2025 Report on High-End Ophthalmic Devices: Domestic Brands Poised for Full Rise and Market Restructuring

In recent years, the domestic high-end ophthalmic equipment sector has emerged as a powerful force. Driven by sustained growth in market demand and supportive policies for import substitution, numerous Chinese brands have sprung up like mushrooms after rain. Some of their products have even demonstrated robust competitiveness, rivaling or even surpassing traditional imported brands.

However, with the surge in the number of domestically produced ophthalmic devices on the market, including the rapid growth of both products under development and those already approved, how to accurately identify which domestic products truly possess differentiated competitiveness and can effectively meet actual clinical needs has become a critical issue that urgently needs to be addressed.

Centered on the theme of “Uncovering the Product Strength of Domestic Brands,” this report aims to reflect the true product competitiveness of Chinese brands by examining clinical needs assessments, NMPA approval status, financing activities, commercialization progress, global expansion strategies, and comparisons of core product parameters.

Core Viewpoints:

Both financing activity and the number of approvals showed positive trends.In terms of financing, from January 1, 2024, to the end of March 2025, there were 14 financing deals in the domestic ophthalmic equipment sector exceeding RMB 100 million each, accounting for 54% of the total. Regarding NMPA approvals, 121 high-end ophthalmic devices received approval from the National Medical Products Administration (NMPA). In certain product categories, such as ophthalmic OCT and optical biometers, the number of approved domestically manufactured products has surpassed that of imported ones, indicating that the industry is in a stage of rapid development.

The localization process for diagnostic equipment is progressing at a faster pace overall.Domestic ophthalmic OCT devices, driven by innovations in swept-source technology, have achieved comprehensive breakthroughs in scanning speed, imaging depth, range, and resolution. Their technical specifications now surpass those of comparable imported products, earning recognition in both domestic and overseas markets. The performance of certain domestically produced optical biometers has reached parity with imported counterparts, positioning them to increase their share of the high-end market in the future. The number of approved domestic ultra-widefield fundus cameras has surged, with key parameters demonstrating strong performance, steadily narrowing the market share gap with leading imported products. In the intraocular pressure (IOP) measurement sector, Chinese companies are leveraging pioneering technological breakthroughs to address long-standing challenges, such as inaccurate IOP readings and the inability to achieve 24-hour continuous IOP monitoring.

The localization process for therapeutic devices has been relatively slow.There are currently no domestically approved products for femtosecond laser systems and combined phacoemulsification-vitrectomy machines, with only a few companies in the R&D stage. Although there are many domestically approved ophthalmic surgical microscopes, the market is heavily dominated by imports; most domestic products fail to meet basic standards, and there has long been a gap in high-end offerings.

In the future, manufacturers of high-end ophthalmic equipment can build long-term competitiveness from multiple dimensions.A comprehensive product portfolio strategy is of significant importance. Companies should also focus on high-potential products such as ophthalmic surgical robots, establish long-term brand strategies to narrow the gap with overseas brands, and firmly pursue global expansion. By leveraging technological innovation and high value-added products, they can penetrate developed markets in Europe and the United States.

High-end ophthalmic equipment encompasses multiple specialized product segments, with dozens of major device types that can be broadly categorized into diagnostic and therapeutic devices.

Classification of Ophthalmic Equipment

This report identifies the following as key product areas for in-depth study, based on a multi-dimensional analysis encompassing market size, the importance of products in ophthalmic diagnosis and treatment, current status, and future prospects: Optical Coherence Tomography (OCT), optical biometers, ultra-widefield fundus cameras, corneal biomechanical analyzers, continuous intraocular pressure monitoring systems, ophthalmic surgical microscopes, femtosecond laser systems (SMILE), integrated phacoemulsification and vitrectomy machines, and ophthalmic surgical robots.

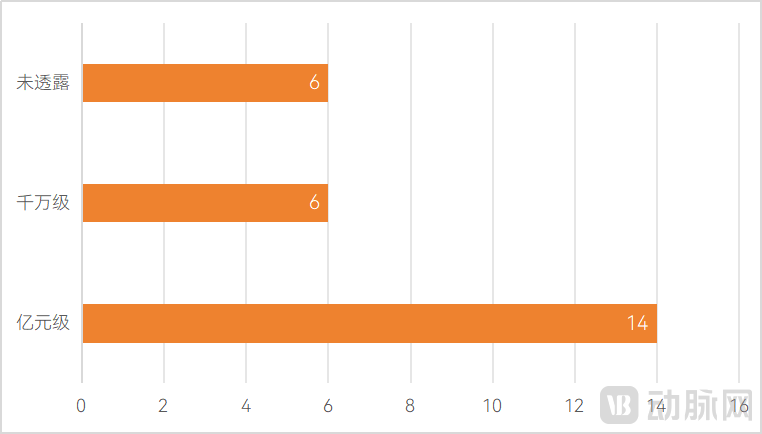

Ophthalmic Equipment Financing Remains Relatively Active, with Over 50% of Deals Valued at RMB 100 Million or More

A high proportion of large-scale financing events.From January 1, 2024, to the end of March 2025, there were 14 financing deals in China’s ophthalmic equipment sector valued at over RMB 100 million each, accounting for 54% of the total number of such deals. The profit-driven nature of capital dictates its flow toward sectors with high growth potential, indicating that the ophthalmic equipment field is highly favored by investors in the current market.

Distribution of Financing Amounts in China's Ophthalmic Equipment Sector in 2024

Distribution of Financing Amounts in China's Ophthalmic Equipment Sector in 2024

From the perspective of specific product sub-segments, products with low domestic production rates and high technical barriers have attracted more extensive capital investment.Represented by SMILE laser systems, combined phacoemulsification and vitrectomy machines, ophthalmic surgical microscopes, and ophthalmic surgical robots, these high-end ophthalmic devices face significant technical R&D barriers. Currently, domestically produced products hold a low market share, making them a focal point for capital investment. Meanwhile, companies with more comprehensive product lineups and faster commercial progress have also attracted substantial attention from investors.

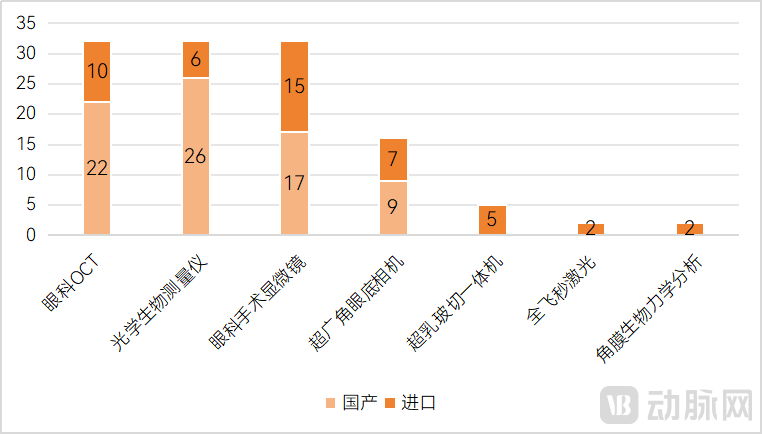

121 Products Approved; Domestic Approvals Surpass Imports in Multiple Product Categories

As of February 7, 2025, a total of 121 high-end ophthalmic devices have received NMPA approval.

The approval progress of domestically produced optical biometers and ophthalmic OCT devices has been particularly significant.There are 32 ophthalmic OCT products approved by the NMPA, with domestically produced products accounting for 68.7%; there are 32 optical biometers, with domestically produced products accounting for 81.2%; there are 32 ophthalmic surgical microscopes, with domestically produced products accounting for 53.1%; and there are 16 ultra-widefield fundus cameras, with domestically produced products accounting for 56.2%.

Classification of High-End Ophthalmic Equipment Approved by the NMPA

Classification of High-End Ophthalmic Equipment Approved by the NMPA

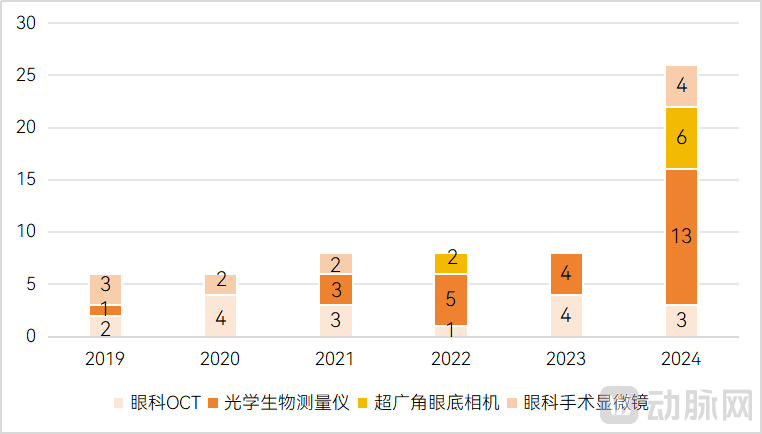

Based on the initial registration dates, the localization process for ophthalmic OCT and ophthalmic surgical microscopes started relatively early. One domestically produced ophthalmic OCT was approved in 2014, and a domestically produced ophthalmic surgical microscope received approval in 2015. Femtosecond laser systems and combined phacoemulsification-vitrectomy machines have seen the slowest progress in localization, with no domestically produced products approved to date.

In 2024, the domestic high-end ophthalmic equipment sector witnessed a significant surge. That year saw a substantial increase in the number of approvals for domestically produced optical biometers and ultra-widefield fundus cameras.

Distribution of NMPA Approval Years for Domestically Produced High-End Ophthalmic Equipment in Recent Years

Distribution of NMPA Approval Years for Domestically Produced High-End Ophthalmic Equipment in Recent Years

This chapter focuses on eight major categories of high-end ophthalmic equipment: optical coherence tomography (OCT), optical biometers, ultra-widefield fundus cameras, corneal biomechanical analyzers, continuous intraocular pressure monitoring systems, ophthalmic surgical microscopes, femtosecond laser systems, and combined phacoemulsification and vitrectomy machines. It analyzes the strength and potential of domestically produced products from multiple dimensions, including product parameter analysis, commercial performance, and global expansion strategies.

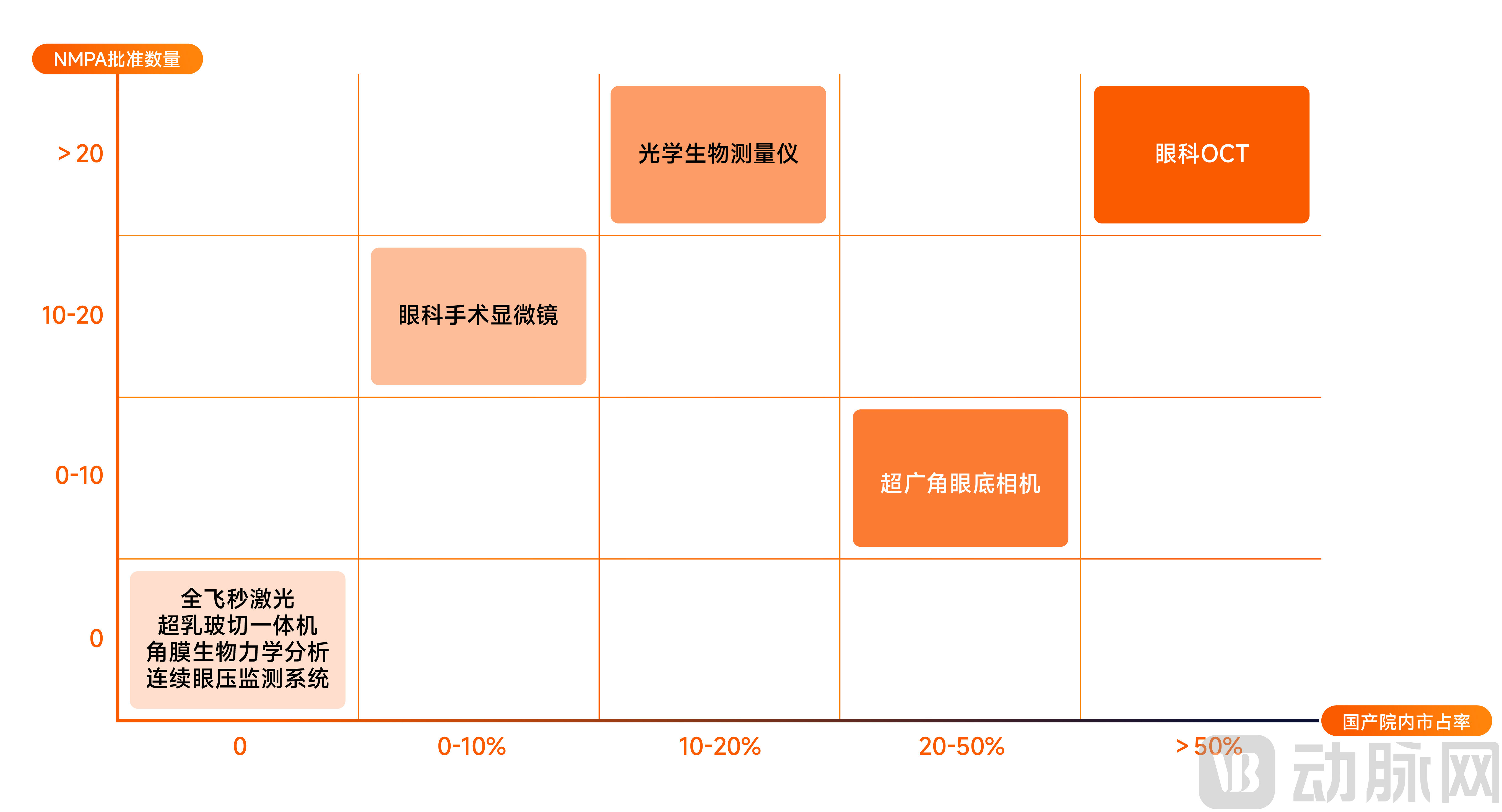

Assessment of the Competitiveness of Domestic Products in Key Product Segments

Assessment of the Competitiveness of Domestic Products in Key Product Segments

Ophthalmic OCT: Chinese Brands Overtake on the Curve, with Domestic Market Share Exceeding 50%

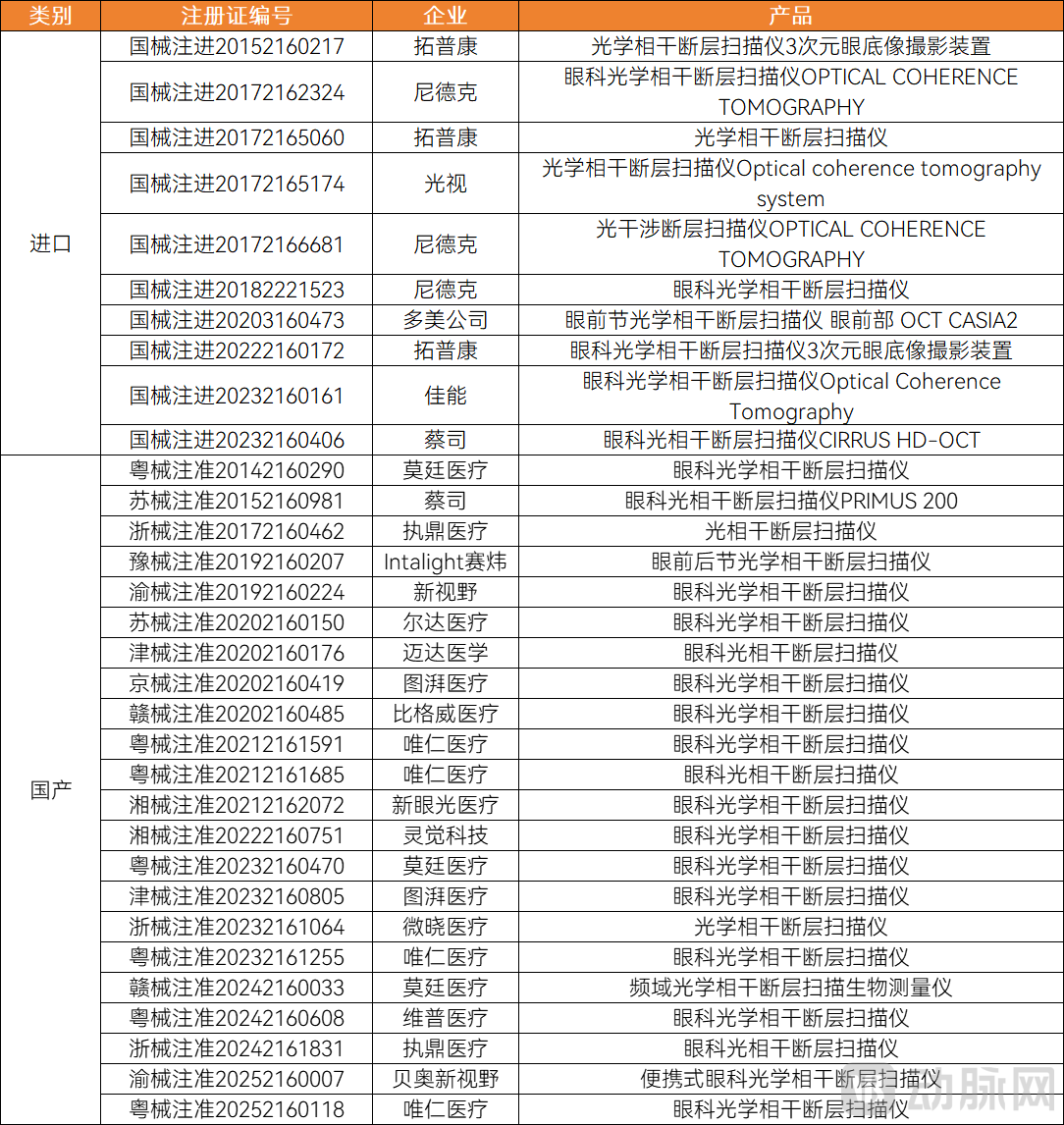

OCT is widely recognized as the high-end ophthalmic device with the fastest pace of localization.First, this is reflected in the number of registrations.The number of domestically produced ophthalmic OCT devices approved by the NMPA has far exceeded that of imported ones. According to statistics from VBInsight, as of February 7, 2025, a total of 32 ophthalmic OCT products had received NMPA registration certificates, with 22 being domestically produced, giving domestic products a significant numerical advantage.

Ophthalmic OCT Products Approved by the NMPA

Ophthalmic OCT Products Approved by the NMPA

Secondly,This is reflected in the performance of core parameters of domestically produced products.According to VBInsight statistics, leading domestically produced products have already demonstrated performance surpassing that of imported counterparts in terms of scanning speed, imaging depth, imaging range, and imaging resolution.

Furthermore,This is reflected in the market share and pricing of domestically produced products.According to Frost & Sullivan data, the number of publicly accessible winning bids for ophthalmic OCT devices in public hospitals in 2023 was 404 units, with the market share of domestically produced products exceeding 50%. Furthermore, the average winning bid price for products from leading domestic enterprises was approximately RMB 1.5 million, which is higher than that of imported products.

This series of data indicates that leading domestic enterprises outperform imported brands in both market share and pricing. This demonstrates that domestic products are not competing solely through traditional low-price strategies; rather, their technological and brand value-added have gained recognition from hospitals. This marks a milestone where domestic products possess the capability to compete head-on with imports across key dimensions, including technology, performance, after-sales service, and price.

Domestic ophthalmic OCT can achieve the aforementioned superiority over imported products, primarily due to breakthroughs and leadership in swept-source OCT technology.The slow pace of upgrades for imported products is partly due to potential incompatibilities between upgraded technologies and existing database and algorithm systems, and partly because their customer base in Europe and the United States is concentrated in the private ophthalmology clinic market, where budgets are tight while swept-source OCT costs remain high. These factors have created opportunities for domestically produced products to overtake their competitors.

Optical Biometers: The Gap with Imported Devices Is Narrowing, but Hospitals Lack a Path to Overtake on the Bend

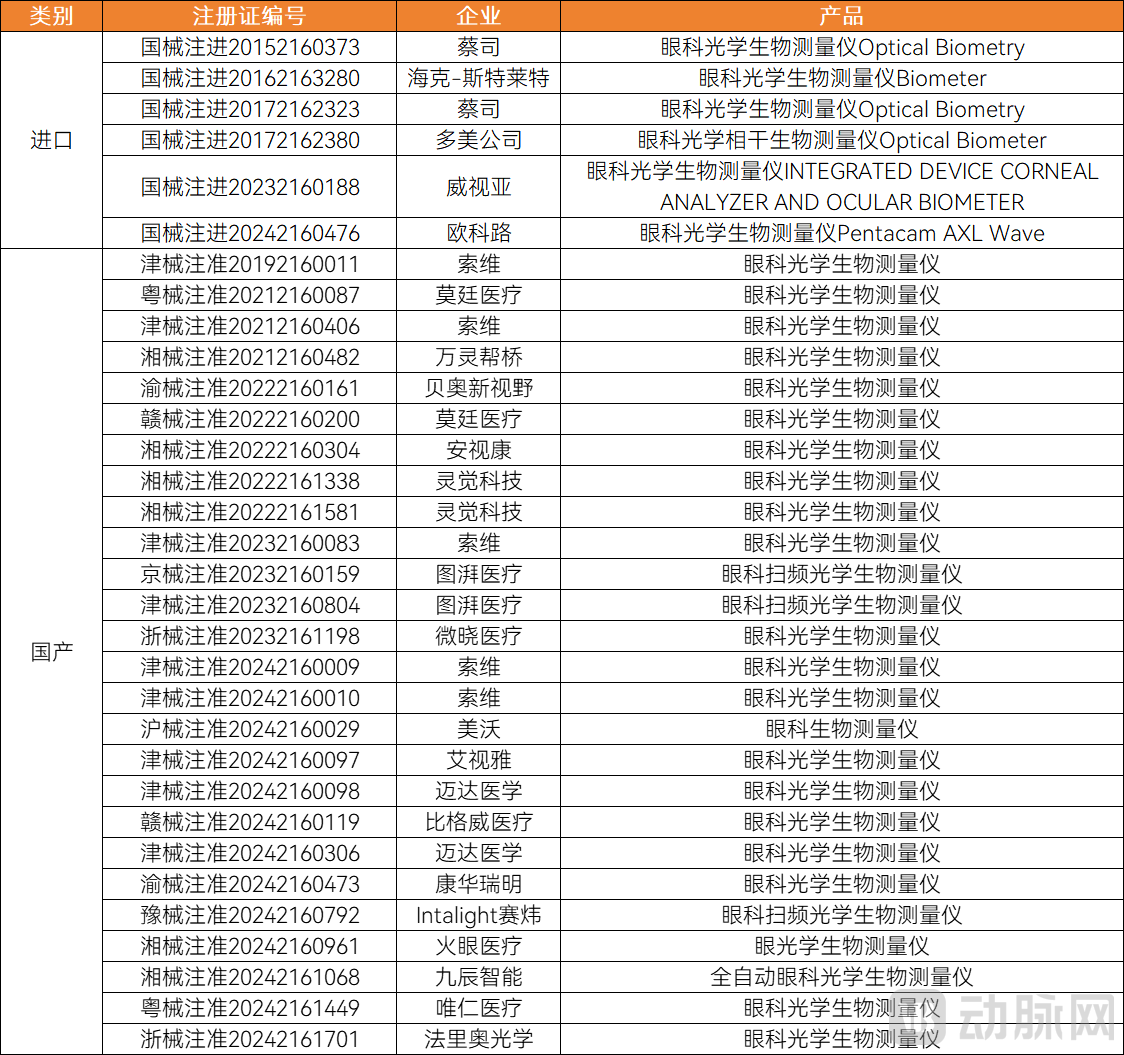

From the perspective of NMPA approvals, domestically produced optical biometers account for a substantial 81.2% of the total. As of February 7, 2025, a cumulative total of 32 optical biometers have received NMPA approval, including 26 domestically manufactured models and 6 imported ones. The 81.2% share of domestic products fully demonstrates their strong competitiveness in market access.

NMPA-Approved Optical Biometer

NMPA-Approved Optical Biometer

However, in the traditional medical market, domestically produced products have a low market share, largely due to limitations in product performance.VBInsight’s research reveals that there is significant market potential for biometers used in myopia control and prevention in lower-tier markets. However, this sector features low technological barriers and entry thresholds, leading to intense competition among domestic manufacturers, primarily driven by price wars. Currently, the specifications of domestically produced optical biometers generally meet only the basic requirements for myopia management, with suboptimal precision, although they offer certain advantages in terms of portability and cost. In contrast, Chinese-made products capable of meeting the high-precision, high-stability, and high-repeatability demands of critical clinical settings remain extremely scarce.

Previously, the high-end optical biometer market was long dominated by imported brands such as the Zeiss Master series, with the IOLMaster 700 series holding a significant market share advantage after a decade on the market. As cataract surgery enters the refractive era, clinical requirements for preoperative, intraoperative, and postoperative stages have increased, necessitating higher measurement accuracy and stability from optical biometers.

Now, domestically produced devices have achieved technological breakthroughs, with some products demonstrating performance metrics that surpass imported counterparts, significantly enhancing the clinical value of Chinese-made equipment in the high-end market.

Ultra-Widefield Fundus Camera: Surge in Approvals for Domestically Produced Models, Poised to Overtake Competitors

Fundus examination equipment is evolving from conventional narrow-field imaging to ultra-widefield imaging, upgrading from optical systems to laser-based cameras, and advancing from single-modality detection to multi-modal and full-modality detection. This trend is not only evident in the ophthalmic OCT sector but also prominently reflected in the field of fundus cameras. Driven by this shift, the fundus camera market is rapidly transitioning from the red ocean of competition among standard fundus cameras to the blue ocean of ultra-widefield fundus cameras.

NMPA-Approved Ultra-Widefield Fundus Camera

In terms of product performance, imported products exhibit technological differentiation, with none yet able to perfectly balance imaging range and color fidelity. Furthermore, multiple domestic enterprises are strategically prioritizing ultra-widefield fundus cameras as key products; it is projected that within the next five years, domestically produced models will surpass imported ones, achieving substantial localization.

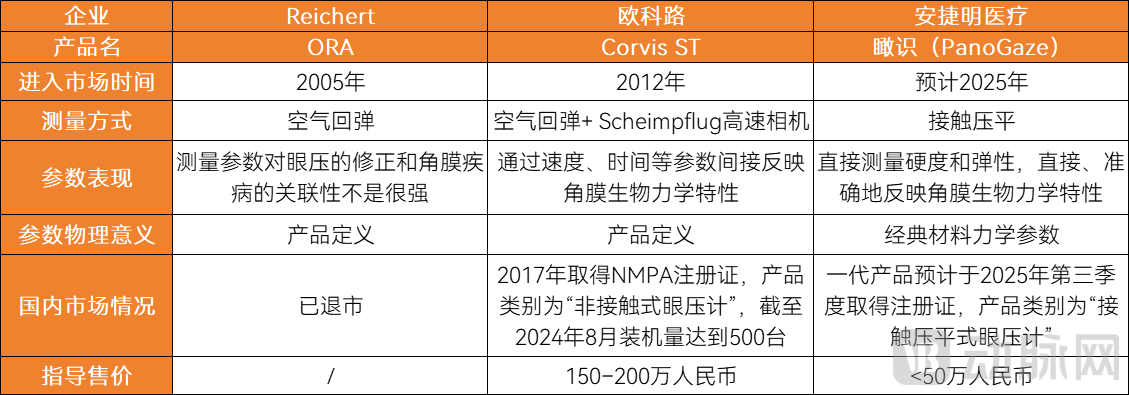

Corneal Biomechanical Analyzer: Pioneering Direct Measurement of Stiffness/Modulus Technology, Domestically Produced Model Coming Soon to Market

Although tonometers have been used in clinical practice for many years, accurate measurement of true intraocular pressure (IOP) remains a significant clinical challenge. An increasing number of scholars recognize that the biomechanical properties of the cornea are a core factor affecting the accuracy of true IOP measurements. Due to limitations in their underlying technical principles, traditional tonometers rely on idealized, uniform assumptions and fail to account for individual variations in corneal biomechanics, resulting in systematic errors in measurement outcomes.

Corneal biomechanical analyzer provides a reliable method for intraocular pressure measurement in clinical practice by analyzing the corneal biomechanical properties of different patients and correcting intraocular pressure calculations.

Two corneal biomechanical analyzers have previously been marketed: the Ocular Response Analyzer (ORA) launched by Reichert in the United States, and the Corvis ST launched by Oculus Optikgeräte in Germany. The ORA has since been discontinued, and there are currently no domestically produced products available on the market.

Global Corneal Biomechanical Analyzer

Global Corneal Biomechanical Analyzer

Continuous Intraocular Pressure Monitoring: Urgent Clinical Needs to Be Met, with Chinese-Made Devices Already Enabling 24-Hour Automated Home Monitoring

The clinical community has long recognized the necessity of continuous intraocular pressure (IOP) monitoring. However, due to the lack of ideal products, clinicians must rely on traditional single-point tonometers, performing measurements every 2–3 hours through “multiple single-point tests” to generate an IOP profile that reflects 24-hour IOP fluctuations. Yet, this approach yields too few data points, making it difficult to ensure capture of IOP peaks and failing to fully present the complete picture of IOP variability.

Furthermore, this approach requires hospitalization and involves repeatedly waking patients at night for measurements. This not only results in poor patient compliance but also places substantial demands on hospital resources, including medical staff and bed capacity. Consequently, very few hospitals are capable of performing this test. Therefore, traditional methods fail to meet the clinical need for continuous intraocular pressure monitoring.

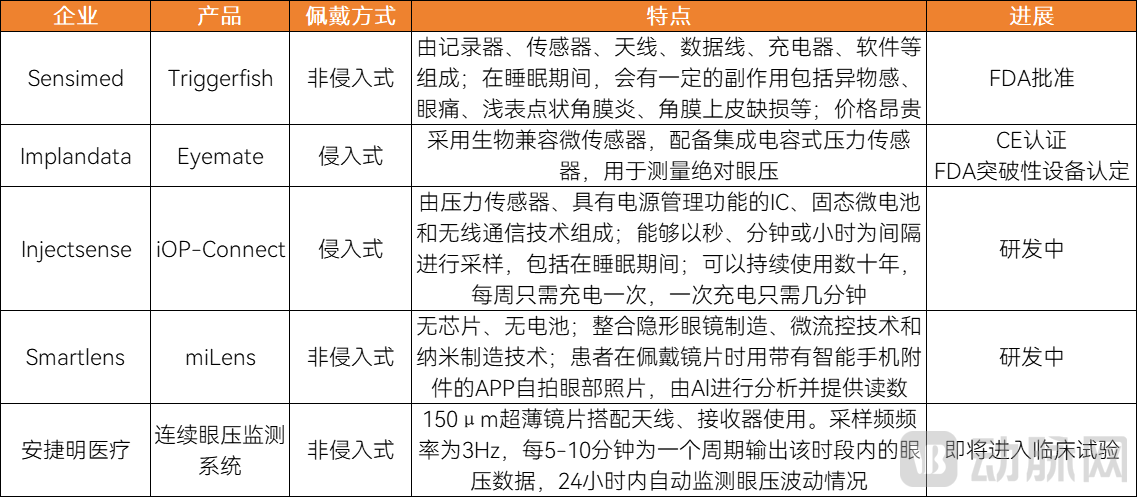

According to statistics, several continuous intraocular pressure monitoring systems are under development worldwide.

Inventory of Continuous Intraocular Pressure Monitoring Systems

A review reveals that companies’ products follow diverse pathways in terms of underlying principles and technical approaches. For instance, based on the mode of use, they are categorized into two major types: invasive and non-invasive. Most patients have low acceptance of invasive products, which are suitable only for surgical patients. Non-invasive products are primarily delivered in the form of contact lenses and can be further subdivided into three technical directions: optical, piezoelectric, and resonant frequency. Among these,Resonant frequency employs wireless transmission, featuring simpler coil design, lower cost, and improved comfort, with the potential to become the mainstream technological approach for intraocular pressure monitoring systems.

Ophthalmic Surgical Microscopes: Domestic Registration Certificates Lead in Number, but a Generational Technology Gap Persists Compared with Imports

Currently, the ophthalmic surgical microscope market is characterized by a high degree of import monopoly, with Zeiss holding over 70% of the market share in China. However, the root cause of this heavy reliance on imports is not barriers to market access.

As of February 7, 2025, excluding products from Tuokang and Zeiss manufactured in China, a total of 14 domestically produced ophthalmic surgical microscopes have received approval from the National Medical Products Administration (NMPA), a number comparable to that of imported products. Although domestic products gained approval as early as 2015, their clinical penetration rate has not seen significant improvement in recent years due to gaps in core performance metrics such as optical imaging technology, equipment stability, and operational precision. Consequently, they have yet to achieve widespread clinical acceptance.

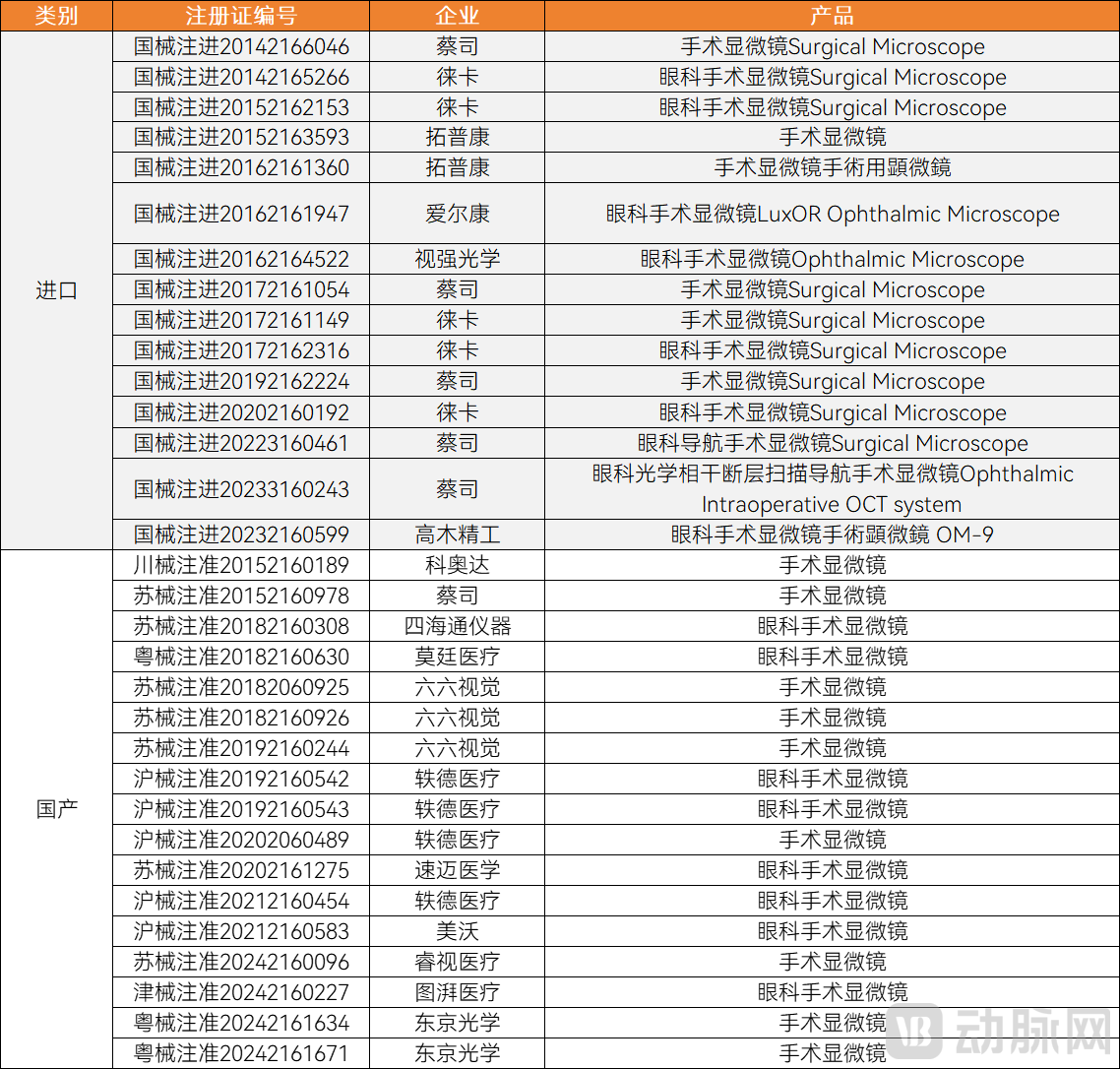

Ophthalmic Surgical Microscope Products Approved by the NMPA

Ophthalmic Surgical Microscope Products Approved by the NMPA

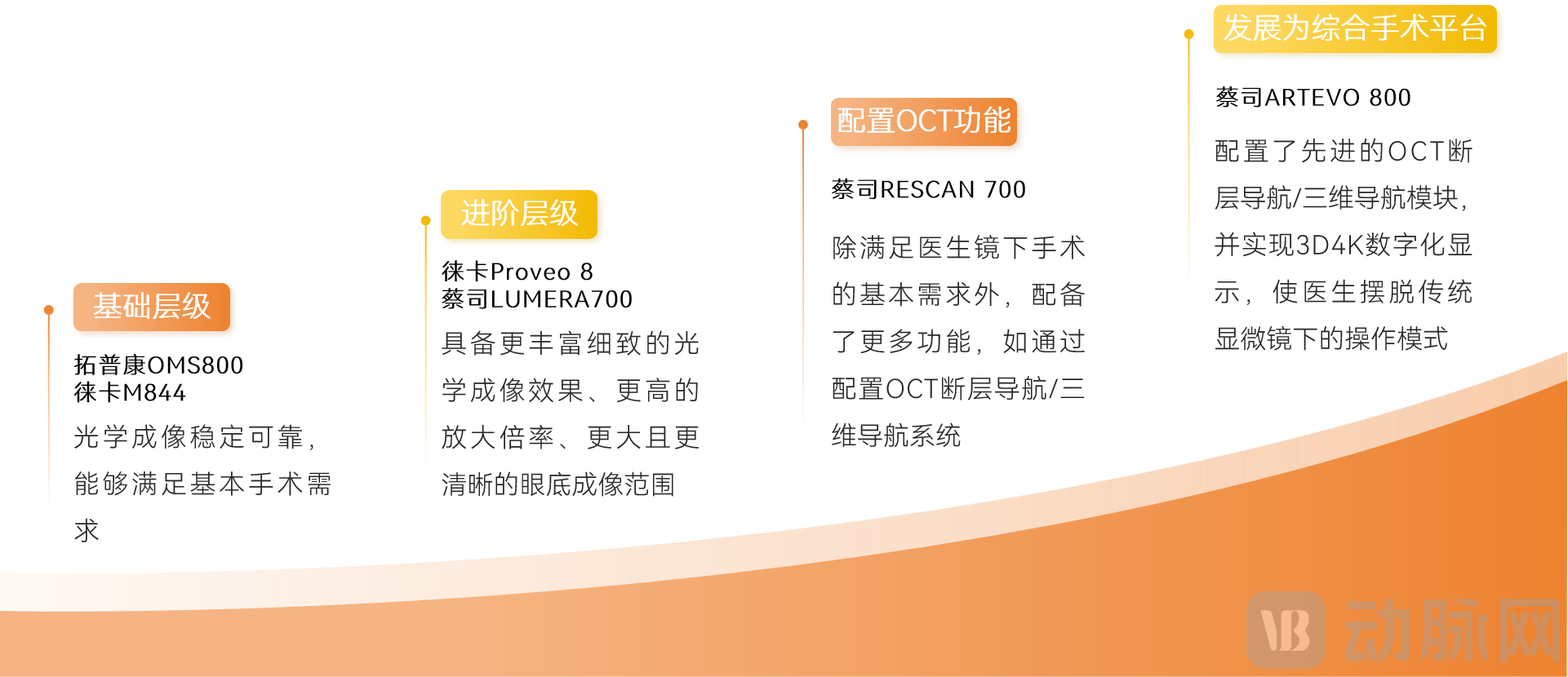

Ophthalmic surgical microscopes have undergone multiple rounds of technological innovation and can be categorized into various tiers. Their functionality has evolved from initially meeting only the basic need for magnified visualization during surgery to becoming comprehensive surgical platform devices that not only provide clear imagery but also offer recording capabilities.

Ophthalmic Surgical Microscopes Have Undergone Multiple Iterations

Ophthalmic Surgical Microscopes Have Undergone Multiple Iterations

VBInsight has reviewed the performance of domestically produced ophthalmic surgical microscopes and, combined with clinical surveys, found that even at the basic level, there is a significant gap between Chinese-made products and imported ones in terms of optical illumination and mechanical performance. The clarity and resolution of the optical systems are insufficient to meet the requirements for fundus surgery, making it difficult to compete in the high-end market. This fully reflects the high difficulty in the research and development of ophthalmic surgical microscope technology.

However, in recent years, Chinese enterprises have been breaking the industry stalemate by launching digital holographic swept-source OCT intraoperative navigation microscopes. Looking ahead,The market for ophthalmic surgical microscopes will exhibit a long-term competitive landscape between domestically produced and imported products.

Phacoemulsification and Vitrectomy Integrated System: Imported Products Hold Over 90% Market Share, While Domestic Alternatives Advance Steadily

The technical bottlenecks in vitrectomy machines are particularly prominent, and no domestically produced combined phacoemulsification and vitrectomy system has yet been approved for market launch.From a technical composition perspective, the phacoemulsification and vitrectomy integrated system consists of three core components: the phacoemulsification system, the vitrectomy cutter, and the vitrectomy machine. The technological barriers for the phacoemulsification system and the vitrectomy cutter are relatively lower, and certain achievements have been made in their localization. However, the vitrectomy machine presents significant technical challenges, becoming the key obstacle to the localization of phacoemulsification and vitrectomy integrated systems; to date, no domestically produced vitrectomy machines have received approval from the National Medical Products Administration (NMPA).

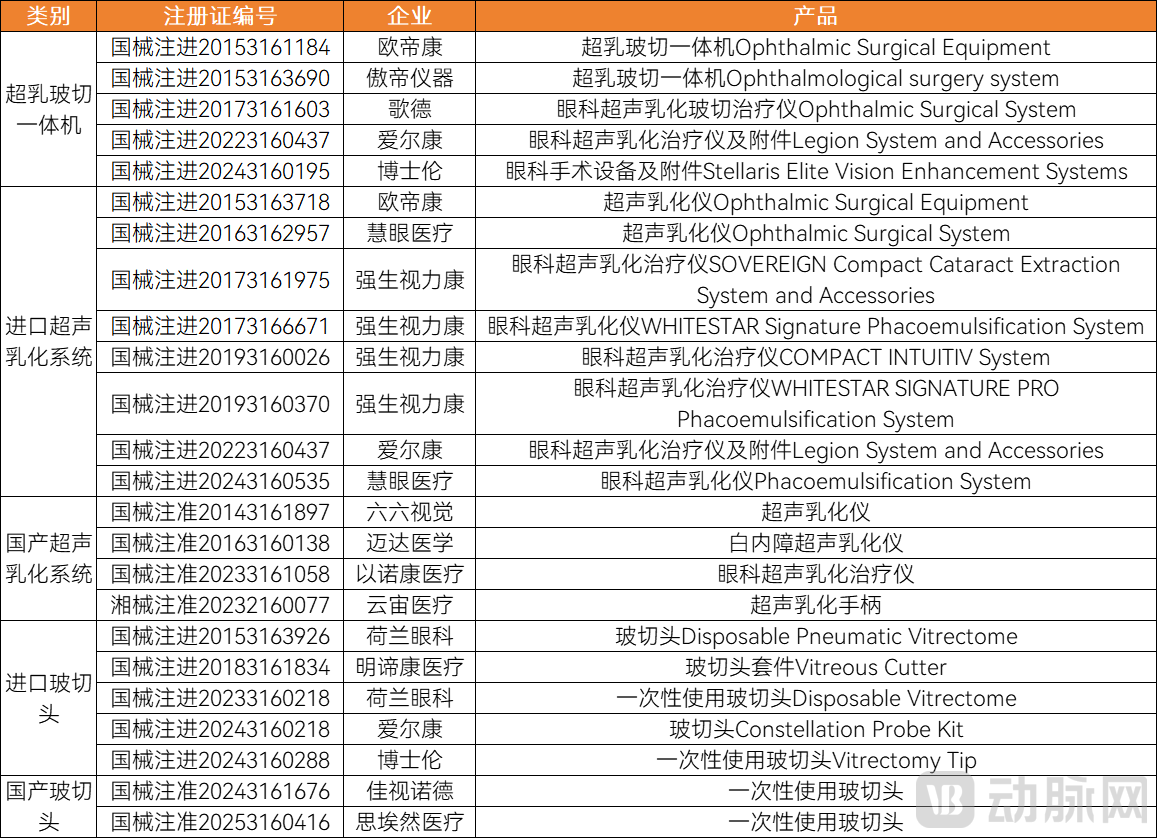

NMPA Approval Status of Phacoemulsification and Vitrectomy Integrated Systems and Related Products

NMPA Approval Status of Phacoemulsification and Vitrectomy Integrated Systems and Related Products

In the current market, imported products demonstrate significant advantages in core parameters, capturing over 90% of the global market share. In contrast, domestically produced combined phacoemulsification and vitrectomy systems are generally in the early stages of research and development, with limited data available on their performance parameters.

The domestic high-end ophthalmic equipment industry is standing at a new starting point. Future trends, and whether the substitution of imported products with domestically produced ones can deepen further, will depend on multiple factors, including product strategy, technological innovation, brand strategy, and policy guidance.

Full-Category Portfolio

A comprehensive product portfolio is becoming an inevitable choice for high-end ophthalmic equipment companies.

Compared with other medical specialties, ophthalmology has a smaller industry scale, yet it involves complex clinical demands and a wide variety of equipment types. Moreover, the market size for any single device is limited, making it difficult to achieve substantial revenue through a single product alone. Therefore, establishing a comprehensive portfolio of high-end ophthalmic equipment is crucial for companies to build competitive advantages and serves as a key factor enabling leading firms to attain significant revenue scales.

Explore More High-Demand Potential Products

Some high-end ophthalmic devices with significant potential are poised to become new growth drivers for the industry and warrant close attention from enterprises, including ophthalmic surgical robots and electrical stimulators for nystagmus.

Among these, ophthalmic surgical robots are widely applied, with many companies currently prioritizing the development of solutions for fundus diseases. Furthermore, in the realm of scientific research, intraocular injection procedures—particularly precise and cutting-edge delivery methods such as subretinal and suprachoroidal injections of gene therapies and cell-based therapies—represent highly promising application scenarios for ophthalmic surgical robots.

The nystagmus neurostimulator is designed to treat congenital nystagmus. By leveraging neuromodulation technology, it effectively suppresses abnormal neural impulses, thereby addressing the root cause of nystagmus. The device is projected to capture a market size of RMB 2–4 billion in China.

Establishing Long-Term Brand and Market Strategies

Although the performance of multiple high-end domestically produced ophthalmic devices is improving and can now rival imported products, it cannot be ignored that there remains a significant gap between domestic brands and their imported counterparts in terms of brand strength and market recognition. Overseas brands have cultivated the Chinese market for many years and invest far more heavily in marketing annually than domestic brands, thereby accumulating substantial brand awareness. In the future, domestic enterprises need to establish long-term brand-building strategies.

Steadfast Global Expansion

Expanding overseas represents a significant incremental market for domestically produced high-end ophthalmic medical devices. Leveraging superior product performance and quality control capabilities, Chinese-made optical coherence tomography (OCT) systems are rapidly gaining recognition in international markets, while other products, such as ultra-widefield fundus cameras, have already been launched globally.

Currently, leading domestic companies are primarily targeting Western countries with high levels of aging populations and developed economies, rather than adopting the low-price strategy and differentiated competition against imported products in Third World countries, as seen with other medical devices. On one hand, the value proposition of leading Chinese-made ophthalmic OCT devices lies not in low pricing, but in the high value-added brought by technological innovation, providing sufficient technical confidence to compete with imported products in the high-end market. On the other hand, demand for ophthalmic diagnostic and therapeutic equipment continues to grow in developed countries, offering a broad market landscape.

The above is an excerpt from the white paper. The overall framework of the report is as follows:

Chapter 1: 2024 Review: Active Financing, Product Boom, and Remarkable Achievements for Domestically Produced High-End Ophthalmic Equipment

1.1 Ophthalmic equipment financing remains relatively active, with deals exceeding RMB 100 million accounting for over 50%

1.2 121 Products Approved; Number of Approvals for Domestically Produced Products Exceeds Imported Ones in Multiple Product Categories

Chapter 2: In-Depth Analysis of Product Competitiveness Across Categories—Leading Brands Have Achieved Multiple Breakthroughs in Performance, Commercialization, and Global Expansion

2.1 Ophthalmic OCT: Chinese Manufacturers Leapfrog in Technology, Capturing Over 50% of the Domestic Market Share

2.2 Optical Biometers: The Gap with Imported Devices Is Narrowing, but Hospitals Lack a Path to Overtake on the Bend

2.3 Ultra-Widefield Fundus Cameras: Surge in Domestic Approvals, Poised to Overtake Competitors

2.4 Corneal Biomechanical Analyzer: Pioneering Direct Measurement of Stiffness/Modulus Technology, Domestically Produced Model to Launch Soon

2.5 Continuous Intraocular Pressure Monitoring: Urgent Clinical Needs to Be Met, with Domestic Devices Already Enabling 24-Hour Automated Home Monitoring

2.6 Ophthalmic Surgical Microscopes: Leading in the Number of Domestic Registration Certificates, but with Technological Generational Gaps Compared to Imports

2.7 SMILE Laser: Domestic Products Have Entered Clinical Trials, but the Cycle for Achieving Import Substitution Is Prolonged

2.8 Phacoemulsification and Vitrectomy Integrated Systems: Imported Brands Hold Over 90% Market Share, While Domestic Products Steadily Advance

Chapter 3 Future Trends: Synergistic Advancement of Multidimensional Corporate Layouts and Policy Optimization

3.1 Enterprises: Multi-dimensional strategies in products, branding, market expansion, and global outreach to build long-term competitiveness

3.2 Policy and Regulation: Continuous Favorable Policies, with Need for Further Improvement in Standardization

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please initiate your inquiry proactively.

Numerous initiatives to localize production have not only driven innovative development in China’s ophthalmology industry but also attracted capital market attention, thereby further fueling industrial growth. On May 9, VCBeat will host an event in Suzhou.“Ophthalmology Industry Innovation and Development Forum”, we invite clinical experts in the ophthalmology sector, research institutions, upstream and downstream enterprises, seasoned investors, and channel partners to jointly explore independent innovation and global development of China’s ophthalmology industry, and to strengthen academic exchange and industrial collaboration within the sector. You are welcome to scan the QR code below to register: