Post-Slump Surge: Medical Equipment Demand Explodes Amid Policy Tailwinds and Procurement Rebound

After Enduring the Winter, Long-Suppressed Demand in the Medical Device Market Has Fully Exploded!

In the first half of 2024, sales of medical equipment were nearly halved, with the winning bid amounts for magnetic resonance imaging (MRI) systems, computed tomography (CT) scanners, and ultrasound devices each declining by 40% year-on-year. It can be said that the medical equipment industry has entered its coldest winter in a decade.

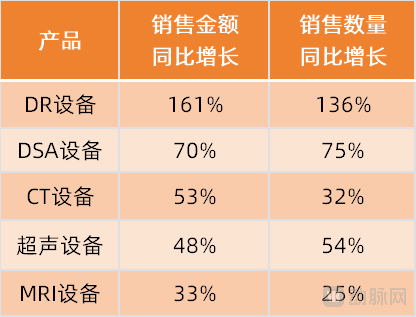

However, the medical device market has once again surged. According to data from Yizhuang Shusheng, the medical imaging equipment market saw a year-on-year growth of over 47% in January 2025. Among these, sales revenue for DR (Digital Radiography) equipment increased by 161% year-on-year, DSA (Digital Subtraction Angiography) equipment by 70%, CT (Computed Tomography) equipment by 53%, ultrasound equipment by 48%, and MRI (Magnetic Resonance Imaging) equipment by 33%.

(January 2025, Sales Volume of Medical Device Products)

The surge in sales of medical devices is partly due toBidding Activities Resume Normalcy, and Suppressed Demand Is Released. Previously, the anti-corruption campaign in the healthcare sector triggered a wave of suspensions and delays in many bidding projects. Currently, bidding activities across various regions have resumed normal operations, leading to a concentrated surge in demand for medical equipment among healthcare institutions.

On the other hand, it is becauseMedical Equipment Trade-in Program andLarge-Scale Implementation of Medical Equipment Renewal and Procurement Plans Across Provinces and Cities. In March 2024, the State Council issued the Action Plan for Promoting Large-Scale Equipment Renewal and Consumer Goods Trade-In. With policy support, most provinces and municipalities launched work plans for medical equipment renewal, which accelerated implementation in 2025. For instance, Sichuan Province released a procurement announcement in late December 2024, with a budget of RMB 437 million to purchase 380 units (sets) of medical equipment such as CT scanners, digital radiography (DR) systems, and color Doppler ultrasound devices; Hebei Province issued an announcement in October 2024, with a budget of RMB 644 million to procure equipment including CT scanners, DR systems, and color Doppler ultrasound devices……

In addition, on January 3, 2025, the National Development and Reform Commission (NDRC) stated that it would support the strategic deployment of high-level hospitals this year by establishing 125 national regional medical centers, allocating RMB 10 billion to support the development of closely integrated county-level medical consortia, and upgrading medical equipment such as CT scanners, B-mode ultrasound systems, and hemodialysis machines for county-level hospitals and township health centers.Driven by this positive news, the medical device market is expected to see further robust growth.。

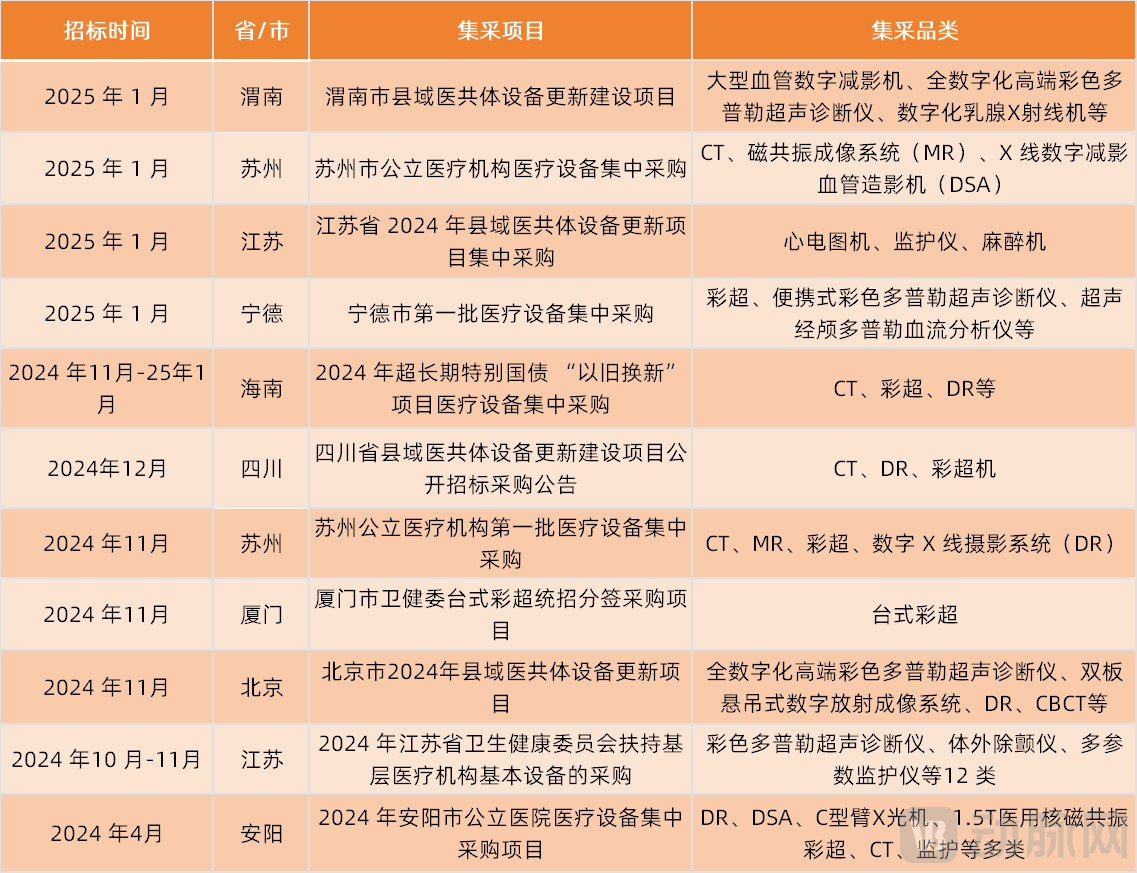

In addition, the medical device market is undergoing dramatic changes under the influence of centralized procurement.. According to statistics, centralized procurement of medical equipment has been rolled out nationwide and is showing an intensifying trend. For example, in January 2025, Weinan released the "Weinan County-Level Medical Community Equipment Renewal and Construction Project," initiating centralized procurement for devices such as DSA, color Doppler ultrasound, and DR; Suzhou issued the "Centralized Procurement Project for Medical Equipment in Public Medical Institutions," covering CT, MRI, DSA (Digital Subtraction Angiography systems), and other equipment; additionally, provinces and cities including Jiangsu, Ningde, Hainan, Sichuan, and Beijing have all launched centralized procurement projects for medical equipment.

The market boom, coupled with centralized procurement, has introduced more variables into the medical device industry. How will the medical device market evolve under the influence of multiple factors? What changes will centralized procurement bring? How should companies respond?

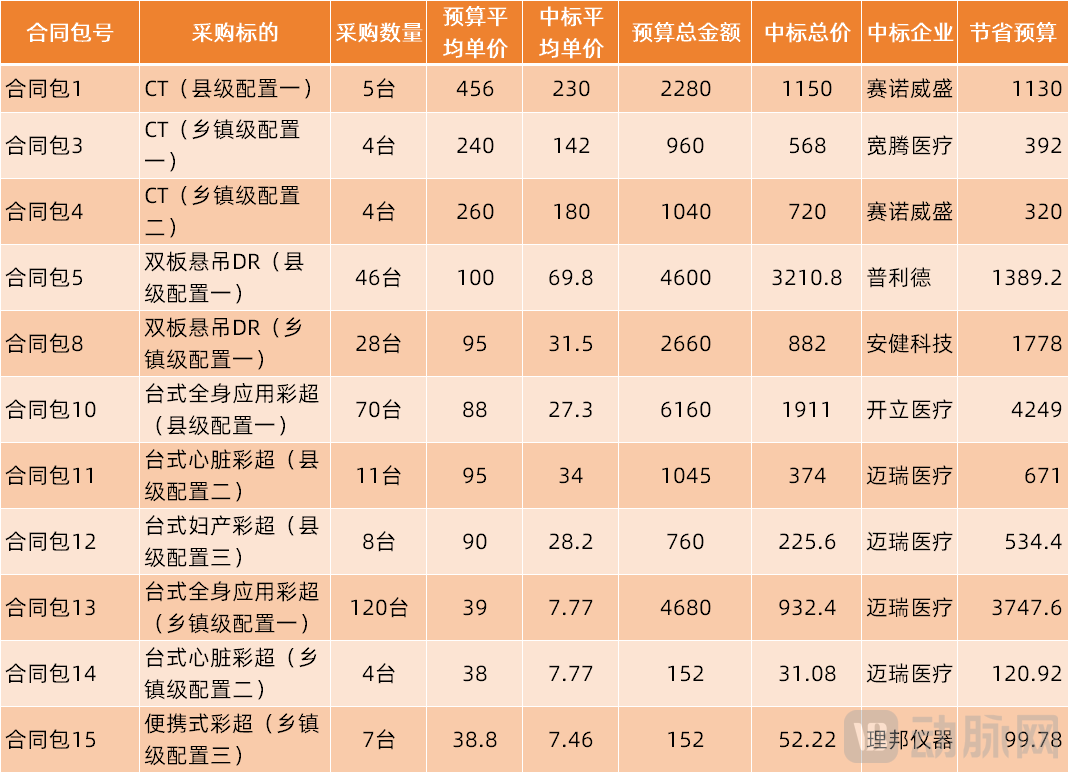

In late January 2025, Sichuan Province released the bid award announcement for the “County-Level Medical Community Equipment Renewal and Construction Project.” The award data showed that, after excluding invalidated bids, a total of 11 contract packages were awarded. The relevant budget amounted to RMB 240 million, while the total winning bid value was RMB 100 million, resulting in budget savings of RMB 140 million and a cost-saving rate of 58.33%.

(Winning Bid Data for the Medical Equipment Upgrade and Construction Project of County-Level Medical Consortia in Sichuan Province, Unit: 10,000 Yuan)

According to the bid-winning data, the price reduction for color Doppler ultrasound products in this centralized procurement was significant, with winning bids 68%-80% lower than the budgeted prices. The price reduction for CT products ranged from 30% to 50%, and for dual-panel suspended DR systems, it ranged from 30% to 60%.

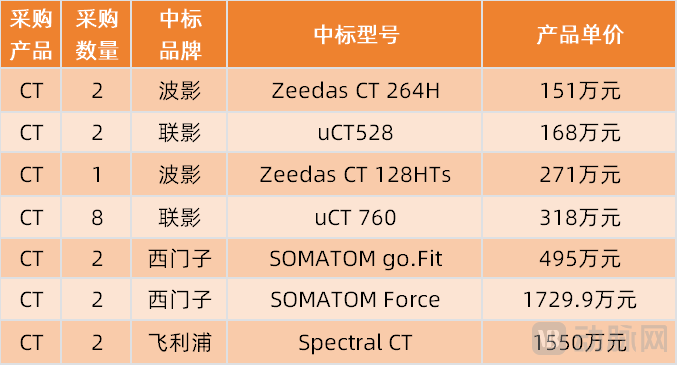

In fact, following the centralized procurement of medical devices, related products have all experienced varying degrees of price reduction. For example, in the Anyang City medical device centralized procurement project, the winning bid unit price for a 256-slice CT scanner decreased from RMB 24.69 million to RMB 14.50 million; for high-end 1.5T MRI systems, it dropped from RMB 12.37 million to RMB 6.31 million; for DSA (Digital Subtraction Angiography) systems, it fell from RMB 6.87 million to RMB 3.45 million; for 64-slice CT scanners, it declined from RMB 7.44 million to RMB 3.95 million; and for ultra-high-end color Doppler ultrasound systems, it reduced from RMB 2.17 million to RMB 1.20 million.

However, the magnitude of price reductions in centralized procurement varies across products with different market positioning.。

For low-end products, price reductions are generallyOver 70%。For example, in the medical equipment renewal and upgrade project for county-level medical consortia in Sichuan Province, the price reductions for desktop whole-body color Doppler ultrasound systems, desktop cardiac color Doppler ultrasound systems, and portable color Doppler ultrasound systems configured at the township level were 79.82%, 79.53%, and 80.77%, respectively.

The Xiamen centralized procurement project for desktop color Doppler ultrasound systems, with unified bidding and separate contract signing, announced its winning bidders in January. Mindray Medical’s Consona Nova desktop ultrasound system, targeted at the primary care market, won the bid, with the winning price representing a 79.8% reduction from the budgeted price. Meanwhile, Mindray’s Nuewa IV desktop color Doppler ultrasound system, designed for primary care and other settings, saw a price reduction of 77.8%.

(Second Round Bid Award Results for the Xiamen Desktop Color Doppler Ultrasound Centralized Procurement Project with Unified Bidding and Separate Contracting)

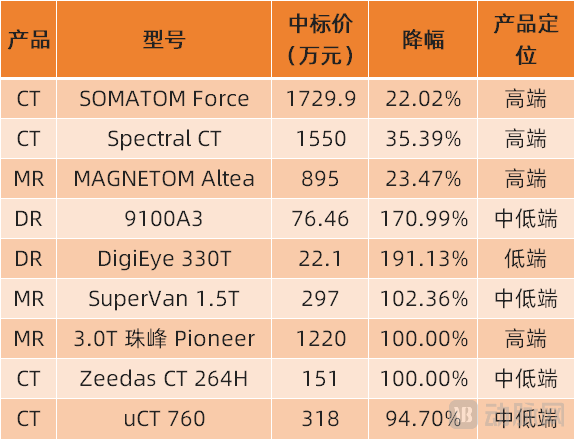

For mid-to-high-end products, price reductions are relatively moderate.,A reduction of approximately 20%-30%。In the first batch of centralized procurement projects for medical equipment in Suzhou City in 2024, Siemens' high-end CT and MR systems saw price reductions of 22.02% and 23.47%, respectively, while Philips' high-end CT systems experienced a 35.39% price reduction.

(Results of the First Batch of Centralized Procurement Projects for Medical Equipment in Suzhou City in 2024)

In addition, in the recently disclosed medical equipment renewal project at Peking University First Hospital, GE Healthcare won the bid for one ultra-high-end 3.0T MRI system at RMB 22 million, one ultra-high-end multi-slice spiral CT scanner at RMB 20 million, and one high-end 1.5T MRI system at RMB 12 million. Siemens Healthineers won the bid for one ultra-high-end 3.0T MRI system at RMB 21.8 million.

High-end and ultra-high-end medical devices continue to command relatively high winning bid prices, with modest price reductions. This is attributable to their greater technical complexity, higher entry barriers, and stronger innovativeness, which limit the number of manufacturers capable of developing such products. As a result, competitive pressure is somewhat weaker, granting these companies greater bargaining power and pricing authority.

Overall, driven by centralized procurement, the prices of medical device products are generally declining. Among these, mid-to-high-end medical devices demonstrate stronger competitiveness, with smaller price reductions and remaining room for adjustment; in contrast, low-end medical devices have experienced more significant price cuts, further intensifying market competition.

Declining product prices, particularly for low-end medical devices, have directly squeezed the profit margins of medical device companies, compelling them to maintain profitability by reducing production costs and optimizing operational processes. For small and medium-sized enterprises (SMEs), the significant compression of profit margins may intensify survival pressures, whereas large enterprises, leveraging their diverse product pipelines, economies of scale, and cost-control capabilities, demonstrate greater resilience.

In response to this situation, domestic enterprises need to leverage their technological advantages to reduce product costs and enhance market competitiveness; meanwhile, they must also accelerate innovation to break into the high-end market.

It is worth noting that repeated centralized procurement has accelerated the replenishment and upgrading of medical equipment in primary healthcare institutions. In the past, some medical devices in China were used beyond their service life, posing various risks. Currently, with the support of centralized procurement, medical equipment suitable for the primary care market is being widely purchased.

Taking the medical equipment procurement data from January 2025 as an example, CT equipment sales volume increased by 32% year-on-year, while sales revenue rose by 53% year-on-year; DR equipment sales volume surged by 136% year-on-year, with sales revenue increasing by 161% year-on-year. It is evident that the growth in sales revenue significantly outpaced the growth in sales volume, indicating a replacement cycle for low-end products and an accelerated adoption of mid-to-high-end products in Grade A tertiary hospitals, where the increased sales volume of mid-to-high-end products drove up the overall sales revenue.

Beyond steep price cuts, volume-based procurement is also reshaping the market landscape for medical devices.

From the perspective of centralized procurement rules, multiple domestic medical equipment centralized procurement projects in China have explicitly stated that they do not accept bids for imported products and only accept Chinese-made medical devices.。

For example, in September 2024, the “Tender Announcement for Centralized Procurement of Medical Equipment Projects” issued by the Hohhot Municipal Health Commission indicated that the centralized procurement of medical ultrasound instruments and equipment would only accept bids from domestically produced medical devices. Similarly, the first and second batches of the “Suzhou City 2024 Centralized Procurement of Medical Equipment for Public Medical Institutions,” conducted in November 2024 and January 2025 respectively, also did not accept bids for imported products. The “Procurement Announcement for Basic Equipment Support for Primary Healthcare Institutions by the Jiangsu Provincial Health Commission in 2024” marked “No” in the option “Whether to Accept Bids for Imported Products.”

Domestic companies also benefit the most from the results of centralized procurement.

Statistics show that in the equipment renewal and construction projects for county-level medical consortia in Sichuan Province, the total winning bid amount was approximately RMB 100 million, with all winning enterprises being domestic brands. Among them, Sinovision won the bid for 9 CT units; Kuanteng Medical won the bid for 4 CT units; Sonoscape won the bid for 70 color Doppler ultrasound systems; Mindray won the bid for 4 procurement packages, totaling 143 color Doppler ultrasound systems; Edan Instruments won the bid for 7 color Doppler ultrasound systems; Perlove and Angell Technology won the bids for 46 and 28 dual-panel ceiling-mounted DR systems, respectively.

Distinguished by market positioning,Domestic brands primarily win bids in the mid- to low-end market, whileThe mid-to-high-end and ultra-high-end markets are primarily dominated by imported brands.. For example, in the centralized procurement project for medical equipment at public healthcare institutions in Anyang City (radiology category), Philips won bids for three mid-to-high-end CT scanners and two high-end MRI systems (1.5T magnetic resonance imaging), GE Healthcare won bids for one DSA system and two ultra-high-end 256-slice CT scanners, and Siemens Healthineers won bids for four ultra-high-end color Doppler ultrasound systems.

Another example,in Suzhou City2024First Batch of Centralized Procurement of Medical Equipment by Public Healthcare Institutions in 2026CTIn the project, United Imaging Healthcare won the bid.10Set, Siemens Healthineers Wins the Bid4Kit (2High-end series,2(ultra-high-end), Boying won the bid3Set, Philips Wins Bid2Kit (Ultra-High-End).

(Suzhou 2024 Centralized Procurement of Medical Equipment for Public Medical Institutions, Batch 1: CT Project)

Fortunately,Domestic brands are also gradually breaking into the high-end marketFor instance, United Imaging Healthcare’s ultra-high-end MR (magnetic resonance) product, the uMR 880, won the bid in the centralized procurement of MR systems for public medical institutions in Suzhou at a price of RMB 17.56 million.

Based on the results of numerous volume-based procurement programs, the number of winning bids secured by domestic brands far exceeds that of imported brands. Meanwhile, domestic brands have achieved significant success in the mid- to low-end markets.,Gradually achieving breakthroughs in the mid-to-high-end and ultra-high-end markets.

Reflected in the market landscape,GE Healthcare, Siemens Healthineers, and Philips Retreat from the Low- to Mid-End Market as Chinese Brands Gain Market Share. Taking CT as an example, in the first three quarters of 2024, for models with fewer than 64 slicesMid- to Low-End CT Market, the market share concentration of imported brands such as GE, Siemens, and Philips decreased year-on-year, with their market share being captured by domestic brands including Neusoft Medical, Wandong Medical, Anke, Minfound, Synovision, Kuanteng Medical, and Kangda Intercontinental.

but for scanners with more than 64 slicesMid-to-High-End CT Market, United Imaging Healthcare, GE HealthCare, Siemens Healthineers, and Philips collectively accounted for 89.93% of the market, representing a year-on-year increase of approximately 11%. Market concentration has further intensified, with the brand effect of leading players becoming increasingly pronounced.

In the past, GE Healthcare, Siemens Healthineers, and Philips once held over 90% of the market share in the high-end product segments such as PET/CT, MR, and CT.

However, the market landscape is gradually shifting. According to United Imaging Healthcare’s annual report data, in the mid-range CT new installation market, United Imaging Healthcare rose from third place in market share in 2023 to first place in the first half of 2024; in the high-end CT (128-slice and above) new installation market, its market share ranking improved from third in 2023 to second in the first half of 2024.

Not only United Imaging Healthcare, but also enterprises such as Neusoft Medical and SinoVision have broken into the high-end CT market. For instance, Neusoft Medical launched the world’s first whole-body spiral CT with a rotation time of 0.235 seconds, and established its euViz Epoch+ Wuji series and NeuViz Glory+ Yaoshi series of ultra-high-end CT systems.

Additionally, United Imaging Healthcare is alsoMR (Magnetic Resonance) and others in the marketBreakthroughs in the high-end segment. For instance, based on the value of newly added market sales, United Imaging Healthcare’s market share in the 1.5T and below superconducting MRI market rose from second place in 2023 to first place in the first half of 2024; in the ultra-high-field MRI equipment market above 3.0T, United Imaging Healthcare maintained its leading market share position throughout 2023–2024.

Domestic brands such as Sonoscape Medical and Mindray Medical areHigh-End Color Doppler UltrasoundBreakthroughs have also been achieved in this area. In 2023, SonoScape launched the S80/P80 series of ultra-high-end color Doppler ultrasound platforms and released the S60 and P60 series of high-end color Doppler ultrasound systems. Mindray has deployed its Kunlun Resona A20, an ultra-high-end ultrasound system for whole-body applications, and the Nuewa A20, an ultra-high-end color Doppler ultrasound device for obstetrics and gynecology.

In addition, domestic brands are gradually emerging in the field of DSA (Digital Subtraction Angiography systems). For a long time, the DSA market has been dominated by overseas brands. Currently, the market share of domestic DSA brands is only about 10%.

Nevertheless, domestic brands are accelerating their breakthroughs. For instance, Neusoft Medical launched the first domestically produced multimodal one-stop high-end Angio-CT imaging system, which combines a 126-slice CT with a high-end angiography system, capturing an 8% market share within two years and breaking the monopoly of imported brands in the DSA market. Building on this foundation, companies such as Neusoft Medical and Vimai Medical have successively introduced high-end DSA equipment to fill the gap in the domestic high-end DSA sector.

Overall, although GE Healthcare, Siemens Healthineers, and Philips continue to hold significant positions in the mid-to-high-end market, they are inevitably losing market share to domestic brands. Supported by favorable policies and enhanced competitiveness of domestically produced products, the market share of Chinese brands is steadily increasing.

Based on the winning bid data from centralized procurement,Another Trend in the Medical Device Industry: Market Share Is Concentrating Among Leading Companies, While SMEs Face Challenges。

Specifically, companies such as Mindray and United Imaging are more likely to secure orders in centralized procurement due to their advantages in product quality, pricing, innovation, scale, and cost. Particularly in the mid-to-high-end market, leading enterprises hold a distinct advantage, while small and medium-sized enterprises (SMEs) have limited presence in this segment. This reduces the likelihood of SMEs winning bids in centralized procurement, thereby squeezing their market share.

Meanwhile, competition among small and medium-sized enterprises (SMEs) in the mid-to-low-end market will intensify further. This heightened competition will not only stem from within the SME sector but also from leading companies entering the fray with their own mid-to-low-end product offerings. Consequently, SMEs will face mounting pressure to either transform or risk being eliminated.

To adapt to the market environment under volume-based procurement (VBP), both leading enterprises and small and medium-sized enterprises (SMEs) must proactively implement changes and adjust their strategies. For instance, VBP has squeezed distributors’ profit margins, which may impact companies’ sales models. As market demand for products differs from the past, enterprises need to timely adjust their innovation directions: on one hand, developing low-cost, high-value-for-money products; on the other hand, pioneering globally leading innovative products to avoid price-driven competition.

While centralized procurement poses risks for small and medium-sized enterprises (SMEs), it also harbors opportunities. By leveraging the momentum of centralized procurement to rapidly bring products that meet market demands to market, companies may accelerate their growth and expansion.