outside this scope. Currently, some medical insurance plans, particularly mid-tier policies, have begun to include rehabilitative care in their coverage.

In January 2025, Ping An’s “e-Sheng Anxin” long-term mid-end medical insurance was launched, covering rehabilitation expenses; treatments received in the rehabilitation department within 30 days after hospital discharge are also eligible for reimbursement. In November 2024, AIA Life Insurance launched the “Zhuoyue Yisheng” series of medical insurance products, whose coverage also includes postoperative rehabilitation.

In recent years, rehabilitation medicine has assumed an increasingly pivotal role within the healthcare service system, and professional rehabilitation therapy serves as an effective measure to prevent disease recurrence and hospital readmission.

Public medical institutions concentrate China’s major healthcare resources and possess a public-welfare nature.In the past, medical insurance was primarily tied to public healthcare resources with a universal coverage mandate. However, current trends indicate that mid-to-high-end healthcare resources are assuming an increasingly prominent role in insurance products.

In the special needs, VIP, and international departments of public hospitals, patients receive treatment as self-pay individuals, are minimally affected by medical insurance policies, and both doctors and patients can make more flexible choices regarding treatment plans and medications. However, special needs medical services within public healthcare institutions are also subject to constraints, with revenue and service volume capped at a certain proportion of the hospital’s total. Therefore, mid-to-high-end private healthcare institutions, which are less influenced by medical insurance policies, also provide patients with more options for medical care and medication.

These medical resources, previously covered mostly by mid-to-high-end health insurance plans, are now also included in the scope of million-yuan health insurance policies.

In August 2024, the upgraded “Ping An Twin Stars Medical” million-yuan medical insurance plan eliminated the deductible within its general medical coverage benefits. In addition to standard hospital wards, policyholders may also receive treatment in the special needs, VIP, and international departments of public hospitals at Tier II level or above.

In fact, million-yuan medical insurance is currently undergoing a transition, with some products beginning to align with mid-tier medical insurance. As previously mentioned, more comprehensive drug coverage and mid-to-high-end medical services, which were originally covered under mid-to-high-end medical insurance plans, are now being incorporated.

VCBeat learned from industry insiders that, with policy changes, currentlySome insurance agents are primarily promoting mid-tier medical insurance plans without social security coverage to their clients. Certain third-party service providers have also shifted their focus, transitioning from million-yuan medical insurance products to mid- and high-end medical insurance offerings.

Overall, health insurance is breaking through its traditional boundaries in terms of medical and pharmaceutical resources as well as coverage scope. The transformation on the product side will inevitably lead to changes in the industry ecosystem, which is also a process of gradually addressing several core industry issues.

First, how should we re-examine the positioning of commercial health insurance within the multi-tiered medical security system?

In the past, traditional health insurance policies primarily covered services within the public healthcare system and adhered to the national medical insurance reimbursement catalog. Their supplementary role in the healthcare security framework was largely limited to secondary expense reimbursement—providing additional coverage at the claims settlement stage—which indeed alleviated some financial burdens for policyholders. However, the critical issue remains that treatments or services not covered by basic medical insurance are often excluded from commercial health insurance coverage as well, or are subject to extremely limited benefits.In short, there is significant overlap between traditional health insurance and the “basic coverage” provided by public medical insurance, while protection beyond the scope of public medical insurance remains inadequate.

Currently, health insurance is transforming its previous state of strong reliance on the public healthcare system and the National Reimbursement Drug List. It now occupies a more distinct position, complementing basic medical insurance across the spectrum—from medical and pharmaceutical resources to claims reimbursement.

According to the National Healthcare Security Administration, the first edition of the Class C Drug List is expected to be released in 2025. This list will primarily cover drugs that demonstrate a high degree of innovation, significant clinical value, and substantial patient benefits, but are currently excluded from the Basic Medical Insurance Catalog due to their deviation from the “basic coverage” mandate. The initiative aims to guide and support commercial health insurance in incorporating Class C listed drugs into their coverage scope. At that time, the Class C Drug List is anticipated to help commercial health insurance establish a clearer positioning for its coverage benefits.

Second, how can claims payout risks be controlled under the new positioning?

In the previous model, given the stringent regulation of public medical institutions and the basic medical insurance fund, commercial health insurance has substantially benefited, in terms of claims risk, from the oversight of medical practices by competent authorities such as the National Health Commission and the National Healthcare Security Administration.

As health insurance expands to “out-of-hospital” settings, it faces a greater number of claim risk points.For instance, high-value medications may disproportionately consume insurance coverage limits, thereby increasing the risk of product losses; furthermore, patients may collude with out-of-hospital pharmacies to fraudulently prescribe medications or engage in excessive consumption.

Certainly, insurance companies and third-party service providers can leverage big data analytics to assess pharmaceutical cost risks, dynamically adjusting deductibles or premiums to balance claims pressure. More importantly, it is essential to safeguard the health status of policyholders, thereby minimizing claims expenditures at the source.

The concept of “insuring health” in the health insurance industry has been proposed for many years. Health insurance products can allocate 20% of their costs to health management, aiming to intervene in health risk factors, control the onset and progression of diseases, and maintain a healthy state. However, the practical implementation of this concept has yielded limited results.In today’s changing macro environment, “health preservation” is being prioritized in earnest. Health management, once focused on formality, will increasingly emphasize substance and outcomes—particularly for non-standard body health insurance products.

In 2024, Taiyi Guanjia secured RMB 920 million in Series C strategic financing, making it the only service-oriented enterprise among the top ten largest funding rounds in the healthcare sector that year; all other recipients were pharmaceutical and medical device companies. Health management is expected to play a pivotal role in the health insurance industry.

Third, can health insurance become a major source of diversified payment for innovative drugs and medical devices?

Since the establishment of the National Healthcare Security Administration, the frequency and volume of innovative drugs included in the National Reimbursement Drug List have increased. However, its positioning as providing “basic coverage” still limits the reimbursement capacity for innovative drugs. Furthermore, in the recent 10th round of national centralized drug procurement, no originator pharmaceutical companies were selected as winners. There is an urgent need for more diversified payment mechanisms for innovative drugs and medical devices to meet patients’ multi-tiered needs.

As health insurance coverage expands—from healthy individuals to substandard risks and further to those with pre-existing conditions—and increasingly incorporates mid-to-high-end medical resources, the theoretical payment volume for innovative drugs and medical devices is expected to grow. Including innovative drugs and medical devices in insurance products is also a key strategy for building differentiated competitiveness in health insurance offerings.

Both parties need to engage in deep collaboration and create value for each other.For instance, by integrating innovative drugs with payment mechanisms for specific diseases, the adoption of personalized treatment regimens can be promoted; through joint resource integration and the development of outcome-based insurance products, healthcare payment models can be shifted from “cost containment” to “value-based care.”

Of course, no transformation yields immediate results. As long as the direction is clear and sufficient momentum exists, commercial health insurance will undoubtedly be revitalized and return to the fast track of growth.