Genuine Biotech Makes Second Attempt at HKEX IPO Amid Heavy Reliance on Azvudine

Genuine Biotech

Innovative Drug Developer

2Month18Day, Genuine Biotech HK StocksIPOThe application has been accepted, and the prospectus has been officially disclosed. It is reported that Genuine Biotech previously2022Year8Genuine Biotech submitted its initial listing application to the Hong Kong Stock Exchange (HKEX) in [Month], which later lapsed after failing to pass the hearing within six months. This marks Genuine Biotech’s second attempt to list on the HKEX. As the halo effect of its blockbuster COVID-19 drug fades, will the capital market remain willing to back innovative pharmaceutical companies that are not yet profitable? Can a single new drug sustain aIPO?

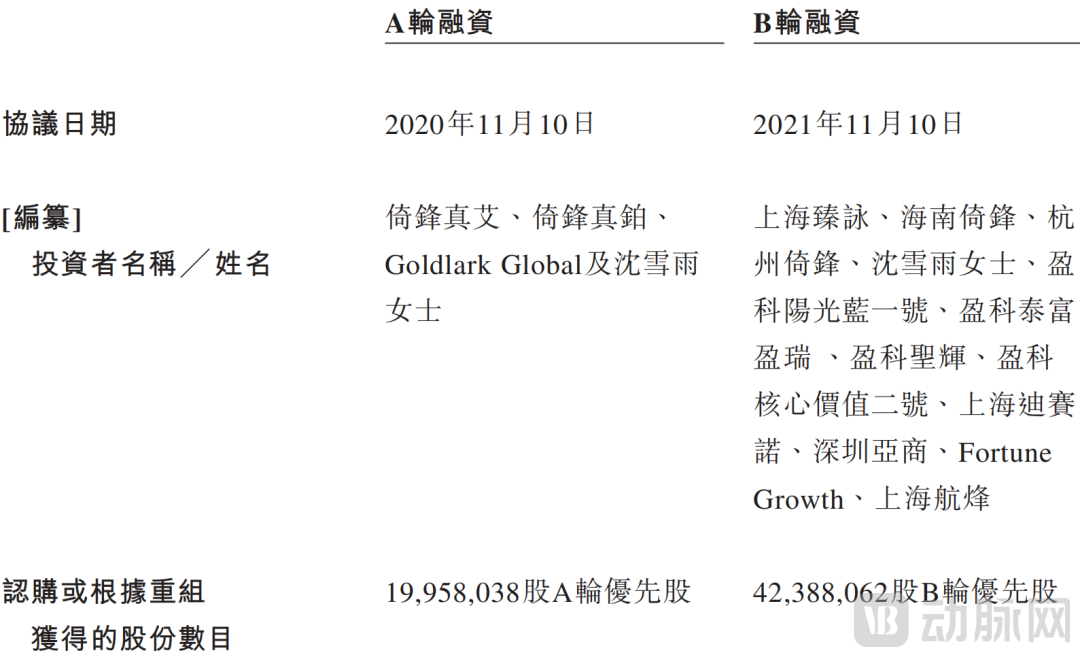

Genuine Biotech, established in September 2012, has demonstrated a noteworthy journey in the capital markets. From 2021 to 2022, the company completed two rounds of financing, raising a total of RMB 712 million. Investors included Jinbailin Investment, Yifeng Capital, Yingke Capital, Yashang Capital, Fuqiang Financial, and Shanghai Desano Pharmaceutical Co., Ltd., among others. Following the completion of its Series B financing round in 2022, the company’s post-money valuation reached RMB 3.56 billion.

Source: Prospectus

30 100 million tabletsGMP Capacity Boost Drives Gross Profit into Positive Territory,Net Loss Narrows

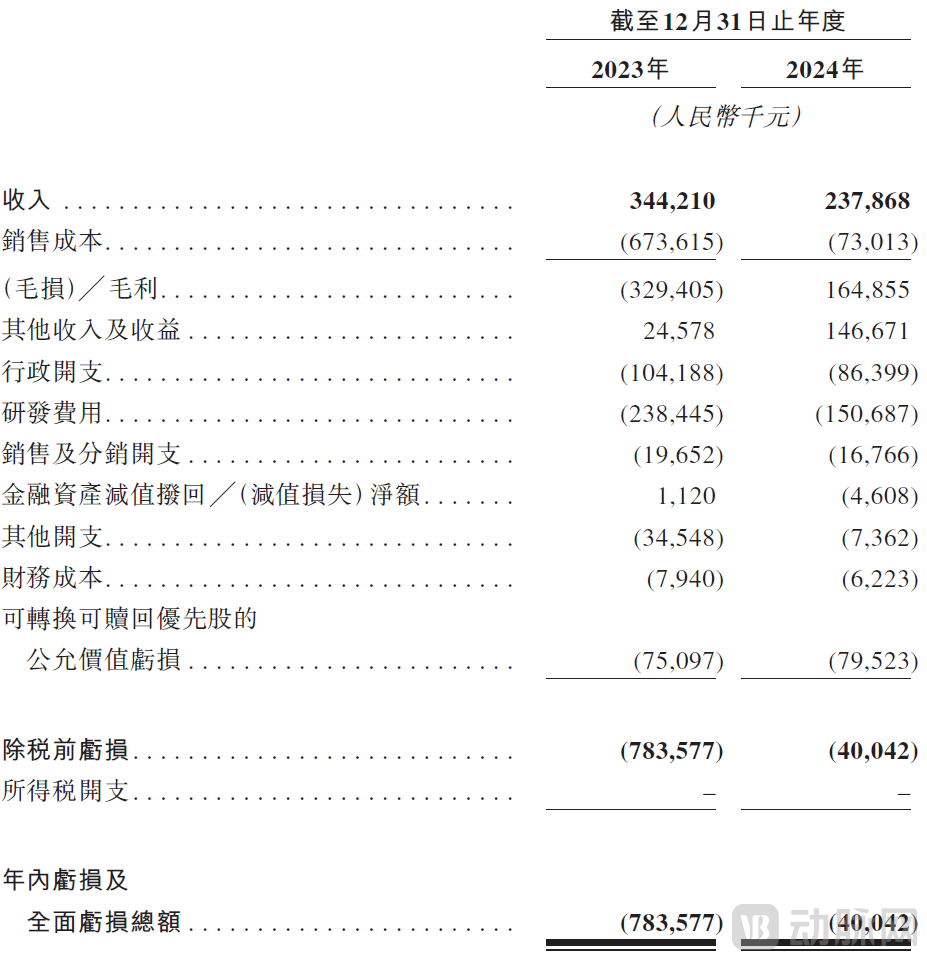

According to the prospectus, Genuine Biotech’s revenue in 2024 amounted to RMB 238 million, representing a year-on-year decrease of 30.9% from RMB 344 million in 2023, with revenue primarily derived from the company’s core product, azvudine.

Revenue Data Source: Prospectus

As the world’s only dual-target oral nucleoside drug approved for the treatment of HIV, Azvudine is undoubtedly Genuine Biotech’s flagship product.

Azvudine is a pyrimidine nucleoside drug that received conditional approval in July 2021 for the treatment of HIV-1-infected patients aged 18 years and older with high viral loads (HIV-1 accounts for more than 90% of all HIV infections globally). Its post-marketing Phase III clinical trials are expected to be completed in the second half of 2025.

Following the onset of the global pandemic in 2020, Genuine Biotech initiated clinical studies to evaluate the efficacy of azvudine in treating COVID-19. In July 2022, azvudine, as a Class 1.1 innovative new drug, received conditional marketing approval from the National Medical Products Administration (NMPA) for the treatment of COVID-19, becoming the first oral antiviral drug developed by a Chinese company and approved by the NMPA for this indication.

In 2023, Azvudine was included in the National Reimbursement Drug List (NRDL) and successfully renewed its contract in 2024. The stable reimbursement scope and pricing have provided strong support for the product’s market promotion and sales. Currently, Azvudine has reached over 50,000 medical terminals across 31 provinces and municipalities in China, establishing a broad market foundation. The approval of new indications eliminates the need to repeat hospital access procedures, significantly enhancing the product’s market competitiveness.

Leveraging its inclusion in the National Reimbursement Drug List and its channel advantage covering 50,000 medical terminals, the drug contributed 94.4% of Genuine Biotech’s royalty income in 2023–2024.

However, as pandemic-related demand subsided, the company’s revenue declined by 30% in 2024, exposing Genuine Biotech’s risk of overreliance on a single product. According to its prospectus, the company incurred a loss of RMB 784 million in 2023. Although the loss narrowed significantly to RMB 40.04 million in 2024, the pressure from its RMB 140 million cash reserve against total liabilities of RMB 410 million remains considerable.

Notably, the company’s gross profit turned positive, shifting from a gross loss of RMB 330 million in 2023 to a gross profit of RMB 160 million in 2024, while its gross margin improved from -96.2% to 67.2%. The significant narrowing of net losses also reflects enhanced production cost control and bargaining power. The company attributed this improvement to the economies of scale derived from its 3-billion-tablet GMP-compliant production capacity, as well as a reduction in the selling expense ratio from 58% to 34% following national medical insurance reimbursement negotiations.

According to the prospectus, Genuine Biotech has established its own GMP-certified production facilities with an annual capacity of approximately 3 billion tablets, which can fully guarantee product supply and meet current commercialization demands. Meanwhile, the company has built a professional commercialization team and a comprehensive management system, completing its online and offline channel layout. In the future, leveraging its 3-billion-tablet GMP production capacity and professional commercialization team, the expansion of its product portfolio is expected to unlock new growth drivers.

How Much Room for Imagination Is There in the Antiviral Drug Market?

HIV is a virus that primarily attacks and destroys CD4+ T cells of the immune system, making patients susceptible to infections and other diseases. The course of HIV infection is divided into four stages: acute infection, latent period, pre-AIDS, and late-stage AIDS.

Based on genotypic differences, HIV can be classified into two major viral types: HIV-1 and HIV-2, with HIV-1 accounting for more than 90% of global HIV infections. Currently, there is no cure for HIV infection, but disease progression can be suppressed or slowed through pharmacological treatment.

The prospectus shows that the market size of HIV drugs in China and globally has continued to grow, increasing from $35.3 billion in 2018 to $43.1 billion in 2023, with a compound annual growth rate (CAGR) of 4.1%. It is expected to grow at a rate of 4.7%, reaching $59.5 billion by 2030.

In recent years, newly approved cART drugs with improved efficacy and safety have become the most widely used HIV medications globally. However, the majority of HIV drugs in the Chinese market are single-agent antiretroviral drugs, rather than the combination formulations containing multiple ART agents that are more readily available in developed markets.

As a backbone NRTI agent, azvudine plays an irreplaceable role in cART combination therapy. Clinical trials have demonstrated that when used in combination with DTG (an integrase inhibitor), it achieves a viral suppression rate of 98.3%, representing a 12-percentage-point improvement over conventional regimens.

As the market size for HIV drugs expands, demand for azvudine is expected to continue rising. However, significant challenges remain, such as Gilead’s Biktarvy, which generates over $7 billion in annual global sales, and Merck & Co.’s long-acting formulation of islatravir, which is poised for imminent launch.

In the face of patent barriers erected by multinational pharmaceutical companies, Genuine Biotech has adopted a differentiated strategy: on one hand, it is deepening the expansion of azvudine’s indications in areas such as hematologic malignancies (CTCL); on the other hand, it is entering fields of high-prevalence diseases with Chinese characteristics, such as liver cancer, through the development of combination therapies.

Regarding the company’s future development, Du Jinfa, Chairman of Genuine Biotech, stated that in 2025 the company will continue to focus on the research and development of original drugs, promote source innovation in pharmaceuticals, enhance clinical development capabilities and efficiency, and more effectively advance the clinical studies and regulatory registration of innovative drugs. Currently, multiple R&D projects are underway.

Building a Five-Pillar Anti-Tumor Drug Portfolio to Establish Long-Term Competitiveness

In the field of oncology, Azvudine demonstrates broad-spectrum antitumor activity. It is the only nucleoside analog antitumor drug developed in the past 30 years that features a dual mechanism and high selectivity, exerting its dual antitumor effects by inhibiting DNA synthesis in tumor cells and modulating immune system function.

Currently, Genuine Biotech is developing the Azvudine/anti-PD-1 combination therapy for the treatment of liver cancer and colorectal cancer, Azvudine/Dorastinib for non-small cell lung cancer, and Azvudine monotherapy as well as Azvudine/CTX for hematologic malignancies.

Company Product Pipeline (Source: Prospectus)

Company Product Pipeline (Source: Prospectus)

Beyond Azvudine, Genuine Biotech has actively built a multi-target anti-tumor pipeline, including EGFR inhibitors, STING agonists, ENPP1 inhibitors, TOPO1 inhibitors, and PSMA ADCs. Several of these R&D projects have entered clinical stages. In the coming years, the company will validate the efficacy of its drugs through extensive clinical trials and further expand into international markets.

Among them, the EGFR inhibitor (Duoxitinib) is a third-generation TKI drug targeting non-small cell lung cancer, capable of overcoming the T790M resistance mutation. Preclinical data demonstrate excellent penetration into brain metastases, and it is currently in Phase I clinical trials.

STING agonist (CTX-009) enhances anti-tumor activity by activating the innate immune response and is currently undergoing clinical trials in combination with PD-1 inhibitors for the treatment of solid tumors.

ENPP1 Inhibitor (DB-001): A Novel Therapy for Metabolically Dysregulated Tumors, Demonstrating Significant Tumor Growth Inhibition in Breast Cancer Animal Models

TOPO1 Inhibitor (DX-102): An Improved Chemotherapeutic Agent Based on Camptothecin Analogue Structure, with Approximately 50% Enhanced Safety Profile Compared to Similar Products

PSMA ADC (DB-301) is a prostate cancer-targeted therapy that employs novel linker technology for precise delivery, achieving an industry-leading drug-to-antibody ratio (DAR) of 4.0.

Regarding the use of proceeds from this IPO, the prospectus indicates that funds will be allocated to: (i) the research and development and commercialization of the Company’s core product, Azvudine, for the treatment of HIV infection, certain hematologic malignancies, and solid tumors; (ii) the research and development of combination therapies involving Azvudine and the Company’s other candidate products for the treatment of HIV infection and certain oncology indications; (iii) the research and development of the Company’s other drug candidates; (iv) further enhancement of the Company’s R&D platform; and (v) working capital and other general corporate purposes.

It has become inevitable for innovative pharmaceutical companies to transition from relying on a single blockbuster drug to adopting a platform-based model. At present, Genuine Biotech stands at a typical crossroads in the development of innovative biopharmaceutical enterprises: while bolstered by the prestige of its first-in-class novel drug, it also faces the growing pains associated with dependence on a single product. The success or failure of its IPO on the Hong Kong Stock Exchange may serve as an important benchmark for the transformation pathways of Chinese biotech companies.