From Doubling to Halving: Data Remains the Key to AI Healthcare Takeoff

Tempus

Precision Medical Technology Researcher

OpenEvidence

Medical Artificial Intelligence Technology Researcher

AI in healthcare has never been as vibrant as it is today. According to incomplete statistics, the DeepSeek large language model has been deployed in nearly 90 top-tier tertiary hospitals (Grade 3A) across China, many of which are locally renowned. Over the past month, stocks of Chinese AI healthcare companies have risen collectively, while across the Pacific, U.S. medical AI firms, led by the AI precision medicine company Tempus AI, have experienced a surge.

It was not long ago that IBM Watson Health, a “pioneer” in AI healthcare, exited the race, and AI healthcare had yet to enter the mainstream spotlight last year. Has the era of AI healthcare suddenly arrived?

Tempus AI went public only last year. Its stock price nearly tripled in January this year, surging from a low of $30 to over $90 per share, before plummeting back to the $50s in recent days. The intense attention surrounding this stock stems not only from the fact that it is an AI company long favored and heavily invested in by Pelosi, but also from the vast and compelling vision it presents for AI in healthcare.

Daily Candlestick Chart of Tempus AI Stock Price, Source: Baidu Stock Connect

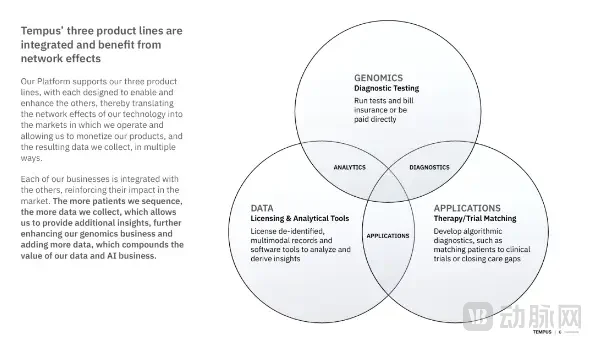

Tempus AI currently offers three distinct product lines: genomics, data, and AI applications.

GenomicsThis is Tempus’s core business, which launches a series of products in the field of oncology diagnosis through gene testing-related services, including tumor tissue gene sequencing and liquid biopsy. As an entry point for data and traffic, gene testing products generate a continuous stream of molecular data through a comprehensive intelligent diagnostic system, thereby driving the growth of its other two product lines.

Data ServicesIn addition to its genomic sequencing business, Tempus has entered the medical imaging sector through its acquisition of Arterys. As of November 2024, its database contained over 250 petabytes (PB) of multimodal data, comprising 1.2 million imaging datasets, more than 1.1 million sample sequencing datasets, and over 250,000 “DNA+RNA” feature datasets. These data are integrated into two core products, Insights and Trials, which provide data services and AI-driven R&D tools to support drug discovery and development for life sciences companies. This segment also represents Tempus’s fastest-growing source of revenue.

AI ApplicationsFocuses on developing and delivering AI-driven CRO services, clinical trial services, and building and deploying clinical decision support tools. Essentially, it provides AI tools to various stakeholders in the healthcare sector through data- and algorithm-based software.

The main products in this series include Next (care, facilitating information exchange between physicians and patients and managing treatment pathways), Algos (algorithms, leveraging deep learning to evaluate biomarkers and assist physicians in determining the suitability of chemotherapy or targeted therapies), One (AI assistant, utilizing AI-aided analysis of patient data to provide rapid recommendations for personalized treatment plans), Hub (management station, enabling physicians or researchers to access and manage patient diagnostic data via mobile devices or computers), Lens (data analytics, responsible for presenting aggregated data and visualizations to researchers to facilitate population-level or individual-level studies), Pixel (AI imaging, AI-based diagnosis of imaging data and tracking of longitudinal changes), and Assays (precision medicine, covering various sequencing methods, including whole-exome sequencing, RNA sequencing, and liquid biopsy).

Three Products of Tempus AI

Tempus is one of the few AI healthcare companies with its own “business flywheel,” consistently structuring its precision medicine strategy around the cycle of “data–analysis–diagnosis–service.”

Specifically, its growth strategy begins with a focus on expanding its hospital network. It provides clinicians with genetic testing and data analytics tools while simultaneously collecting valuable patient data. Furthermore, it actively collaborates with additional healthcare institutions to promote the adoption of sequencing technologies.

Building on this foundation, they sell data services to pharmaceutical companies, which not only assist in the precise selection of clinical trial populations but also uncover the potential of new drugs, thereby laying a solid financial groundwork for future collaborations with pharmaceutical enterprises.

With the expansion of database scale and advancements in algorithmic capabilities, the company continues to develop new AI-powered products, ranging from intelligent pathological diagnosis to primary tumor site identification, thereby progressively penetrating a broader array of clinical scenarios. Meanwhile, it has expanded its focus from oncology to other disease areas, including cardiovascular diseases and rare disorders, unlocking the value of technology and data across more applications. Finally, through a global strategy, the company has partnered with leading medical institutions in North America, Europe, and Asia, further broadening its data sources and enhancing its industry influence.

It is precisely this end-to-end strategy, encompassing data collection, analytical modeling, diagnostic services, and commercial partnerships, that has driven the company’s sustained high-speed growth in the field of precision medicine. Over the past two years, the surge in AI computing power and a significant reduction in diagnostic costs have made the collection, access, and integration of massive medical datasets more efficient, while also enabling complex horizontal and vertical data analysis. This technological advancement has provided strong support for accelerating growth.

Tempus AI’s projected annual revenue for this year is approximately $1.23 billion, representing a year-over-year growth of more than 75%.

In the primary market, another healthcareAI Rising Star OpenEvidence Just Completed $75 Million in Funding, led by Sequoia Capital, propelling the company’s valuation to surpass $1 billion. Founder Daniel Nadler previously established Kensho, a financial data company that was sold to S&P for $700 million in 2018. In 2021, he self-funded the creation of OpenEvidence, focusing on developing AI assistants for physicians.

OpenEvidence adopts a freemium model, generating revenue through advertising and primarily acquiring users via word-of-mouth referrals within hospitals. Pat Grady, a partner at Sequoia Capital, pointed out that this organic growth model is extremely rare in the healthcare industry and is typically seen only in internet-based products.

Currently, OpenEvidence has established a partnership with The New England Journal of Medicine and plans to expand its portfolio of medical journal resources this year. This round of funding will be primarily used to optimize AI algorithms and broaden the network of medical data partners.

The prominence of companies at two different stages once again underscores:The Foundation of Medical AI Is Data。

Tempus AI, in particular, has been collecting data in the healthcare sector for many years, making it difficult for other U.S. AI healthcare companies to catch up in the short term. It has established partnerships with more than 200 biopharmaceutical companies, connecting 65% of academic medical centers and 50% of oncologists in the United States. With 8.5 million clinical records, 1.2 million imaging records, and 250 petabytes (PB) of multimodal data, Tempus has built a strong core competitive barrier. In November 2024, Tempus acquired Ambry Genetics, a genetic testing company with a 25-year history, gaining access to additional valuable data and expanding its business into pediatrics, rare diseases, immunology, reproductive health, and cardiology.

“It is often said that the healthcare industry generates the most data, seemingly making it a perfect match for AI.”

Yet reality is fraught with challenges—the healthcare sector suffers from a severe shortage of affordable, high-quality training data that is both efficient and readily usable. The issues involved are not only highly technical but also tedious, and project cycles are often protracted, making the entire industry far from “sexy” in the eyes of the tech innovation community.

In Season 1 of “Silicon Valley,” there is a classic scene in which every tech startup in Silicon Valley displays the same bold slogan: “Make the World a Better Place.” Yet on the unique battlefield of AI + healthcare, an additional caveat may be needed: “Make the World a Better Place, Subject to FDA Approval Timelines.”

Even the smallest change in the healthcare industry requires coordinating a staggering number of stakeholders, navigating layers of regulatory approval processes, and bridging a long time gap before achieving true profitability.Through direct engagement, it becomes evident that physicians do not expect large language models to work miracles in curing cancer. Their more pragmatic expectation is whether such models can help automate the processing of Category C procedural reports involved in Step B of Class A surgeries. These genuine needs can only be fully appreciated through long-term, in-depth immersion in the industry and a thorough understanding of clinical workflows.

Therefore, in such a complex industry, it is crucial to promote data circulation through authoritative standards or policies.

In the United States, FHIR (Fast Healthcare Interoperability Resources) and HL7 standards have been widely adopted to ensure the interoperability of healthcare data across different institutions. Standardized data facilitates the seamless integration of AI technologies in healthcare, driving the implementation of applications such as medical imaging analysis and computer-aided diagnosis. Europe is also promoting healthcare data interoperability by establishing similar standards.

In contrast, the standardization of medical data in China is still evolving, but a key turning point occurred at the end of last year: Xuanwu Hospital of Capital Medical University, in collaboration with the Beijing International Big Data Exchange, successfully completed Beijing’s first public hospital data transaction. In the future, this dataset will be applied to the research and development of domestically produced carotid artery stents, helping healthcare institutions gain a more precise understanding of cerebrovascular diseases among the Chinese population.

This signals the dawn of an era characterized by the free flow of health data. Previously, for hospitals, policy-guided medical IT construction, while enhancing comprehensive competitiveness in the long term, was recorded merely as a cost on income statements in the short term. The realization of health data trading may change this landscape: by selling de-identified data at scale, hospitals can transform data governance from a cost center into a revenue stream, thereby stimulating their proactive drive to deepen informatization efforts and providing richer, high-quality resources for the data infrastructure of AI-driven healthcare.

The most significant difference in the current wave of AI in healthcare, compared to previous iterations, is likely its “systematic” nature. In other words, AI is no longer merely a standalone module or a single-function tool; instead, it is embedded within hospitals’ health information systems, enabling interconnectivity across multiple segments such as medical imaging, electronic health records, medication management, and follow-up care systems.

In fact, Chinese healthcare institutions are at a relatively advanced level in AI adoption. According to the 2024 China edition of Philips’ “Future Health Index” report, 86% of surveyed healthcare institution administrators stated that they have already deployed or plan to invest in generative AI, a proportion significantly higher than that in the United States (75%). Regarding specific application scenarios, 47% of respondents reported having deployed AI in radiology departments, 44% are applying AI for inpatient monitoring within hospitals, and 40% are using AI in medication management processes.

Despite impressive deployment rates, hospitals are primarily concerned with practical issues such as “whether it can alleviate physician shortages,” “whether it can reduce documentation burdens,” and “whether it can lower misdiagnosis rates.”If an AI product only addresses a minor pain point in the short term, or if its long-term maintenance costs are prohibitively high, hospitals will deem it not worth the investment.

At the time, one of the fatal flaws of IBM Watson Health was its lack of deep integration into clinical scenarios. It failed to align with hospital workflows or seamlessly interface with physicians’ daily operational systems, making sustained adoption difficult. Physicians require tools that are concise, user-friendly, and time-saving. In contrast, Watson’s interaction workflow imposed high demands on hospitals’ health information technology (HIT) systems and often entailed additional training costs and maintenance investments. For many healthcare institutions, mere “inconvenience in use” was sufficient to deter them from adoption.

Moreover, in promoting Watson Health, IBM tended to pursue a strategy focused on “large-scale projects and major clients.” However, given that each hospital has its own distinct management systems, levels of informatization, and budgeting processes, achieving scalable replication and implementation proved difficult. For IBM, the substantial investments required for research and development, maintenance, and customization failed to yield commensurate market returns in the short term; for hospitals, the high procurement and operational costs gave rise to hesitation. Both parties bore significant financial pressure, ultimately leading them to reluctantly halt their efforts.

The most notable example was the termination of its partnership with MD Anderson Cancer Center, where substantial investment failed to yield expected results, sparking widespread skepticism across the industry. The failure of this “flagship project” had a strong demonstrative effect, directly undermining commercial confidence in IBM Watson within the healthcare sector and leading other potential partners to reserve judgment on the feasibility of its technology.

Unlike the Watson era, the current market has seen the emergence of numerous enterprises capable of harnessing massive datasets, uncovering deep-seated value, and delivering diverse solutions. The application of AI in healthcare has long transcended the single dimension of “assisted diagnosis,” expanding across the entire industry chain, including pharmaceuticals, diagnostics, patient services, and scientific research. By integrating a profound understanding of biological and clinical data, AI in healthcare has evolved from early, simple software tools into a comprehensive, interdisciplinary, multi-scenario application ecosystem.

Investment in the medical AI sector remains in its early stages, with the AI health tech industry projected to achieve a compound annual growth rate (CAGR) of 43% from 2024 to 2032. This is a market with explosive growth potential.

Nevertheless, the lessons from Watson remain thought-provoking: the market will not pay for mere concepts. Only by being firmly grounded in high-quality data and leveraging robust technological R&D to precisely address clinical needs can AI seamlessly integrate into medical workflows, thereby creating tangible value for physicians, patients, and researchers.

After all,AI in healthcare is not about “AI needing the healthcare industry to tell its story,” but rather about “healthcare needing AI to drive innovation.”

VCBeat’s VBEF Future Healthcare & Medicine Top 100 Exhibition has accompanied us for a decade, during which we have jointly witnessed the Chinese healthcare industry’s journey toward “newness.” The sector continues to surge with robust innovative power, showcasing its unique charm on the global stage. In May 2025, we will continue to uphold this mission as we host the 2025 Future Healthcare & Medicine Top 100 Exhibition in Suzhou. During the conference, we will hold the Forum on Innovative Applications of Large AI Models in Healthcare at 2:00 PM on May 9. Readers interested in AI in healthcare are welcome to scan the QR code to register for the event.