40% Return Rate: Chinese Innovative Drugs Face 'Breakup' Crisis in Overseas Markets?

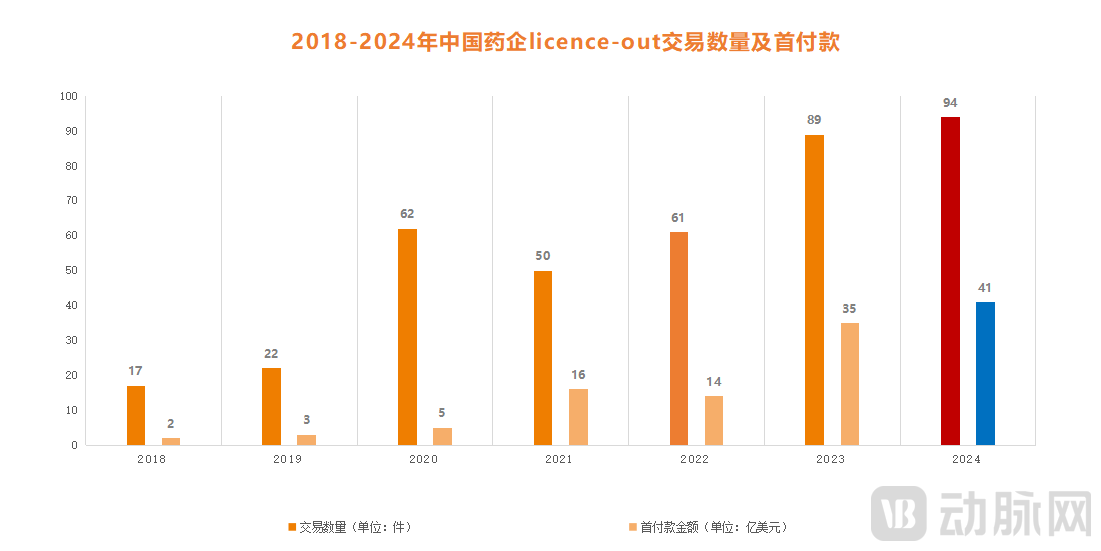

In 2024, China’s innovative drug business development (BD) transaction market was exceptionally active. According to research reports,In 2024, Chinese pharmaceutical companies completed a total of 94 license-out transactions, with the total transaction value reaching $51.9 billion, a year-on-year increase of 26%; among these, upfront payments amounted to $4.1 billion, representing a 16% year-on-year increase.。

Figure 1. Number of license-out deals and upfront payments by Chinese pharmaceutical companies, 2018–2024 (Source: PharmCube)

Figure 1. Number of license-out deals and upfront payments by Chinese pharmaceutical companies, 2018–2024 (Source: PharmCube)

In 2025, this momentum continued. It is reported thatIn the first quarter alone, there were already more than 20 global licensing deals involving Chinese pharmaceutical companies., including Roche’s investment of over $1 billion in Innovent Biologics, and Lepu Biopharma’s landmark collaboration with ArriVent on a preclinical ADC, valued at more than $1.2 billion. In fact, this is just the beginning. Under pressure from the patent cliff, overseas pharmaceutical giants are showing unprecedented enthusiasm for innovative drugs from China and plan to further “snap up” assets. This means that,BD Deals Poised to Hit New Highs This Year。

Amidst the bustling atmosphere,Many domestic pharmaceutical companies have already reaped the benefits.. For example, DualityBiologics,In just six years since its establishment, it has generated over $6 billion in license-out deals., which propelled its successful listing on the Hong Kong Stock Exchange in the recent period, setting a historical record for Chapter 18A companies with a 113% surge. Another beneficiary of business development (BD) dividends is Baili Tianheng. In 2024, the company not only turned losses into profits but also saw its net profit skyrocket by 575% to RMB 3.708 billion. This achievement was inseparable from an epic BD deal struck at the end of 2023,BMS reached a blockbuster deal with Baili Tianheng for BL-B01D1, with a total transaction value of $8.4 billion, including an upfront payment of $800 million.。

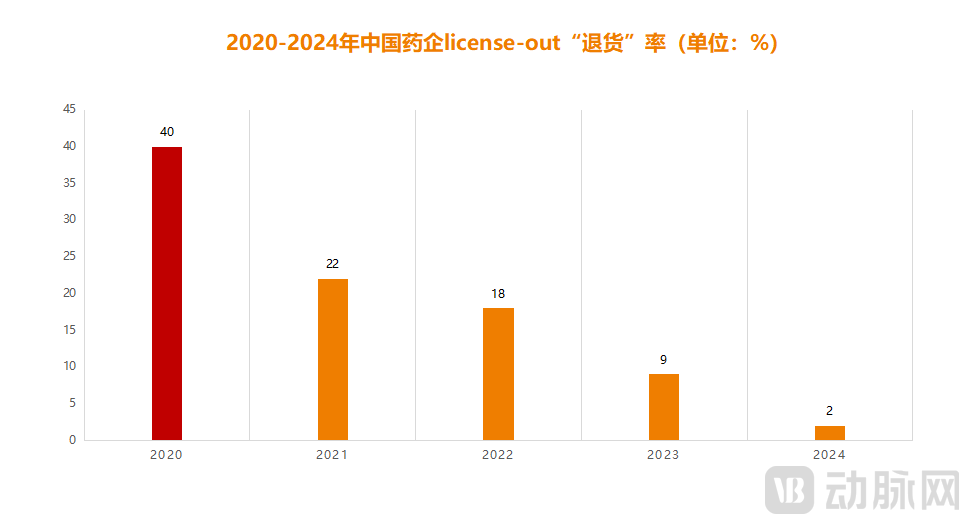

Figure 2. Return Rate of License-Out Deals by Chinese Pharmaceutical Companies, 2020–2024 (Statistics by VCBeat, as of April 2025)

Figure 2. Return Rate of License-Out Deals by Chinese Pharmaceutical Companies, 2020–2024 (Statistics by VCBeat, as of April 2025)

However, everything has two sides. News of BD failures is also emerging. According to incomplete statistics from VCBeat, as of April 20, 2025,Of the 62 license-out deals completed in 2020, 25 have clearly terminated collaborations, resulting in a “return rate” of 40%.Meanwhile, the “return rates” for 2021 and 2022 have currently reached approximately 20%, with many partnerships terminated this year, such as InnoCare’s orelabrutinib and CSPC Pharmaceutical Group’s ADC candidate EO-3021.

In fact, this is just the tip of the iceberg; there is much more hidden beneath the surface. This means that,After Two Years of Frenzied BD Boom, Domestic Innovative Drugs Have Entered a “Reckoning” Phase。

“Breaking Up” Is Hard to Do with Dignity

Since the beginning of 2025, disputes over business development (BD) deals involving domestically developed innovative drugs have been incessant. Among these, the most contentious case has undoubtedly been between Novo Nordisk and Hengli Pharmaceutical: In February 2025, Novo Nordisk accused Hengli Pharmaceutical of fraud, alleging that its founder, Mr. Huang, intentionally concealed negative clinical trial data for ocedurenone prior to finalizing the deal in late 2023, and consequently sought $800 million in damages.

In a similar vein, Clover Biopharmaceuticals has recently become embroiled in a business development (BD) dispute. In March 2025, Clover received written notice from Gavi, the Vaccine Alliance, stating that it would unilaterally terminate the advance purchase agreement and demanding the refund of $224 million in prepayments. Gavi asserted that it had received only approximately 12 million vaccine doses by 2025, far below the contracted quantity, thereby justifying its demand for a refund. However, Clover has currently refused to reimburse the funds, contending that the request lacks basis, and has pledged to take necessary measures to safeguard its rights and interests.

In addition, CSPC and Elevation Oncology, as well as InnoCare Pharma and Biogen, have recently experienced some minor friction due to their “breakups.” In this regard, a senior investor stated, “After all, given that the collaboration involves hundreds of millions or even billions of U.S. dollars, achieving an amicable resolution in the event of disputes is by no means easy.”

So, what exactly led both parties to the point of “breaking up”? And what was the key reason that prevented a dignified split?

This needs to be examined from multiple dimensions,First, subsequent clinical data have been suboptimal.Taking the recent termination of collaboration between CSPC and Elevation as an example, in July 2022, Elevation licensed the Claudin18.2 ADC project EO-3021/SYSA1801 from CSPC for a total consideration of nearly $1.2 billion. However, less than three years later, the Phase I clinical data in the United States deeply disappointed Elevation. The objective response rate (ORR) was only 22.2%, representing a significant decline from the initial figure of 47.1%, thereby precluding further development.

Figure 3. Global CLDN18.2 ADC Development Pipeline (Statistics by VCBeat, data as of May 2024)

Figure 3. Global CLDN18.2 ADC Development Pipeline (Statistics by VCBeat, data as of May 2024)

Next is the ever-changing competitive landscape of the pipeline.In August 2024, Merck & Co. announced the return of rights to Kelun-Biotech’s SKB315. Although this target has generated significant anticipation, by April 2024, four Claudin18.2 ADCs had already entered Phase III clinical trials globally, leaving SKB315, which remains in Phase II, at a clear disadvantage. In response, a senior investor stated, “For targets characterized by intense homogenization competition and lagging clinical progress, overseas pharmaceutical companies would rather forgo upfront payments than decisively choose to terminate collaborations.。”

Then there is the strategic adjustment of the “buyers” themselves, which will also force domestically produced innovative drugs out of the market.Taking Coherus as an example, in January 2024, it chose to “return” JS006 from Junshi Biosciences. The trigger for this decision stemmed from an acquisition: in September 2023, Coherus acquired Surface Oncology. After reassessing its pipeline, Coherus determined that terminating the collaboration with Junshi Biosciences on the TIGIT project would maximize value by reallocating resources to the most promising or competitive candidates in its portfolio. Indeed, amid the current market downturn, strategic adjustments by “buyers” are becoming even more direct and rapid.

Finally, there are changes at the policy level, specifically referring to the FDA’s inconsistent and capricious regulatory stance.. In 2019, at the American Association for Cancer Research (AACR) conference, Richard Pazdur, Director of the FDA’s Oncology Center of Excellence, encouraged Chinese pharmaceutical companies to bring more PD-1/PD-L1 inhibitors to the U.S. market to intensify competition and thereby lower drug prices in the United States. However, when Chinese companies actually presented a slew of PD-1 and PD-L1 candidates, the FDA refused to acknowledge them and began raising various objections, catching domestic enterprises off guard.

Take sintilimab, the first domestically produced PD-1 inhibitor to attempt FDA approval, as an example. This was originally a landmark business development (BD) deal, but it was reluctantly put on hold in December 2022, with Eli Lilly returning the rights to Innovent Biologics. The key factor behind this setback was the hurdle posed by the FDA: the agency rejected sintilimab’s application for marketing approval in the United States for the treatment of non-squamous non-small cell lung cancer (NSCLC), deeming that the application, based solely on Phase III clinical trials conducted in China, was insufficient for U.S. approval. However, public opinion took a different view. Many believed that if sintilimab were approved in the U.S., its price would be 40% lower than that of existing similar products, which would clearly encroach on the market share of American companies such as Merck & Co. Therefore, the decision was made to firmly keep it out of the U.S. market.

In addition, the shifting industry trends and the involutionary vortex triggered by homogeneous competition are also contributing to the bursting of the BD collaboration bubble. It is not difficult to see that although the reasons for “returns” vary, they can all be attributed to one key factor, namelySurvival Anxiety。

“After the Return,” It’s Not Just Money That Is Lost

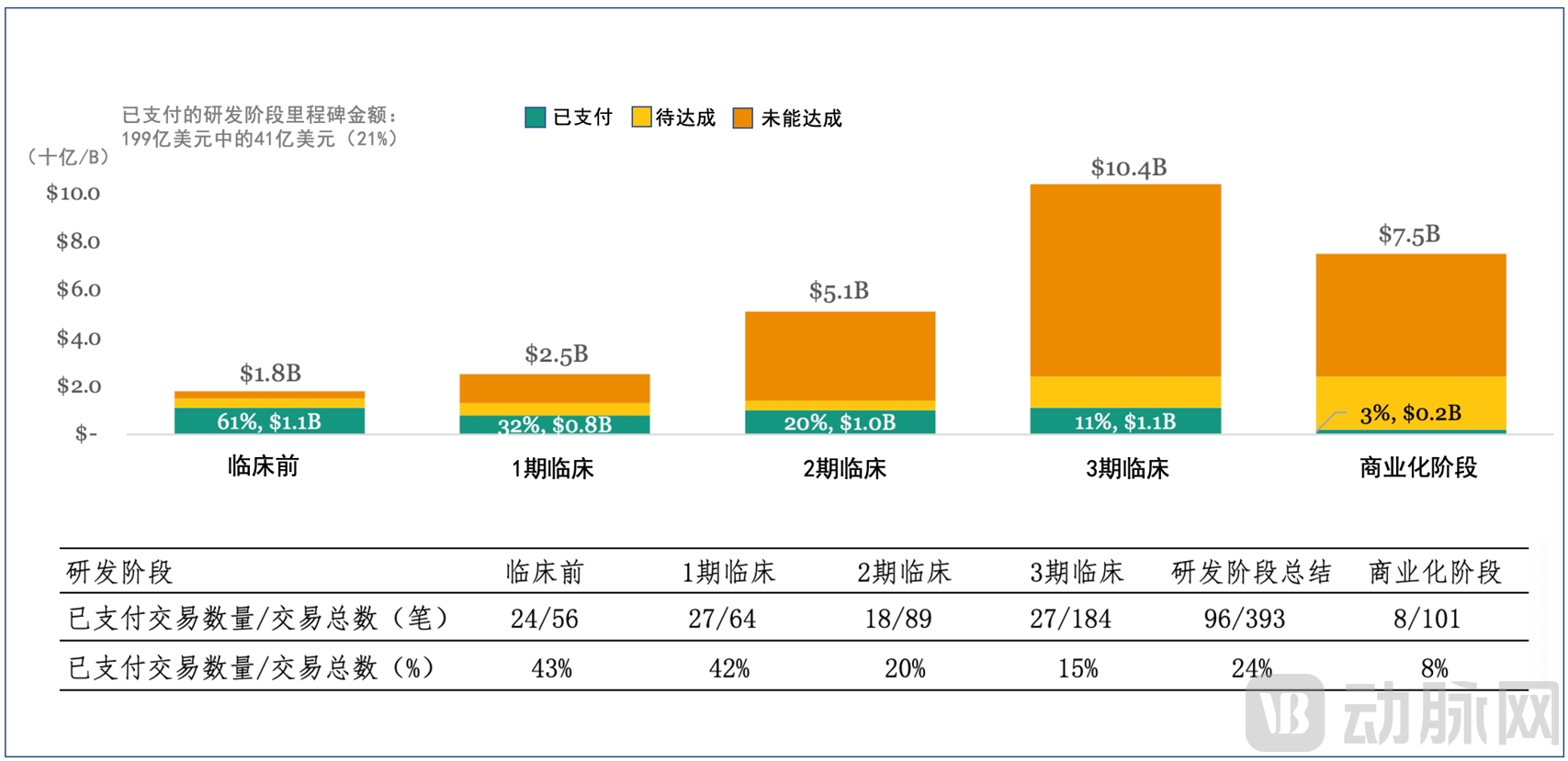

Once the collaboration is terminated, subsequent milestone payments become “mere fleeting clouds,” which undoubtedly represents a significant loss for Chinese pharmaceutical companies. According to statistics from SRS ACQUIOM,In 2023, the milestone achievement rate for innovative drugs in China was only 22%, with the rate declining further in later stages.。

Figure 4. Achievement of Milestones Across R&D Stages for Biopharmaceutical Products with Mid-2023 Expirations (Source: R&D Ke)

Figure 4. Achievement of Milestones Across R&D Stages for Biopharmaceutical Products with Mid-2023 Expirations (Source: R&D Ke)

This means that the vast majority of domestically produced innovative drugs ultimately receive only the upfront payment, which is precisely the lowest portion of revenue.Because China’s innovative drug license-out deals have long followed the narrative logic of “high total value, low upfront payment,” the upfront payment typically accounts for only about 2%–5% of the total transaction value., taking CSPC Pharmaceutical Group’s Claudin 18.2 ADC as an example, the upfront payment from its collaboration with Elevation was only $27 million, while the subsequent $1.168 billion in milestone payments would require successful progression through Phase III clinical trials to commercialization. However, as the partnership was terminated during Phase I, CSPC ultimately received only a small portion of the potential revenue.

In response, a pharmaceutical company executive stated, “As the “Party A,” MNCs always hold the core bargaining power in transactions.. Moreover, as domestic pharmaceutical companies are eager to collaborate with multinational corporations (MNCs) to secure cash flow, they tend to be more accommodating during negotiations, resulting in generally lower upfront payments. This situation is favorable for MNCs, as they incur minimal costs if project progress encounters obstacles.

In fact, this is not the only area where Chinese pharmaceutical companies suffer losses after terminating collaborations.The abrupt halt of pipelines and the collapse of market confidence are equally urgent messes to clean up.。

In September 2023, I-Mab announced the full termination of its collaboration agreement with AbbVie regarding investigational CD47 monoclonal antibody lemzoparlimab and other products. As an innovative pharmaceutical company without any commercialized products, I-Mab’s cash flow heavily relied on business development (BD) revenue. However, following AbbVie’s withdrawal, the company was forced to slash its pipeline to survive. By July 2024, I-Mab’s innovative drug pipeline had been reduced to only three candidates; in January 2025, it further announced the suspension of development for the CD73 monoclonal antibody uliledlimab.

Moreover, the successive release of “negative” news can trigger a series of chain reactions,The most obvious issue is the subsequent difficulty in finding a suitable “buyer.”In this regard, a seasoned investor remarked, “For a biotech company whose ‘core competencies’ are not yet robust, the termination of a collaboration during a phase that requires substantial cash burn amounts to premature ‘death.’ First, it suddenly loses its source of cash flow; second, market confidence in the company will be severely undermined. Subsequently, the only way to find another ‘buyer’ would be by disclosing exceptionally strong data from clinical trials, but such a possibility is extremely slim.”

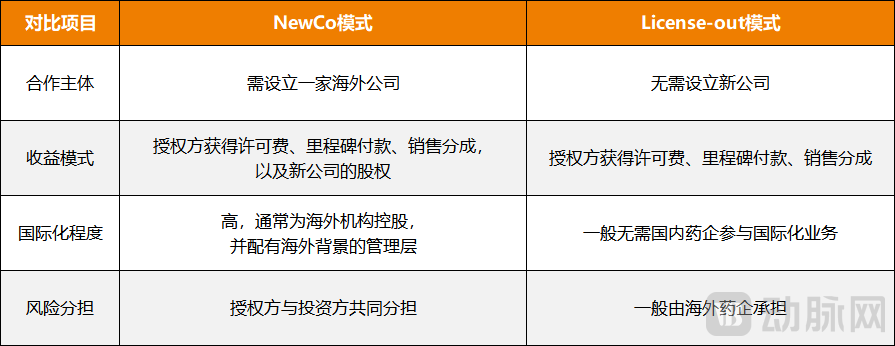

The underlying reasons are as follows:The core issue still lies in the asymmetry of risk assumption between buyers and sellers.Thus, the “NewCo” model began to stand out. According to statistics,In 2024, the total value of deals reached by Chinese innovative pharmaceutical companies through the NewCo model exceeded RMB 60 billion, representing a 54% increase from 2023.. As of 2025, the NewCo model continues to maintain a high-growth trajectory; in January alone, five companies were established through this model.

Figure 5. Comparison of Differences Between the NewCo Model and the License-out Model (Graphic by VCBeat)

Figure 5. Comparison of Differences Between the NewCo Model and the License-out Model (Graphic by VCBeat)

Compared with traditional license-out,The most significant distinction of the NewCo model lies in the deeper alignment between buyers and sellers.. Because it is completely detached from the parent entity, requiring the establishment of a new company to be jointly operated by both the buyer and the seller, this approach is clearly more reasonable than license-out, which cedes all decision-making authority to multinational corporations (MNCs). It not only mitigates risks but also maximizes and sustains long-term benefits.

Domestic pharmaceutical companies have clearly recognized this as well, with Keymed Biosciences serving as an example,Over the past six months, it has rapidly completed three NewCo transactions, with a potential total value of $1.14 billion, accounting for as high as 95% of its total revenue.. This performance is closely tied to its strategic choices: establishing data barriers through rapid clinical advancement, securing survival resources via flexible licensing deals, and exploring internationalization and platform-based transformation under controlled risk.

Stay rational; do not treat BD as a “lifeline.”

Many industry insiders speculate that, following the recent surge in overseas business development (BD) deals over the past two years, instances of “returns” or terminations of Chinese innovative drugs will become increasingly frequent in the coming years.

This is not alarmist rhetoric, nor is it anything new; in mature markets such as Europe and the United States, the ebb and flow of innovative drug transactions has long become commonplace. According to statistics from the Cotellis database,Among the new drugs approved by the FDA, 80% have undergone one or more transactions.. This means that “product returns” are, in fact, the most likely outcome, which aligns closely with the “nine deaths, one life” rule governing innovative drugs.

In this regard, a seasoned investor remarked, “BD itself is like “gambling on jade stones.”, especially as an increasing number of transactions begin to focus on early-stage or even pre-clinical pipelines, this characteristic will become more pronounced. After all, early-stage molecules face numerous variables; any slight disturbance could lead to immediate termination. Even for top multinational corporations (MNCs) like Pfizer, the clinical success rate is less than 5%.

Therefore, amidst the current fervor, it is even more critical to view the essence of this business development (BD) deal with rationality.

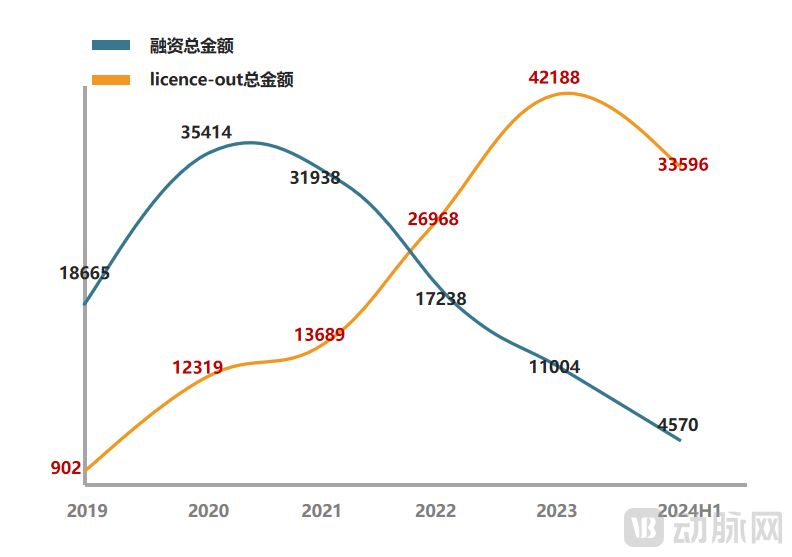

Figure 6. Comparison of Total Financing Amount for Innovative Drugs in China and Total Value of License-out Transactions (Data Source: PharmaCube)

Figure 6. Comparison of Total Financing Amount for Innovative Drugs in China and Total Value of License-out Transactions (Data Source: PharmaCube)

On the one hand, in a market environment where exit pressures and survival challenges carry equal weight, business development (BD) can indeed address urgent needs, and even help some domestic pharmaceutical companies reverse their fortunes.. In the past year or two, such success stories have been abundant, a trend corroborated by data. According to a Huatai Securities research report, upfront payments for business development (BD) deals involving China’s innovative drugs reached $6.273 billion from January to November 2024, nearly double the $3.977 billion raised through direct corporate financing. BD has clearly become the most important source of cash flow for domestically produced innovative drugs.

However, on the other hand, it is also necessary to recognize thatSecuring a business development (BD) deal does not guarantee a perfect outcome, as it not only exposes the company to the risk of being acquired at a low valuation but also imposes significant valuation adjustment mechanism (VAM) pressures associated with transactions involving multinational corporations (MNCs).. In fact, in the innovative drug sector, which rigorously tests long-term commitment, the difficulties and challenges that follow warrant greater caution than the initial eagerness and excitement surrounding license-out deals. This is particularly true amid the escalating China-U.S. tariff war, where heightened uncertainty in overseas transactions significantly increases the likelihood of deal failures.

Therefore,BD should be a choice made after weighing the pros and cons, rather than a desperate attempt born of urgency.. Next, for domestically produced innovative drugs to successfully expand into overseas markets,It is imperative to introduce new elements to demonstrate one’s competitive edge, such as leading global R&D progress, benchmarking against superior global clinical data, or achieving significantly higher global sales revenue., and this is, in fact, the timeless market logic for innovative drugs: robust clinical data and substantial commercialization potential.

Only in this way can one have the opportunity and confidence to “remarry” an MNC, even if faced with product returns someday.

1. “China’s ADC Bubble Is Bursting” – Yiyao;

2. “Chinese Innovative Drugs’ License-Out Deals ‘Collectively’ Returned: Is the Industry Facing a Final Reckoning?” — MedTrend

3. “The Myth of a Return Wave for China’s Innovative Drugs” — Gazelle Club.