China's Pet Vaccine Market Surges Amid Economic Headwinds: Domestic Players Break Foreign Dominance via Three Strategic Paths

Research conducted at the College of Veterinary Medicine, China Agricultural University, has yielded an intriguing finding: when a country’s per capita GDP reaches $3,000–$8,000, the pet industry enters a “golden period” of rapid growth. This theory has now been nearly perfectly validated in the Chinese market.

In 2024, China’s per capita GDP reached RMB 95,700, equivalent to approximately USD 14,000. Meanwhile, the pet economy has continued to expand, with iResearch Consulting projecting that the market size will exceed RMB 345.3 billion in 2024. Looking back, as early as around 2010, when China’s per capita GDP surpassed the USD 4,000 threshold, a number of astute domestic companies recognized the significant potential of the pet economy and began establishing their presence in the pet pharmaceutical sector.

However, within the realm of veterinary pharmaceuticals, pet vaccines represent a formidable challenge characterized by high technical barriers. Achieving breakthroughs in any of the core processes—such as strain selection, adjuvant development, and process implementation—is exceptionally difficult.

For a long time, the domestic pet vaccine market in China has been dominated by international giants such as Zoetis and Merck Animal Health, which collectively held a 90% market share. However, the landscape has begun to shift in recent years. In 2023, China’s first domestically produced feline triple vaccines successfully passed the emergency evaluation by the Ministry of Agriculture and Rural Affairs and were officially launched, marking the beginning of large-scale import substitution for pet vaccines in China.

Domestic pet vaccines have demonstrated strong market competitiveness since their launch. Data from the General Administration of Customs shows that both the volume and value of imported pet vaccines have declined for six consecutive quarters. The "2025 White Paper on China's Pet Healthcare Industry" further points out that since April 2024, the market share of domestically produced vaccines has steadily risen, gradually shaking the dominant position held by foreign-funded vaccines.

Today, domestically produced pet vaccines are breaking the long-standing monopoly of foreign giants with unstoppable momentum, while the market share of imported vaccines is steadily shrinking. How will domestic substitution reshape the landscape of the multi-billion-dollar pet vaccine market?

The pet vaccine market exhibits significant counter-cyclical characteristics.Amid the current environment of insufficient consumer demand, the pet vaccine market continues to maintain high growth. Survey results indicate that in both China and other regions worldwide, when incomes drop by 20%, pet-related expenditures are among the last things most people are willing to cut.

Liu Yang, Vice President of Aichong Biologics, told VCBeat, “From a conservative perspective, the current pet vaccine market has surpassed RMB 10 billion. Among this, mandatory rabies vaccines contribute a baseline of RMB 3–4 billion, while feline triple vaccines and canine combination vaccines have formed niche markets valued at RMB 2–3 billion and RMB 2 billion, respectively, both maintaining rapid annual growth. Drawing on the development of overseas pet markets, the next five years will be a golden period for the growth of the pet vaccine industry.”

The domestic pet vaccine market is driven by two core engines of growth. First, the continuous increase in the pet population: data from the "2023-2024 White Paper on China's Pet Industry" shows that the number of cats and dogs in urban areas of China has exceeded 100 million, surpassing the number of newborns in 2024.

Second, pet owners’ awareness of disease prevention has improved. Compared with the veterinary consultation rates in developed countries in Europe and the United States, the rate in China remains relatively low, and vaccine penetration is also at a modest level. Taking the feline triple vaccine as an example, the vaccination penetration rate in China is less than 10%, indicating substantial room for market growth. In recent years, heightened awareness of disease prevention among Chinese pet owners has led more of them to vaccinate their pets to reduce the risk of illness.

In the multi-billion yuan pet vaccine market, “Miaosanduo” was once an unshakable symbol. As Zoetis’s exclusive brand of feline triple vaccines, the product has been the only officially approved feline triple vaccine in China since it received formal approval and entered the Chinese market in 2011. Before 2023, feline triple vaccines in China were synonymous with “Miaosanduo.”

This phenomenon reflects a deeper industry landscape: core pet vaccine categories, including not only the feline triple vaccine but also rabies vaccines for animals and canine combination vaccines, are similarly dominated by foreign giants such as Zoetis, Intervet, and Boehringer Ingelheim, which collectively hold over 90% of the market share.

In recent years, domestic companies have gradually made breakthroughs in core pet vaccine categories. Several domestically produced feline triple vaccines have been approved for market launch, and Chinese-made vaccines are beginning to breach the defensive barrier established by foreign competitors.

Domestic Pet Vaccine Market Landscape Data Source: Public Information, Corporate Interviews

As domestic companies achieve breakthroughs in their R&D pipelines, this foreign-dominated market is undergoing a value reassessment.

Currently, there are more than ten domestic pet vaccine manufacturers in China. Domestic entrants can be divided into two major categories: one is the traditional veterinary drug background group, represented by Ringpu Biology and Pulike; the other is the technology spillover group that has crossed over from the human pharmaceutical sector, represented by Aichong Biologics and Hisun Animal Health.

These two major camps are building competitive barriers across three dimensions: strain adaptation, process upgrading, and product innovation.

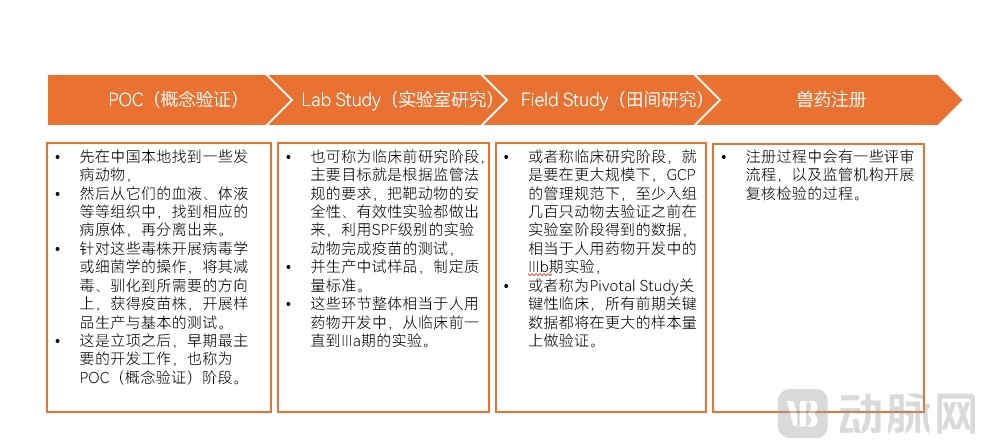

Pet Vaccine R&D Process Data Source: Matrix Partners China

Strain adaptation is a major advantage of domestically produced pet vaccines.Genetic clusters of circulating strains vary globally; when vaccine strains do not match circulating strains, vaccine efficacy is significantly compromised. Domestic pet vaccines are developed from isolated local circulating strains, ensuring higher strain compatibility.

Taking the feline triple vaccine as an example, among the three viral strains it targets, feline herpesvirus and feline parvovirus are DNA viruses that rarely undergo mutation. In contrast, feline calicivirus is a single-stranded RNA virus. During replication, the RNA-dependent RNA polymerase of RNA viruses lacks proofreading function, leading to an increased error rate and thereby significantly raising the probability of mutations. According to a report by CICC, Zoetis’ “Fel-O-Vax” feline triple vaccine uses the FCV-255 strain isolated in the United States and has not been updated for nearly a decade since its entry into the Chinese market in 2011.

Domestic vaccine manufacturers are also optimizing their production processes to enhance competitiveness.Vaccine production involves dozens of manufacturing processes, which can affect the purity and antigen content of the vaccine.

Liu Yang stated, “In the field of pet vaccine production, many overseas companies typically design their processes based on veterinary biological products intended for large livestock animals. However, pets are generally smaller in size and more sensitive to biological products, making them more prone to adverse reactions; therefore, there are higher requirements for product quality details. In terms of manufacturing processes, companies transitioning from human pharmaceuticals to pet vaccines hold a distinct advantage. Their production methods adhere to the stringent standards of human vaccines, resulting in products that are more stable and effective, with a lower incidence of side effects.”

Innovation-Driven Breakthroughs: A Pathway to Building Competitiveness for Domestically Produced Pet Vaccines, by pioneering new tracks to identify new markets. Pathways for innovation in pet vaccines include developing novel vaccines that cover new diseases, expanding vaccine coverage to more subtypes, and reducing the number of required vaccinations.

Sterilization vaccines represent a major, globally innovative product developed in China. The current method for pet sterilization is surgical sterilization, which requires anesthesia, carries potential risks of complications, and contradicts principles of animal welfare. In contrast, sterilization vaccines induce temporary infertility through bioengineering techniques, requiring only one injection per year. This approach significantly enhances convenience and reduces the cost of sterilization for pet owners.

No comparable products have been launched globally yet, while Chinese companies have taken the lead in R&D deployment. It is reported that Aiyi Animal Pharmaceuticals’ contraceptive vaccine has entered the clinical stage, and PetBio’s sterilization vaccine is expected to enter clinical trials this year.

In the cutting-edge field of mRNA vaccines, several Chinese pet vaccine manufacturers have also established their presence. In 2025, Ringpu Biology’s mRNA vaccine production line passed the static acceptance inspection for Good Manufacturing Practice (GMP) compliance for veterinary drugs, with plans to develop a quadrivalent mRNA vaccine for cats.

In terms of product competitiveness, domestic pet vaccine manufacturers can deliver impressive results. Take Aichong Biologics as an example: its inactivated rabies vaccine achieved a potency of 8.3 IU in reports from the National Reference Laboratory for Veterinary Biological Products under the Ministry of Agriculture, significantly exceeding the national standard requirement of no less than 2 IU. This performance also surpasses that of foreign-branded products. “Ruimiaoshu,” the domestically produced feline triple vaccine launched by Ringpu Biology, shipped one million doses within six months of its market debut, with first-month sales exceeding RMB 10 million.

However, in terms of distribution channels, domestic enterprises still need to break through the “iron curtain.” Foreign-funded companies continue to firmly control professional channels. The profound challenge for domestic substitution lies in whether Chinese manufacturers can secure these professional channels; currently, domestic companies still lag behind their foreign counterparts in channel capabilities.

The pet vaccine market is dominated by veterinary hospitals, with high-end chain veterinary hospitals serving as the strongholds for foreign brands. Taking Zoetis as an example, the company has established in-depth collaborations with major domestic chain veterinary hospitals such as New Ruipeng and Ruipai. Leveraging their global influence and reputation, foreign brands possess strong bargaining power within professional veterinary medical channels. In contrast, emerging domestic brands still require time to build their influence.

Industry insiders stated, “Foreign enterprises such as Zoetis have long cultivated specialized channels like professional pet hospitals and hospital chains, establishing strong, tightly integrated relationships with these institutions. In contrast, domestic companies rely more heavily on distributor channels and maintain fewer connections with professional medical institutions in China.”

There is also a gap between domestic and foreign enterprises in the maturity of their distributor networks. Multinational corporations have accumulated extensive channel management experience. Foreign-funded enterprises boast clearly defined distributor network hierarchies, standardized management practices, and professional service capabilities within their distributor networks. In contrast, Chinese enterprises have only recently begun to develop their channel infrastructure; their distributor systems remain relatively fragmented, and their distributors’ service capabilities are weaker compared to those of foreign-funded enterprises.

There is also a gap between domestic and foreign enterprises in terms of service and technical support. Foreign-funded companies can provide testing services supporting vaccines, design immunization protocols, and engage in training interactions with veterinarians. Through these educational and training initiatives, they embed their product philosophy within the veterinary community, thereby driving continuous growth in pet medication usage and enhancing stickiness with veterinarians. In contrast, interactions between Chinese pet vaccine manufacturers and veterinarians often remain limited to the level of product sales.

To enhance service capabilities, domestic enterprises are also striving to bridge capability gaps. By regularly organizing veterinary training sessions, clinical case-sharing meetings, and academic conferences, they are strengthening relationships with veterinarians and boosting doctors’ trust in domestically produced pet vaccines.

Finally, as the number of participants in the domestic pet vaccine market increases, price wars become inevitable. An investor once told VCBeat that the growing number of entrants into China’s pet vaccine sector has pushed the market toward intense competition.

Price wars are detrimental to the long-term development of the industry. The pet vaccine sector requires sustained R&D investment; however, reduced profits resulting from low pricing can hinder subsequent technological innovation and R&D spending, thereby undermining the industry’s long-term sustainable growth. Furthermore, cost pressures stemming from low-price competition pose risks to product quality, eroding consumer confidence in domestically produced vaccines.

While price wars may expand market share in the short term, they are a short-sighted strategy in the long run. Domestic vaccine manufacturers should focus their efforts on R&D, product quality, and supply chain capabilities, rather than engaging in cutthroat competition through price wars.

Saying Goodbye to Cutthroat Competition Does Not Mean Giving Up on Competition; Going Global Is Also a Direction for Domestically Produced Pet Vaccines.

The team at Aiyi Animal Pharmaceuticals is well-versed in the foreign registration regulations for animal vaccines in more than 60 countries worldwide. Zhu Xianzhu, founder of Aiyi Animal Pharmaceuticals, stated in an interview that, from an international perspective, China has established a high-standard regulatory framework in the field of animal vaccines. Many countries recognize qualifications such as the Veterinary Good Manufacturing Practice (GMP) certificates issued by Chinese regulatory authorities. High-quality pet vaccines developed and manufactured in China hold significant potential for global expansion. Geographically, China is well-positioned to serve multiple Asian markets, where regional epidemic strains are similar, thereby ensuring better vaccine match and efficacy.

Southeast Asia is the first destination for Chinese pet vaccine companies expanding overseas. In terms of per capita GDP, several Southeast Asian countries have exceeded USD 4,000, indicating that the regional market is in a phase of rapid growth. However, due to the lack of local pet vaccine production capacity, the supply still relies heavily on foreign-funded enterprises. Therefore, Chinese companies entering the Southeast Asian market can gain a first-mover advantage.

The pet vaccine market is characterized by the convergence of consumer and medical attributes. As the growth rate of new pet ownership in China slows, domestic vaccine manufacturers stand at a critical juncture in the upgrading of the pet healthcare industry. They face a historic choice: either become mired in the quagmire of low-price competition, depleting their capacity for innovation, or wield technological breakthroughs as their spear and service ecosystems as their shield to carve out new battlegrounds in the global market. The dawn of this industry will always belong to those enterprises that transform laboratory data into clinical trust and forge their channel weaknesses into strengths in service delivery.

References:

White Paper on the Pet Industry Exclusive Interview | 2024: How Zoetis Continues to Focus on the Chinese Market – White Paper on the Pet Industry

How to Choose the Feline Triple Vaccine? — Hayao Mengchong

Tapping into the Blue Ocean of Animal Vaccines for Over 100 Million Pets: A Conversation with the Founder of Ai Yi Animal Pharmaceuticals | [Matrix Partners China’s Low-Key Company Feature] — Matrix Partners China

CICC | Pet Economy Special Report #2: Domestic Pet Animal Health Products Break the Ice and Set Sail – CICC Insights