China's Pet Innovative Drug Market: Challenges and Opportunities Amid Only Two Domestic Class-1 Approvals

Pets refer to animals kept in households, primarily including cats, dogs, turtles, birds, rabbits, saltwater fish, and freshwater fish, while reptiles and arachnids include spiders, lizards, and scorpions. With the continuous improvement of people’s material and spiritual well-being, the pet population in China has been steadily increasing. According to data from Frost & Sullivan, the number of pets in China grew from 310 million in 2020 to 430 million in 2024, representing a compound annual growth rate (CAGR) of 8.2% during this period. Looking ahead, driven by the promotion of pet culture through social media, the pet population in China is projected to reach 570 million by 2029, with a CAGR of 5.8% from 2025 to 2028.

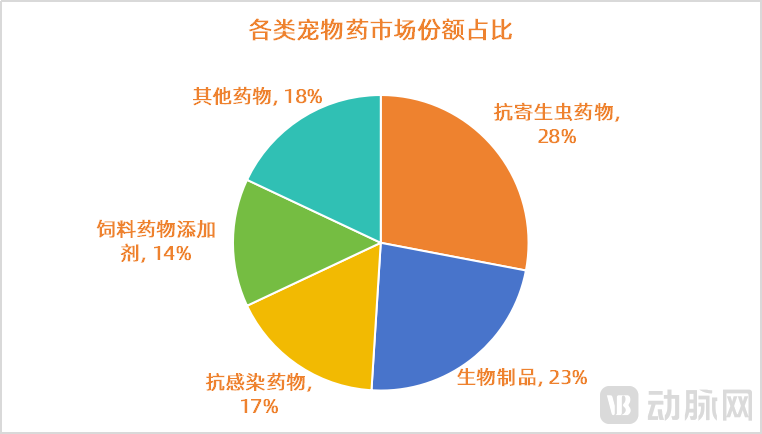

However, compared with European and American countries, the proportion of pet-owning households in China remains relatively low, indicating that the market still holds enormous potential, which in turn has driven the rapid development of the veterinary healthcare industry.Pet medicines refer to drugs specifically used for the prevention, treatment, and diagnosis of diseases in pets, ensuring their physical and mental well-being, as well as preventing zoonotic transmission to safeguard the health and safety of pet owners. Categorized by product type, pet medicines include antiparasitic drugs, biological products, anti-infective agents, feed additives, and other pharmaceuticals. By dosage form, they are primarily available as tablets, liniments, sprays, drops, ointments, injections, and vaccines. Among these, antiparasitic drugs hold the largest market share, accounting for 28% of the global market, with a total value reaching $3.115 billion.

Based on data from the article “Study on the Synthesis Process of Non-rofecoxib,” graphic by VCBeat

According to Frost & Sullivan data, to meet the substantial demand in the pet healthcare market, the number of pet diagnosis and treatment institutions in China grew from 16,000 in 2020 to 26,000 in 2024, representing a compound annual growth rate (CAGR) of 12.9% during this period. The number of such institutions is projected to reach 44,000 by 2029, with a CAGR of 10.4% from 2025 to 2028.

According to QYResearch data, the global pet pharmaceutical market reached USD 12.608 billion in 2019 and is projected to reach USD 20.058 billion (approximately RMB 145.555 billion) by 2026, with a compound annual growth rate (CAGR) of 7.04%. Meanwhile, Frost & Sullivan data shows that China’s pet pharmaceutical market grew from RMB 9.39 billion in 2020 to RMB 20.95 billion in 2024, representing a CAGR of 22.2% during this period. The market size in China is expected to reach RMB 35.41 billion by 2029, with a CAGR of 10.4% from 2025 to 2028.

Despite the vast, untapped potential of the pet pharmaceutical market, valued at hundreds of billions, China’s capacity for independent research and development of innovative pet drugs remains in its infancy. To date, only two domestically developed Class I innovative pet drugs have received marketing approval: Vitacoxib Chewable Tablets by Oubofang (approved in 2016) and Lishutinib by GeGeWu and Elanco Animal Health (approved in 2024). Currently, the majority of China’s pet drug market is still dominated by overseas animal health giants. Globally, most pet pharmaceutical products are concentrated among leading companies such as Boehringer Ingelheim (which owns Merial), Merck & Co. (which owns Intervet/Schering-Plough Animal Health), Elanco Animal Health (which acquired Bayer’s animal health division), Zoetis (formerly Pfizer’s animal health division, spun off and listed independently in 2013), and Virbac.

Amid the monopoly held by animal health giants, what pain points must Chinese pet innovative pharmaceutical companies overcome to achieve a leapfrog development and secure a foothold in the market?

Challenges in the R&D of Innovative Drugs for Pets

“Even Higher Than” Innovative Drugs for Human Use

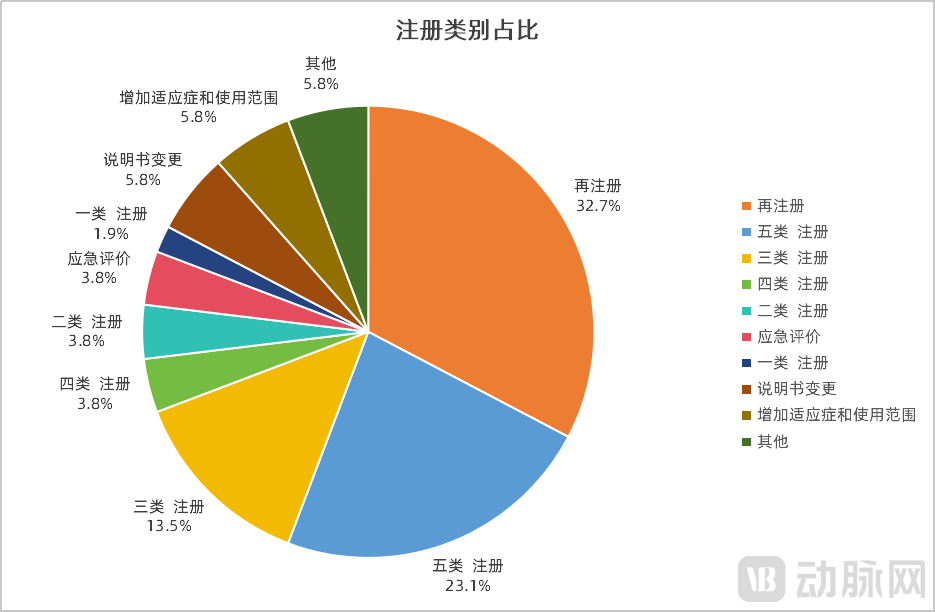

According to publicly available data, the Ministry of Agriculture and Rural Affairs approved a total of 52 pet drugs for registration or re-registration in China in 2024. Among these, 31 were domestically produced and 21 were imported, with the number of domestically produced pet drugs exceeding that of imported ones.

Notably, among the 52 veterinary drugs approved in 2024,Re-registration, Class III, Class IV, and Class V devices, label improvements, and emergency registrations account for over 40 products,Only one approved veterinary drug is classified as a Class I new veterinary drug, indicating that China’s capacity for independent R&D and industrialization of innovative veterinary medicines urgently needs to be strengthened.

According to incomplete statistics, the proportion of approved pet drugs by registration category in 2024. Graphic by VCBeat.

The only Class I new veterinary drug approved in 2024 was ritlecitinib and ritlecitinib tablets, developed and submitted by GeGewu (Zhuhai) Biotechnology, Elanco (Shanghai) Animal Health, and Elanco (Sichuan) Animal Health. This marks the second domestically developed Class I chemical veterinary drug to be approved for market launch in China after an eight-year gap. According to public information, the newly approved ritlecitinib is the third JAK kinase-targeting veterinary drug globally (the other two being Zoetis’s Apoquel and Elanco’s Zenrelia), and the first JAK inhibitor for dogs in China, providing a new therapeutic option for managing canine pruritus.

China’s Ministry of Agriculture and Rural Affairs approved its first Class I new veterinary drug for pets in March 2016, when “Vetacoxib Chewable Tablets (Bei’anke),” a chemically synthesized pet medication independently developed by Obofang, was granted approval as a Class I new veterinary drug. Vetacoxib Chewable Tablets marked a breakthrough in China’s original innovative pet chemical drugs, enabling the country to secure a “Best-in-Class” product in the global $1.8 billion pet pain management market.

Why Has China Seen Late and Low-Volume Commercialization of Innovative Veterinary Drugs? After extensive verification, VCBeat has concluded that the complexity of developing an innovative veterinary drug is no less than, and may even exceed, that of developing an innovative human pharmaceutical.

First, there is a relative scarcity of basic research on pet diseases in humans.Unlike pets, livestock and poultry are critical to public livelihood. China has made substantial research investments in these economic animals; by contrast, as the pet industry is an emerging sector, its foundational research and scientific funding still require strengthening.

Second, there is a lack of institutions in China that comply with the Good Clinical Practice (GCP) for veterinary drugs and are specifically dedicated to conducting clinical trials for pets.Development of innovative drugs for pets also requires preclinical studies, including toxicological safety assessment, pharmacological and efficacy evaluation, and pharmacokinetic studies. Clinical trials must be conducted in veterinary hospitals qualified under Good Clinical Practice (GCP) standards for veterinary drugs. According to the China Veterinary Drug Information Network, most GCP-compliant trial institutions focus on economic animals such as pigs, cattle, sheep, and poultry. Only a few institutions have the necessary capital to conduct clinical trials for pets, and most of these are affiliated with agricultural universities or animal health companies.

Third, due to species differences between pets and humans, not all drug development experiences from human medicine can be directly applied to veterinary drugs.Compared with the development of human drugs, the development of innovative veterinary drugs possesses unique characteristics spanning from reagent selection and analytical method establishment to animal model construction and formulation development. Luo Haoshu, founder of Weijiexin, told VCBeat, “The CMC processes and proprietary manufacturing technologies involved in the development of innovative veterinary drugs—particularly the technical expertise and data packages for emerging products such as antibody-based veterinary therapeutics—are held by a handful of leading animal health companies. For startups, the lack of publicly available reference materials necessitates that their R&D personnel possess extensive experience in both scientific research and industrialization.”

Furthermore, from the perspective of market behavior,Lu Kun, General Manager of GeGeWu Biology, analyzed, “Since human health is undoubtedly the top priority, researchers have conducted extensive and in-depth studies on human diseases, resulting in secondary market activity that is far more vibrant than that for innovative pet drugs. In comparison, the field of innovative pet drugs differs by an order of magnitude from that of innovative human drugs in terms of the number of R&D personnel, level of attention, and capital investment. Given these disparate foundational conditions, the R&D difficulty for innovative pet drugs is naturally much higher.”

Shi Liming, a partner at QinZhi ChongLe Fund, also told VCBeat, “The market size for pet pharmaceuticals is smaller than that for human drugs, and the return on investment is not as high. For certain complex diseases in pets, whether companies and capital choose to invest in R&D and production requires a careful balance between market potential and development costs, as well as adjustments to R&D strategies to meet the specific needs of pets.”

According to industry insiders, the development cycle for a Class I innovative veterinary drug (such as an mRNA vaccine or antibody-based therapy for pets) is generally around 6 to 8 years, with costs typically ranging from RMB 30 million to RMB 50 million.The lengthy development cycles and high costs pose significant challenges for most startup pet pharmaceutical companies.

Product selection is crucial,

Dermatology, age-related diseases, and oncology remain blue-ocean markets.

Compared to the common challenges faced by every innovative pet pharmaceutical company, such as technical hurdles in drug development and a general scarcity of foundational resources and funding,How to conduct differentiated product selection before project initiation is the key issue that tests whether innovative pet pharmaceutical companies can rise to the forefront by leveraging blockbusters.Globally, top-tier animal health companies all possess several flagship products that dominate the market. These products enjoy strong reputations and high market shares, making them unassailable by startup offerings in the short term.

A significant factor behind the success of Zoetis’s Apoquel lies in its successful product selection, which focused on the large and underserved market of canine dermatological diseases.Skin diseases are the most common ailments in dogs. In the Chinese market alone, the number of canine skin disease cases has increased by more than 30% for two consecutive years. However, China’s share remains low compared to the global market. Taking canine atopic dermatitis as an example, the diagnosis rate in China is 33%, significantly lower than the 90% reported in the United States. It is foreseeable that the Chinese market for canine skin diseases will continue to have substantial growth potential in the future.

Beyond canine dermatology, medications for age-related diseases in pets also represent a blue ocean market.According to data from the "2023–2024 White Paper on China's Pet Industry," it is projected that over 30 million pets in China will enter middle and old age within the next three years. Consequently, there will be a surge in the incidence of pet digestive disorders, metabolic diseases, cardiovascular and cerebrovascular conditions, endocrine disorders, and neurological diseases, making these areas new potential markets for veterinary pharmaceuticals. In addition, there is substantial demand for health supplements related to pet aging, such as products supporting gastrointestinal health, coat health, basic nutritional supplementation, and joint/bone health.

Moreover, much like in human medicine, oncology treatment for pets remains a significant challenge, and behind this challenge lies a vast untapped market.Currently, there are over a hundred anti-cancer drugs approved for marketing worldwide to treat human tumors, with approximately 1,300–1,500 various anti-cancer drug formulations prepared from these agents. In contrast, the number of drugs available for treating pet tumors is limited, with only a few mainstream products on the market, such as Zoetis’ tyrosine kinase inhibitor (TKI) Palladia and Merck’s PD-1 antibody Gilvetmab. Clearly, whichever veterinary pharmaceutical company next secures approval for its oncology drug will rapidly gain a first-mover advantage and capture this blue-ocean market.

Focusing on “product selection,” the innovative pet drug sector has spawned many interesting niches in recent years, with numerous companies even establishing strategic footholds in areas such as anti-motion sickness drugs, weight-loss medications, antidepressants, and contraceptives for pets.On the surface, these indications appear overly “gimmicky” compared to conditions that severely impair pets’ quality of life, such as oncologic diseases, dermatologic disorders, and age-related diseases. However, this is not the case.Shi Liming, a partner at Qinzhi Chongle Fund, told VCBeat that there is market demand for motion sickness medications, weight-loss drugs, and antidepressants, so they cannot be dismissed as mere “gimmicks.” However, the practice of overstating either the risks or the efficacy of these drugs remains open to debate.

For example, obesity,Pet owners today generally provide excellent care, leading to overfeeding and widespread obesity among pets, making weight loss necessary. However, there are various approaches to weight management, such as dietary restriction, adjusting dietary composition, or increasing physical activity. The market for non-prescription weight-loss medications targeting obesity not yet associated with disease exhibits strong consumer-driven characteristics. In contrast, obesity-related conditions such as heart disease, diabetes, and hypertension require professional medical treatment.

Furthermore, long-distance travel with pets has become increasingly common, making motion sickness a frequent issue.However, most cases of motion sickness in pets can be prevented. Measures include regulating the pet’s diet before travel, ensuring adequate ventilation in the vehicle during transport, creating a comfortable riding environment, or bringing small toys to distract the animal. For more severe cases of motion sickness, sedative products may be considered to alleviate symptoms.

On the other hand,Due to disease, castration, environmental changes, inadequate care by pet owners, etc.,Pet depression is not uncommon,Pet owners can alleviate symptoms by increasing exercise and spending more time with their pets, and may also use approved medications such as clomipramine and pregabalin under veterinary guidance.

Overall, innovative pet drugs with genuine market demand are essential medications.

In the short term, the pet pharmaceutical market resembles the consumer healthcare market.

Innovative Drug Costs Are Increasingly Covered by Commercial Insurance

After product selection and project initiation, balancing innovation with pricing remains a major hurdle to the commercialization of innovative pet drugs. The application of new technologies with superior therapeutic efficacy inevitably leads to higher costs. However, relevant regulations, pricing mechanisms, and medical insurance systems in the veterinary pharmaceutical sector still require further refinement. Therefore, how to ensure that pet owners remain willing to pay for high-quality products is a critical question that innovative pet pharmaceutical companies must address clearly from their inception.

How to Find a Reasonable Balance Between Drug Pricing and Sustained Innovation: Zhang Wei, Senior Investment Manager at QinZhi Capital, Analyzes a Multi-Layered Strategy

First, enhance market competition through policy design,For example, accelerating the research and development and market access of generic drugs, breaking the monopoly of veterinary channels on drug distribution, allowing more non-veterinary retailers to participate in sales, thereby reducing prices through supply and demand regulation.

Secondly, establish a systematic incentive mechanism to support innovation,including providing targeted tax incentives for pharmaceutical companies, establishing government- or industry-led R&D funding programs, and optimizing the drug approval process to shorten the cycle from laboratory to market, thereby reducing financial burdens on enterprises and improving returns on innovation.

Furthermore, to improve the accessibility of cutting-edge therapies, efforts can be made to encourage the pet insurance industry to expand its coverage.Include cell therapy and antibody drugs in the reimbursement list, while establishing special financial assistance programs to help pet owners with limited economic means share the treatment costs.

From a corporate perspective, Luo Haoshu, founder of Weijiexin, added further insights.“The ultimate payers for innovative pet drugs are ordinary consumers. While a segment of high-net-worth individuals may be less price-sensitive to these innovations, as a company, we still aim to deliver products that help pet owners reduce costs and enhance efficiency, pursuing a strategy of small margins but high sales volume. On the other hand, in my view,”"In the short term, the pet pharmaceutical market resembles the consumer healthcare market, with pet owners increasingly opting for commercial insurance to cover a portion of veterinary medication costs."

Lu Kun, General Manager of Gege Wu Biology, offered a new perspective, telling VCBeat, “Innovative drugs for pets are similar to innovative human drugs; the larger market is actually in Europe and the United States.”In the European and American markets, both insurance coverage and consumer spending power have led to a higher current acceptance of innovative pet pharmaceuticals. Therefore, Chinese pet pharmaceutical companies can target global demand for pet medications from the initial project planning stage, in preparation for subsequent entry into broader blue-ocean markets.”

For the global expansion of innovative veterinary drugs, pioneers have already paved the way:In early 2024, Elanco Animal Health reached a licensing agreement for lasutinib with Gegewu Bio, a portfolio company of Yinming Biologics.In October of the same year, Lishutinib Tablets were approved as a Class I new veterinary drug in China, marking the first JAK inhibitor for canine use in the country.As a pioneer in the global expansion of innovative Chinese pet pharmaceuticals, GeGeWu Biotech’s licensing collaboration with Elanco Animal Health represents a synergy between its R&D strengths and Elanco’s global resources, serving as a paradigm of “localized R&D + global strategy.”

Industry insiders revealed,Many domestic pet pharmaceutical companies have already begun negotiations with overseas multinational corporations (MNCs). In the future, the global expansion of innovative pet drugs will become an important pathway for pet pharmaceutical enterprises to achieve profitability and establish a global presence, mirroring the internationalization trajectory of innovative human pharmaceuticals.

Finally, Professor Luo Haoshu, founder of Weijiexin, candidly stated, “I personally believe that the window for the industrial boom in global innovative pet drugs has opened, but a fixed market landscape has yet to take shape. In the next three to five years, Chinese innovative pet drug companies will compete on the same stage as their global counterparts. Those who can deliver high-quality products rapidly, capture market share, and build a strong reputation will establish themselves in the innovative pet drug sector. If this critical period is missed, opportunities for overtaking competitors later will be slim.”

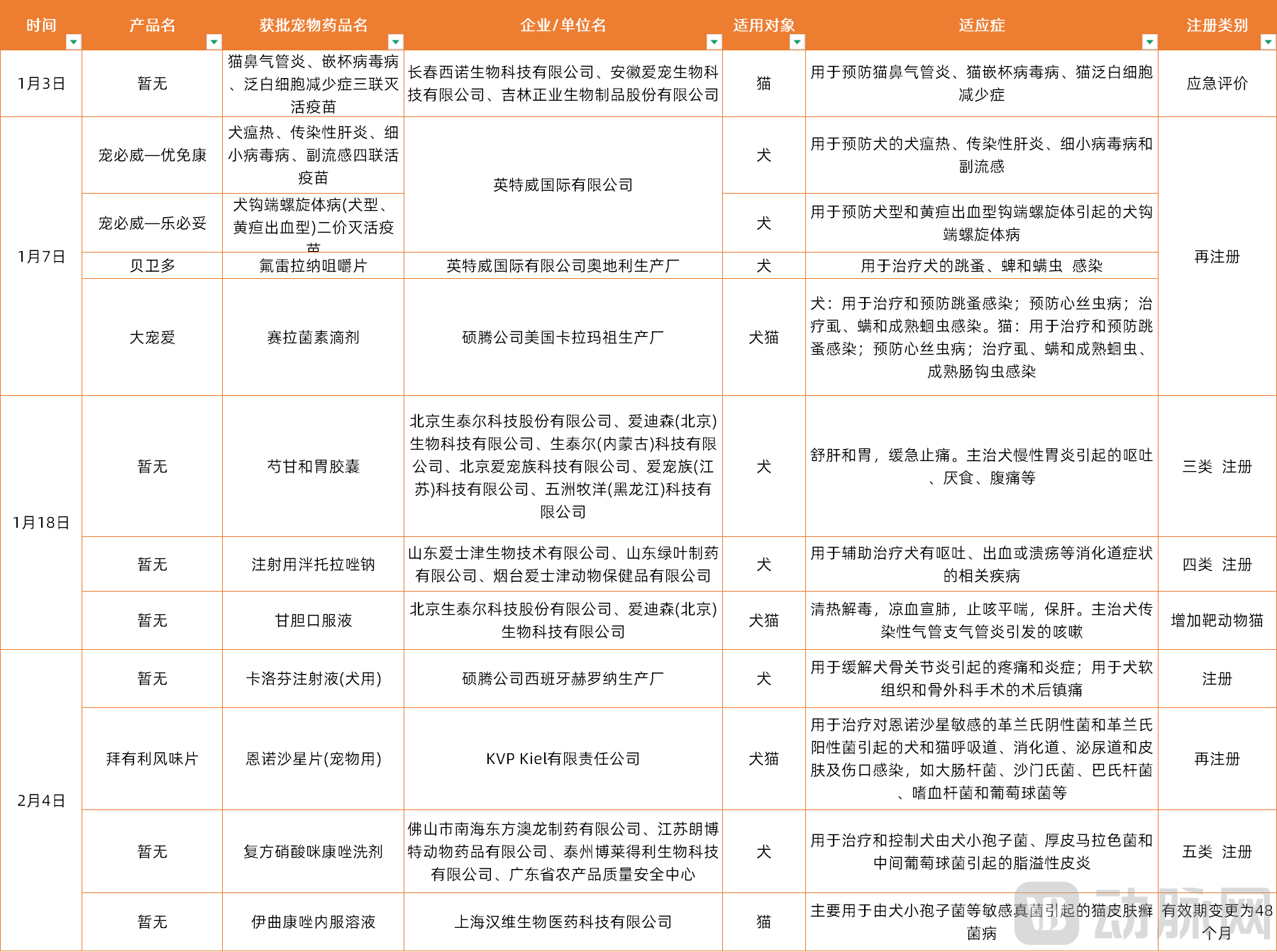

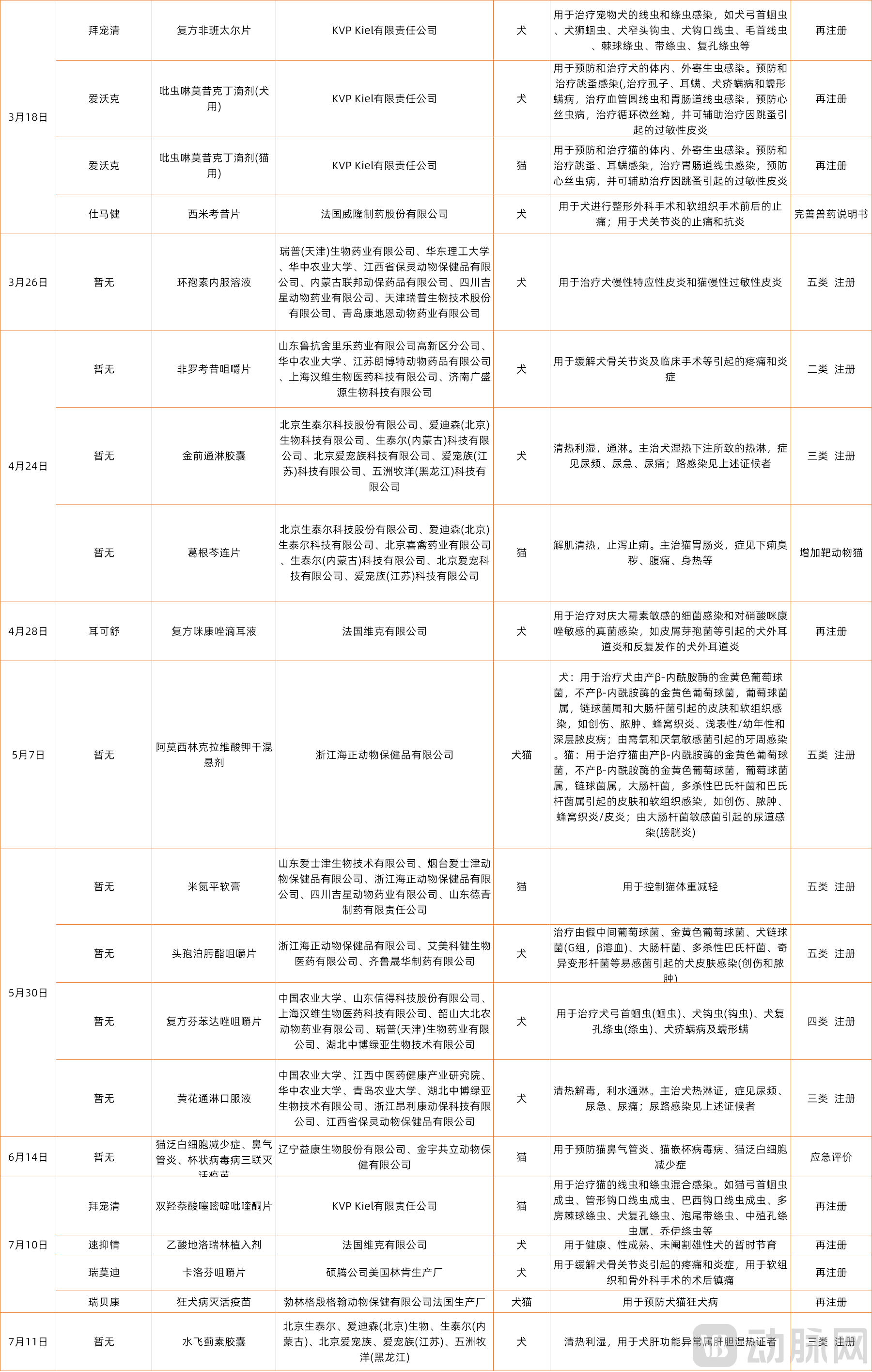

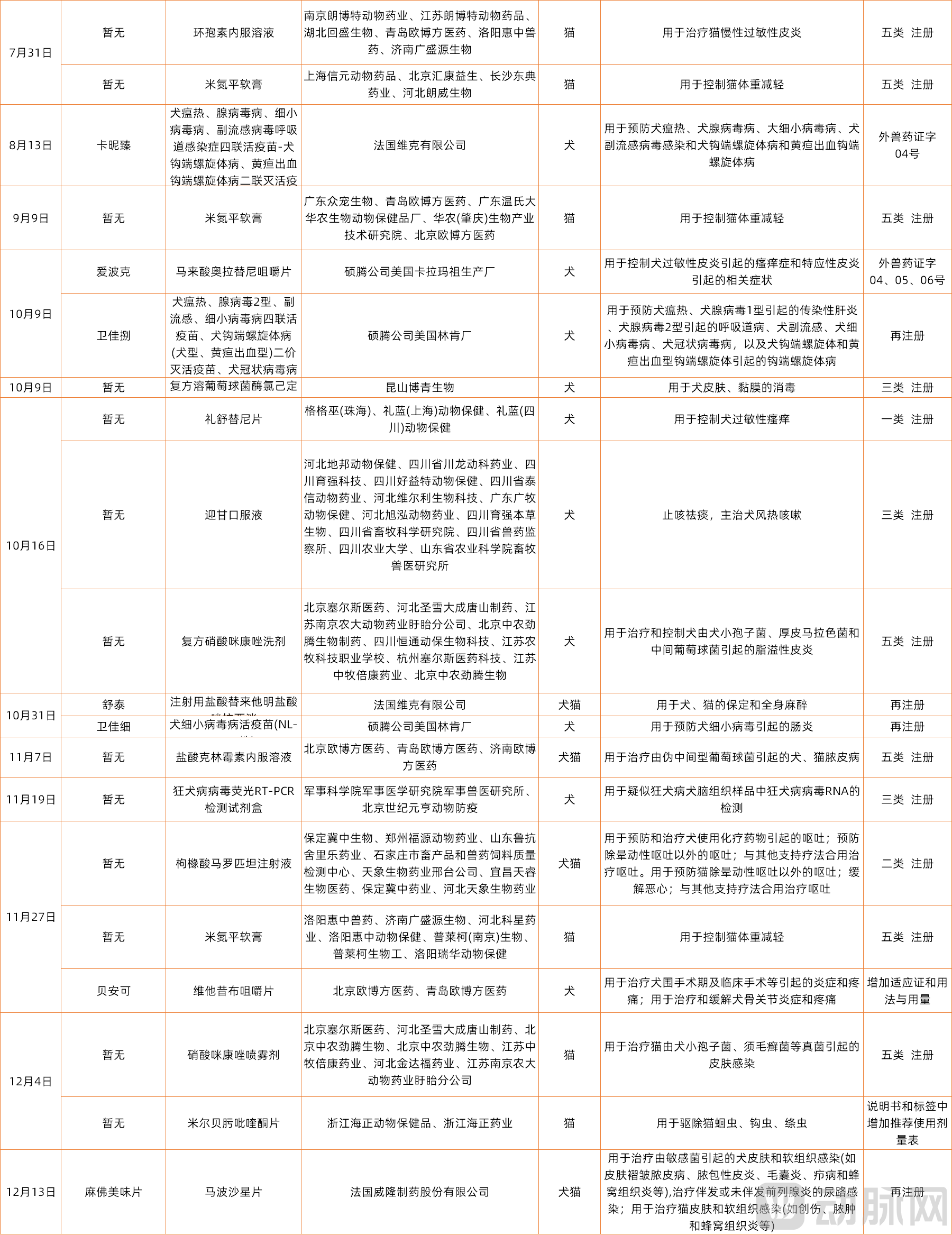

Below is the list of veterinary drugs approved in China in 2024:

References:

1. "Study on the Synthesis Process of Parecoxib"

2. “Research on the Policy, Regulatory, and Management System for Veterinary Drugs Used in Pets in China”

3. “Zoetis Upgrades and Launches Apoquel: A Proactive Move or a Reactive Response?”

4. “2024 Policy Review: Launch of the New Veterinary Drug Evaluation System and Increase in Import Tariffs on Pet Food to 10%”