Stealth Rise of China's Innovation Assets: Why Global Capital Is Rushing In

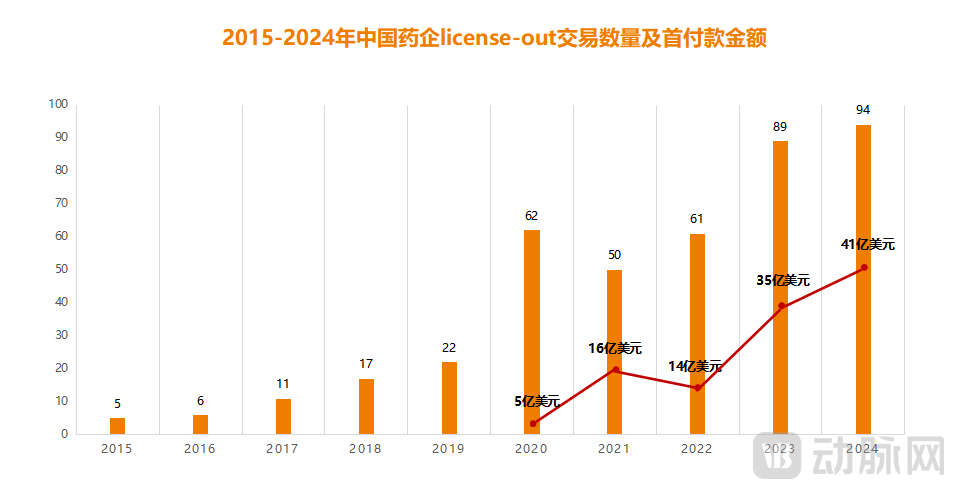

Recently, PharmCube and Tsinghua University jointly released a landmark report, with data showing thatIn 2024, Chinese pharmaceutical companies completed a total of 94 license-out transactions, with the total transaction value reaching $51.9 billion, a year-on-year increase of 26%; among these, upfront payments amounted to $4.1 billion, representing a 16% year-on-year increase.。

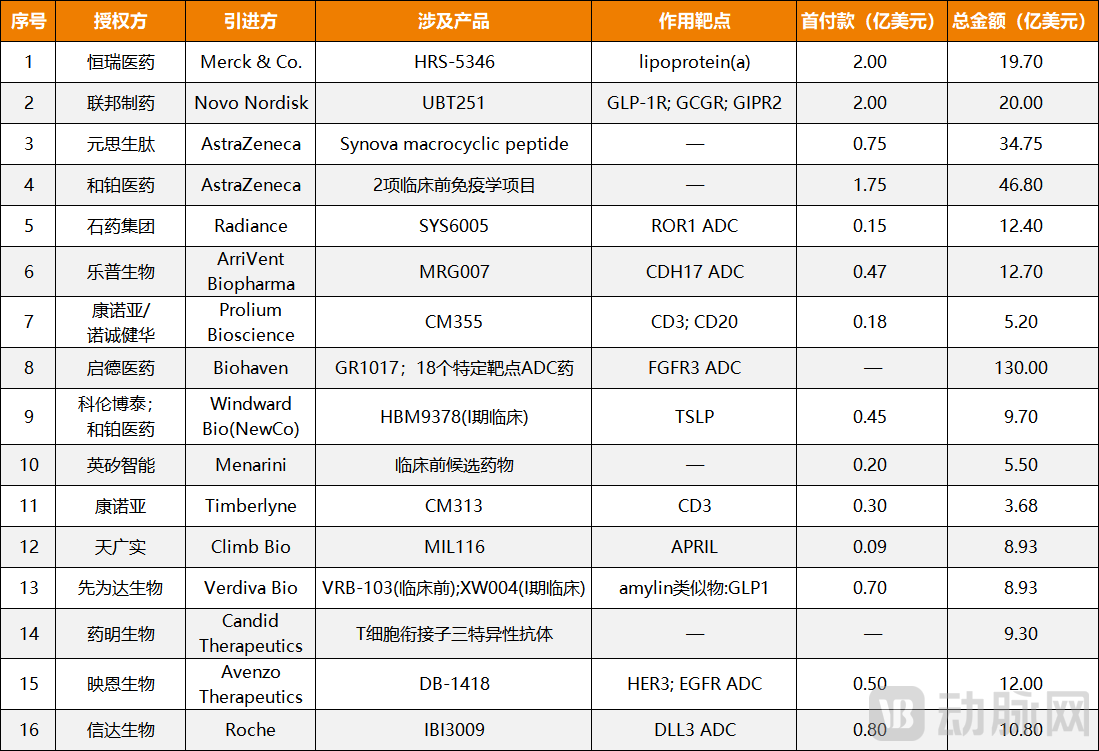

Figure 1. Summary of License-out Projects with Disclosed Amounts in Q1 2025 (Data Source: PharmaCube)

Figure 1. Summary of License-out Projects with Disclosed Amounts in Q1 2025 (Data Source: PharmaCube)

In 2025, this momentum continues. It is reported thatIn the first quarter of this year alone, there have been more than 20 global licensing deals involving Chinese pharmaceutical companies.This includes Roche’s billion-dollar-plus investment in Innovent Biologics, as well as Lepu Biopharma’s landmark collaboration with ArriVent Biopharma on a preclinical ADC, valued at over $1.2 billion. Yet this is merely the prologue. Under the dual pressures of patent cliffs and performance demands, overseas pharmaceutical giants will continue to “snap up” Chinese innovative drugs in 2025, signaling that business development (BD) deal volume is poised to reach new highs.

And behind each large transaction,“Chinese Innovative Assets”This concept is emerging; in fact, it refers not only to innovative drugs but also encompasses high-end medical devices and digital health. Taking medical devices as an example,As of 2024, the localization rate of medical device product registrations in China has reached 67%., In addition, in terms of technological breakthroughs, frontier fields such as surgical robots, medical imaging, and brain-computer interfaces have gradually established their own advantageous positions. Digital healthcare has also performed remarkably.In 2024, a total of 40 medical software products meeting the widely accepted definition of digital therapeutics were approved, setting a new historical high.。

It is evident that the overall value of “Chinese innovative assets” is rising significantly, garnering increasing attention and recognition from global markets. Consequently, a journey of medical value discovery—centered on “Chinese innovative assets” and translating technological innovation into business growth—is opening up new narrative possibilities.

Chinese Innovative Assets: From the Margins to the Center of the Global Stage

At the JPM Conference held in January 2025, Chinese innovative drugs stole the spotlight. Not only was the strongest-ever delegation sent, with more than 30 leading pharmaceutical companies participating, but dozens of events such as “China Night” were also held to full capacity, with many attendees even standing throughout the entire sessions. Furthermore, the topic of “Chinese innovative drugs” was repeatedly highlighted at major core forums, with at least 10 multinational corporations (MNCs) emphasizing the importance of Chinese innovative drugs and the China market in their keynote speeches.

At the recently concluded CMEF, domestically produced medical devices also garnered significant attention. Exhibits with a high proportion of Chinese-made products, such as “Medical Robots” and “Medical Imaging,” were packed throughout the entire event with representatives from leading global medical device companies seeking collaboration opportunities.

As an industry bellwether, Chinese medical enterprises are seeing their voices grow louder at both conferences.In fact, it also reflects the evolving role of “Chinese innovative assets” on the international stage, gradually transitioning from a complete supporting role to one of the leading protagonists.。

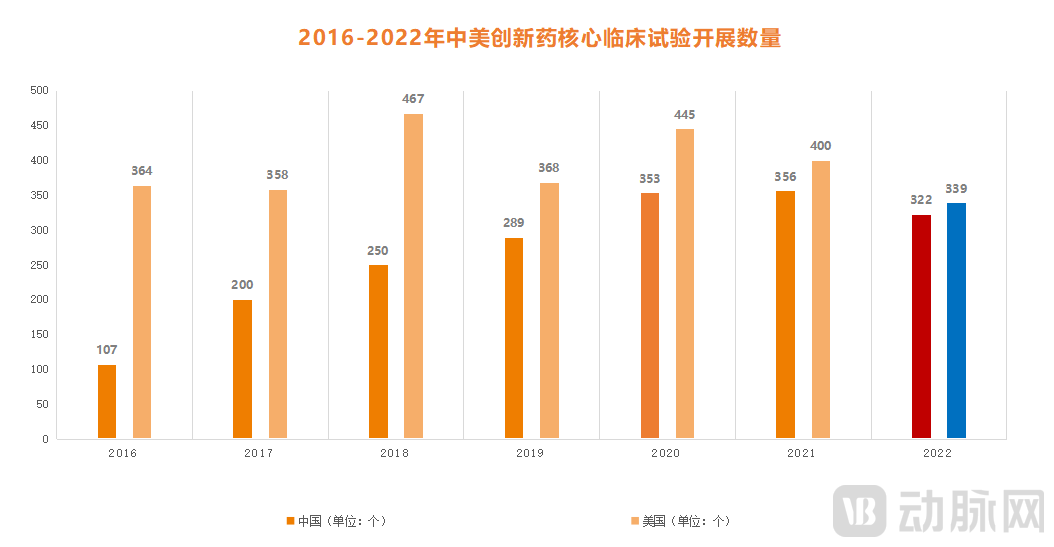

Figure 2. Number of Core Clinical Trials for Innovative Drugs Conducted in China and the United States, 2016–2022 (Data source: PharmCube)

Figure 2. Number of Core Clinical Trials for Innovative Drugs Conducted in China and the United States, 2016–2022 (Data source: PharmCube)

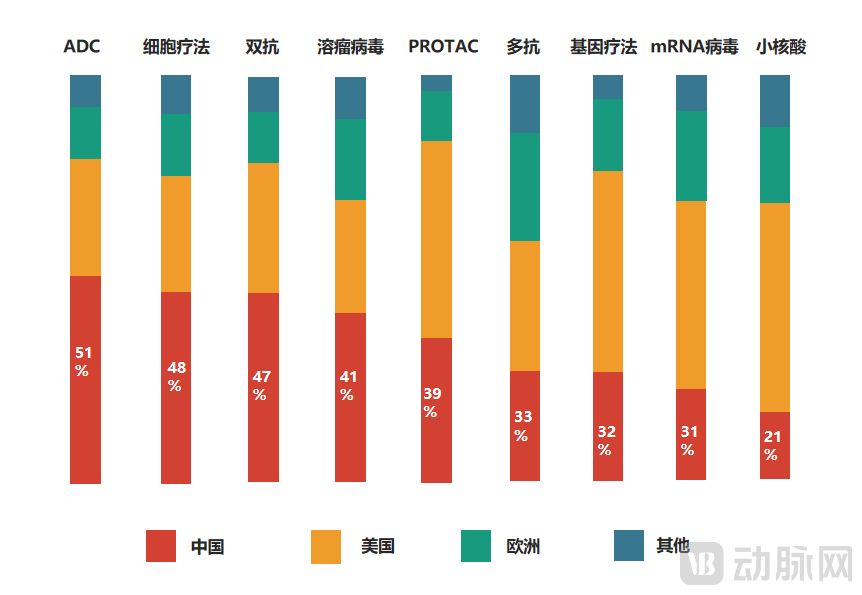

This can be verified from multiple dimensions. Taking the biopharmaceutical sector as an example, in terms of innovation capacity, according to statistics from PharmaCube, China conducted 322 core clinical trials for innovative drugs in 2022, nearly on par with the 339 trials in the United States, and significantly ahead of the United Kingdom and Japan. Furthermore, in terms of overall quality,By 2024, China ranked first globally in the proportion of emerging pipelines, including antibody-drug conjugates (ADCs), cell therapies, bispecific antibodies, and oncolytic viruses., especially for ADCs. China has already become the largest country in terms of outbound licensing deals for ADC pipelines, with domestically produced ADC new drugs accounting for more than 40% of the global pipeline.

The final point is reflected at the corporate level. It is reported that Chinese pharmaceutical companies have secured 11 spots in the “Top 50 Global Pharmaceutical Companies by Market Capitalization” ranking, with the total number second only to the United States (19 spots). Zooming in further on individual companies, Hengrui Medicine’s market capitalization has surpassed the RMB 300 billion mark. After breaking into the top 20 last year, it has once again climbed to its highest-ever rank of 18th. In the CXO sector, the WuXi AppTec group remains firmly positioned as the world’s fourth-largest CXO company, just one step away from breaking into the top three.

In the medical device sector, Chinese-made products are also demonstrating strong performance: Mindray Medical’s revenue hit a new high in 2024, bringing it close to breaking into the top 20 of the global medical device rankings; MicroPort Medical has obtained CE certification for 22 products in Europe, with its international expansion becoming increasingly prominent; and iRay Technology spent eight years mastering core components, emerging as the global leader in digital X-ray detectors.

It is evident that “Chinese innovative assets” are currently embarking on an epic journey of internationalization. Of course, this has not happened overnight; rather, it is the result of the combined drive of multiple key factors.

First and foremost is the emphasis on innovation. Specifically, from the implementation of reforms to the new drug review and approval system in 2015 through to 2025, China’s pharmaceutical industry achieved leapfrog development, transitioning from generic drugs to me-too innovations, and further to First-in-class and Best-in-class therapies. The medical device sector has followed a similar trajectory. Driven by the market logic of domestic substitution, the median R&D intensity of Chinese medical device companies rose rapidly from 3.2% to 6.8% in 2024, with annual R&D expenditure exceeding RMB 100 billion.

Secondly, China is also making significant strides in translating innovation into practical applications. For instance, in terms of R&D efficiency, taking antibody drugs as an example,In China, the process from assembling an R&D team to submitting an Investigational New Drug (IND) application can be completed in as little as 18 months, whereas in the United States, it may take 2 to 4 years., which is actually attributable to key factors such as the absence of generational gaps in knowledge and technology, an efficient CRO system, a robust talent pool, and a comprehensive industrial ecosystem. Additionally, in the approval process,In recent years, the Special Approval Procedure for Innovative Medical Devices has shortened the product launch cycle by 30%. In 2024, a total of 62 products were approved through this channel, representing a 25% year-on-year increase.。

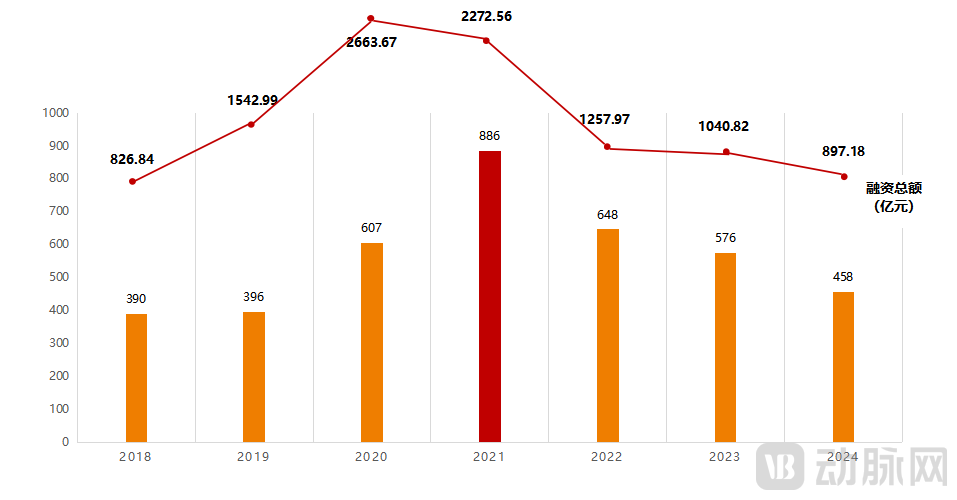

Figure 3. Investment and Financing in China’s Innovative Drug Market: Primary and Secondary Markets, 2018–2024 (Data Source: PharmCube)

Figure 3. Investment and Financing in China’s Innovative Drug Market: Primary and Secondary Markets, 2018–2024 (Data Source: PharmCube)

Finally, at the capital level, a large influx of investment institutions has provided continuous momentum for “Chinese healthcare assets.” According to statistics from the PharmaCube InvestGo database,From 2015 to 2024, China’s innovative drug sector raised a total of RMB 1.23 trillion from primary and secondary markets, driving the successful public listing of more than 500 pharmaceutical companies.This substantial growth underscores the comprehensive rise of “Chinese innovative assets,” which are increasingly engaging in the global industrial ecosystem.

“Chinese Innovative Assets” Witness a Global Buying Frenzy

According to a set of data from DealForma,In 2024, approximately 31% of the innovative drug candidate molecules licensed by large multinational pharmaceutical companies originated from China, whereas this figure stood at 0% in 2019.. This means that major overseas pharmaceutical companies have been frantically snapping up innovative drugs from China in recent years.

Certainly, it is not only innovative drugs that have caught the eye of the global market; domestically produced medical devices are also on the “hot list” for acquisition. In recent years, global medical device giants such as Medtronic, Siemens, Boston Scientific, and BD have been continuously increasing their investments in the Chinese market—whether by expanding investment in China, accelerating localized production, or establishing R&D centers and manufacturing facilities within the country. Their intent is clear: to gain early access to high-quality Chinese assets and seize first-mover advantage in the market.

The reason for this strategic layout is that,In addition to the significantly enhanced value of the aforementioned “Chinese innovative assets,” a crucial point is their ability to help companies “defy the odds and turn their fate around” during market downturns.。

In fact, many pharmaceutical companies have already reaped significant benefits. For instance, Alumis acquired the core asset ESK-001 from FT Group, a subsidiary of the established Chinese pharmaceutical company Haisco, for $180 million in 2021. Three years later, Alumis leveraged this asset to secure $529 million in financing and officially listed on the Nasdaq in June 2024. Another example is Aiolos, which in August 2023 licensed the monoclonal antibody AIO-001 for the treatment of adult asthma from Hengrui Medicine with an upfront payment of only $25 million. Within just six months, Aiolos was acquired by GlaxoSmithKline for a total consideration of $1.4 billion, marking a resounding success.

Medical device companies have also reaped the benefits, achieving substantial returns in both R&D progress and market monetization by acquiring Chinese medical device assets. Taking Boston Scientific as an example, its revenue reached $16.747 billion in 2024, a year-on-year increase of 17.61%. Although specific data for the Chinese market was not separately disclosed in its financial report, China was listed as a “high-growth market,” contributing approximately 20% of its global revenue.

Therefore,A New Wave of Global Acquisitions Targeting “Chinese Innovative Assets” Is Intensifying, with Plans Emerging to Directly Swallow Up High-Quality Chinese Medical Assets。

Focus on the innovative drug sector,At the asset stage, multinational corporations (MNCs) are increasingly shifting their focus toward early-stage development, showing particular interest in pipelines that have not yet entered clinical trials.. It is reported that among the nearly 20 global business development (BD) deals completed by Chinese biotech companies in the first quarter of this year, preclinical projects accounted for more than half. This marks a significant departure from the historical preference of multinational corporations (MNCs) for mature assets. Regarding this trend of “the earlier, the hotter,” a pharmaceutical company founder analyzed two key reasons: First, Chinese innovative drugs are continuously enhancing their competitiveness in upstream stages such as target selection and molecular design, thereby strengthening the innovativeness and certainty of early-stage assets. Second, as Chinese assets gain increasing recognition in the global market, entering the field early is essential to securing a favorable position in the future.

Figure 4. Comparison of the Number of Innovative Drug Pipelines Under Global Development in China, the United States, and Europe (Note: Data as of December 14, 2024)

Figure 4. Comparison of the Number of Innovative Drug Pipelines Under Global Development in China, the United States, and Europe (Note: Data as of December 14, 2024)

Secondly, in the asset sector,MNCs are no longer confined to oncology; instead, they are casting a wider net across broader niche segments, including high-profile areas such as inflammation, immunology, cardiovascular diseases, and metabolism.. Taking autoimmune diseases as a particular example, several large-scale transactions have been completed to date, including AstraZeneca’s $1.2 billion acquisition of Gracell Biotechnologies; AbbVie’s $1.7 billion deal to secure global rights to Mingji Bio’s preclinical TL1A antibody; and, in January this year, an exclusive licensing agreement between Kelun-Biotech, Harbour BioMed, and Windward Bio AG for the anti-thymic stromal lymphopoietin monoclonal antibody SKB378/HBM9378, featuring an upfront payment of $970 million.

Figure 5. Summary of NewCo Transactions in 2024 (Data source: HaoYue Capital)

Figure 5. Summary of NewCo Transactions in 2024 (Data source: HaoYue Capital)

Finally, in terms of asset transaction structures, models such as business development (BD), mergers and acquisitions (M&A), NewCo, and reverse NewCo continue to emerge, creating substantial overall scope for collaboration.. For instance, with the surge in popularity of the NewCo model in 2024, incomplete statistics from VCBeat indicate that Chinese pharmaceutical companies have completed nearly 30 overseas transactions through this model, involving a total value exceeding USD 10 billion. This is merely the beginning; more blockbuster collaborations are expected to materialize under this framework, with increasingly open structures. This trend undoubtedly provides greater opportunities for overseas pharmaceutical companies to acquire high-quality Chinese assets.

Amid the Frenzy, “China’s Innovative Assets” Urgently Need Protection

A review of the corporate annual reports released in succession recently reveals that many domestic pharmaceutical companies have achieved a turnaround from losses to profits for the first time through business development (BD) deals, including Baili Tianheng, Allist Pharmaceuticals, and Alphamab Oncology. Taking Baili Tianheng as a prime example, its net profit reached RMB 3.708 billion in 2024, representing a year-on-year increase of 575%. This remarkable performance was largely driven by a landmark BD deal: in late 2023, Bristol Myers Squibb (BMS) entered into an agreement with Baili Tianheng for BL-B01D1, with a total transaction value of up to $8.4 billion.

Figure 6. Number of License-Out Transactions and Upfront Payments by Chinese Pharmaceutical Companies, 2015–2024 (Data Source: East Money Securities)

Figure 6. Number of License-Out Transactions and Upfront Payments by Chinese Pharmaceutical Companies, 2015–2024 (Data Source: East Money Securities)

In fact,Amid the challenging backdrop of difficult IPOs, a poor financing environment, and limited payment capacity over the past two years, the importance of business development (BD) for domestic innovative drugs is unquestionable, as it has become the primary source of cash flow for Chinese biotech companies.According to a Huatai Securities research report, the upfront payments for business development (BD) deals involving Chinese innovative drugs reached $6.273 billion from January to November 2024, nearly double the $3.977 billion raised by companies through direct financing.

However, everything has two sides.While overseas business development is “rescuing” Chinese biotechs, it is also siphoning off a portion of China’s promising innovative drug candidates, thereby leading to the loss of “Chinese innovative assets.”。

Such concerns are well-founded. On one hand, from the perspective of asset wastage, many large pharmaceutical companies, after acquiring Chinese innovative drug pipelines, may choose to abandon their R&D due to changes in industry demand or internal business adjustments, causing some promising projects to be prematurely terminated. On the other hand, considering bargaining power, if best-in-class innovative drugs are sold to overseas pharmaceutical giants, they will become “imported drugs” when they later enter the Chinese market, inevitably imposing a greater financial burden on the National Healthcare Security Administration and patients. Therefore, safeguarding China’s innovative drugs has become an urgent priority.

Figure 7. Market Share of U.S. Companies in Subsectors of China’s Medical Device Industry (Data Source: East Money Securities)

Figure 7. Market Share of U.S. Companies in Subsectors of China’s Medical Device Industry (Data Source: East Money Securities)

In fact, it is not only innovative drugs that require protection; domestically produced medical device assets also need safeguarding. This has become increasingly critical amid the escalating “US-China tariff war.” Specifically,Although domestically produced medical devices have developed rapidly in recent years, core components in some cutting-edge fields—such as electrophysiology, neurointervention, ultrasonic scalpels, implantable collamer lenses (ICLs), and CT X-ray tubes—still rely on overseas imports, with an import rate exceeding 60%.。

Therefore, if substantial tariffs are imposed, it will inevitably lead to increased production costs for domestic medical device manufacturers, thereby squeezing their profit margins. For instance, the localization rate of CT X-ray tubes is currently below 20%, with heavy reliance on suppliers such as Varex (USA) and Siemens (India). Following the imposition of additional tariffs, the cost of importing a single X-ray tube will increase by more than RMB 200,000, which would directly erode the gross profit margin of domestic equipment manufacturers by 10% to 15%.

In the rapidly developing field of domestically produced surgical robots in recent years, the impact of increased tariffs has been even more devastating. Although Chinese companies such as MicroPort and Tinavi have achieved breakthroughs in complete system manufacturing at this stage, key components still need to be sourced from overseas giants. It is reported that Intuitive Surgical’s da Vinci robotic system holds over half of the market share in China, and the procurement costs for its core servo motors and reducers have currently increased by nearly 40% due to tariffs.

It is not difficult to see that,The battle for “China’s innovative assets” has already begun, with domestic players long stirring beneath the surface.。

Thus, we are witnessing a current rebound in the primary market of China’s healthcare sector. According to incomplete statistics from the VCBeat Orange Database, a total of 82 financing deals were completed in China’s healthcare sector in March alone, with the total financing amount exceeding RMB 10 billion, indicating a clear momentum of recovery. In addition, an increasing number of leading enterprises have begun to participate. It is reported that central state-owned enterprises such as China Resources Pharmaceutical, Sinopharm Group, and China General Technology Group have all transformed into “super buyers,” with the cumulative disclosed amount currently exceeding RMB 26 billion. This is merely the “warm-up phase,” and subsequent investments are expected to be even larger.

But this is not enough; in the view of many industry professionals,The Momentum to Retain “China’s Innovative Assets” Needs to Be Stronger. To this end, held on May 9-10, 2025“VBEF Future Healthcare & Pharma Top 100 Exhibition”VCBeat will build core elements around “China’s Innovation Capital”Bringing together 2,000+ high-quality innovative assets in the healthcare and pharmaceutical industries, along with 1,000+ capital buyers, launching a two-day premium investment promotion conference, venture capital forums covering more than 15 innovative sub-sectors, and thematic forums centered on Newco and BD, to present and showcase the unique appeal of “Chinese healthcare assets” during the two-day exhibition.

Scan the QR code to register for the project. For any inquiries, please contact the author directly.

In the words of a seasoned investor, “This not only provides a window for investors at large to discover high-potential projects, but also builds a bridge for many high-quality projects to access the capital markets. Furthermore, with its early-stage focus on value discovery and later-stage provision of precise resource outreach and linkage value,”It can be described as a precise match between ‘high-quality assets’ and ‘core buyers’.。”

We have every reason to believe that as the “stage” for collaboration and transactions centered on “Chinese innovative assets” continues to expand, more landmark moments will emerge in China’s healthcare and pharmaceutical innovation market, bringing with them greater market opportunities. Consequently, the overall value and vitality of “Chinese innovative assets” will be maximized.

VCBeat hereby invites more industry peers to join us, collectively becoming a vital force driving the sustained development of “Chinese innovative assets”!

Scan the QR code for details on the 2025 VBEF Conference.