Race to Enroll Patients Heats Up as Domestic Autoimmune Drug Makers Enter a Make-or-Break Battle

Recently,Hospitals in the Jiangsu-Zhejiang-Shanghai Region Frequently Engage in "Talent Wars". Taking the dermatology department of a tertiary hospital in Hangzhou as an example, whenever a new patient is admitted, doctors begin to compete fiercely, with messages such as “I’ll take this one,” “Save this one for me first,” “I need this one urgently right now,” and “This one belongs to me for now” repeatedly flooding their internal chat groups.

In fact, this is not an isolated case. According to a set of statistical data, as of June 2024, the number of clinical research projects on atopic dermatitis that have been launched in Zhejiang Province alone has exceeded 500; in addition, from the perspective of major mainstream platforms, a large number of clinical recruitments related to autoimmune diseases are emerging one after another; finally, in various industry groups, discussions mainly revolve around the topic of clinical recruitment. It is not difficult to find that,The entire autoimmune disease sector is currently immersed in a frenzied race to capture patients.。

Figure 1. Vigorous Clinical Recruitment for Domestically Produced Autoimmune Disease Drugs

This was undoubtedly a rare sight, yet it was not unprecedented. The phenomenon of clinical trials “poaching” patients had prior precedents in China, most notably during the era of PD-1/PD-L1 inhibitors, a landmark therapeutic class. It is reported that at the peak of competition, patients with non-small cell lung cancer (NSCLC) in major Chinese cities were once in short supply for trial enrollment. Given that this patient population is substantial, with an annual new-case growth rate exceeding 80%, the emergence of such “excess demand over supply” underscores the intense competitiveness of clinical development. In the aftermath, a clear watershed moment emerged in the PD-1 landscape, with blockbuster products such as Baizean (tislelizumab), Tyvyt (sintilimab), Opdivo (nivolumab; note: “Kaitanni” likely refers to a domestic PD-1, but commonly associated brands include tislelizumab, sintilimab, camrelizumab, and serplulimab; however, based on common market leaders: Baizean, Tyvyt, Airuika [camrelizumab], and Hansizhuang [serplulimab]) rose to prominence, capturing significant market share.*Correction for brand names based on standard English trade names in China:*Baizean (tislelizumab), Tyvyt (sintilimab), Airuika (camrelizumab), and Hansizhuang (serplulimab).Revised translation with accurate brand names:This was undoubtedly a rare sight, yet it was not unprecedented. The phenomenon of clinical trials “poaching” patients had prior precedents in China, most notably during the era of PD-1/PD-L1 inhibitors, a landmark therapeutic class. It is reported that at the peak of competition, patients with non-small cell lung cancer (NSCLC) in major Chinese cities were once in short supply for trial enrollment. Given that this patient population is substantial, with an annual new-case growth rate exceeding 80%, the emergence of such “excess demand over supply” underscores the intense competitiveness of clinical development. In the aftermath, a clear watershed moment emerged in the PD-1 landscape, with blockbuster products such as Baizean (tislelizumab), Tyvyt (sintilimab), Airuika (camrelizumab), and Hansizhuang (serplulimab) rising to prominence and capturing significant market share.

So now, the scene of "talent war" is reappearing in domestic clinical research on autoimmune diseases. Does this mean that the field will soon see a clear winner? Is a long-awaited "big battle" now poised to erupt?

Autoimmune Diseases Enter the “All-In” Era

In 2024, the commercialization of autoimmune disease products reached a new level.

Figure 2. Top 5 Best-Selling Autoimmune Drugs in 2024 (Source: Public Information)

Figure 2. Top 5 Best-Selling Autoimmune Drugs in 2024 (Source: Public Information)

An analysis of financial reports reveals that autoimmune disease therapies not only claim three spots in the global top 10 best-selling drugs, rivaling oncology treatments, but also demonstrate significant growth across multiple products. Sanofi’s dupilumab (Dupixent) achieved robust sales of $14.179 billion, a year-on-year increase of 23%. AbbVie’s risankizumab (Skyrizi) and upadacitinib (Rinvoq) recorded sales of $11.718 billion and $5.971 billion, respectively, with both experiencing growth rates exceeding 50%. In response, the industry has continually expressed admiration.Autoimmune diseases today are what oncology was a decade ago, underscoring the immense market potential in the autoimmune sector.。

Specifically, autoimmune diseases—represented by psoriasis, rheumatoid arthritis, systemic lupus erythematosus, atopic dermatitis, and asthma—affect a large patient population that is showing significant growth. Coupled with the currently low market penetration rates, there is substantial untapped potential. Furthermore, from an industry landscape perspective, unlike the oncology sector, which has become a hyper-competitive “red ocean” in a saturated market, the autoimmune disease field remains relatively open, harboring numerous opportunities for incremental market growth.

This has clearly attracted the attention of leading global pharmaceutical companies, and in recent years,The “Clash of the Titans” is gradually shifting from oncology to autoimmune diseases.。

Take AbbVie’s defense of its “blockbuster” autoimmune drug as an exampleIt is reported that to offset the impact of Humira’s patent expiration, AbbVie has been significantly increasing its investments in recent years. In 2024 alone, the company completed seven transactions in the immunology sector, with a total value exceeding $5 billion, accounting for half of its annual mergers and acquisitions activity. Despite these efforts, AbbVie remains cautious, as evidenced by a surge in R&D spending on autoimmune diseases. In 2024, the company invested $12.191 billion in R&D, representing a year-on-year increase of 66.66%. Notably, this marks the highest level of R&D expenditure in the company’s history.

With some players “defending their throne,” others are inevitably eager to “seize the crown”—such is Sanofi.In the first half of 2024, dupilumab’s sales reached $6.66 billion, officially surpassing Humira to become the new leading drug in the autoimmune sector. By year-end, dupilumab further expanded its lead, breaking through the $14 billion mark with a 23.1% growth rate, thereby removing any suspense from the competition for the title of the next-generation blockbuster autoimmune drug. However, Sanofi is not content to remain passive; beyond dupilumab, it has nine other drugs in the autoimmune space with sales each projected to exceed $5 billion, undoubtedly bolstering its competitive position.

“Johnson & Johnson, one of the ‘Big Three’ in autoimmune diseases, is certainly not idle; it is striving hard to ‘save itself.’”In 2024, several of Johnson & Johnson’s autoimmune products experienced negative growth, with its flagship drug ustekinumab declining by 4.6% year-on-year. Infliximab, which once generated over $90 billion in revenue for Johnson & Johnson, saw its 2024 income drop to $1.605 billion. Golimumab edged down by 0.3%, with annual revenue reaching only $2.19 billion. Under this pressure, Johnson & Johnson has aggressively increased its investments in recent years. Notably, the company spent as much as $6.5 billion to acquire Momenta. Earlier this year, Johnson & Johnson further expanded its portfolio by acquiring the preclinical-stage STAT6 inhibitor KP-723 for $1.25 billion, signaling a strong “all-in” commitment to the autoimmune sector.

In addition to the traditional hegemon,Emerging players, represented by Novartis and Roche, are also continuing to ramp up their investments.It is reported that Roche’s ocrelizumab has surged into the top five best-selling drugs globally in the autoimmune field in 2024. With only two approved indications to date, this suggests that its sales volume is far from reaching its ceiling. Novartis is also a company to watch; it is currently advancing 15 Phase I/II clinical projects and eight Phase III projects in the autoimmune space. Over the next five years, Novartis expects to release results from six Phase III trials and more than ten Phase II trials. Underpinning these efforts is a massive investment exceeding tens of billions of U.S. dollars.

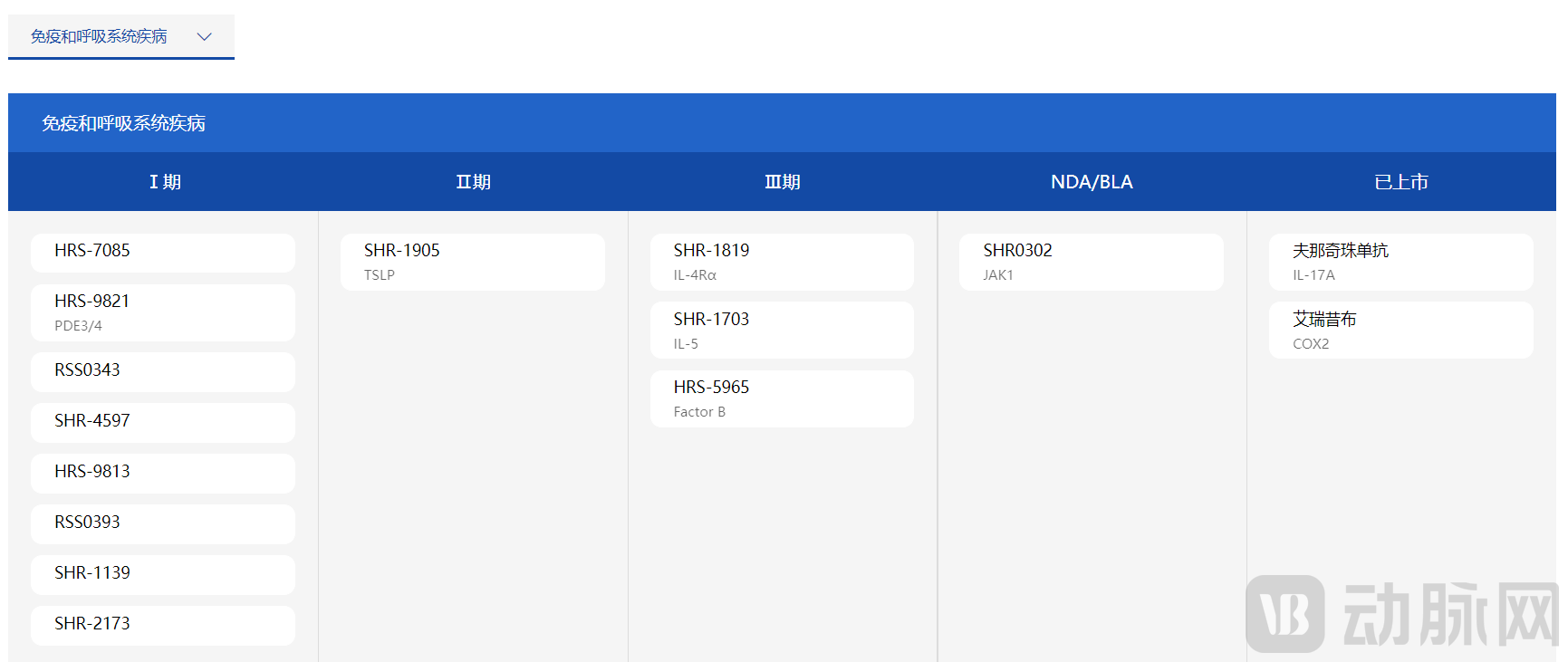

Figure 3. Progress of Hengrui Medicine’s Autoimmune Disease R&D Pipeline (Source: Hengrui Official Website)

In fact, not only MNCs,Chinese pharmaceutical companies are also “betting big” on autoimmune diseasesAccording to incomplete statistics from VCBeat, since 2020, a total of 58 listed pharmaceutical companies in China have entered the autoimmune disease sector. Hengrui Medicine is the most typical example, with 17 pipelines currently in clinical trials, the highest number among domestic companies. Another representative case is 3SBio Inc., which divested all its oncology pipelines in 2023 to focus entirely on R&D in the autoimmune field. It now boasts the most comprehensive portfolio within the IL family, with all its programs ranking among the top three domestically in terms of development progress.

Amid the current capital winter, it is rare to see leading pharmaceutical companies in a specific therapeutic area flocking to invest. However, looking beyond the surface to the essence, each substantial investment sends a clear and critical message to the industry:Autoimmune Diseases Are Gradually Replacing Oncology as the Core Engine of Growth in the Global Pharmaceutical Market。

Domestic Autoimmune Drugs Enter an Intensive Launch Phase

2024 was undoubtedly the breakout year for domestically produced autoimmune drugs.

Focusing on the product side, three blockbuster drugs were approved for market launch throughout the year: Zhixiang Jintai’s selicrelumab, Hengrui Medicine’s funakizumab, and Keymed Biosciences’ CM310 (spesolimab).All three approved drugs carry significant weight: Sipucibai is the first domestically developed and the second globally launched IL-4R antibody drug, while Sailiqi and Funaqizhu were both approved on the same day, jointly becoming the first domestically produced IL-17A monoclonal antibody drugs.。

Beyond approved products, domestically developed autoimmune drugs are demonstrating even stronger momentum in the R&D pipeline,Multiple Key Targets Are Set to Enter a Period of Intensive Clinical Readouts。

Figure 4. Progress in the Development of Domestically Produced IL-4R-Targeted Drugs (Phase III Clinical Trials and Above)

Figure 4. Progress in the Development of Domestically Produced IL-4R-Targeted Drugs (Phase III Clinical Trials and Above)

Taking the IL-4R monoclonal antibody as an example, in addition to the already marketed dupilumab,Currently, there are still 8 domestically produced IL-4R monoclonal antibodies in Phase III clinical trials., including Akeso’s mandokimab, Hengrui Medicine’s SHR-1819, Zhixiang Jintai’s GR1802, and 3SBio’s SSGJ-611. This means that domestically produced IL-4R monoclonal antibodies will be intensively launched in the next 1–2 years, posing a strong challenge to the blockbuster drug dupilumab, which generates billions in revenue.

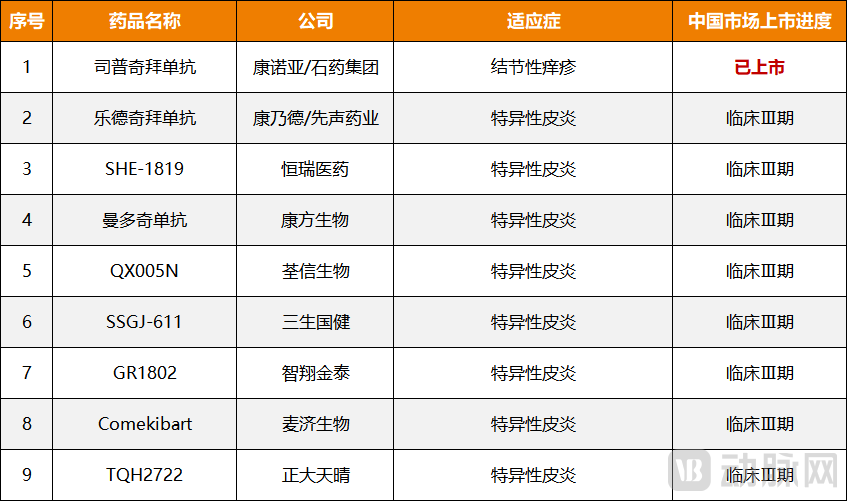

Figure 5. Progress in the Development of Domestic IL-17A Targeted Drugs (Phase III Clinical Trials and Above)

Figure 5. Progress in the Development of Domestic IL-17A Targeted Drugs (Phase III Clinical Trials and Above)

Compared with IL-4R, competition among IL-17A monoclonal antibodies is more intense, and correspondingly, Chinese manufacturers are exerting greater efforts. On one hand, domestic drugs have secured two of the six marketed IL-17A monoclonal antibody products; on the other hand, from the perspective of the clinical pipeline,Currently, more than 10 IL-17A monoclonal antibodies have entered Phase III clinical trials in China., primarily involving leading companies such as Akeso, Bio-Thera Solutions, and Junshi Biosciences. It is evident that domestic IL-17A monoclonal antibodies are currently in a strong position to “encircle” overseas pharmaceutical companies.

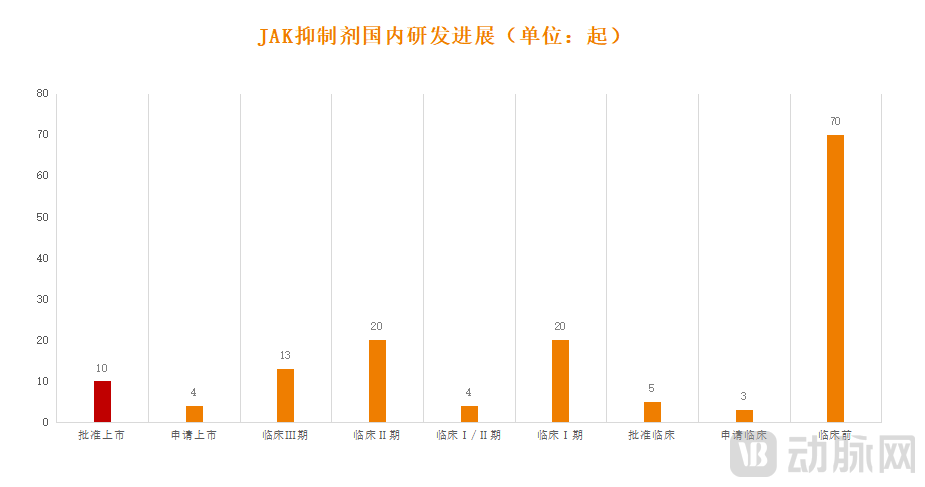

Figure 6. Progress of JAK Inhibitor R&D in China (Data source: Insight database)

Figure 6. Progress of JAK Inhibitor R&D in China (Data source: Insight database)

Having discussed the interleukin antibody family, we now turn our focus to another key target in the autoimmune field: JAK inhibitors. According to statistics from the Insight database, Currently, there are four JAK inhibitors in the NDA stage in China, with more than 50 others under development, of which 13 have entered Phase III clinical trials.Among these, Dizal Pharmaceutical’s golidocitinib is in the first tier and was officially approved for market launch in June 2024. Notably, golidocitinib is the world’s first and only novel drug targeting the JAK/STAT pathway for the treatment of relapsed or refractory peripheral T-cell lymphoma (r/r PTCL), breaking through the clinical treatment bottleneck in this field.

Domestic JAK inhibitors in the second tier include Hengrui Medicine’s itacitinib and Zelixir Pharma’s garsocitinib, both of which are currently at the stage of filing for market approval. Specifically, itacitinib has submitted marketing applications for four indications in China, three of which are expected to be approved in the first half of this year; meanwhile, garsocitinib has multiple indications already in Phase II clinical trials or beyond. It is foreseeable thatDomestically Produced JAK Inhibitors, Experiencing Rapid Growth, Are Poised for Significant Volume Expansion Within the Next Three Years。

And as multiple drugs have reached the stage of marketing application or late-stage clinical trials, this unequivocally demonstrates:Domestic autoimmune disease therapeutics are entering their moment.,The market landscape dominated by imported drugs has been broken one by one.。

Surrounded by Giants, Domestic Firms in Fierce Competition: How Can Commercialization Break Through?

In fact,The current wave of approvals for domestically developed autoimmune drugs is merely the prologue; the ensuing commercialization battle will be the ultimate litmus test of their success.。

According to Frost & Sullivan’s projections, the domestic autoimmune disease drug market in China will grow to $19.9 billion by 2030, with a compound annual growth rate (CAGR) of 27.2%. Faced with such a lucrative market, competition among future products will undoubtedly become increasingly fierce, particularly for domestic autoimmune disease pharmaceutical companies.It must not only contend with fierce challenges from foreign giants but also face intense domestic competition among local peers.。

So, how can one truly stand out?

First and foremost, it is essential to maintain a pricing advantage.. In fact, autoimmune diseases are referred to as “immortal cancers.” Conditions such as ankylosing spondylitis and systemic lupus erythematosus are typically not directly fatal but are difficult to cure completely, requiring patients to take medication long-term or even for life. Consequently, patients are particularly sensitive to drug prices.

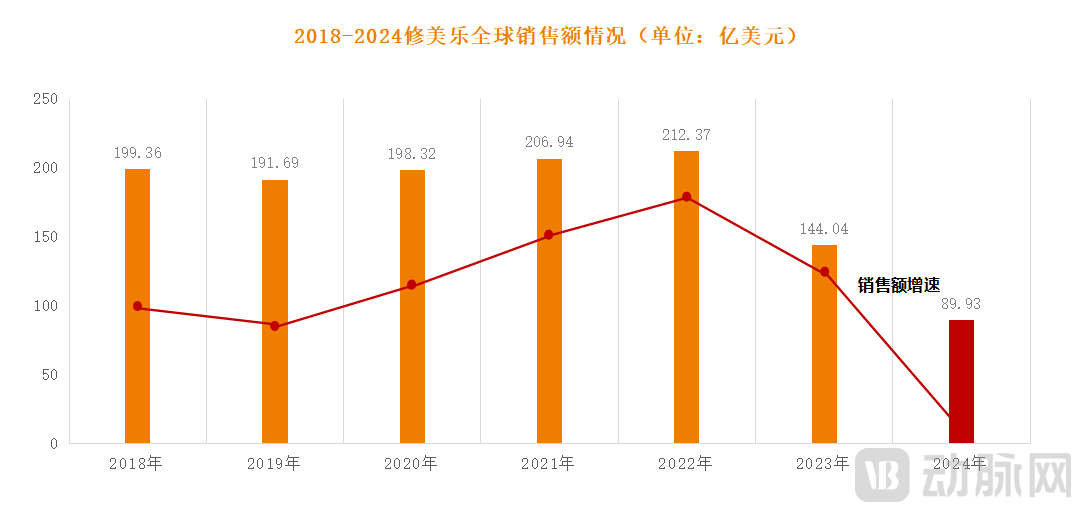

Figure 7. Global Sales of Humira from 2018 to 2024 (Source: Public Data)

Figure 7. Global Sales of Humira from 2018 to 2024 (Source: Public Data)

Taking Humira’s struggles in the Chinese market as an example, the drug entered China as early as 2010, but its sales performance remained lackluster. Its peak annual revenue reached only RMB 27 million and continued to decline. The primary reason for this was its high pricing; for the first nine years after approval, Humira maintained a price of RMB 7,600 per injection, resulting in an annual treatment cost of nearly RMB 200,000 for patients. Although the price dropped to RMB 1,290 per injection after being included in the National Reimbursement Drug List, it was too late. Competing interleukin antibodies had already gained significant market traction, further eroding Humira’s market share.

This undoubtedly serves as a wake-up call for domestically developed innovative drugs for autoimmune diseases. In the current market landscape, only by offering “high-quality products at affordable prices” can companies remain competitive. Consequently, participating in the National Reimbursement Drug List (NRDL) negotiations—trading price for volume—has become a common strategy.This is partly because the current penetration rate of the autoimmune disease market is low, with less than 30% of domestic patients seeking medical care. Inclusion in the National Reimbursement Drug List (NRDL) can rapidly expand coverage to lower-tier markets and improve drug accessibility. Furthermore, from a perspective of stable revenue generation, autoimmune diseases are comparable to chronic conditions; thus, NRDL inclusion opens up greater growth potential.

Secondly, it is essential to expand the indications as broadly as possible.. Unlike tumors, autoimmune diseases exhibit comorbidity rates; a single innovative drug can target more than 10 indications. Therefore, once the first indication is approved, it has the potential to become a blockbuster. Hence,Autoimmune diseases have always been conquered by targeting specific indications.Taking dupilumab as an example, its rise to become the new generation’s leading autoimmune drug is primarily driven by the rapid expansion of its indications. It has currently received approval for seven indications, and this momentum continues to accelerate.

This holds true for domestically produced drugs as well; only by securing approval for more new indications can they gain a firm foothold in the fiercely competitive market. 3SBio has long recognized this. After shifting away from its “all-in” strategy in oncology to focus on autoimmune diseases, it now boasts the most comprehensive pipeline within the IL family. The company has established a presence in high-prevalence indications such as chronic obstructive pulmonary disease (COPD), atopic dermatitis, asthma, and psoriasis, with its development progress ranking among the top three among domestic competitors, thereby clearly securing a first-mover advantage.

Finally, in terms of differentiation. As is well known, the development of domestically produced autoimmune drugs in China started relatively late, and the market has long been monopolized by foreign pharmaceutical companies. Therefore, to compete with them, or even to overtake them on a curve, it is necessary not only to offer more competitive pricing but also to achieve differentiation. Taking IL-17A monoclonal antibodies, which face the most intense competition, as an example, Chinese manufacturers have made significant efforts. Secukinumab from Zhixiang Jintai adopts a fully human IgG4 antibody format, exhibiting higher affinity and stronger activity. Meanwhile, Funakizumab, approved around the same time, has expanded its indications beyond psoriasis to include psoriatic arthritis, lupus nephritis, Graves' ophthalmopathy, and axial spondyloarthritis.

In response, a pharmaceutical company executive stated, “For autoimmune diseases, the future directions for differentiation of mature targets include, on one hand, further reducing dosing frequency and extending the dosing interval; on the other hand, modifying the dosage form to improve patient adherence and market penetration.In addition, emerging targets such as TSLP, OX40, and TL1A also warrant close attention. A differentiated strategic deployment can not only prioritize gaining favor from major pharmaceutical companies but also significantly enhance the likelihood of driving marketed drugs to profitability, thereby creating a virtuous cycle.”

It can be said that, at present, with the continuous increase in the number of novel biologics, their market penetration rate, and their coverage under medical insurance schemes,Domestic autoimmune drugs are clearly riding the wave of a golden era of development.But ultimately, who will stand out depends on hard-core capabilities. However, what is certain is that at a time when multiple disease areas have become extremely saturated and pharmaceutical companies are gradually feeling exhausted, the new narrative of “autoimmune diseases” has clearly attracted more attention from Chinese pharmaceutical companies, and those “early movers” are expected to be the first to reap market dividends.

1. “The Multi-Billion-Dollar Autoimmune Disease Sector Ignites! What Kind of Chinese-Made Blockbuster Drug Do We Need?” — E-Drug Manager;

2. “The Long-Established Leader in Autoimmune Diseases Is Way Ahead of Its Time” — Archimedes;

3. “When Domestic Autoimmune Drugs Tore Open a Gap” — Yaozhi.com.