VISEN Pharmaceuticals, Dubbed 'Hong Kong’s First Growth & Development Biotech', Officially Listed on HKEX

VISEN

Endocrine-related Disease Treatment Drug Developer

Today, after updating its prospectus, VISEN Pharmaceuticals (VISEN), the only company listed on the Hong Kong Stock Exchange focused on endocrinology and developing long-acting growth hormone, officially made its debut on the HKEX.

As a scarce and purely focused target in the field of endocrine innovation in the current Hong Kong stock market, VISEN has continued to attract high attention from the market since its listing application, earning it the title of "the first growth and development stock in Hong Kong." VISEN is a biopharmaceutical company in the late stages of research and development, with products close to commercialization. It focuses on the endocrine field and is committed to providing First-in-Class or Best-in-Class products and treatment solutions for endocrine diseases.

In 2018, Danish pharmaceutical company Ascendis Pharma A/S (NASDAQ: ASND, hereinafter referred to as “Ascendis”), together with Vivo Capital and Sofinnova Ventures, jointly established VISEN Pharmaceuticals in Shanghai. Ascendis contributed product rights as equity, while Vivo Capital and Sofinnova Ventures provided financial support. Pursuant to an exclusive license agreement between VISEN Pharmaceuticals and Ascendis, the company is authorized to develop, manufacture, and commercialize endocrine therapeutic candidates, including lonapegsomatropin, navepegritide, and palopegteriparatide, in designated territories.

In other words, unlike the capital-driven NewCo model that has focused on overseas markets in recent years, VISEN has adopted a reverse NewCo strategy: introducing promising overseas pipelines into China and equipping them with domestic management teams to facilitate product commercialization, while the company itself will complete financing or go public in the local market.

VISEN’s market appeal stems not only from its scarcity but also from its product pipeline and impending commercial breakthroughs. The company’s marketing authorization application for lonapegsomatropin in China has been accepted by the NMPA, with commercialization imminent, and it also boasts multiple potential first-in-class (FIC) or best-in-class (BIC) candidates in the field of endocrine therapy.

Meanwhile, the healthcare sector of Hong Kong stocks began to recover. At the beginning of 2025, Hong Kong stocks embarked on a new round of gains, with the Hang Seng Index rising by 13.43% in February alone, and the Hang Seng Tech Index surging by 17.88%. Although the healthcare sector saw more modest gains, both the Hang Seng Biotechnology Index and the Hang Seng Healthcare Index showed significant improvement compared to the same period last year.

Leveraging the aforementioned advantages, VISEN has emerged as the most representative biotech company in the Hong Kong stock market following the opening of trading in the Year of the Snake, and is poised to become the first bellwether in the new issue market.

Growth Hormone: Products + Channels

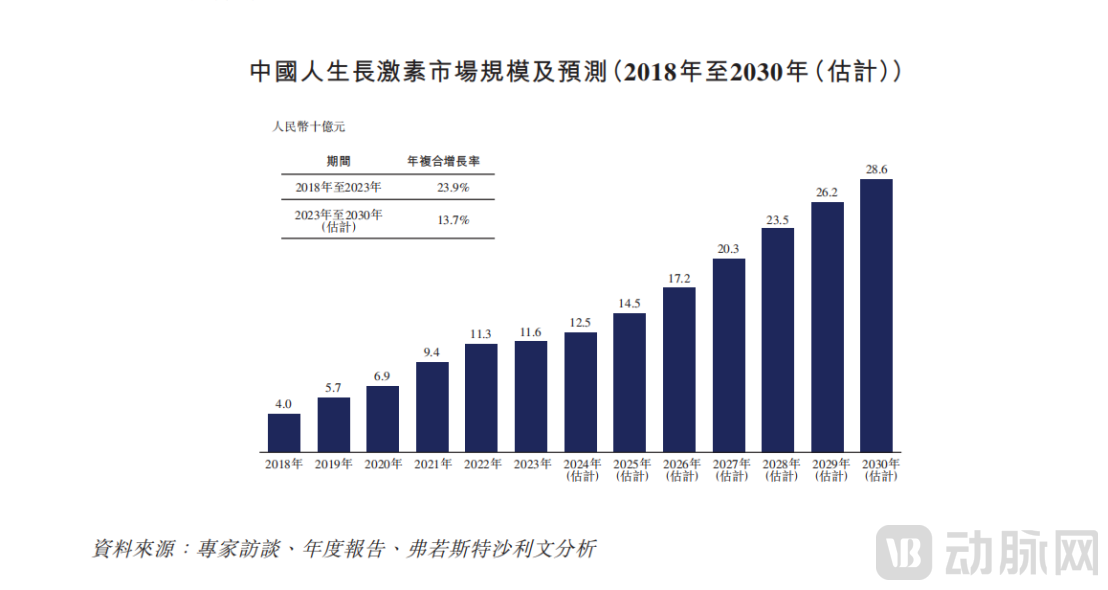

According to the "Top 100 Drugs by Hospital Sales in China" published by YaoRong Cloud, the national in-hospital sales revenue of growth hormone reached RMB 1.714 billion in 2022. Meanwhile, based on data from Changchun High-Tech, Novo Nordisk, United Cell, and Weiming Haiji, the total nationwide sales of various growth hormone products amounted to approximately RMB 12.5 billion in 2022. This suggests that the proportion of in-hospital sales of growth hormone may have fallen below 15%. However, according to a report by Frost & Sullivan, the current split between in-hospital and out-of-hospital sales of growth hormone is approximately 30:70.

However, despite the increasingly fierce competition in the growth hormone market, the real battlefield lies beyond hospitals.

First, growth hormone is a strictly controlled prescription drug with standardized indications for use. It should only be administered under the guidance of professional physicians after examinations confirm endogenous growth hormone deficiency, or upon diagnosis of idiopathic short stature, Turner syndrome, or short stature caused by growth hormone deficiency. However, despite being a prescription medication, many parents, influenced by pharmaceutical companies’ product education initiatives, proactively visit hospitals to inquire about it.

Therefore, the safety of treatment is one of the most concerned issues, including whether the formulation carries the risk of inducing tumors, other endocrine disorders, acromegaly and changes in appearance, as well as problems such as myopia.

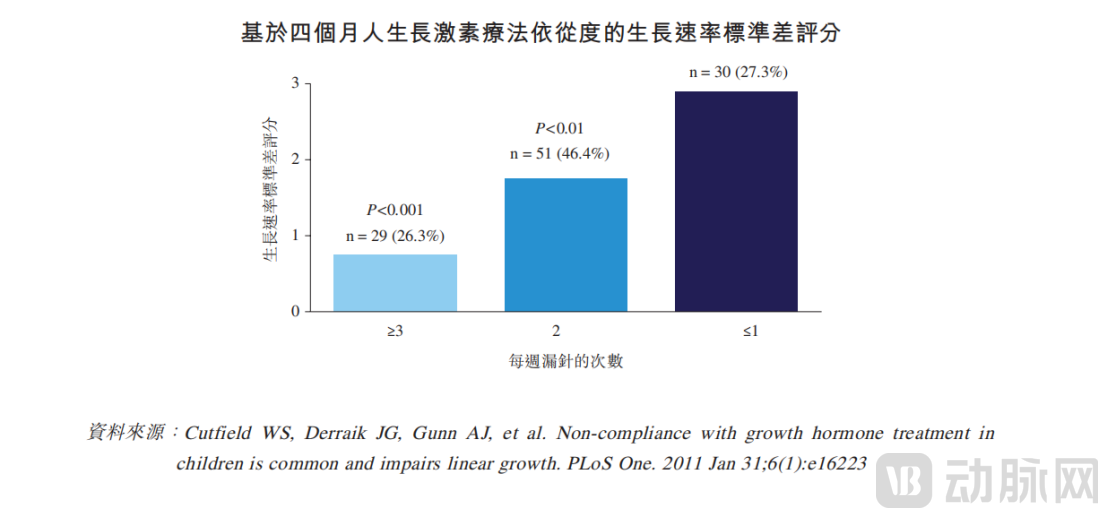

Next are the perennial issues surrounding growth hormone therapy: administration route and dosing frequency. According to Sinopharm Securities, long-term adherence to daily growth hormone formulations is poor; some patients exhibit irregular medication use or insufficient dosing during treatment, as well as premature discontinuation, thereby compromising therapeutic efficacy. Regarding dosage forms, powder formulations, which require reconstitution prior to use, are gradually being replaced by liquid formulations. In the competitive landscape for liquid formulations, the future battleground will undoubtedly be long-acting preparations.

This also explains why VISEN’s long-acting growth hormone, currently under review for market approval, is particularly worthy of attention.

Lonapegsomatropin preserves the natural bimodal mechanism of action of endogenous growth hormone by releasing unmodified human growth hormone, encompassing both direct effects on the growth plates and indirect effects mediated by IGF-1 in the liver. Leveraging this advantage, lonapegsomatropin has demonstrated a statistically significant higher 52-week annualized height velocity (AHV) compared to short-acting (daily injection) human growth hormone, potentially enabling children with pediatric growth hormone deficiency (PGHD) to achieve therapeutic goals more effectively within the limited treatment window.

Lonapegsomatropin demonstrates key pharmacological effects, including the molecular structure of the active drug, receptor-binding affinity, plasma concentration, tissue distribution, and safety profile, all of which are comparable to those of short-acting (daily injection) human growth hormone. The latter has been used by clinicians for over 30 years, engendering great confidence in its safety. In contrast, other long-acting growth hormones (LAGHs) permanently alter the molecular structure of human growth hormone, resulting in significant differences in the pharmacological properties of the new active drug molecules compared to short-acting (daily injection) human growth hormone, thereby limiting their clinical efficacy.

Compared with short-acting (daily injection) recombinant human growth hormone, lonapegsomatropin eliminates the need for injections on more than 300 days per year, which may significantly improve treatment adherence and efficacy.

Source: VISEN Prospectus

Moreover, details determine success or failure: Long-acting growth hormone can be stored for 54 months at 2–8°C, or for up to 6 months at room temperature of 30°C or below. This storage requirement is more patient-friendly compared to other growth hormone products, which typically require constant refrigeration at 2–8°C and have a shelf life of no more than 24 months. This advantage provides great flexibility for children with Pediatric Growth Hormone Deficiency (PGHD) and their caregivers, facilitating the transportation and use of the medication.

In China, growth hormone treatments are primarily paid for out-of-pocket. Given that market demand far exceeds in-hospital supply capacity, the growth hormone market has adapted to this reality with a model of in-hospital prescribing and out-of-hospital dispensing, where the latter dominates.

Although VISEN’s long-acting growth hormone has not yet been officially launched, the company has entered into a partnership with United Family Healthcare to jointly explore innovative development models aimed at enhancing pediatric growth and development services in China. VISEN emphasizes that its collaboration with United Family Healthcare is designed to advance the “diagnosis and treatment standards for disorders related to children’s growth and development in China’s non-public medical institutions,” thereby further meeting Chinese children’s demand for high-quality, diverse, and personalized healthcare services.

VISEN’s long-acting growth hormone, lonapegsomatropin, marketed under the brand name Skytrofa and submitted for marketing approval, is priced relatively high in overseas markets. For instance, in the United States, a carton containing four pens with a total dose of 9.1 mg of Skytrofa is priced at $9,198. While its domestic pricing in China remains undisclosed, the collaboration with United Family Healthcare signals that channel development needs to be prioritized earlier. Moreover, as living standards continue to rise in China, there is a broad consumer base for premium-priced pharmaceuticals and medical services.

It is worth noting that although declining fertility rates may, to some extent, affect the sales of growth hormone, its application in China has not yet been fully tapped. According to treatment guidelines and consensus recommendations, earlier initiation of growth hormone therapy yields better outcomes for children with growth hormone deficiency. However, among children actually receiving treatment in China, 70% are aged 10–13 years. Considering both treatment costs and the efficacy of growth promotion, the golden window for treating short stature is generally considered to be between 3 and 12 years of age. This indicates that a significant number of Chinese patients are either not being treated during the optimal therapeutic window or are experiencing delays in treatment.

In addition, the population of adults with growth hormone deficiency (GHD) is substantial. Adult GHD is associated with increased adiposity, dyslipidemia, cardiac dysfunction, premature atherosclerosis, reduced muscle strength and exercise capacity, decreased bone mineral density, insulin resistance, and impaired quality of life. As its symptoms are often insidious and clinical attention to diagnosis and treatment remains insufficient, it represents a significant market opportunity in the future.

Source: VISEN Prospectus

MNCs Bet Over $2 Billion on Long-Acting Platform, Beyond Growth Hormone

VISEN’s lonapegsomatropin leverages the innovative TransCon (Transient Conjugation) long-acting technology, offering the unique advantage of “native action” in its product profile. It requires only once-weekly dosing while maintaining the native structure of growth hormone as its active ingredient.

Recently, Ascendis announced that it has granted Novo Nordisk an exclusive global license to the TransCon technology platform for the development, manufacturing, and commercialization of Novo Nordisk’s proprietary once-monthly GLP-1 receptor agonist for metabolic diseases, including obesity and type 2 diabetes, as well as an exclusive license for its cardiovascular disease products. Under the agreement, Ascendis is eligible to receive upfront payments and development and regulatory milestone payments totaling up to $285 million (over RMB 2 billion).

The achievement of this authorization also affirms that, in the comparative diversity of long-acting technologies, TransCon technology stands out as a leader among global long-acting technology platforms.

The key technical barrier to long-acting formulations lies in the fact that, for protein and peptide drugs, options for extending half-life are extremely limited. Due to the complex mechanisms of tissue distribution, receptor binding, and metabolic clearance of peptide hormones in vivo, it is difficult to achieve long-acting effects without compromising efficacy and safety.

The TransCon molecule comprises three components: the unmodified parent drug, an inert carrier molecule that protects the parent drug, and a linker that temporarily connects the two. These three components combine to form a prodrug, in which the carrier molecule keeps the parent drug in an inactive state and prevents its clearance from the body. Upon injection into the human body, the active, unmodified parent drug is released in a controlled manner under physiological pH and temperature conditions. This achieves a breakthrough from short-acting to long-acting efficacy, thereby reducing the burden of disease treatment. Since the parent drug remains unmodified, its original tissue distribution and physiological effects are preserved.

The TransCon platform temporarily links carrier molecules to biologically active parent drugs via a unique linker structure. Depending on the carrier employed, TransCon prodrugs can be designed for systemic (throughout the body) or local (e.g., within tumors) action to achieve specific therapeutic objectives. Leveraging its innovative long-acting technology principle, the TransCon platform is broadly applicable to the development of protein, peptide, and small-molecule drugs across multiple therapeutic areas.

Notably, the TransCon platform not only provides an innovative solution for extending the half-life of growth hormone but also enables the development of other hormonal therapeutics. For instance, certain hormones with rapid in vivo metabolism, such as parathyroid hormone (PTH), were previously undruggable because they could not maintain stable serum hormone levels after injection, thereby precluding their use in treating related hormonal deficiency disorders (hypoparathyroidism). However, the TransCon long-acting technology platform has now resolved the druggability challenges associated with such hormonal agents.

In addition to Lonapegsomatropin, VISEN’s other two products are also built on the TransCon technology platform. They address technical challenges related to patient compliance and drug developability in endocrine therapies at different levels, establishing significant technological barriers. Clinical trial data have demonstrated that the differentiated therapeutic areas targeted by these two pipeline candidates are characterized by substantial unmet clinical needs.

Source: VISEN's Prospectus

Source: VISEN's Prospectus

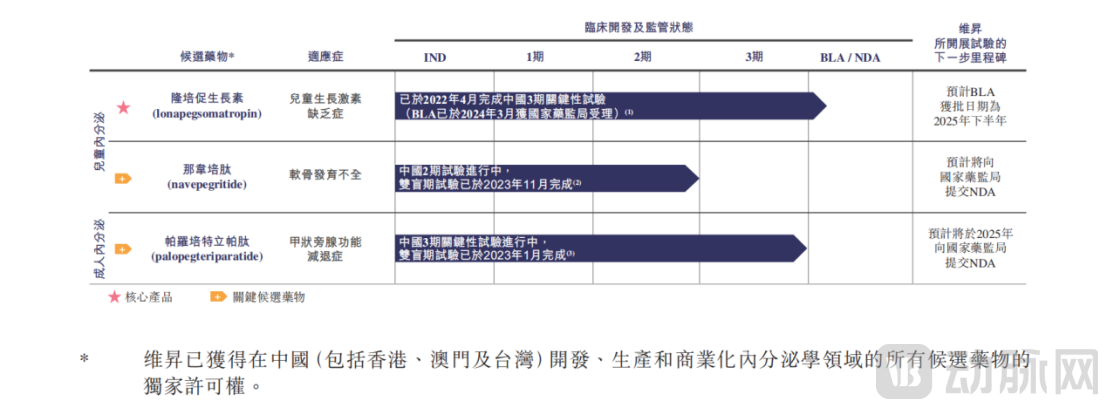

Palopegteriparatide: A Therapeutic Solution for the Treatment of Hypoparathyroidism in AdultsCurrent therapies for hypoparathyroidism are inadequate due to limited efficacy, the need for high-dose chronic calcium supplementation, and an increased risk of associated complications. Palopegteriparatide is designed to restore physiological levels and activity of parathyroid hormone over a 24-hour period, thereby addressing various aspects of the disease, including normalizing serum calcium, urinary calcium, and serum phosphorus levels.

Notably, palopegteriparatide has been launched in several European countries and is the first and only PTH hormone replacement therapy approved by the FDA for this indication. The double-blind phase of its pivotal Phase III clinical trial in China has been completed, meeting the primary endpoint.

According to Frost & Sullivan data, the number of patients with hypoparathyroidism in China was 410,100 in 2023 and is projected to reach 495,600 by 2030. Currently, as there is no approved parathyroid hormone replacement therapy for the treatment of hypoparathyroidism in China, palopegteriparatide is the only parathyroid hormone replacement therapy that has initiated clinical development in the country.

Navepegritide is a disease-modifying therapy for the treatment of Chinese pediatric patients aged 2 to 10 years with achondroplasia, whereas no effective disease-modifying therapies have currently been approved in China. Disease-modifying therapy refers to a treatment approach that delays, slows, or reverses disease progression by targeting the underlying cause of the disease. VISEN licensed navepegritide from Ascendis Pharma in November 2018. Previously, Ascendis Pharma had conducted studies on navepegritide in 45 healthy adult male subjects in a Phase I global clinical trial.

According to Frost & Sullivan data, the number of patients with achondroplasia in China was 51,200 in 2023 and is projected to reach 51,900 by 2030. Currently, there are no approved disease-modifying therapies for achondroplasia in China. Navipeptide is the first therapy for achondroplasia undergoing clinical development in China to date. Navipeptide has completed the double-blind phase of its Phase II clinical trial for the treatment of achondroplasia in China.

Commercial Monetization Imminent

VISEN’s financing trajectory is equally clear. In November 2018, VISEN secured a $40 million Series A funding round from its founding shareholders—Ascendis Pharma, Vivo Capital, and Sofinnova—bringing the company’s post-money valuation to approximately $80 million.

In January 2021, VISEN completed a $150 million Series B financing round, led by Sequoia China, with participation from OrbiMed, Sherpa Capital, Cormorant Asset Management, HBM Healthcare Investments, Pivotal bioVenture Partners, Logos Capital, Chenling Capital, and existing founding shareholders. The company’s post-money valuation was approximately $1.03 billion.

Following its successful hearing at the Hong Kong Stock Exchange (HKEX), Anke Biotechnology, a key player in China’s growth and development market, announced that it would invest up to $31 million as a cornerstone investor to subscribe for shares in the company’s initial public offering (IPO) on the HKEX.

It can be said that the “product introduction + capital infusion” model has enabled VISEN to stand on the shoulders of overseas pioneers, fully leveraging their dual advantages in funding and technology. By tailoring solutions to the needs of Chinese patients, VISEN has rapidly and steadily advanced its product development in China. This once again highlights the strategic advantages of the reverse NewCo approach: it not only maximizes the shortening of the cycle from R&D to market launch, quickly filling market gaps, but also enables preemptive positioning in competitive therapeutic areas amidst intense market competition.

Proactive strategic positioning also pertains to VISEN’s monetization capability, which is a key reason for the company’s strong recognizability in the capital markets.

The commercial monetization potential is highly certain. Growth hormone needs no further elaboration. The structural opportunity of long-acting formulations replacing short-acting ones is unlocking an incremental market worth tens of billions, and VISEN’s lonapegsomatropin is strategically positioned at this technological high ground, making future profit growth predictable.

If palopegteriparatide and navitropide can be launched first, they will undoubtedly fill the gap in the domestic market. As the exclusive rights holder in China, VISEN enjoys a significant first-mover advantage in this competitive vacuum, which will become a key variable driving the company’s performance growth.