China's Most Expensive Myopia Surgery Sees Domestic Breakthrough Ending Import Monopoly

Recently, a domestically produced “ICLSparking Industry Attention—In January 2025, Aierbo Nuode’s Dragon Crystal PR phakic intraocular lens received marketing approval. Currently, the first batch of implantation surgeries is being carried out at ophthalmic medical institutions across China, and early post-implantation experiences have already been shared by patients on social media platforms.

Prior to this, the domestic market for refractive lens implants in myopia surgery was nearly monopolized by STAAR Surgical AG’s (hereinafter referred to as “STAAR”) EVO ICL. The overall cost of the procedure remained consistently high, ranging from approximately RMB 28,000 to RMB 34,000 or even higher, making it the most expensive type of myopia correction surgery.Driven by the growing demand for refractive lens implantation surgery in China, STAAR Surgical’s performance has soared; over the past two years, its annual revenue from the Chinese market has exceeded $150 million each year, making it a key pillar of the company’s income.

Nowadays,In addition to the newly launched Dragon Crystal PR, other Chinese companies such as Haohai Biological Technology, Medico, and Yandele are currently developing phakic intraocular lens (pIOL) products. As more domestically produced products enter the market in the future, the competitive landscape is expected to be reshaped.

Currently, refractive surgeries are primarily categorized into corneal refractive surgery and intraocular refractive surgery based on anatomical location. For patients with high myopia or thin corneas, corneal refractive surgery may increase the risk of postoperative complications such as refractive regression and corneal ectasia. In such cases, phakic intraocular lens (IOL) implantation, a mainstream intraocular refractive procedure, demonstrates significant advantages. With features including a wide correction range, minimal surgical trauma, and reversibility (i.e., the lens can be explanted), it enables more patients to achieve spectacle independence through refractive surgery.

In terms of intraocular lens implantation, STAAR Surgical’s EVO ICL has historically held a near-monopoly in the Chinese market.In terms of the same implantation method, Longjing PR is the first product in China to break the monopoly of EVO ICL, mainly achieving breakthroughs in materials, optical design, and other aspects.

One of STAAR Surgical’s core competencies lies in its lens material—Collamer, a collagen copolymer characterized by softness, excellent elasticity, and high biocompatibility. In contrast, Longjing PR utilizes the patented Balacrylic balanced acrylic material, which features a high refractive index, enabling an enlarged optical zone while reducing lens thickness. Publicly available corporate information indicates that the optical zone diameter of Longjing PR reaches up to 6.0 mm. Combined with an aspheric biconcave design, this results in a flatter posterior surface and greater peripheral vault height.

In terms of product specifications, the Longjing PR has a total diameter ranging from 11.5 mm to 14.2 mm, available in 10 models with 0.3 mm increments to match varying ciliary sulcus diameters. The correctable refractive power ranges from -3.25 D to -18.00 D in 0.25 D increments, enabling more precise correction of high myopia. These features better meet patients’ needs for personalized correction.

Overall, the Longjing PR overcomes the existing limitations of the EVO ICL by offering a larger optical zone, more granular model stratification, and lower anterior chamber depth requirements.

Phakic Intraocular Lens Products Already Marketed in China, Data Source: High-End Medical Device Institute Data Center, Publicly Available Corporate Information

In fact,Prior to the launch of Longjing PR, another phakic intraocular lens (pIOL) had already been marketed in China, namely Yijing PRL, under Haohai Biological Technology. However, Yijing PRL differs significantly from Longjing PR and EVO ICL in terms of indications and product design.

Yijing PRL is primarily indicated for patients with high to ultra-high myopia ranging from -10.0 D to -30.0 D. With a smaller overall diameter and a material specific gravity approximately equal to that of aqueous humor (1:1), the implant does not need to be fixated within the ciliary sulcus; instead, it floats freely in the posterior chamber of the eye. According to Yan Zhenguo, Director of Lanzhou Huaxia Eye Hospital and an expert proficient in various refractive surgeries, Yijing PRL becomes the sole surgical option for cases of ultra-high myopia beyond the correction range of both EVO ICL and Longjing PR, or for patients with narrow anterior chamber angles or ciliary body cysts.

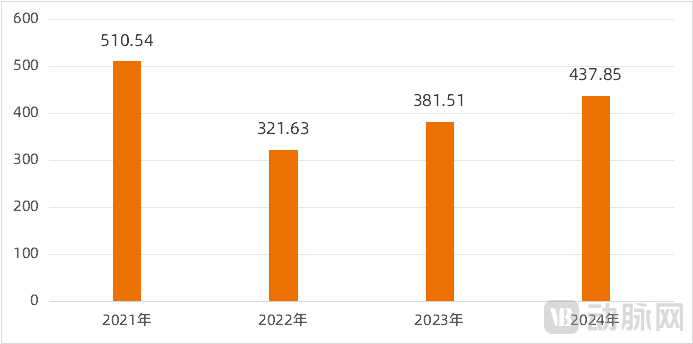

Therefore, strictly speaking, the EYELENS PRL does not have a direct competitive relationship with the other two major products; its patient pool is limited due to restricted indications. Financial reports from Haohai Biological Technology indicate that since 2021, the annual revenue of Hangzhou Aijinglun, the parent company of EYELENS PRL, has ranged between RMB 3 million and RMB 5 million. This is not in the same order of magnitude as the annual revenue of over USD 100 million generated by EVO ICL in the Chinese market during the same period (noting that the overall surgical costs for EYELENS PRL and EVO ICL implantations at medical institutions are comparable).

Revenue of PRL’s Parent Company in Recent Years (in RMB 10,000), Data Source: Haohai Biological Technology Financial Reports

VCBeat learned that,While initially breaking the import monopoly, domestically developed products under research and development are poised for launch, aiming to achieve further breakthroughs in materials, design, and other areas.

For example, Medico’s MPL is advancing its R&D and registration process in China, building on its previous market entry into Southeast Asia, Europe, and South Korea. Liu Liang, CEO of Medico, told VCBeat that the domestic clinical trials for MPL have been completed, with the registration application expected to be submitted in 2025. MPL uses hydrophobic silicone as its primary material, which has a global track record of over 20 years as an intraocular implant, demonstrating excellent biocompatibility and safety. Compared to the EVO ICL, it features a higher refractive index and greater softness, allowing for a larger optical zone, thinner profile, and a broader correction range, up to -28.00 D.

Since acquiring Hangzhou Aijinglun in 2020, Haohai Biological Technology has immediately embarked on upgrading its PRL (Phakic Refractive Lens) product. Compared with the previous generation, the second-generation aqueous humor-permeable product enables aqueous humor circulation and provides a broader range of vision correction. The project is currently in the clinical trial phase, with subjects progressively completing all clinical observations. Product registration is expected to be initiated within 2025.

Furthermore, Yandele has developed a new generation of phakic intraocular lenses using globally patented cross-linked polyolefin materials, offering superior biocompatibility to reduce the incidence of adverse reactions.

Can domestically produced new products successfully break into a niche market that has been monopolized by a single brand for many years? To answer this, we must first examine STAAR’s “rise to prominence.”

STAAR’s rapid rise has been underpinned by the Chinese market. China has a high prevalence of high myopia. In the past, when patients with strong intentions to undergo refractive surgery did not meet the criteria for corneal refractive procedures, STAAR’s Implantable Collamer Lens (ICL) implantation became the primary option.

Since entering the Chinese market in 2006, STAAR Surgical launched the ICL V4c model with a central port design (now known as the EVO ICL) in China in 2014, further enhancing surgical safety and reducing surgical trauma. Since then, STAAR Surgical’s performance has soared.

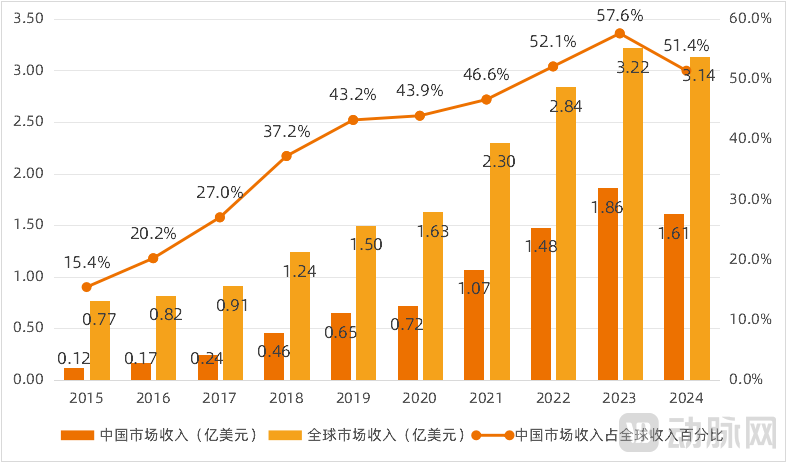

Financial report data shows that in 2015, STAAR Surgical’s global revenue was approximately $77 million, with the Chinese market accounting for only 15.4%, or about $12 million. Over the following decade, revenue from the Chinese market grew rapidly, steadily increasing its share of the company’s total revenue and driving overall business growth. The peak was reached in 2023, when the Chinese market contributed $183 million to STAAR Surgical’s revenue, representing 57.6% of the company’s global revenue, while STAAR Surgical’s total global revenue hit a record high of $322 million.

STAAR Surgical’s Revenue in the Chinese and Global Markets Over the Past Decade, Source: Company Financial Reports

However, the upward trend reversed in 2024. According to STAAR’s latest financial report, the company’s total revenue for 2024 was approximately $314 million, a 3% year-over-year decline, with performance in the Chinese market significantly impacting overall results. In 2024, revenue from the Chinese market amounted to approximately $161 million, down 13.1% year over year. STAAR attributed the sharp decline to “fluctuations in demand for ICL procedures due to economic downturn and weak consumer spending.”

In addition, STAAR experienced its first loss since 2018, with a deficit of approximately $20.21 million in 2024. To address these challenges, STAAR has successively announced decisions regarding adjustments to its management structure and executive team, as well as workforce reductions at its manufacturing facilities, since 2025.

A review of the company’s development history reveals that,Over the past decade, STAAR and the Chinese market have mutually benefited: STAAR capitalized on the surge in demand for myopia surgery in China with just a single product., for a long time, the cost of ICL surgery has remained at a relatively high level, with standard lenses costing around 28,000 yuan for both eyes and toric lenses around 34,000 yuan for both eyes;Meanwhile, STAAR has vigorously promoted the EVO ICL and trained a large number of surgeons, effectively enhancing awareness and trust in implantable collamer lens surgery among Chinese patients, thereby achieving mutual reinforcement between technology and market adoption.

However, the EVO ICL was approved for market launch in China in 2014, more than 10 years ago.Long-term clinical application, with the advantage of having its safety and efficacy fully validated.;However, another issue has emerged: there are no new products to meet patients’ increasing demands. A major limitation of the EVO ICL is its limited optical zone, which makes it difficult to adequately correct vision in patients with large scotopic pupils.

As the next-generation product in STAAR’s global market, the EVO+ ICL features a larger optical zone to reduce postoperative glare and cater to patients with larger scotopic pupils. Although the product received CE certification in 2015, it has yet to be launched in mainland China.

Currently, the EVO+ ICL is available only in Hong Kong, China, and has been introduced at Boao Lecheng as a specially approved surgical procedure. It is understood that the total cost of EVO+ ICL surgery in Hong Kong or Boao, Hainan, ranges from RMB 60,000 to 80,000, more than double that of the standard EVO ICL. Although these two locations have attracted some patients with urgent needs and substantial financial means, VCBeat has learned from medical institutions that patients without urgent requirements are more inclined to postpone their surgery, preferring to wait for the EVO+ ICL to be launched in mainland China. Meanwhile, the domestically produced Longjing PR, recently launched, also features a large optical zone, with surgical costs comparable to those of the standard EVO ICL.

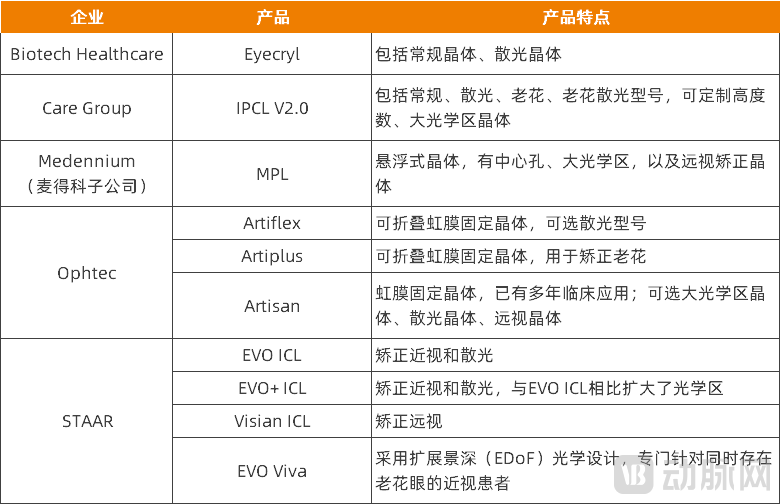

Phakic Intraocular Lens Products Already Launched Overseas, Source: Company Official Websites

Looking at other global companies and products, including STAAR’s EVO series, offerings from Biotech Healthcare, Care Group, Medennium, Ophtec, and others have either been in clinical use for a considerable period (most are posterior chamber intraocular lenses, with only Ophtec’s products being anterior chamber lenses placed on the iris) or feature diversified product portfolios. Notably, Maideke has acquired Medennium and is working to introduce its MPL intraocular lens into the Chinese market. Furthermore, given STAAR’s already dominant market share in China, there is no public information indicating that additional overseas products will enter the Chinese market in the short term.

Overall,STAAR is experiencing fluctuating demand and a transition between legacy and new products in the Chinese market. With no additional imported products expected to enter the market in the short term, the coming period may well represent a window of opportunity for domestically produced differentiated products to rapidly expand their market share.

Currently, breaking the import monopoly has become an inevitable trend in the field of ophthalmology. Whether for refractive surgery products, high-end imaging devices, or ophthalmic diagnostic products, how to enhance technological innovation capabilities and improve the cost-effectiveness of product applications has become a significant industry issue.

In terms of refractive surgery lenses, although domestically produced phakic intraocular lenses have begun to gain traction, it is certain that STAAR’s market position will remain difficult to challenge in the short term, and the benchmark value of its EVO series products persists.

Overall,Domestically produced products must not only demonstrate sufficient product strength to reflect their clinical application value, but also build strong brand influence to gain trust among physicians and patients.

From the perspective of clinical needs, Yan Zhenguo, President of Lanzhou Huaxia Eye Hospital, candidly acknowledged that there is still room for improvement in currently marketed refractive lenses, including the EVO ICL. For instance, the corrective range of the EVO ICL is limited, and due to its soft material, some patients experience a significant postoperative decrease in vault height. Among domestically produced alternatives, the Dragon Crystal PR (Longjing PR) features a relatively stiff material, which demands greater surgical expertise and operational precision from surgeons, and it currently cannot correct astigmatism. The Eyemirror PRL (Yijing PRL) lacks a central port; therefore, to ensure aqueous humor outflow, patients must undergo laser peripheral iridotomy one week prior to surgery. Furthermore, given similar product functionalities, domestic manufacturers need to adopt reasonable pricing strategies to demonstrate their cost advantage.

Liu Liang, CEO of Medico, also believes that clinical value is particularly critical for domestically produced products. Taking posterior chamber phakic intraocular lenses (ICLs) as an example, since these devices do not need to be precisely “wedged” into the ciliary sulcus, they reduce the challenges physicians face in measuring the ciliary sulcus and accurately selecting the appropriate lens model. The central hole design helps avoid the need for surgeons to perform additional iridotomies, which will also facilitate market penetration into lower-tier cities in the future.

In terms of brand strength, STAAR Surgical and its EVO ICL have established a perception among numerous physicians of "extensive case experience with superior outcomes," while also creating an impression among a large patient population of being the "global leader" or even the "only global option." Domestic products need to break through these existing perceptions among both physicians and patients by building a distinct brand image.

The selection of refractive surgery must be based on rigorous ophthalmic examinations, with the premise that examination data align with product indications. However, if a patient meets the criteria for multiple surgical options, they hold the decision-making power regarding the surgical method or product. Therefore, patient-oriented science popularization is equally important.

Currently, ophthalmic medical institutions across China are actively promoting their launch of the first batch of domestically produced Longjing PR intraocular lens (IOL) implants. On social media platforms, influential physicians are providing scientific education on these domestic IOLs, highlighting their functional features such as larger optical zones and a wider variety of models to the general public. Meanwhile, some key opinion leaders are framing the release of these domestic IOLs as “cutting-edge Chinese technology.”

As a leading ophthalmic healthcare institution, He Eye Specialist Hospital has been actively driving innovation in the field through procurement, collaborations, investments, and independent R&D, making significant strides in ophthalmic pharmaceuticals, medical devices, AI, and digitalization. On May 9, VCBeat and He Eye Specialist Hospital will jointly host an Ophthalmic Industry Innovation and Development Forum, featuring offline exchanges in Suzhou.DiscussionHow Chinese Ophthalmic Innovation Enterprises Challenge International Giants,Accelerate breakthroughs in technology and commercialization for domestic ophthalmic innovation enterprises, and strengthen collaboration between innovative companies and healthcare institutions.. Welcome everyoneScan the QR code below to register:

Overall, the concentrated market presence in recent months has made a strong start for brand building of domestically produced myopia-correcting intraocular lenses. The launch of subsequent new products must also precisely distill their core value and vividly and intuitively showcase the differentiated advantages of Chinese-made products to the public.

Myopic refractive lens products face not only competition among different products and companies for the same indications, but also competition from corneal refractive surgery. Compared with corneal refractive surgery, the main limitations of intraocular lens implantation are its high cost, insufficient personalization, and the need to enhance patient trust.

“In China, refractive lens implantation accounts for less than 20% of all refractive surgeries,” Liu Liang admitted. In the past, EVO ICL was virtually the only product available in the Chinese market, leaving both physicians and patients with limited choices. However, as more players enter the field, patient health literacy and physicians’ treatment philosophies are expected to evolve. “As the safety and efficacy of the procedure gain broader recognition among both healthcare providers and patients, the proportion of lens implantations is projected to rise to 40–50%, while the overall penetration rate of refractive surgery will also increase.”

References:

Xu Jingjing, Yu Yifeng, Xiong Jian. Research Progress on the Safety and Efficacy of ICL V4c Implantation[J]. Practical Clinical Medicine, 2024, 25(4): 129-132.