At a Crossroads: The Rise and Regulatory Reckoning of China's Home-Use RF Beauty Devices

By April 2025, home beauty device brands have only one year left to meet compliance requirements.

Since the National Medical Products Administration issued the regulation “Placing Household Radiofrequency Beauty Devices Under Class III Medical Device Management,” the implementation date of the new rule has been postponed from the originally scheduled April 2024 to April 2026, granting companies entering the market a valuable window for adjustment.

Now that half the time has elapsed, industry differentiation has already become apparent:With products from Zongjiang Technology, Yushi Technology, and Time Machine Intelligence having secured the first batch of four Class III medical device certificates, other brands that have yet to obtain qualification stand at a crossroads in their destiny.—Either continue to invest capital in a final push for regulatory approval, or abandon the radiofrequency track and pivot to emerging technologies such as “acoustic” and “optical” modalities, or alternatively, exit the beauty device market entirely.

▲ Data source: NMPA official website; Graphic by VCBeat

Undoubtedly, under the regulatory storm, the market logic for home-use beauty devices has undergone a dramatic transformation.

As numerous medical enterprises pivot toward the out-of-hospital market, home-use beauty devices are among the earliest categories to capitalize on the opportunities presented by new distribution channels.

As early as 2015, home beauty devices quickly gained popularity among young users, driven by the rapid penetration of mobile internet at the consumer level. “The biggest advantage of home beauty devices is their compact and portable design. Coupled with their claimed professional-grade efficacy—for instance, radiofrequency (RF) devices work by inducing collagen fiber contraction in the dermis upon reaching a specific temperature, thereby delivering skin-tightening and wrinkle-reducing effects—they rapidly found market success. This provided young consumers in economically developed regions with a new option for skincare,” Liu Xin (a pseudonym used at the interviewee’s request), an investor previously focused on the non-surgical medical aesthetics sector, told VCBeat. “In the past, seeking treatments at medical aesthetic clinics required considerable effort to select suitable facilities and locations, along with advance appointment scheduling. Now, users can perform skincare routines anytime, anywhere, using home beauty devices.”

The Boom Is Reflected in the Data. According to data from Huajing Industry Research Institute, the market size of home beauty devices in China reached RMB 3.82 billion in 2017 and surged to RMB 9.76 billion by 2021, becoming a market worth over RMB 10 billion and achieving growth of more than 150% over four years.

Capital has moved swiftly in response. Data from the VCBeat Orange Database shows that around 2021, numerous investment firms and corporations—including IDG Capital, Shunwei Capital, Honghui Capital, Fortis Capital, Tiantu Investment, Aoniu Capital, Xinpao Capital, Sanqi Tiansheng, Xiaomi Group, and Tencent—have all placed significant bets on companies in the home beauty device sector.

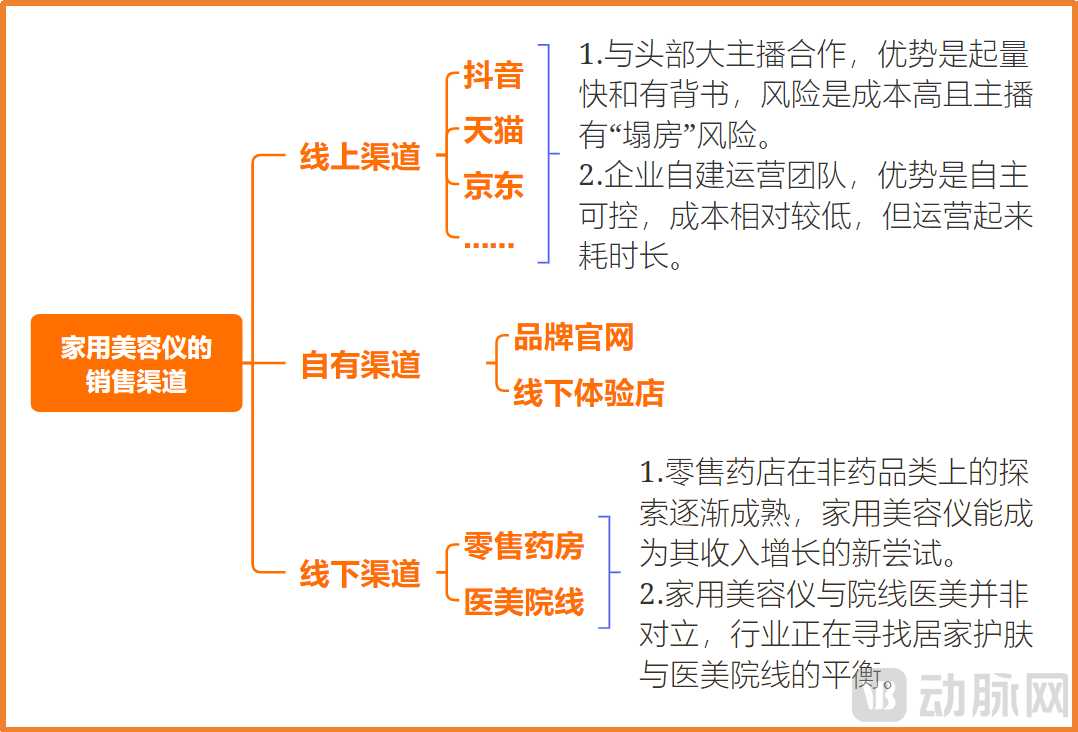

Behind the surge in sales and the industry’s exceptional hype, online channels have played an indispensable role.

According to VCBeat, sales of home-use beauty devices are almost entirely concentrated on new channels such as Tmall, Douyin, and JD.com. For instance, during the first four hours of the 2023 Tmall Double 11 pre-sale period, all ten top-growing brands in the home appliances category were beauty device brands, including Flower Knows (Huazhi), Jiemeng, and JOVS.

Similarly, on the Douyin platform, during the Double 11 shopping festival of the same year, among the top 10 brands by cumulative GMV in Douyin’s beauty sector, ranks 4 through 7 were all occupied by beauty device brands (data source: Shangzhizhen Online Retail Big Data Platform; statistics cover the pre-sale period from October 20 to October 31, 2023).

“Although overall data for 2024 was not available, platforms such as Tmall, Douyin, and JD.com continued to serve as core traffic gateways for home-use beauty devices through major promotional campaigns (e.g., Double 11),” said investor Liu Xin.

Onboarding onto online platforms is easy. The key issue here is,How Are Home Beauty Device Brands Mastering New Channels?

First,The most direct yet effective approach is to collaborate with top-tier live-streaming influencers.On one hand, top-tier livestreamers command high traffic volumes, generating greater exposure for at-home beauty devices and thereby driving sales. For instance, Li Jiaqi once achieved a gross merchandise value (GMV) exceeding RMB 44.97 million in a single session promoting the Ulike hair removal device; similarly, brands such as Jmeng have collaborated with prominent streamers like Mr. Dong, Make Friends, and the Guangdong Couple for livestream sales. On the other hand, top-tier streamers significantly lend credibility to at-home beauty device brands, as evidenced by the widespread practice of brands looping clipped highlights from these influencers’ sales livestreams on their official social media accounts.

However, the aforementioned approach carries significant risks: in addition to the substantial costs incurred by engaging top-tier live-streamers, any subsequent reputational scandal involving a streamer could also have a negative impact on the brand.

Therefore,Many companies also begin to build their own operations teams once their brand has gained a certain level of recognition, leveraging live streaming for technical explanations and real-time interaction to enhance user stickiness.For example, the in-house live-streaming team of Jmeng, a home beauty device brand, leveraged its collaboration with aerospace technology to showcase the product’s technological prowess and enhance consumer trust.

Meanwhile, regarding specific operational strategies, an industry expert pointed out in a previous interview with VCBeat that the copywriting and content for home-use beauty devices primarily target young consumers’ anxiety about aging, thereby reducing users’ decision-making costs and increasing repurchase frequency.

It is evident from the above that the primary factor determining whether consumers purchase home-use beauty devices largely depends on the effectiveness of marketing and promotional efforts.Therefore, the home-use beauty device industry is a typical marketing-driven business.

Excessive Emphasis on Marketing Exposes Hidden Risks in the Home Beauty Device Industry: Many Entrants Allocate Most Funds to Distribution Channels and Engage in Overly Exaggerated Promotion, While Neglecting Product Quality, Leading to Frequent Negative News

Taking Sina’s consumer service platform, Black Cat Complaints, as an example, there have been over 1,700 complaints related to home-use beauty devices accumulated on the platform, with issues primarily focusing on quality defects and safety risks. Among these, a certain brand of home-use beauty device was detected to have a maximum working surface temperature of 74.1°C, far exceeding the safety limit (exposure to 44°C for six hours can cause skin damage). Users experienced skin redness, swelling, burns, and even permanent scarring after use.

Amid various forms of market disorder, the question of how to foster healthy market development has become a pressing challenge for industry participants.

Enhancing user education is one potential approach, but evaluating product quality remains challenging due to the specialized knowledge required and the associated high learning curve. Strictly controlling manufacturers’ product release quality is another solution; however, given the profit-driven nature of the market, inferior products can easily drive out superior ones (Gresham’s Law). Therefore, raising the entry barriers for home-use aesthetic devices and entrusting regulatory authorities with oversight represents a viable path forward.

Thus, in March 2022,The National Medical Products Administration has decided to regulate radiofrequency-based beauty devices as Class III medical devices after extensively soliciting industry feedback.As the most stringent regulatory pathway, Class III medical devices are subject to requirements that mandate proof of safety and efficacy; manufacturers must obtain a registration certificate before they can produce or sell these products.

The benefit is that certified products do not need to expend significant effort and cost to explain whether they are a scam or pose safety risks, thereby simplifying the user's decision-making process.

Since then, the home-use beauty device industry has officially entered a new phase.

The implementation of the new regulations has not proceeded smoothly.

Initially, the policy was scheduled to take effect on April 1, 2024. However, shortly after the new regulations were introduced, the implementation date was postponed by two full years to April 1, 2026, taking into account multiple factors such as the fact that most registration applicants are home appliance manufacturers, the impact of the pandemic, and the implementation of relevant standards.

Behind the turbulence lies the acute pain felt by industry participants.

The reason is that, following their reclassification as Class III medical devices, home-use radiofrequency beauty devices are now required to undergo clinical trials, with actual efficacy and safety becoming the key evaluation criteria. This has increased R&D costs for companies and significantly prolonged the market approval process, resulting in no related sales revenue from this business segment for several years and posing challenges to their financial health.

Specifically, once a company decides to obtain the necessary certification for market entry, it must prepare the application materials, including securing clinical trial filing. Upon completion of the filing, the product can proceed to the participant enrollment phase of clinical trials, which typically takes 1–2 years. This is followed by regulatory testing and reporting for medical device registration, requiring approximately six months. Furthermore, after submission of the registration application, companies may be requested to provide supplementary research materials or supporting data, thereby extending the overall timeline.

Taking the RF beauty device under Zongjiang Technology’s AMIRO brand as an example, the product underwent registration testing, completed clinical trials at multiple Grade A tertiary hospitals, formally submitted its registration application and received acceptance, convened an expert review panel, and completed a series of supplementary tests and validations.The entire process, from project initiation to approval, took over two and a half years, with a cumulative investment of tens of millions of yuan.

Shen Xun, Chief Product Officer of the home beauty device brand Huazhi, also revealed while appearing on a program hosted by a Weibo key opinion leader (KOL) that, following the implementation of the new regulations, the brand redesigned its products in accordance with medical-grade standards—particularly in terms of creepage distance and electromagnetic compatibility (EMC)—to obtain Class III medical device certification.Investment also exceeded RMB 10 million.

The substantial time and financial costs have deterred many brands, leading to industry differentiation. In addition to radiofrequency (RF) devices, common at-home beauty devices include ultrasound, light spectrum, and microcurrent products. As fewer players enter the RF segment, a market leader effect will gradually emerge, while other product categories face intensifying competition.

As a result, few brands remain at the table in the home-use beauty device industry.

At this point, multiple industry experts interviewed by VCBeat all believe that,With the implementation of licensing requirements for home-use beauty devices, the industry has officially entered a healthy development phase characterized by competition based on product strength.

Faced with entirely different market logic, brands urgently need new strategies to break through.

VCBeat, through interviews with multiple parties, believes thatHome-use beauty devices that have obtained certification will no longer need to focus excessively on online platforms for channel selection; instead, they should strive to prioritize a balanced multi-channel approach.: Online channels such as Tmall, Douyin, and JD.com focus on traffic generation and serve as the primary battlegrounds, with sales volumes surging during major promotional events across these platforms. In contrast, brand official websites and offline experience stores have become new arenas for user experience and service, thereby strengthening brand loyalty and serving as key strongholds.

It is worth noting that offline retail pharmacies may emerge as a new battleground for home-use beauty devices. On one hand, as medical device-certified products, home-use beauty devices can enhance consumer trust when sold in pharmacies. On the other hand, retail pharmacies are increasingly mature in their exploration of non-pharmaceutical categories and possess the capability to provide professional guidance and skincare consultations to consumers, making home-use beauty devices a new avenue for revenue growth.

Meanwhile, at-home beauty devices and clinical medical aesthetics are not mutually exclusive; some brands are actively embracing new scenarios to strike a balance between home skincare and professional clinic treatments.

▲ Graphic by VCBeat

Furthermore, in terms of marketing, brands have traditionally relied on celebrity and KOL endorsements along with social media viral campaigns to reach consumers; in the future, however, users may place greater emphasis on endorsements from leading experts and top-tier research institutions.

Under the new strategic approach, home-use beauty devices are bound to carve out a new path.

With only one year left before the deadline, home-use beauty device brands still have much homework to do. The most critical task is to meet users’ genuine needs.

After all, home-use beauty devices belong to the out-of-hospital market, and their core sales logic must be user-centric, making consumer insights crucial.

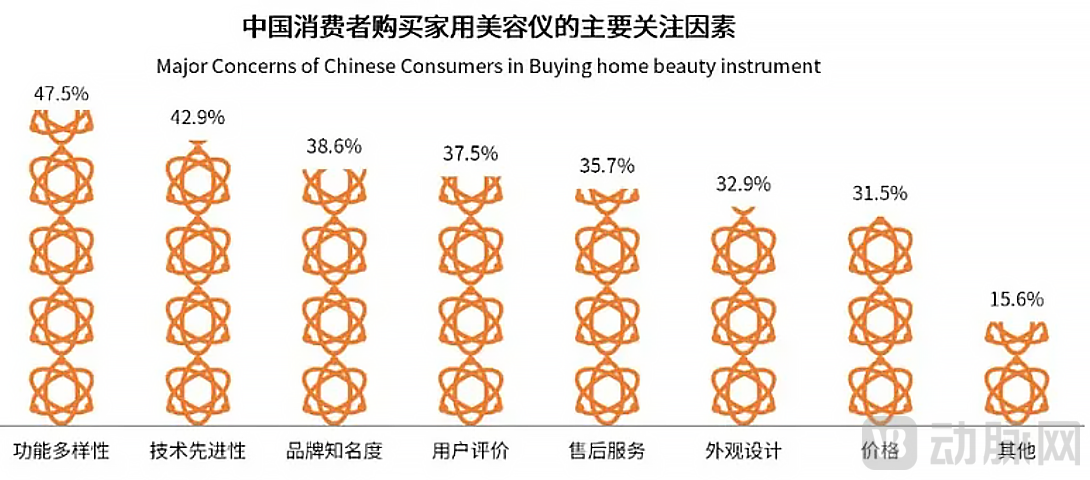

According to survey data from iiMedia Research, functional diversity and technological advancement are key factors influencing consumer decisions. As a result, consumers tend to exhibit highly rational purchasing behavior when buying high-value, multifunctional products such as home-use beauty devices.This means that home-use beauty devices will follow the skincare industry’s trend of intensifying competition in clinical evidence, data, and efficacy.

▲Image source: iiMedia Research's "Research Report on Consumer Insights into China's Home Beauty Device Industry in 2024"

In the exploration of niche consumer segments, home-use beauty devicesProduct design can also be customized for specific populations., such as developing radiofrequency-based beauty devices specifically designed for men to create differentiation.

In terms of personalization, enhancing home-use beauty devices with intelligent technology is also a key direction. For instance, some brands have already begun integrating AI technologies—such as AI-based ultra-high temperature control algorithms, AI motion and posture recognition algorithms, and PID fuzzy control algorithms—into their products, thereby making the functionality of these devices more precise and better aligned with individual user needs.

Regarding user insights as a core element, brands must not only develop industry know-how through practice but also engage in exchanges with various stakeholders to avoid unnecessary detours. On May 10, VCBeat will co-host the “Out-of-Hospital Market New Product and New Channel Growth Conference” with Health Growth Club at the 2025 VBEF Top 100 Future Healthcare and Pharma Exhibition (VBEF), held at the Suzhou International Expo Center. The event will invite distributors, dealers, agents, corporate marketing heads, sales directors, procurement managers, and high-traffic influencers from across China to attend and provide insights into the typical characteristics of today’s new users. Everyone is welcome.Attend the Conference。

In summary, for companies determined to cultivate the home-use beauty device sector over the long term, it is essential to continuously build technological reserves and optimize products, while also gaining deep insights into user needs.

In this process, those who can meet users' real needs will capture a larger market.

We believe that as the formal implementation of mandatory certification for practitioners progresses, the home-use beauty device industry will move beyond its early stage of unregulated, wild growth, and news reports of beauty devices causing disfigurement will cease. This shift will inevitably drive a sustained rise in consumer demand, adding new and compelling commercial narratives to the beauty economy.