Consumer Genomics Pioneer 23andMe Files for Bankruptcy Amid Collapse of Business Model

23andMe

Genomic Sequencing Service Provider

On the 23rd, U.S. time, prominent consumer genetic testing company 23andMe filed for bankruptcy protection and announced the immediate resignation of its co-founder and CEO, Anne Wojcicki. On the 24th, its stock plummeted 50% at the open, with its market capitalization falling to $24 million.

23andMe is one of the earliest companies to offer direct-to-consumer genetic testing services, selling direct-to-consumer personal genomics services by mailing DNA collection kits.

23andMe was founded in 2006 and went public in 2021, with its market capitalization once peaking at $6 billion. The company’s saliva-based testing kits were once highly sought after by users worldwide, and its ancestry testing service enjoyed a period of widespread popularity. Capital markets also showed strong enthusiasm for 23andMe, which completed a total of 26 funding rounds from prominent investors including Google, Illumina, Sequoia Capital US, and WuXi AppTec. Sequoia Capital US invested in 23andMe across two rounds, contributing nearly $145 million.

However, in the nearly ten years since its founding, 23andMe has never been profitable, accumulating losses of over $2.3 billion. As of December 31, 2024, 23andMe’s cash and cash equivalents totaled only $79.4 million.

Prior to this bankruptcy protection filing, 23andMe had attempted privatization and sought acquisition in 2024, but both efforts were unsuccessful.

23andMe Has a World-Class Management Team, and Co-Founder Anne Wojcicki Is the Ex-Wife of Google’s Founder. Why Did This Former Star Company and Investor Darling Fall from Grace?

Industry insiders believe that 23andMe’s downfall was inseparable from the fatal flaws inherent in the industry itself. From peak prominence to bankruptcy, 23andMe stumbled into five major pitfalls.

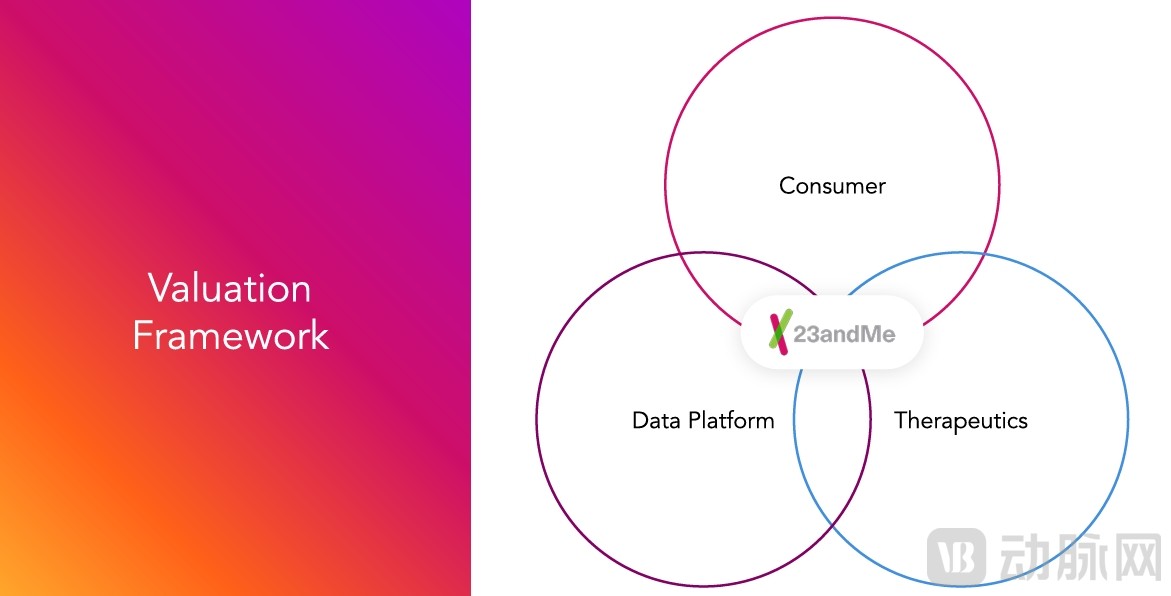

In 23andMe’s vision, its consumer business, data platform, and drug development are three mutually reinforcing pillars.

First, the inherent flaws of consumer-grade genetic testing.The “saliva-for-report” model pioneered by 23andMe was once hailed as a biotech revolution, but its core product is essentially a consumer novelty catering to curiosity. Although 23andMe’s $99 test can reveal ancestry information and potential risks for certain chronic diseases, the results are neither suitable for serious clinical applications nor capable of providing precise diagnoses, and they offer little room for extended follow-up services.

Consumer-grade genetic testing does not address users' essential needs, resulting in low user stickiness.In the consumer-facing business sector, many companies need to allocate substantial resources to marketing and promotion. 23andMe once enlisted multiple celebrities, such as Ivanka Trump, to endorse its services. However, due to weak consumer spending continuity and low user stickiness, the one-time purchase model has led to sluggish revenue growth and expanding losses for 23andMe. The company’s total annual revenue was $272 million in fiscal year 2022 and $299 million in 2023. According to the latest financial data for the third quarter of fiscal year 2025 (ended December 31, 2024), 23andMe’s consumer services revenue amounted to $39.6 million, representing an 8% decline compared to the same period last year.

The inherent flaws in this industry are further corroborated by the trajectories of other consumer genetic testing companies worldwide. Invitae, another company offering consumer genetic testing services similar to 23andMe, primarily focused on low-cost screening for potential genetic disorders and prenatal testing. Despite securing a $1.15 billion investment from SoftBank, led by Masayoshi Son, Invitae also filed for bankruptcy in 2024.

Other companies offering similar testing services include AncestryDNA. In 2020, the company was acquired by global private equity giant Blackstone for $4.7 billion. According to Reuters, AncestryDNA’s sales growth has also been slowing.

These companies’ testing offerings are characterized by “broad but shallow” coverage, encompassing only a subset of disease-associated genetic loci. This limitation fails to meet the precision demands of clinical practice and undermines their value in informing medical decision-making, resulting in persistently declining user retention rates.

The second major pitfall is the fatal paradox of data monetization.Data monetization was once held in high hopes as a business venture,23andMe’s vast accumulated genetic and phenotypic database holds promise for drug development. In previous funding rounds, 23andMe touted its genetic and phenotypic database comprising 14 million users. However, the application of these data in healthcare has encountered multiple obstacles.

Data Monetization Must Not Cross Ethical Red Lines, users' genetic data cannot be directly used for drug development; data monetization requires user consent. Although publicly disclosed data from 23andMe shows that over 80% of its members agree to have their data used for drug development, the company still faced scrutiny when it sold its database to pharmaceutical companies, even with user consent. Users often do not fully understand how their data will be used when they provide consent.

Data monetization also faces technical bottlenecks. To reduce costs, most consumer-grade genetic testing products on the market opt for lower-cost gene chips. However, the number of detection loci covered by gene chips is far lower than that of clinical-grade whole-exome sequencing, and their accuracy remains to be improved, making them insufficient for clinical applications and new drug development.

The third major pitfall is the breach of trust caused by the 2023 data leak.In 2023, 23andMe experienced a five-month-long data breach that exposed the personal data of 7 million customers, affecting nearly half of its user base and dealing a significant blow to the company’s reputation. To resolve the incident, 23andMe paid a $30 million settlement. However, the loss of user trust proved irreparable, also exposing critical management vulnerabilities within the company.

The fourth pitfall is the disastrous outcome of high-stakes gambling in drug development.Drug R&D was once viewed as the company’s second growth curve, but this capital-intensive business has failed to provide a viable path forward.

In drug development, 23andMe partnered with GSK in 2018, enabling GSK to leverage 23andMe’s database for drug target discovery and other research. The two companies agreed to share profits from any marketed drugs, and 23andMe received a $300 million equity investment from GSK. Over the next five years, 23andMe and GSK advanced approximately 50 projects. However, no drugs successfully reached the market during this period. In 2023, GSK chose to “part ways,” ending their exclusive research collaboration.

23andMe itself has two drug candidates in clinical development, including an antibody therapy designed to restore the immune system’s ability to kill cancer cells by blocking the immune checkpoint CD200R1, and a drug that restores anti-tumor immunity by targeting ULBP6.

Drug development is characterized by long cycles and high costs; in August 2024, before its products had reached Phase III clinical trials, 23andMe disbanded its internal R&D team and halted all therapeutic development.

Fifth, the failure to timely transition into clinical-grade business.. There are multiple transformation paths to break through business bottlenecks. In 2022, 23andMe acquired Lemonaid Health. As a telehealth and pharmacy services provider, Lemonaid Health can extend users’ healthcare experience on the 23andMe platform, but it has also led to increased operating expenses. Meanwhile, competition in the U.S. telehealth and pharmacy services market is intense, with Lemonaid Health facing rivalry from other telehealth platforms and traditional healthcare institutions. 23andMe’s market share failed to expand rapidly, and its revenue declined.

23andMe has not expanded its clinical testing business, diversified through other medical-grade tests, or ventured into areas such as early cancer screening and companion diagnostics.

In recent years, numerous consumer genetic testing companies have fallen into operational distress or even undergone bankruptcy restructuring. The trajectory of this sector’s rise and fall—from the peak frenzy of “genetic fortune-telling” to the current industry-wide shakeout—offers profound insights for the field of medical technology innovation. Medtech enterprises must reconstruct their development logic across dimensions such as strategic planning, technology translation, and business models to avoid repeating past mistakes.

The Collapse of the Consumer Genetic Testing Industry Is Inevitably the Result of Overreliance on Single-Market DividendsThe collapse of the consumer genetic testing industry is, in essence, the inevitable outcome of companies’ excessive reliance on dividends from a single market. The bankruptcy of multiple firms has exposed their overdependence on phased market demand; when policies shifted or market demand waned, their businesses rapidly contracted. Tying a company’s fate closely to demand in a single market is undoubtedly risky. Demand for ancestry testing has been diverted by TikTok-influenced gene tests (such as “Celebrity Lookalike DNA”). Serious players must pivot toward areas such as medical-grade reproductive screening, early cancer detection, and chronic disease management.

Secondly, cost control is also essential. The ability to manage costs is critical to the success of consumer-grade genetic testing companies. Testing service providers typically need to make substantial investments in testing platforms and equipment. Meanwhile, for consumer-facing businesses, many companies must also allocate significant resources to marketing and promotion. Enterprises must balance R&D investment with market returns; those unable to reduce costs through technological innovation are at risk of being eliminated from the market.

Companies also need to establish differentiated competitive barriers. Leading enterprises can create a moat by integrating laboratory resources and expanding value-added services such as health management, thereby building an extensive genetic testing business network. Medical technology innovation must develop "counter-cyclical" capabilities and explore diverse markets through technological extensibility. For instance, genetic testing companies can adopt a dual-drive model targeting both B2B and B2C segments: offering lightweight services such as ancestry analysis and health risk assessment in the consumer market, while deeply cultivating high-barrier areas such as early cancer screening and genetic disease diagnosis in the clinical market.

The bursting of this $6 billion valuation bubble not only signaled the demise of a star enterprise but also marked a defining moment for the biotechnology industry: as the capital frenzy subsides, only technologies that address genuine clinical pain points can withstand market cycles.

The current industry adjustment period presents a window of opportunity for value reshaping. Technological innovation in healthcare is, at its core, a marathon. The lessons from the consumer genetic testing sector serve as a cautionary tale for latecomers: only by abandoning short-term profit-seeking mindsets and building moats in technological depth, cost efficiency, and clinical value can companies achieve the fundamental leap from capital narratives to genuine medical revolution. This is not only a test of corporate strategic resilience but also a recalibration of the innovation logic across the entire industry.

References:

Privatization a Done Deal? All 23andMe Independent Directors Resign, Citing Strategic Differences with CEO – Shenghui