From Pharma to High-End MedTech: How Chinese Drugmakers Are Building the Next Johnson & Johnson

Drug-Device Synergy Enters a New Era.

Over the past two years, domestic innovative drug companies have significantly boosted their revenues through business development (BD) deals; however, most of their product pipelines remain far from commercial realization. In the innovative drug industry, which operates on a 10-year cycle, pharmaceutical companies must identify new growth curves to achieve success. Medical devices are increasingly becoming the accelerator of choice for many of these firms.

It is hardly new for pharmaceutical companies to diversify into the medical device sector. However, many past cross-industry ventures focused on low-technology areas, lacking strategic objectives and driven primarily by short-term profit considerations. With the entry of Hengrui Medicine, the leader in innovative drugs, it is evident that pharmaceutical companies have entered a new era regarding pharmaceutical-device synergy. They are now leveraging their expertise in specific disease areas, identifying weaknesses within their ecological industry chain platforms, and seeking breakthroughs accordingly.

If pharmaceutical R&D is a race against time, then identifying the right balance in drug-device combination products represents a crucial step for Chinese pharmaceutical companies to build a new industrial ecosystem with Johnson & Johnson as their benchmark.

Hengrui Medicine has entered the field of medical devices.

As a leading innovator in China’s pharmaceutical industry, Hengrui Medicine boasts a robust product pipeline spanning oncology, cardiovascular diseases, autoimmune disorders, and other therapeutic areas. The commercial launch of key drugs—including imrecoxib, apatinib, pyrotinib, camrelizumab, and remimazolam tosylate—has driven sustained growth in the company’s sales.

However, what truly sets Hengrui apart from other companies is not only the richness of its R&D pipeline but, more importantly, its forward-looking strategic layout.

The 2015 drug review reforms ushered in an era of rapid growth for China’s innovative pharmaceutical industry. Yet in 2016, Hengrui invested RMB 500 million to establish Suzhou Hengrui Medical Devices Co., Ltd., focusing on the research and development of medical equipment, high-value consumables, and integrated solutions. Hengrui MedTech carries the strategic mandate of extending the group’s reach from the pharmaceutical sector into the broader healthcare industry.

In January 2025, the first fully domestically developed ECMO system, independently researched and developed by Suzhou Hengrui Medical Device Co., Ltd., officially received market approval from the National Medical Products Administration. This achievement marks a significant breakthrough in China’s independent research, development, and industrialization of high-end medical devices, breaking the long-standing foreign monopoly on related technologies.

The ECMO system approved for Hengrui Medicine consists of components such as the main console, circulation kit, arterial and venous cannulas, blood warmer, and puncture kit, marking the first fully domestically produced ECMO system in China. Its core components feature innovative technologies pioneered in China, including a fully magnetically levitated drive ECMO blood pump and multimodal control, ensuring high operational stability and low hemolysis. Clinical trial results demonstrated that the system met its predefined clinical endpoints, with no adverse events or device defects related to the investigational medical device reported, thereby exhibiting excellent efficacy and safety.

The successful approval of Hengrui’s ECMO system not only achieves the strategic significance of a breakthrough in the independent research and development of domestically produced equipment, but also realizes the tactical significance of significantly reducing clinical usage costs. This is because Hengrui has not only developed the device itself, but also mastered the manufacturing process for PMP (polymethylpentene) hollow fibers, the key material used in oxygenators. The bottleneck issue concerning raw materials will become a thing of the past, truly achieving full domestic substitution across the entire ECMO system industry chain.

Unlike some pharmaceutical companies that previously diversified into low-value medical devices, Hengrui has been fully committed from the outset to the research and development of high-end medical equipment and high-value consumables. Its approach comprehensively covers the entire lifecycle of medical devices, spanning from initial conceptual design to final clinical application, as well as breakthroughs in consumable technologies.

This intensive and meticulous R&D effort has propelled Hengrui to prominence. Beyond ECMO, Hengri has established a broad presence in the fields of oncology intervention, peripheral intervention, and neurointervention, with ongoing development of products such as CVAD (catheter-based ventricular assist device) and IABP (intra-aortic balloon pump).

As can be seen, the majority of projects currently selected by Hengrui are dominated by foreign brands; for instance, the ventricular assist device (VAD) market is occupied by Abbott and Johnson & Johnson. Upon its initial entry into the medical device sector, Hengrui targeted the opportunity for domestic substitution of high-end medical devices. More importantly, leveraging Hengrui’s accumulated expertise in the pharmaceutical industry, the future innovative strategy of pharmaceutical-device synergy will become the core driver of Hengrui’s differentiated competition, although this path is not without challenges.

It took Salubris 16 years to gain initial insights into the synergistic development of pharmaceuticals and medical devices.

Speaking of Salubris, this established pharmaceutical company, founded in 1998, has had its moments in the spotlight. In 2018, it achieved annual operating revenue of RMB 4.652 billion and net profit of RMB 1.458 billion, making it highly sought after by secondary market investors. However, an unexpected loss of bid in the 2019 volume-based procurement led to a continuous decline in its performance, highlighting significant operational pressures.

Fortunately, upon its listing in 2009, Salubris established a wholly-owned subsidiary, Shenzhen Salubris Biomedical Engineering Co., Ltd., to engage in the research and development of medical devices, and has been continuously building its in-house R&D capabilities over the subsequent decade. After years of development, with a total investment exceeding RMB 1 billion, the company has built several technology platforms centered on drug-loading core technologies, including a drug-eluting stent coating technology platform, a drug-coated balloon technology platform, a precision targeted drug delivery technology platform, as well as structural design and processing technologies for various alloy materials.

Amidst continued performance declines and eroding market share, Salubris has accelerated its transformation, establishing a dual development strategy focused on both innovative drugs and medical devices.

In the field of medical devices, Salubris has established a presence across four key segments—cerebrovascular, cardiovascular, cardiac structural heart, and peripheral vascular—as well as six major clinical departments: cardiology, cardiac surgery, neurology, neurosurgery, nephrology, and vascular surgery. In the area of neurointervention, the Maurora sirolimus-eluting vertebral artery stent system had cumulatively been implanted in over 50,000 cases by the end of 2024. Additionally, products such as the AlphaStent coronary stent and the LAMax left atrial appendage occluder have successively received regulatory approval and been launched on the market.

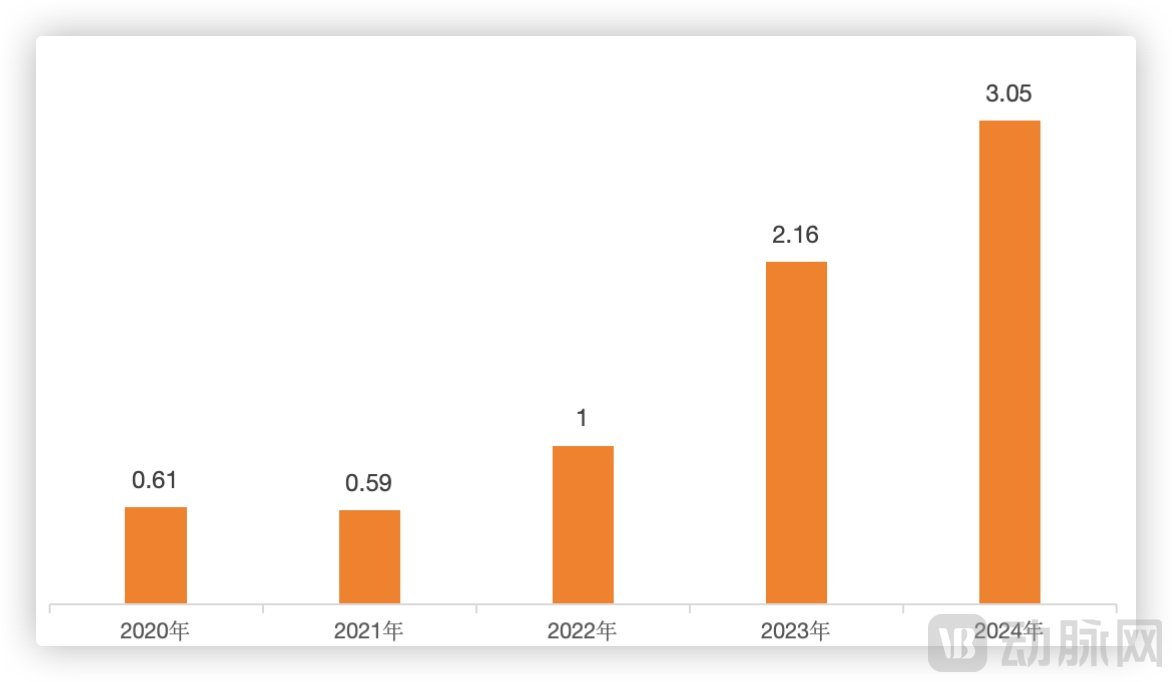

Salubris's Medical Device Business Revenue in Recent Years (Unit: 100 Million Yuan), Data Sourced from Corporate Financial Reports

From a revenue perspective, although the medical device business has experienced rapid growth, its base remains relatively small. In 2024, revenue from medical devices reached RMB 305 million, representing a year-on-year increase of 41.68%, yet accounting for less than 10% of total revenue. Notably, the core device product, the sirolimus-coated drug-eluting balloon, generated RMB 137 million in revenue, with a gross profit margin as high as 75.5%.

From the results, although Salubris aims to achieve synergistic integration of pharmaceuticals and medical devices in its core business areas by attempting to provide comprehensive solutions for relevant departments—particularly targeting the chronic disease sector where physicians’ prescribing habits are relatively entrenched—it seeks to continuously strengthen its business model through an integrated “drug + device + service” approach. However, in actual implementation, the synergy between pharmaceuticals and medical devices has not yet yielded the desired outcomes. The commercialization of medical devices is a long-term process, and it will take time to achieve economies of scale.

Salubris has also recognized that the sluggish progress in medical device R&D has hindered the large-scale implementation of its integrated pharmaceutical-device business model, and has begun to introduce AI technologies in an effort to accelerate development speed.

For instance, during the development of left atrial appendage (LAA) occluders, AI is leveraged to analyze extensive clinical data, thereby optimizing the device’s shape, size, and materials to better accommodate the diverse LAA anatomies and physiological needs of different patients. During clinical trials, the integration of AI enables in-depth mining of massive datasets, uncovering latent correlations and patterns among data points. This facilitates a more robust assessment of the device’s performance and safety, providing an evidence base for product improvement and optimization.

From past glory to setbacks, Salubris proactively entered the medical device sector through forward-looking strategic planning. Today, its integrated pharmaceutical and device strategy is being steadily implemented, with initial success in its strategic transformation. Looking ahead, Salubris will continue to integrate multimodal solutions centered on diseases, enhancing both clinical value and commercial barriers. This serves as a classic case of Chinese pharmaceutical companies exploring the “pharmaceutical-device synergy” ecosystem.

Technological synergy in building a closed-loop diagnosis and treatment system has become a key pillar of Grand Pharma’s ecosystem strategy.

When it comes to Grand Pharma, its extensive layout in the field of nuclear medicine must be mentioned. Its pipeline involves 12 innovative drugs, covering five radionuclides including 68Ga, 177Lu, 131I, 90Y, and 89Zr, and spanning seven cancer types such as liver cancer, prostate cancer, and brain cancer. It has achieved a comprehensive layout across multiple segments, including R&D, production, sales, and regulatory qualifications for nuclear medicines, and is steadily advancing the construction of a domestic Class A qualification radionuclide production platform.

However, as early as 2015, Grand Pharma focused on addressing clinical pain points and benchmarked against globally advanced products and technologies, establishing a comprehensive layout in three areas: vascular access management, structural heart disease, and electrophysiology and heart failure. Currently, there are 16 products in its medical device segment, with multiple products in the field of vascular access management already approved and marketed in China. Grand Pharma has established an innovation platform for the development of both passive and active medical devices, forming a R&D and production network with four centers in China and multiple bases overseas, while actively constructing new R&D centers and platforms both domestically and internationally.

Grand Pharma’s Portfolio of Precision Interventional Devices for Cardiovascular and Cerebrovascular Diseases, Data Sourced from the Company’s Official Website

From a product perspective, Grand Pharma has sequentially rolled out three drug-coated balloon products—RESTORE, APERTO, and LEGFLOW—entering the high-end medical device sector for cardiovascular and cerebrovascular diseases; it has deployed NOVASIGHT, an innovative intravascular imaging diagnostic device, laying a solid foundation for an integrated platform of precision interventional diagnosis and treatment; it has introduced HeartLight X3, a next-generation laser ablation platform for atrial fibrillation treatment, thereby entering the electrophysiology segment; and it has launched the CoRISMA series for heart failure treatment and an intravascular lithotripsy system for treating arterial calcification.

Grand Pharma’s medical device strategy focuses on differentiation. Taking drug-coated balloons as an example, unlike traditional drug-eluting stents, they can dilate narrowed blood vessels and rapidly release drugs to the vessel wall, effectively reducing the likelihood of restenosis.

Upon its market launch, the Restore drug-coated balloon was the first in China to carry dual indications for both de novo coronary artery lesions and in-stent restenosis. Subsequently approved, APERTO is the first drug-coated balloon indicated for stenosis of arteriovenous fistulas in dialysis patients. Featuring both high-pressure resistance and a drug coating, it significantly outperforms conventional high-pressure balloons in prolonging fistula patency and improving the quality of life for dialysis patients.

NOVASIGHT, approved in May 2023, is the first device capable of simultaneously utilizing intravascular ultrasound (IVUS) and optical coherence tomography (OCT) for invasive coronary assessment. This synchronous imaging approach provides physicians with more detailed and accurate data, facilitating improved evaluation and treatment of cardiovascular diseases. Furthermore, this integrated two-in-one solution eliminates the need for hospitals to purchase two separate systems, thereby streamlining operational workflows and reducing costs.

Furthermore, Grand Pharma’s DEEPQUAKE Peripheral Vascular Shockwave System has also received marketing approval. This system delivers non-focused pulsed acoustic pressure waves to the lesion site during low-pressure balloon dilation, effectively disrupting both superficial and deep calcification while sparing vascular soft tissue. This enables precise “translesional” therapy, significantly enhancing safety.

In addition to product differentiation, the establishment of a synergistic ecosystem among products is also a major feature of its medical device strategy.

Taking the field of vascular intervention as an example, Grand Pharma has built a precise interventional diagnosis and treatment platform for cardiovascular and cerebrovascular diseases by leveraging its comprehensive, integrated solution comprising drug-coated coronary balloons, the NOVASIGHT intravascular dual-modality imaging system, and shockwave calcium modification systems. This approach aligns with the post-centralized procurement trend, where innovation in single products is prone to intense market saturation, while clinical practice increasingly demands greater synergy among different medical devices.

After years of in-depth development in the medical device sector, Grand Pharma’s active medical device R&D and production base in Wuhan Optics Valley and its passive medical device R&D and production base in Changzhou have both been put into operation. Additionally, the Shanghai Medical Device R&D Center, focusing on structural heart disease, has been officially established. Furthermore, R&D centers have been set up in countries such as the United States and Australia, marking the commencement of a globalized R&D initiative.

Thanks to these strategic initiatives, Grand Pharma has expanded its innovative footprint beyond vascular intervention to cover niche segments such as neurointervention, structural heart disease, electrophysiology, and heart failure, with the aim of building a new ecosystem centered on a cluster of high-end medical device products.

Behind Domestic Pharmaceutical Companies' Foray into the Medical Device Sector Lies Insight into Industry Development.

When it comes to pharmaceutical-medical device synergy, Johnson & Johnson is an unavoidable benchmark. After decades of comprehensive strategic deployment and ecosystem integration, Johnson & Johnson has not only achieved significant accomplishments in the pharmaceutical sector but also established multiple medical device industry chains covering surgical instruments, cardiovascular interventions, and aesthetic medicine equipment. Leveraging its global capabilities, Johnson & Johnson has implemented this ecosystem across global markets. As of the first quarter of 2025, the company’s healthcare business revenue reached $8 billion, with over 50% derived from overseas markets.

Compared with Johnson & Johnson, domestic pharmaceutical companies’ path toward pharmaceutical-device synergy is still in its early stages.

On one hand, Johnson & Johnson has emerged as a leader across multiple fields after decades of development, establishing a comprehensive suite of solutions. In contrast, while Chinese pharmaceutical companies have recognized the vast potential of the pharmaceutical and medical device ecosystem, they remain in the early stages of achieving technological self-sufficiency.

Taking Hengrui as an example, although the core materials and components of ECMO have achieved full domestic production in China, and its percutaneous left ventricular assist system has entered the Green Channel for expedited regulatory review, its internationalization process is still in its infancy, with future development remaining to be tested. Meanwhile, in terms of ecosystem building, Hengrui currently relies on independent R&D and has not yet undertaken industrial integration.

Hengrui’s current situation is a microcosm of Chinese pharmaceutical companies diversifying into the medical device sector. Its emergence has been driven by both policy support and genuine market demand, benefiting from the technological accumulation achieved during the recent wave of domestic substitution, which has enabled Chinese enterprises to continuously iterate as they transition from imitation to innovation. Inspired by these vivid examples, an increasing number of pharmaceutical companies are following suit. For instance, Buchang Pharmaceuticals, a long-established leader in traditional Chinese medicine, announced in March that it would invest in establishing Suzhou Hepu Medical Devices.

Although Chinese companies still lag behind Johnson & Johnson in terms of globalization capabilities and ecosystem building, they have already demonstrated their potential along this development path. Perhaps becoming the next Johnson & Johnson is merely the starting point; the ultimate goal for Chinese pharmaceutical companies is to forge a synergistic pharmaceutical-medical device ecosystem tailored to their own development needs.