The Trillion-Dollar Market and the Harsh Reality of 'Nine Lives Lost': Three Core Challenges That Must Be Solved for Successful Out-of-Hospital Market Expansion

Editor’s Note:

The landscape of the healthcare and wellness industry is undergoing rapid restructuring. As the focus shifts from “hospital-centric” models to “collaboration between in-hospital and out-of-hospital settings,” a new product marketing ecosystem is accelerating its formation. Driven by top-down policy initiatives and structural changes within the industry, this trend has become unstoppable. This year, VCBeat and Wang Rui, an expert in the out-of-hospital market, jointly launched the Health Growth Community. They will host the “Out-of-Hospital Market New Product and New Channel Growth Conference” at the 2025 VBEF Top 100 Future Healthcare and Medicine Exhibition on May 10. In the month leading up to the conference, we discussed the out-of-hospital incremental market—a key focus across the industry—with Wang Rui, Secretary-General of the Health Growth Community.

New changes are underway.

In the in-hospital market, which once accounted for the vast majority of market share, numerous drugs that failed to win bids in centralized procurement have withdrawn and are seeking new sales channels since the normalization of this policy. Although winning bidders have secured large-scale orders, their gross margins are being sharply compressed under the DRG/DIP payment reforms. Furthermore, the prescription circulation regulatory platforms implemented across various regions have effectively severed the reliance of healthcare companies on traditional marketing pathways. The convergence of these factors has made it increasingly difficult for the in-hospital market to serve as a pillar for enterprises seeking new growth.

In contrast, the out-of-hospital market offers growth potential for both “Rx-to-OTC” switches (prescription drugs transitioning to over-the-counter status) and new industry products. For instance, annual sales of Pudilan Anti-inflammatory Tablets reached RMB 1.5 billion after their OTC transition; budesonide nasal spray achieved an out-of-hospital growth rate more than three times that within hospitals; and orlistat leveraged e-commerce platforms to achieve a monthly sales surge into the tens of millions.

The emergence of blockbuster products one after another is revealing the immense potential of the out-of-hospital market.

The fierce growth momentum in the out-of-hospital market has made capturing this segment an undeniable key strategy for healthcare and wellness enterprises.

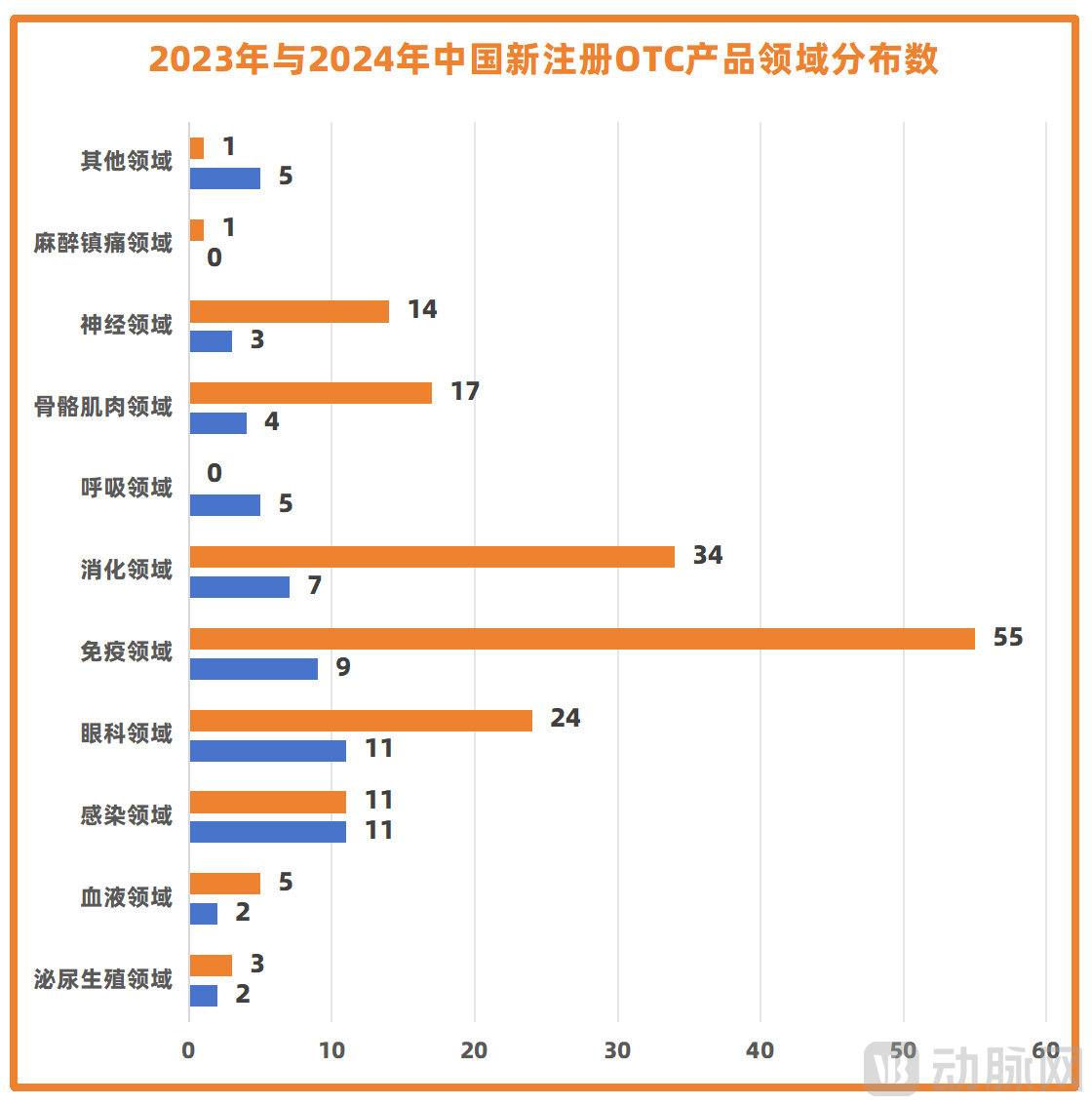

Taking the registration volume of over-the-counter (OTC) drugs as an example, data from IQVIA shows that China saw 165 newly registered OTC products in 2024, representing a year-on-year increase of 280% compared to 2023. This strong growth momentum fully reflects pharmaceutical companies’ heightened focus on and active engagement in the out-of-hospital market.

Meanwhile, it is evident that OTC products are rapidly expanding into multiple therapeutic areas in 2024, with a significant increase in the number of registrations particularly in immunology, gastroenterology, ophthalmology, and neurology. Furthermore, OTC product formulations are becoming increasingly diverse; the emergence of novel dosage forms such as topical solutions and ointments underscores the growing emphasis on varied routes of administration and the accelerating segmentation of market demand.

▲ Data source: IQVIA; Chart by VCBeat

The increase in supply and robust demand are driving the continuous expansion of the out-of-hospital market.According to estimates by Menet, the out-of-hospital market is projected to reach a total volume of RMB 1.6 trillion by 2029, matching or even surpassing the in-hospital market.

Behind the evolution of any ecosystem lies a transformation of the entire system—The rapid growth of the out-of-hospital market is closely tied to the rise of innovative channels.

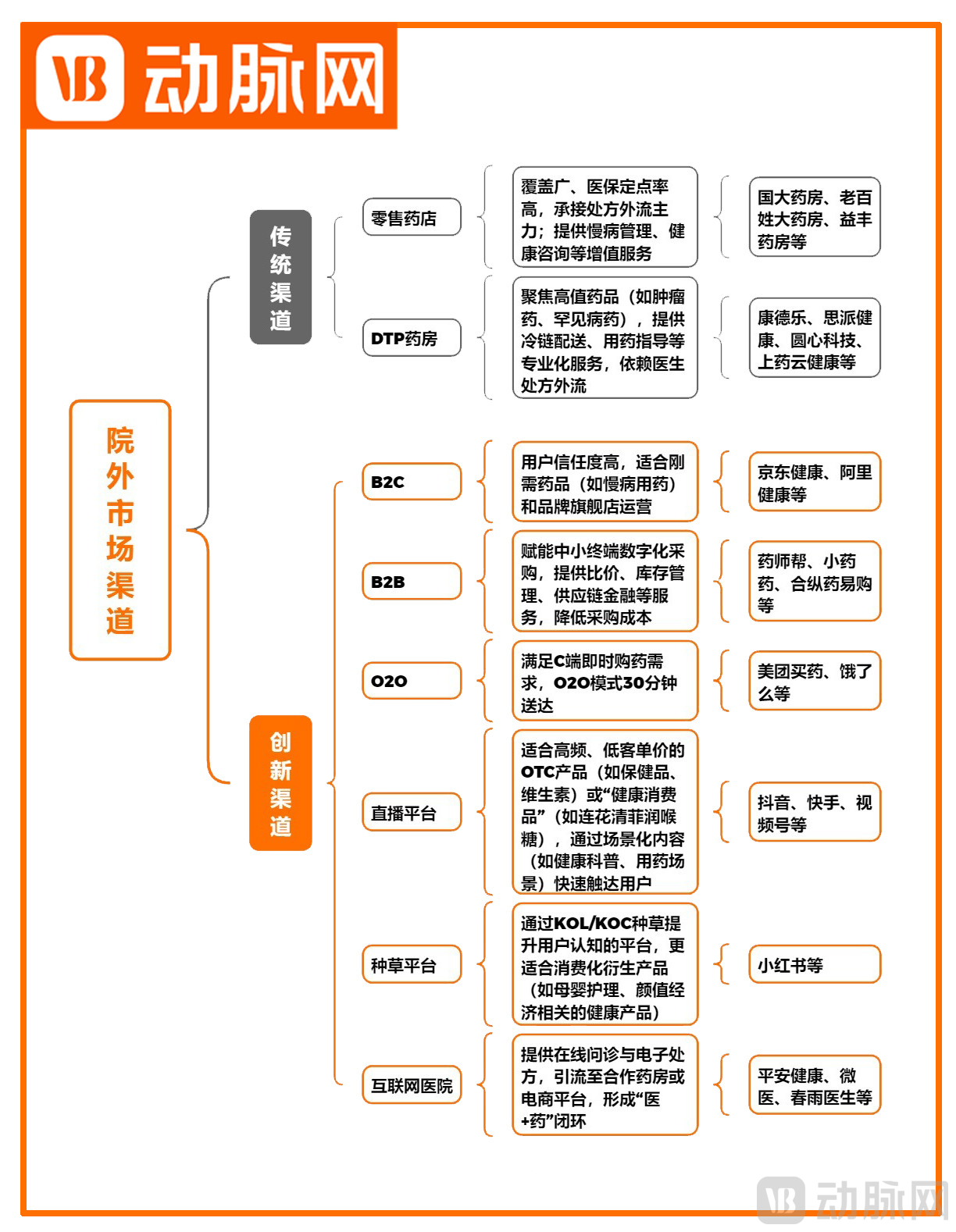

Specifically, the out-of-hospital market features two major channel structures. The first is the traditional offline retail terminal, comprising a vast and widely distributed network of physical pharmacies, including community pharmacies, hospital-adjacent pharmacies, and Direct-to-Patient (DTP) pharmacies. According to 2024 statistics from the National Healthcare Security Administration, there are now over 650,000 pharmacies nationwide. This traditional pharmaceutical sales channel is currently characterized by intense competition, marked by significant "involution" and challenges such as cost pressures. Data from Sinopharm Information (Zhongkang) indicates that an estimated 39,000 retail pharmacies closed across China in 2024, resulting in a closure rate of 5.7%.

The other end is the online innovation channel,Including B2C, B2B, O2O, live-streaming platforms, social recommendation platforms, and internet hospitals, these new channels are the key forces driving the emergence of a new wave of blockbuster products.

▲ Classification of Out-of-Hospital Market Channels | Graphic by VCBeat

Taking the B2C channel as an example, a foreign pharmaceutical product launched exclusively on JD.com’s e-commerce platform rose to the top position on JD’s “Top Medicines” ranking within one week of its release, thanks to digital marketing efforts. Within one month of launch, it climbed to second place in the OTC glucosamine category. Although this medication was already a household name in Europe, it faced significant challenges in expanding through hospital channels upon entering the Chinese market due to its price being 6–8 times higher than that of similar OTC products. Similarly, an innovative targeted therapy for migraine developed by another multinational pharmaceutical company demonstrated comparable performance: on its first day of exclusive launch at JD Pharmacy, it sold 1,000 boxes, which was 1.5 times the combined sales volume across all other non-JD Pharmacy channels.

On social commerce platforms, Giant Biogene’s product Comfy has sold over 250,000 units on Xiaohongshu (Little Red Book); Bloomage Biotech’s Runbaiyan has also seen a significant surge in sales, with its volume surpassing 110,000 units on the platform and generating cash flow exceeding RMB 10 million.

Live-streaming platforms have also emerged as a significant growth driver. Taking Mandi, an OTC hair loss product, as an example, it ranked first in gross merchandise value (GMV) among pharmaceutical and health brands on Douyin Mall during the 2024 Singles’ Day shopping festival. Its multi-channel strategy, particularly the growth driven by new channels, has enabled Mandi to capture over 70% of China’s hair loss medication market share, with an average annual growth rate of 106.33%.

It is not difficult to observe that, whether for legacy products or new offerings, performance achieved through innovative channels has already established a second growth curve for many enterprises.

The narrative of blue-ocean strategy is always alluring, yet those who enter often find themselves navigating treacherous undercurrents beneath the surface. The stark reality leaves many new ventures facing odds of survival that are slim at best.

Therefore, how to achieve out-of-hospital growth has become a new challenge for decision-makers at major enterprises.

“Based on our observations, numerous healthcare and wellness companies are now eager to enter the out-of-hospital market, yet many lack clarity on how to do so effectively. Meanwhile, some companies that have already established a presence in this market may see their products suddenly gain popularity, only to experience a sharp decline in sales within a year or two. In fact, these companies often fail to fully understand the underlying reasons for their products’ initial surge in demand,” Wang Rui, Secretary-General of the Health Growth Society, told VCBeat.

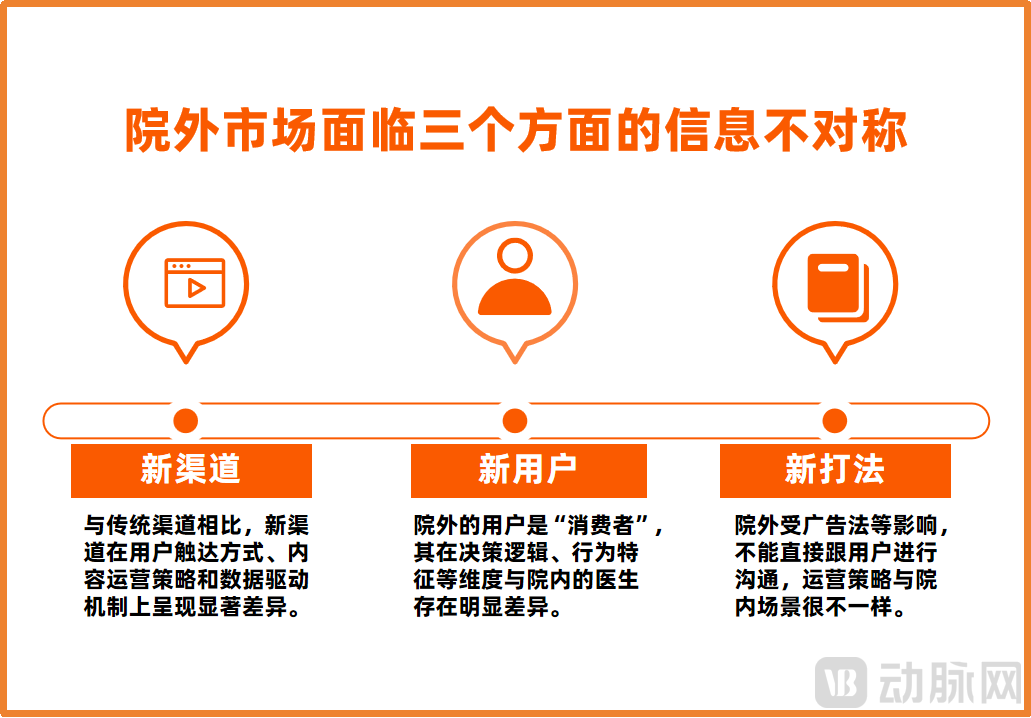

In Wang Rui’s view,The difficulty of operating in the out-of-hospital market is fundamentally rooted in extreme information asymmetry across three dimensions.

First, there is information asymmetry for market entrants in understanding and connecting with new channels.This stems from the fact that most enterprises remain heavily reliant on traditional in-hospital channels to reach physicians, creating an information gap with the core objective of new out-of-hospital channels: direct consumer engagement. Furthermore, traditional in-hospital channels lack accumulated end-user data, while emerging channels differ significantly in user outreach methods, content operation strategies, and data-driven mechanisms. These new channel characteristics—such as the plethora of third-party operational service providers, the influence of key opinion leaders (KOLs) in driving product adoption, algorithmic matching for precise target audiences, and the accumulation of private-domain traffic—pose structural challenges to corporate marketing systems.

Second, there is information asymmetry in the understanding and perception of new users.Previously, the “users” within hospitals were physicians; now, the users outside hospitals are “consumers.” These represent two entirely distinct populations. The two groups exhibit significant differences in dimensions such as decision-making logic (professional authority–driven vs. individual health demands) and behavioral characteristics (centralized medication scenarios vs. autonomous consumption pathways), thereby exacerbating the cognitive gap for enterprises in integrating old and new user personas and gaining insights into their needs.

Third, there is information asymmetry in corporate strategies based on new channels and new users.For instance, products that previously sold well within hospitals now face restrictions on direct consumer communication outside hospitals due to regulations such as the Advertising Law. Consequently, operational strategies—including product selection, specifications, dosage and formulation, and marketing approaches—must be adjusted accordingly.

▲ Chart by VCBeat based on interview content

Due to information asymmetry, companies inevitably took many detours.

For example, a pharmaceutical company’s product was included in the centralized volume-based procurement (VBP) program, with the VBP price dropping to a fraction of its original level. This led to the loss of the hospital market, and due to the lack of a mature out-of-hospital marketing strategy, sales of the drug have declined year after year since its inclusion in VBP. Currently, the product is essentially being abandoned.

The underlying reason is that this pharmaceutical company has insufficient understanding of new out-of-hospital users, failing to establish a brand awareness and user education system for the out-of-hospital market, thereby hindering the implementation of new strategies.

Product selection is equally critical, as the out-of-hospital market is more consumer-oriented; many star products from the in-hospital market may not be suitable for transition to out-of-hospital channels. According to VCBeat’s observations, current best-selling out-of-hospital products are primarily distributed across the following categories: digestive health (e.g., probiotics, lactulose oral solution, Ludangshen oral liquid), bone health (e.g., glucosamine), skincare and allergy treatment (e.g., ketoconazole cream, budesonide nasal spray), respiratory system (e.g., Lianhua Qingke tablets), vitamin and mineral supplements (e.g., niacin, calcium tablets), qi and blood tonics (e.g., Huangqi Jing), and men’s health (e.g., lidocaine-prilocaine cream).

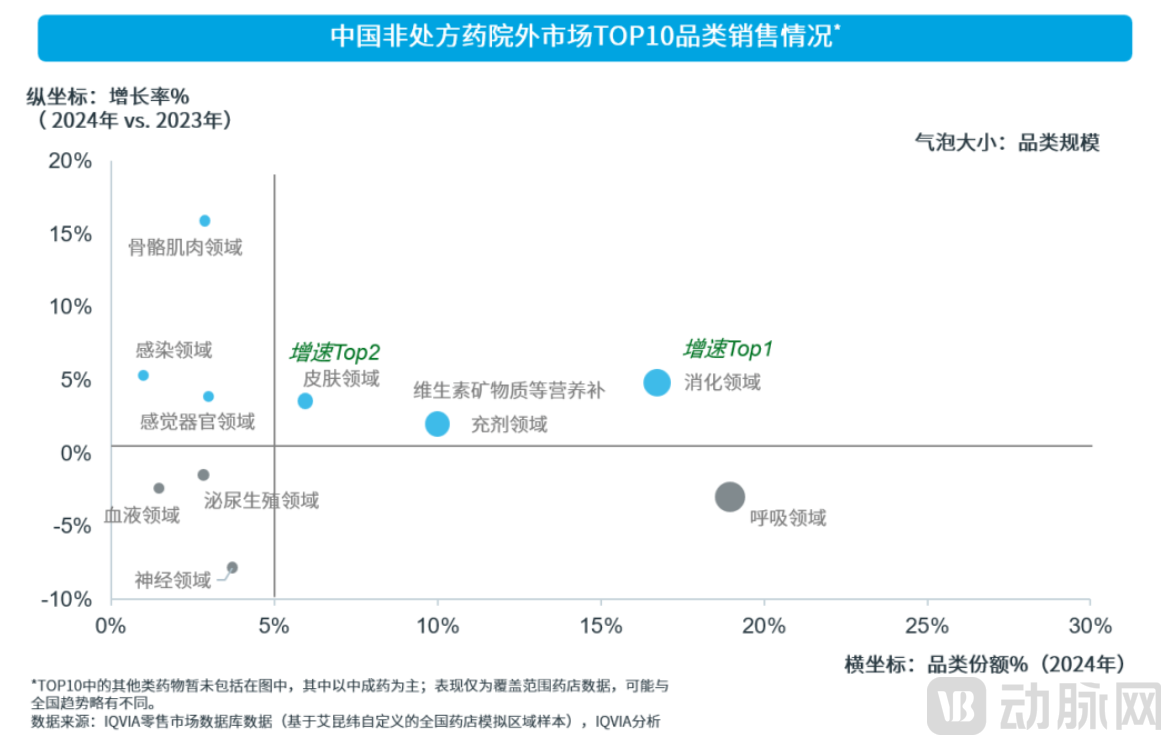

In the over-the-counter (OTC) out-of-hospital market, IQVIA data shows that the top two fastest-growing categories in 2024 were in the gastrointestinal and dermatological segments, respectively.

▲Image source: IQVIA

“Product selection for the out-of-hospital market must be approached systematically from the consumer’s perspective, ensuring that products possess brand power (consumer trust), product efficacy (addressing consumer pain points), and affordability (economic accessibility for consumers)."stated Wang Rui."

Furthermore, in new channels,Product selection should also be tailored to the tone and user profiles of different platforms.Selecting the wrong platform at the outset can lead to misallocation of resources, resulting in wasted time and capital.

Generally speaking, live-streaming platforms such as Douyin and Kuaishou are suitable for high-frequency, low-unit-price OTC products (e.g., health supplements, vitamins) or “consumer health products” (e.g., throat lozenges), enabling rapid user reach through scenario-based content (e.g., health education, medication scenarios). Platforms like Xiaohongshu, which enhance user awareness through KOL/KOC recommendations, are more suited for consumer-oriented derivative products (e.g., maternal and infant care, appearance-related health products). E-commerce platforms such as Tmall and JD.com, characterized by high user trust, are ideal for essential medicines (e.g., chronic disease medications) and brand flagship store operations, allowing precise demand matching via search-based e-commerce models. O2O platforms like Meituan Medicine and Ele.me cater to urgent medication needs (e.g., cold remedies, fever-reducing patches), primarily serving urban white-collar workers and young families, with an emphasis on immediacy and convenience...

In summary, whether for out-of-hospital innovative channels that command substantial traffic and hold the keys to growth, or for new products specifically developed for the out-of-hospital market in urgent need of growth, identifying a partner with matching value will become a matter of paramount importance.

To address the industry’s pain points, it is essential to establish an optimal ecosystem that brings together enterprises with innovative out-of-hospital products, platform providers operating new distribution channels, and operational partners with extensive practical experience, thereby facilitating robust multi-party communication.

In response, VCBeat will host the “Conference on Growth of New Products and New Channels in the Out-of-Hospital Market” at the 2025 VBEF Top 100 Future Healthcare and Pharmaceutical Exhibition (VBEF), to be held at the Suzhou International Expo Center on May 10. By inviting participants from across China—including out-of-hospital market channel partners, distributors, agents, corporate marketing heads, sales directors, procurement managers, and traffic-generating IP influencers—the conference aims to facilitate efficient matching between new channels and high-quality products.

On-site, to enable enterprises to gain a more tangible understandingNew Channels, JD Health will reveal how e-commerce enables pharmaceutical and medical device brands to achieve N-fold growth in both brand building and business operations.

Addressing the challenges faced by enterprisesNew UserOn the issue of product selection, Fanzhuo Group and Xiushi Biopharma will decode the breakthrough strategies for Chinese medical aesthetics materials, while Hengxu Capital will interpret the commercial growth logic of foods for special medical purposes from an investment perspective.

InNew ApproachOn Douyin and Weibo, Professor Duan Tao of Shanghai First Maternity and Infant Hospital, an industry influencer with tens of millions of followers, will share his methodology for incubating mega-IPs and recount the most authentic and practical hands-on experience.

Beyond that, Sun Yuewu, Chairman of the Committee of the China Association for the Promotion of Pharmaceutical Health Development, will provide an on-site analysis of policies and product opportunities in the out-of-hospital market. Representatives from enterprises such as Guangzhou Baiyunshan Huangpu Dahua Health, Huimei Digital Technology, Sichuan Zhenghexiang Group, and Hua Medicine will share insights into the growth drivers of new business models and channels in the out-of-hospital market from various perspectives.

In addition to gaining systematic insights and practical strategies from leading players in new channels—such as pharmaceutical e-commerce platforms, MCN agencies, and DTP pharmacies—as well as manufacturers of emerging out-of-hospital market categories, including pharmaceutical and medical device companies, special medical purpose foods, and health products, attendees will also have the opportunity to engage in on-site discussions and explore resource collaboration opportunities in the out-of-hospital market.

It is also worth mentioning that this off-site forum was co-hosted by the Health Growth Society, the first “super-link hub” in China’s out-of-hospital market, and VCBeat.

“The original intention behind VCBeat and my joint launch of the Health Growth Community was to center on the demand for commercial growth outside hospitals, by bridging the ‘production (pharmaceutical companies/medical devices/health products) – sales (new channels)’ link, and building an out-of-hospital market ecosystem community driven by new products, new production, and new channels. This aims to help medical and health enterprises address the three major information asymmetries mentioned earlier, enabling efficient matching between high-quality products and new channels,” said Wang Rui, Secretary-General of the Health Growth Community.

Specifically, the Health Growth Community has three key characteristics. First, it focuses on new channels that are primarily online. Second, it conducts in-depth analysis and selection of benchmark cases to identify the top-performing products, companies, and operators driving out-of-hospital growth within the industry, thereby helping more enterprises understand how to better leverage new channels, acquire new users, and adopt innovative strategies. Third, it adheres to a long-termist approach, partnering with companies for the long haul to help them achieve genuine sales growth and open up financing pathways for out-of-hospital products (high-quality assets).

It has been revealed that Health Growth Society will launch four targeted IP initiatives in 2025: two conferences and trade exhibitions focused on out-of-hospital market growth; the selection of outstanding case studies from the out-of-hospital market and the publication of a white paper on this sector; small-scale private advisory board meetings centered on out-of-hospital market topics to analyze case studies; and relevant corporate training programs for companies operating in the out-of-hospital market, thereby providing genuine empowerment and support for new products and new channels.

In summary, the Growth Conference for New Products and New Channels in the Out-of-Hospital Market provides an excellent platform for interaction and exchange for enterprises seeking to enter or boost their sales in this sector. With the long-term support of the Health Growth Community, these companies can collectively capitalize on the opportunities presented by the out-of-hospital market.

“As the out-of-hospital market is on the verge of entering a phase of breakthrough growth, certain high-quality products well-suited for this channel will inevitably gain consumer acceptance, which will undoubtedly drive the emergence of more blockbuster products with annual sales exceeding RMB 1 billion,” said Wang Rui, Secretary-General of the Healthy Growth Society.

During this process, enterprises must build systematic capabilities to identify new channels, user segments, and strategies tailored to their needs, thereby establishing an irreplaceable competitive moat amid the ecological restructuring of the healthcare industry and achieving new growth in the out-of-hospital market.