From Cash Burners to Profit Machines: The Self-Sustaining Strategies of 14 Chinese Biotechs

Chinese innovative drugs are rising rapidly with unprecedented momentum, setting one record after another.

On the transaction front, the deal value and number of license-out transactions by Chinese innovative pharmaceutical companies have reached new highs. According to incomplete statistics from VCBeat, a total of 76 license-out deals were recorded in China’s innovative drug sector in 2024, three times the number of license-in transactions (26) during the same period. In terms of deal value, the upfront payments for license-out transactions from January to October 2024 amounted to approximately USD 3.16 billion, with the total transaction value reaching as high as USD 51.1 billion, far exceeding the full-year total for license-out deals in 2023. License-out, NewCo formations, mergers and acquisitions, and other business development (BD) strategies have collectively become part of a virtuous cycle in the development of China’s biotech ecosystem.

On the clinical front, China’s innovative drugs are rapidly being developed and launched globally. According to data from PharmaCube, based on statistics of innovative drugs that entered clinical trials for the first time each year, the cumulative number of innovative drugs in active status developed by Chinese enterprises reached 3,575 by the end of 2024, surpassing the United States to rank first worldwide. Additionally, by the end of 2024, a total of 923 innovative drugs had received their initial global approval. Among these, the share of innovative drugs first launched in China rose from just 4% of the global total in 2015 to nearly 38% in 2024.

The rapid clinical progress and active capital transactions have also been directly reflected on the corporate front, with an increasing number of Chinese biotech companies advancing to the commercialization stage and entering the global arena. The innovative drug business model, transitioning from biotech to biopharma, is being validated in China.

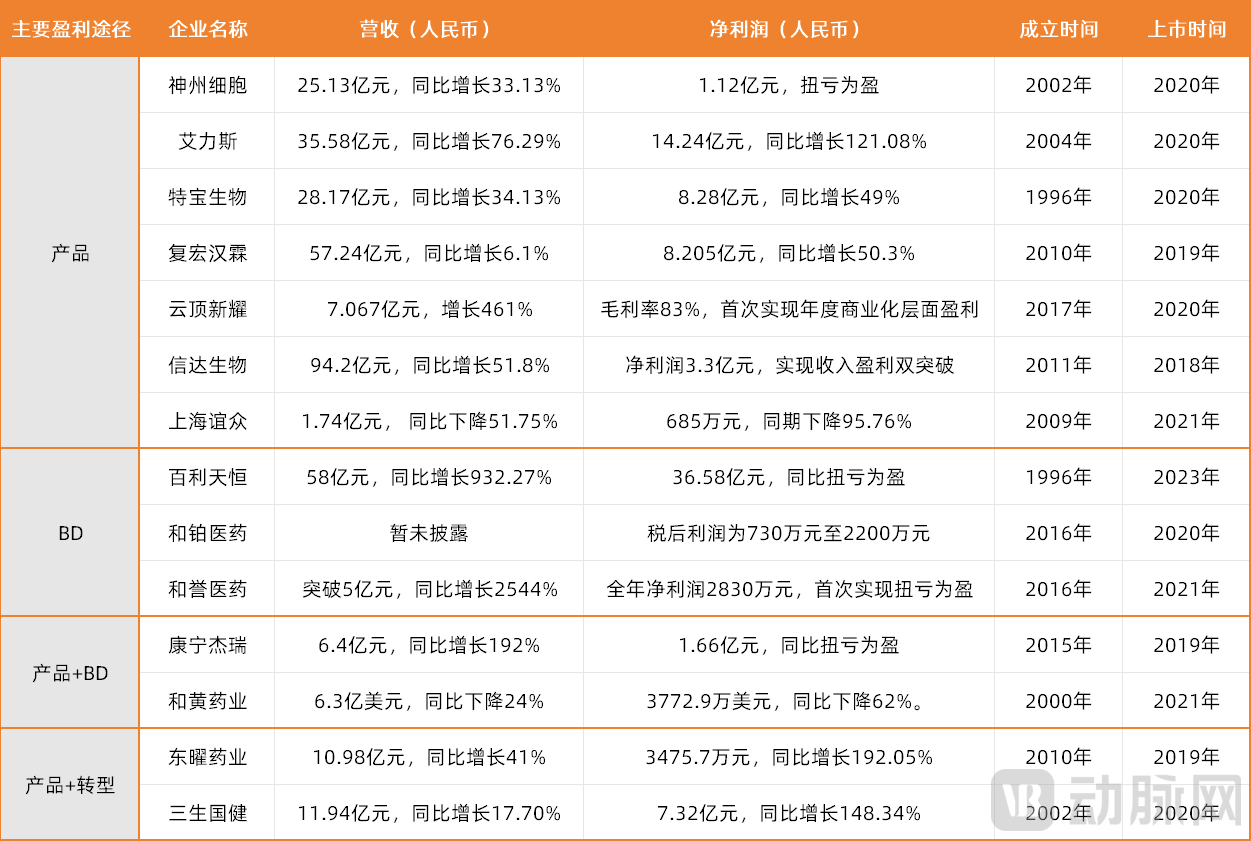

According to incomplete statistics, as of March 27, 2025, a total of 14 biotech companies in China, including Sinocelltech, Henlius, Allist, Amoytop Biopharma, Everest Medicines, Innovent Biologics, Shanghai Yizhong Pharmaceutical, Baili Tianheng, Harbour BioMed, Keymed Biosciences, TopAlliance Biosciences, 3SBio, Hutchison MediPharma, and Abbisko Therapeutics, have achieved profitability. Meanwhile, other enterprises such as Junshi Biosciences, Dizal Pharmaceutical, Zeltex Pharmaceuticals, and RemeGen have significantly narrowed their losses through revenue generation, cost-cutting measures, and improved operational efficiency.

List of Profitable Biotech Companies in 2024 (Based on Incomplete Statistics)

(Listed in no particular order; as of March 27)

These profitable biotech companies were almost all founded more than a decade ago. In contrast to start-up biotechs established in recent years, these early-stage players have fully experienced the drug review and approval system reform initiated in 2015, witnessing the evolution of China’s innovative drugs from barrenness to widespread proliferation. Furthermore, the 2018 reform of listing rules for biopharmaceutical companies on the Hong Kong Stock Exchange, coupled with the establishment of the STAR Market (Science and Technology Innovation Board) in mainland China, spurred a wave of rapid development among biotech firms. Capitalizing on this favorable investment climate, the aforementioned biotechs went public in 2018 and thereafter. Driven by the dual engines of policy dividends and capital influx, the vast potential of China’s innovative drug industry has gradually come into global view. Chinese biotech firms, like brilliant new stars, are shining brightly in the vast ocean of pharmaceuticals.

Product is King,

Profits Soar 8,829.33%

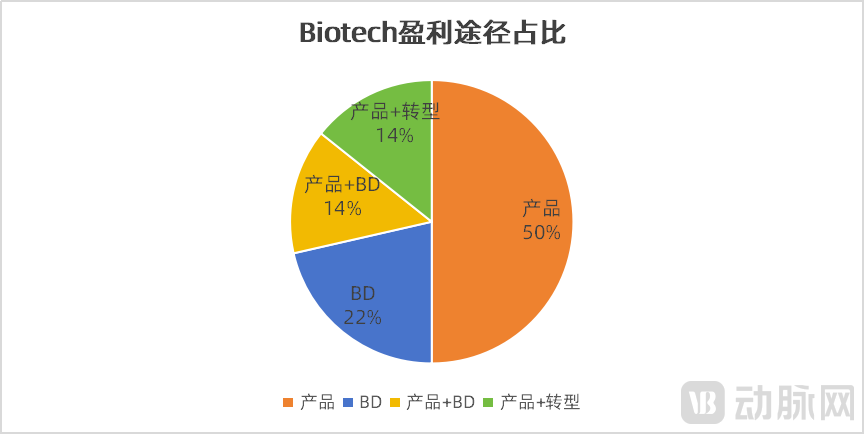

Breakdown of Biotech Companies’ Primary Revenue Streams, Chart by VCBeat

In various corporate announcements, when addressing the drivers of profitability, terms related to “products,” such as the commercialization of core products and the scale-up of core business lines, are cited by most biotech companies as the primary factors influencing their financial performance.Among the 14 companies, seven achieved profitability solely through their products; additionally, four other companies cited their products as a contributing factor to their profitability. Furthermore, the three companies that primarily achieved profitability through business development (BD) did so essentially because their products and technologies gained recognition from large pharmaceutical companies and multinational corporations (MNCs), even though these products had not yet entered the commercialization stage.

Among them, the 2024 financial performance of Sinocelltech and Allist, two biotech companies that have achieved substantial profitability primarily through product sales, has recently drawn particular attention.

According to Sinocelltech’s 2024 preliminary earnings report, the company achieved total operating revenue of RMB 2.513 billion during the reporting period, representing a year-on-year increase of 33.13%; it realized an operating profit of RMB 568 million, a year-on-year surge of 8,829.33%; and recorded a net profit attributable to shareholders of the parent company of RMB 112 million, marking a turnaround from loss to profit compared with the same period last year. According to the announcement, the primary driver of the revenue growth was its core product, Anjiayin.®Sales remained stable, revenue from other marketed products increased, and overall operating income rose compared to the same period last year. Anjiayin®(SCT800) was approved for market launch in July 2021, becoming China’s first domestically produced recombinant coagulation factor VIII product to receive marketing approval, with an indication for hemophilia A, a rare disease. In 2023, Anjia Yin®Sales revenue reached approximately RMB 1.78 billion, representing a year-on-year increase of over 77%, and securing the leading market share among similar products. Based on Sinocelltech’s encouraging 2024 preliminary earnings report, it is foreseeable that in 2024, Anjiayin®Sales are expected to exceed RMB 2 billion.

Another biotech company, Allist, also delivered impressive performance. According to Allist’s 2024 preliminary earnings release, the company’s total revenue in 2024 reached RMB 3.558 billion, a year-on-year increase of 76.29%; net profit attributable to shareholders of the parent company amounted to RMB 1.424 billion, up 121.08% year on year; and net profit attributable to shareholders of the parent company after deducting non-recurring gains and losses stood at RMB 1.352 billion, representing a year-on-year increase of 122.96%. As disclosed in the announcement, its core product, furmonertinib mesilate tablets (brand name “Aifusha®”) generated sales revenue of RMB 3.506 billion, accounting for 98.54% of total revenue. Furmonertinib is the third EGFR-TKI (epidermal growth factor receptor tyrosine kinase inhibitor) approved in China and the second domestically produced third-generation agent in this class. It is indicated for the treatment of patients with epidermal growth factor receptor (EGFR) mutation-positive non-small cell lung cancer (NSCLC) and was commercialized in March 2021. That same year marked the beginning of Allist’s meteoric rise in performance. In just four years, Allist’s revenue surged by 6,300-fold. Relying solely on one small-molecule targeted therapy, Allist achieves annual sales exceeding RMB 3 billion, a feat regarded as an “industry legend.”

However, for early entrants, having a flagship product cannot be the sole foundation for a company’s enduring success.Taking Allist as an example, there are currently nearly 10 EGFR-TKI drugs marketed in China, and competition has become increasingly fierce. Furthermore, resistance to third-generation EGFR-TKIs remains a challenge, prompting numerous domestic and international companies to initiate research and development of fourth-generation EGFR-TKIs. Whether furmonertinib, a third-generation EGFR-TKI, can maintain its competitive advantage amidst technological iteration and product upgrades remains uncertain.

To mitigate the risk of relying on a single product for the majority of the company’s profits, biotech firms often establish multiple pipelines targeting different mechanisms and indications at inception, advancing them in a staged manner.Taking SinoCellTech as an example, to mitigate the risk of reliance on a single product, the company has simultaneously established three major product portfolios in oncology, autoimmune diseases, and vaccines. In addition, besides its revenue “pillar””Anjiayin®In addition, Shenwai has three marketed products: the CD20 monoclonal antibody Anpingxi, the adalimumab biosimilar Anjiarun, and the bevacizumab biosimilar Anbeizhu. These three products have made extremely significant contributions to the company’s profitability (accounting for approximately 20% of revenue), and all three monoclonal antibodies are currently included in the National Reimbursement Drug List.

Furthermore, for latecomers, there exists an unofficial “Rule of Three” in the pharmaceutical industry: for new drugs targeting the same mechanism with comparable efficacy and pricing, the first-in-class drug will capture 70% of the market share, the second entrant approximately 20%, and all subsequent drugs targeting the same mechanism will compete for the remaining 10%.Although this statement originated more than three decades ago, it remains applicable today. Taking PD-(L)1 inhibitors as an example, IQVIA statistics show that the global market size for PD-(L)1 inhibitors reached $36 billion in 2021, with Keytruda, Opdivo, and Tecentriq—the top three PD-(L)1 agents—accounting for 91% of the global market. However, as the PD-(L)1 inhibitor market matures and bispecific and multispecific antibodies gain prominence, the dominance of these leading products is gradually waning.

Therefore, late-entrant biotech companies must achieve optimization or innovation in pipeline targets, indications, CMC processes, head-to-head clinical trials, and commercial pricing to more readily realize their goal of overtaking competitors.

BD Wins,

A New Path to Profitability for Biotech

In 2024, many Chinese biotech companies leveraged business development (BD) as a key revenue stream to achieve short-term commercial viability and advance the R&D of their core pipelines.From the perspective of drug types involved in transactions, the majority of deals have focused on antibodies and antibody-drug conjugates (ADCs), as well as cell and gene therapy (CGT) products. According to incomplete statistics from VCBeat, among the 76 license-out transactions recorded from January to October 2024, half (38 deals) involved antibodies and conjugated drugs, while the CGT sector accounted for 5 deals. Among the license-out transactions related to antibodies and conjugated drugs, bispecific antibodies and ADCs were the primary focus, with 9 deals involving bispecific antibody drugs and 14 deals involving ADC drugs.

Li Yuhui, Founding Managing Partner of Panlin Capital, pointed out that although the CGT sector is not as hot as antibodies and antibody-drug conjugates (ADCs) at this stage, and its development phase is clearly behind that of antibodies and ADCs, CGT remains an investment area that Panlin favors and continues to strategically position itself in. Specifically, if technology and products are well-developed, business development (BD) will naturally follow; blindly catering to the BD preferences of large pharmaceutical companies, on the other hand, carries significant risks.

It is evident that the mainstream business model of Chinese biotech companies is rapidly evolving from “pipeline in-licensing plus commercialization” to “independent R&D plus out-licensing.” Business development (BD) has become one of the most critical pathways for Chinese biotechs to survive and even achieve profitability. In 2024, Baili Tianheng, Harbour BioMed, and Allist Pharmaceuticals all achieved profitability through BD activities. Similarly, Alphamab Oncology and Hutchmed have also attributed part of their profitability to BD in their financial reports.

Taking Harbour BioMed, known as a “BD enthusiast,” as an example, the company reported a net profit (after-tax profit) of RMB 7.3 million to RMB 22 million in 2024, with net operating cash inflow reaching RMB 220 million, a record high. In its announcement, Harbour BioMed stated that its sustainable profitability is primarily driven by the following factors: accelerated growth through its unique business model, sustained strategic partnerships with global pharmaceutical companies and leading biotechnology firms; continuous growth in recurring revenue components in 2024, including platform-based research income and milestone payments from partners as collaborative projects matured; and effective cost control and efficient operational management.

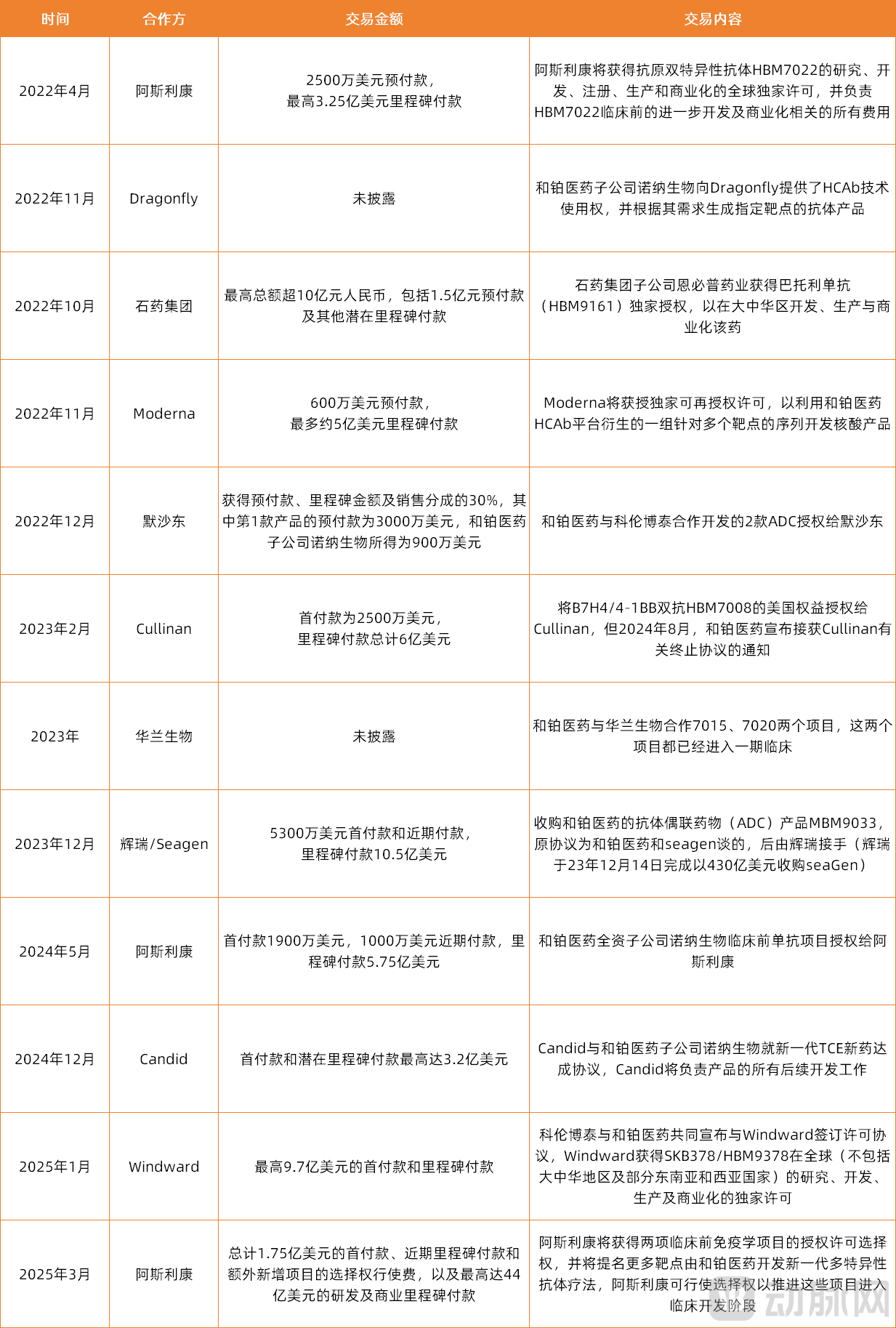

According to incomplete statistics, Harbour BioMed's BD transactions in recent years

According to the NextPharma global new drug database by PharmaCube, Harbour BioMed has entered into 45 external collaborations to date. Among these, 27 collaborations were with overseas pharmaceutical companies, involving three multinational corporations (MNCs): AstraZeneca, Pfizer, and AbbVie. Additionally, according to incomplete statistics from VCBeat, since 2022, Harbour BioMed has completed more than 10 out-licensing deals, with the known cumulative total value of these collaborations approaching RMB 100 billion (including subsequent milestone payments).

Just this year, Harbour BioMed has already secured two major deals: in January, Harbour BioMed and Kelun-Biotech jointly announced a NewCo collaboration with Windward Bio for HBM9378/SKB378, with a total deal value of approximately $970 million; in March, Harbour BioMed announced a strategic partnership with AstraZeneca, with a total transaction value reaching $4.575 billion.

The rapid momentum of BD transactions among Chinese biotech firms is the result of joint efforts by both buyers and sellers.

For the buyer,Li Yuhui, Founding Managing Partner at Panlin Capital, pointed out that multinational pharmaceutical companies are increasingly recognizing the R&D capabilities of Chinese pharmaceutical firms, both in terms of innovation capacity (particularly combinatorial innovation) and clinical data. Secondly, the cost of innovative drug development in China is relatively low, as reflected across various stages including early-stage R&D, CROs, CDMOs, and clinical development. Finally, Chinese innovative drug companies demonstrate high capability and efficiency, giving them a certain advantage in developing best-in-class therapies. Consequently, multinational pharmaceutical giants are inclined to continuously replenish their pipelines with assets from China.

Furthermore, other institutions have pointed out that certain innovative drug assets in China possess their own scarcity. Taking antibody-drug conjugate (ADC) therapies as an example, many large pharmaceutical companies previously discontinued such pipelines due to suboptimal clinical performance. The Chinese R&D teams involved returned to China and continued their research based on a positive outlook for the future development of ADCs. As ADC therapies gained international prominence with impressive clinical data, numerous Chinese ADC drug assets simultaneously came to fruition.

For the seller,Gaining favor from MNCs and major pharmaceutical companies is a testament to the recognition of Biotech’s core competencies. A case in point is Harbour BioMed’s Harbour Mice® platform.®Platform capable of generating fully human monoclonal antibodies in both classic antibody (H2L2) and heavy-chain-only antibody (HCAb) formats, working in synergy with the single B-cell cloning screening platform to optimize antibody discovery efficiency. Centered around Harbour Mice®Through its platform, Harbour BioMed has established a comprehensive antibody drug discovery technology suite encompassing single B-cell cloning, next-generation sequencing, bioinformatics, proprietary immunization techniques, protein science, yeast/phage/mammalian cell display technologies, and antibody engineering. This integrated system has effectively accelerated the development of innovative antibody therapeutics.

Furthermore, key factors influencing whether a biotech company gains recognition from multinational corporations (MNCs) include its focused therapeutic areas (e.g., autoimmune and metabolic disease drugs), product technology platforms (TCE bispecific/multispecific antibodies, cell and gene therapy [CGT] drugs, and radiopharmaceuticals), and the development stages of its pipeline. Regarding pipeline progress, industry experts note that Phase I clinical trials or the pre-clinical stage represent the optimal window for business development (BD) activities, as capital leverage is maximized at this point.

It is worth noting that returns and termination of collaborations are common occurrences in the partnership landscape for innovative drugs and their supply chains. Internal adjustments within multinational corporations (MNCs), shifts in the competitive market landscape, developments in clinical data, or sudden force majeure events may lead to the termination of business development (BD) agreements. Well-known Chinese pharmaceutical companies such as BeiGene, I-Mab, InnoCare Pharma, Hansoh Pharmaceutical, CStone Pharmaceuticals, Jacobio Pharmaceuticals, and LinkHealth have all experienced the termination of license-out partnerships.

In light of trends in business development (BD) deals for innovative drugs and the common challenges encountered during the transaction process, VCBeat has specially invited executives from both buyer and seller sides who have been deeply involved in BD transactions to share their practical experience at an offline event in Suzhou on May 10. Friends are welcome to register and participate.

Money can also be “saved,”

The ratio of total operating expenses to sales decreased by 561.8%

Beyond relying solely on products or business development (BD) to achieve profitability, a segment of biotech companies has attained profitability through diversified strategies, leveraging their product portfolios as a cornerstone while integrating BD, CXO services, and cost-reduction and efficiency-enhancement initiatives. Examples include Alphamab Oncology and Hutchison China MediTech, which rely on “product+BD”This dual model has achieved profitability; while Allist Pharma and 3SBio rely on “products + transformation”This dual-drive strategy achieved profitability.

Taking Eastar Pharma as an example, the company’s revenue in 2024 was approximately RMB 1.098 billion, representing a year-on-year increase of 41%. Among this, sales revenue from products amounted to around RMB 877 million, up 39% year on year, primarily driven by its core product, Puxinting.®Steady growth in sales volume of bevacizumab injection; CDMO/CMO business revenue reached RMB 207 million, a year-on-year increase of 47%. In 2024, driven by its dual-engine strategy, Allist Pharmaceuticals achieved a net profit of approximately RMB 34.757 million, successfully turning profitable in 2024.

Moreover, in the current climate of market cooling, nearly every profitable biotech company has cited cost-saving “strategies”—such as expanding revenue streams, cutting expenses, reducing costs, and improving efficiency—as key drivers behind its profitability. For instance, Everest Medicines, the first publicly listed company dubbed a pioneer in “AI + innovative drugs,” saw its total operating expenses (including general and administrative, R&D, and distribution and sales expenses) as a percentage of sales drop dramatically by 561.8%, reflecting a substantial boost in operational efficiency. In its annual report, Everest Medicines stated that its net loss for the year narrowed significantly by RMB 107.5 million, attributable not only to increased product sales but also to improved operational efficiency.

Furthermore, companies such as Junshi Biosciences, RemeGen, Zai Lab, Dizal Pharmaceutical, and CanSino Biologics have implemented strict cost controls by improving operational efficiency or reducing sales expenses, thereby significantly narrowing their losses. This suggests that for innovative drugs, which often require a decade-long cycle for research, development, and commercialization, cash can also be “saved” during the pre-commercialization phase when biotech firms have not yet established stable cash flows from their pipelines.

Overall, regardless of the model employed, any approach that enables biotech companies to achieve lawful profitability or narrow their losses is considered a sound model. Over the past decade, China’s biotech sector has risen rapidly, transitioning from the development of “me-too” drugs to an innovation-driven stage focused on “first-in-class” and “best-in-class” therapies. In addition to specific factors such as commercialization of core products, business development (BD) licensing, strategic transformation, and cost control, macro-level factors—including policy support, capital availability, and patient demand—have also been significant drivers of revenue growth for Chinese biotech firms.

In the future, the path to profitability for Chinese biotech companies will become increasingly diversified. On one hand, enterprises need to continue deepening their presence in the domestic market and optimizing commercialization strategies; on the other hand, they should enhance global competitiveness through overseas innovation and international collaboration. As R&D capabilities for innovative drugs continue to improve, Chinese biotech firms are poised to occupy a more prominent position on the global stage, creating greater value for the industry and patients while delivering more accessible medicines.

References:

1. The contents of announcements such as performance forecasts, preliminary earnings reports, and annual reports issued by the biotech companies mentioned in the text

2. “2024 White Paper on Innovative Drugs and Supply Chain”

3. "China's Innovative Drug Industry from a Global Perspective: A Ten-Year Review and Outlook"