2025 Laboratory Automation Industry Research Report: Rising Domestic Adoption Rate and Thriving Overseas Expansion

The complex and profound life sciences industry has long been regarded as a “slow industry” due to its high technical barriers and lengthy validation cycles. Moore’s Law is nearly “ineffective” in this field, yet its inherent potential for transformation is being rapidly unleashed alongside innovations in emerging technologies. Through deep empowerment by automation upgrades and data intelligence, laboratory research efficiency is seeing rapid improvement. The patterns and value embedded within vast amounts of biological information are gradually being unlocked, accumulating momentum for the industry to break through its tipping point.

Although laboratory automation and the development of digital intelligence are still in their early stages, with a long way to go before realizing the ultimate vision of “lights-out laboratories,” they have already demonstrated extraordinary potential, becoming a core driving force for leapfrog industrial upgrading.

To gain insight into the latest progress of medical laboratories in automation and digital-intelligent transformation, the current exploration and accumulation of business models by domestic enterprises, the maturity and application depth of laboratory automation and digital-intelligent products across various fields and scenarios, industry-advantaged solutions, unmet needs, and future trends, VBInsight has authored the "2025 Laboratory Automation Industry Research Report."

Core Viewpoints:

Most companies in the laboratory automation sector are still in a relatively early stage of development:No dominant market leader has yet emerged, and domestic companies still face numerous challenges in their efforts to capture market share from foreign competitors. From early 2024 to the present, 13 companies in this sector have secured a total of RMB 2.09 billion in new rounds of financing.Among them, companies that specialize in integrating hardware and software and offering customized services, thereby providing comprehensive laboratory automation solutions, have attracted the most market attention.

Not confined to any specific business model, the company employs a dual strategy of integrating hardware with software and combining standard products with customization to meet market demands. It enriches its portfolio of self-developed products, either by horizontally expanding into diverse application scenarios or by vertically deepening its expertise. Meanwhile, it incubates and invests in startups while flexibly pursuing various business cooperation strategies.AI May Be the Core Element Determining the Future Competitiveness of Software Products. Amid the Capital Winter, the Domestic Substitution Rate of Laboratory Automation Equipment Rises Contrary to the Trend.Domestic solutions have gained recognition in overseas markets, with higher product premium margins than in China, making the global expansion path highly popular. The internationalization of small general-purpose devices is progressing faster than that of large complex equipment,Overseas expansion destinations range from Europe to the Asia-Pacific region, including markets such as India and the Middle East.

Hospital laboratories are highly automated, resulting in fierce "red ocean" competition; however, third-party testing still offers significant market entry opportunities.The Inevitable Trend in the Development of Fully Automated Integrated Mass Spectrometry Systems Encompasses Multiple Opportunities, with Numerous Segments Urgently Requiring Automation Upgrades.The biopharmaceutical sector expects automation equipment to be more flexible, precise, stable, and compliant, leveraging cutting-edge technologies such as AI and machine vision to reduce operational error rates and lower the barrier to entry.Synthetic biology exhibits a relatively high degree of automation, yet the development of automated platforms for strain testing faces significant challenges. There are substantial differences in automation requirements among various user groups.Focusing on the “last mile” of sequencing applications, automation upgrades across numerous stages still require optimization, and multi-party collaboration within the industry can foster a win-win outcome.

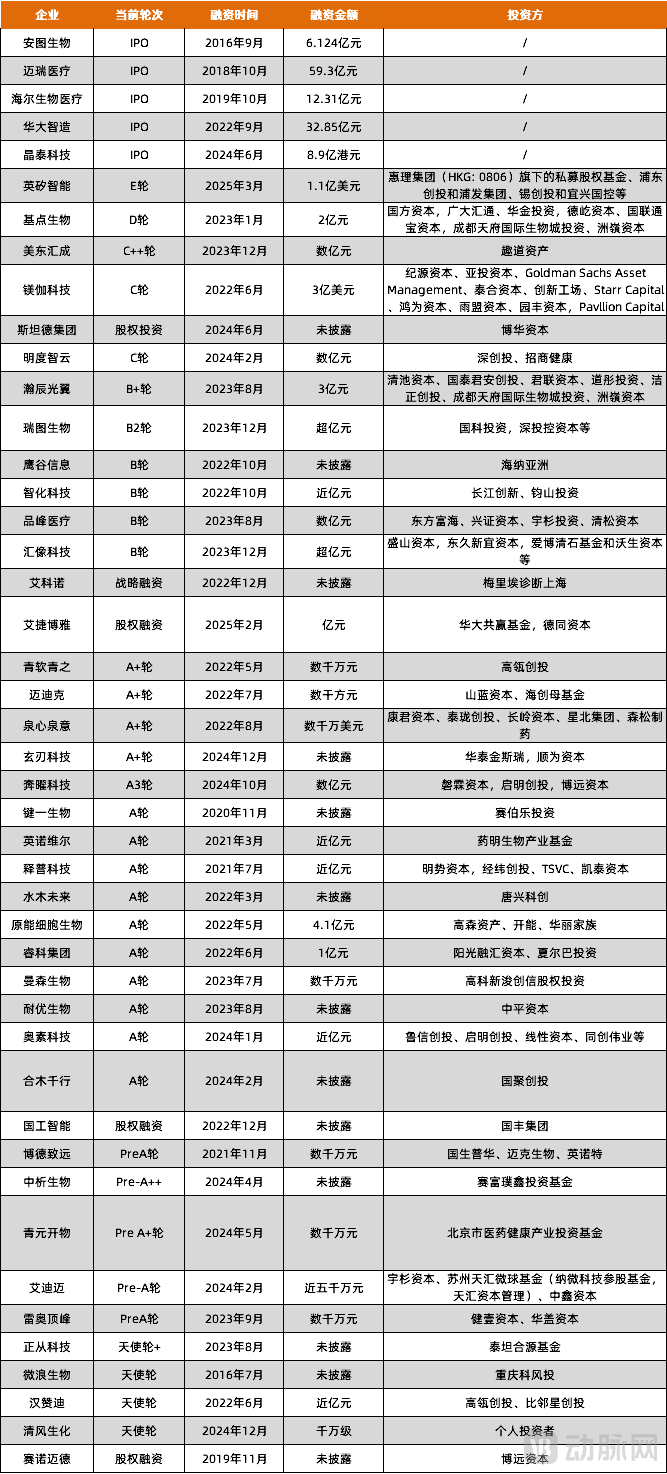

Despite the ongoing capital winter, the laboratory automation sector remains vibrant. From early 2024 to the present, a total of 13 companies in the laboratory automation space have completed new rounds of financing, raising a combined total of RMB 2.09 billion. Notably, XtalPi completed its IPO in mid-2024, and Insilico Medicine closed a $110 million Series E financing round in March 2025. Other laboratory automation companies that secured significant funding include Mingdu Zhiyun, Benyao Technology, and Aidimai Technology.

Overview of Financing in the Laboratory Automation Sector from Early 2024 to Present

Source: VBInsight; Chart by VBInsight

From the overall financing perspective,Apart from certain leading enterprises in niche segments that are relatively mature due to their overall competitive business advantages and scale (with laboratory automation being only one component of their strategic layout or an aspect reflecting their business strengths),Most companies in China’s laboratory automation sector are still in the relatively early stages of development: no clear industry leader has yet emerged, and significant challenges remain to be overcome in competing with foreign laboratory automation firms for market share.

Overview of the Latest Financing Rounds for Nearly 50 Companies in the Laboratory Automation Sector

Source: VBInsight; Chart by VBInsight

Specifically, companies engaged in the automation of clinical or third-party testing laboratories tend to be at later stages of financing.This has given rise to listed companies such as Autobio Diagnostics and MGI Tech. In particular, the maturity of this sector has risen rapidly in the post-pandemic era, leading to intense competition. In the fields of life science research and development, including biopharmaceuticals and synthetic biology, some companies have reached later stages of development (such as XtalPi and Insilico Medicine). These companies are primarily users rather than providers of automated equipment, and the competitive landscape for laboratory automation enterprises in these related fields remains unclear.

Companies that specialize in integrating hardware and software to provide customized laboratory automation solutions have attracted the most market attention, with some entering the mid-to-late stages of their financing cycles.such as MegaRobo and HuiXiang Technology. Some companies that provide specialized solutions in niche scenarios, such as Mingdu Zhiyun and Ruitu Biology, have also entered the mid-to-late stages of financing.

Some companies centered on the hardware development of laboratory automation equipment, such as Naiyou Bio, HanZanDi, Zhongxi Bio, and Aidimai, are still in their early stages of financing. However, they are the main force driving domestic equipment to surpass imported ones. As the demand for locally supplied equipment in China continues to rise, their business capabilities have become increasingly prominent, with a promising future ahead.

Amid the capital winter, there are stillMany companies have achieved strong performance over the past two years.

In the primary market,Insilico Medicine leveraged its sixth-generation AI-powered robotic laboratory to enhance the efficiency of AI-driven new drug discovery and development. Coupled with its “in-house pipeline + license-out” business model, the company achieved a compound annual growth rate (CAGR) of 230% in revenue from 2021 to 2023. MEGA Robotics also publicly disclosed that its overall revenue grew twentyfold from 2019 to 2024.

In the secondary market,In 2024, XtalPi’s intelligent automation business generated RMB 162 million in revenue, surpassing its drug discovery and development segment (RMB 104 million), with a year-on-year growth of 87.8%. MGI Tech’s 2024 financial report also noted that the core operations within its laboratory automation and new business segments maintained a steady upward trend. During the reporting period, 212 additional units of laboratory automation products were installed and sold, representing a quarter-on-quarter increase of 40.91% in the second quarter.

Industry Landscape + Analysis of Mainstream Business Models

Based on differences in core products and business models, VBInsight categorizes companies developing laboratory automation and digital-intelligence products into software developers, hardware equipment developers, and system integrators offering integrated hardware-software solutions, and has mapped out the corresponding industry landscape.

Laboratory Automation Industry Landscape

Data Source: Official websites and public accounts of respective companies; chart by VBInsight.

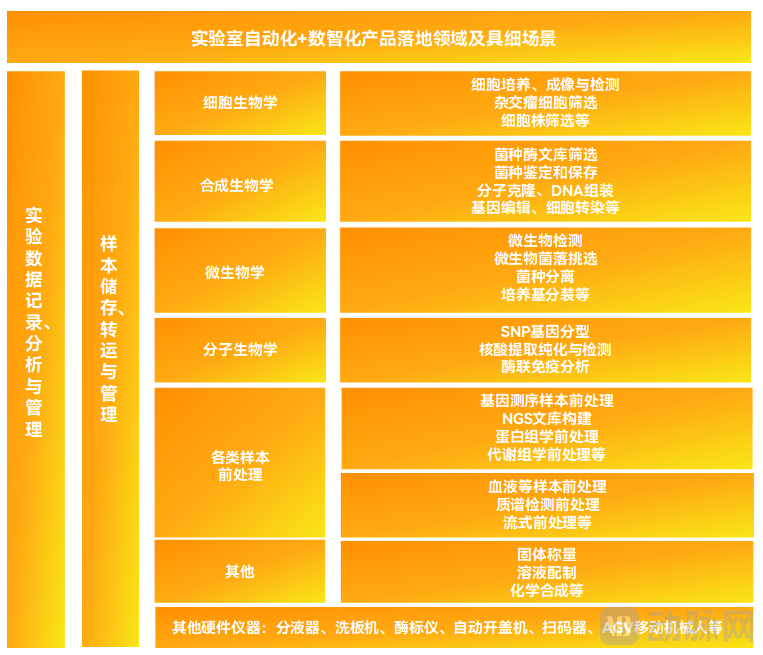

Laboratory Automation + Digital Intelligence Product Implementation: Domains and Specific Scenarios

Data sources: Public information, research interviews; chart by VBInsight.

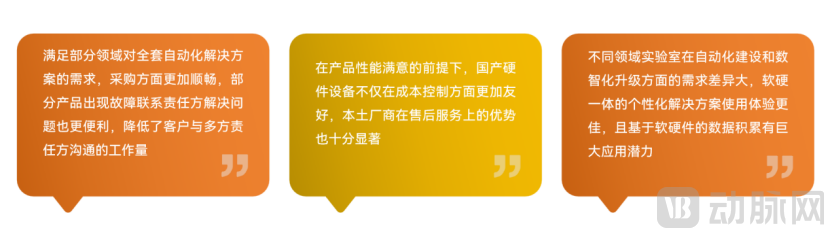

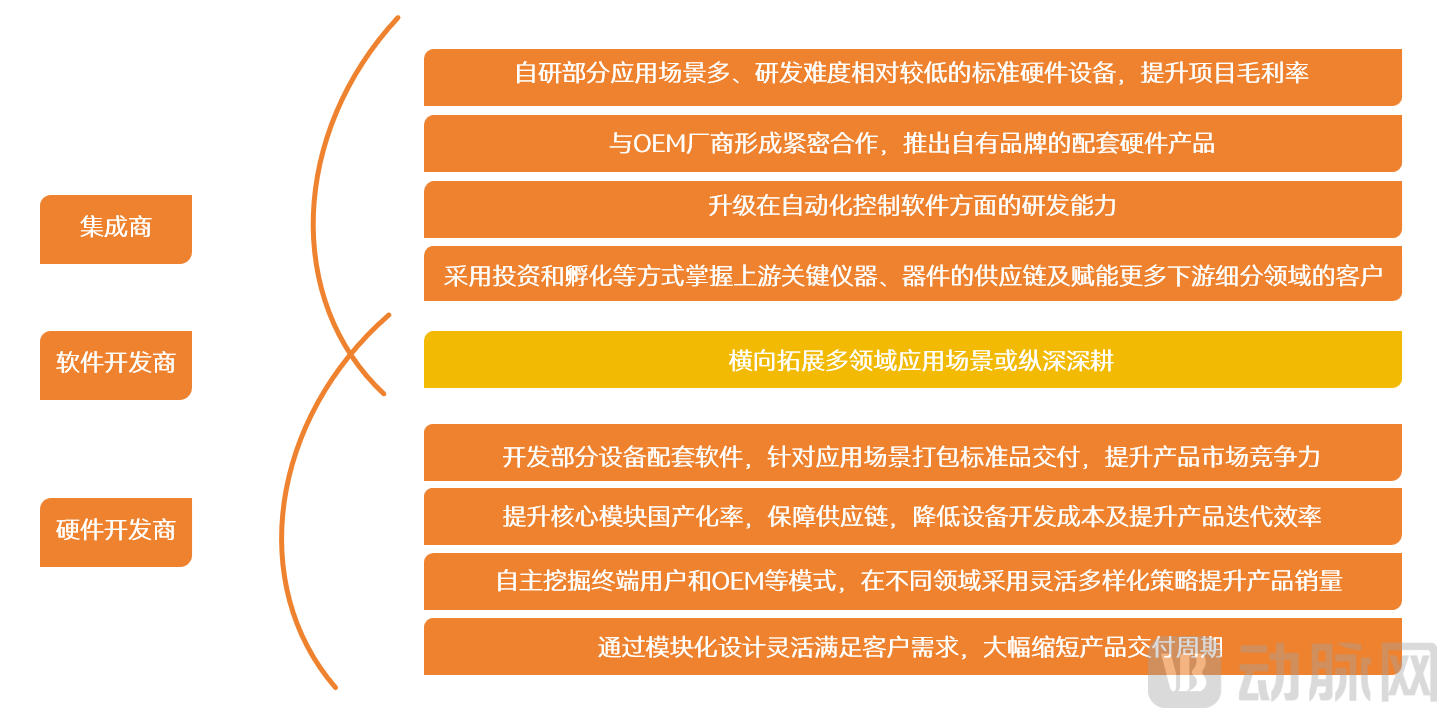

Integrated hardware-software solutions offer numerous advantages, gaining market favor and attracting significant capital interest.The primary reason lies in,Laboratory automation development across various sectors in China, particularly among clients in the life sciences field, exhibits a high demand for customization.

Advantages of Integrated Hardware-Software Automation Solutions

Source: Survey interviews; Chart by VBInsight

For global giants such as PerkinElmer, Siemens, and Thermo Fisher Scientific that provide integrated hardware-software solutions,In contrast to the relatively fragmented domestic orders, objective factors such as the resistance and difficulties associated with overseas remote deployment make it challenging for companies to offer such customized services from a cost-benefit perspective. This market, characterized by robust demand, has provided both momentum and fertile ground for many Chinese enterprises to deploy integrated hardware-software solutions.

Not limited to a specific business model, we adopt multiple strategies—including the integration of hardware and software, as well as a combination of standard products and customization—to meet market and customer demands.

Integrated hardware-software solutions are not the exclusive domain of system integrators; hardware developers also deliver products by providing complementary software or bundling standardized equipment into comprehensive solutions.This is because the laboratory automation sector is still in its early stages of development, and companies have not yet established clear business models. As a result, each company flexibly leverages its team’s strengths to provide both standardized products and customized solutions within its capabilities.

Integration of Hardware and Software, Standard Products Plus Customization: A Multi-Strategy Approach to Meet Market and Customer Demands

Data source: Survey interviews; chart by VBInsight

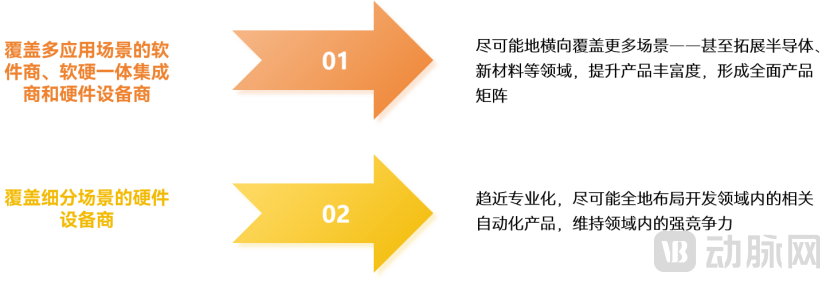

Laboratory automation companies expand horizontally into multi-domain application scenarios or deepen their expertise vertically,Maintain strong competitiveness within the field.

Laboratory Automation Companies: Either Horizontally Expanding into Multi-Domain Application Scenarios or Vertically Deepening Their Expertise

Source: Survey interviews; graphic by VBInsight

Automation vendors with a focus on different domains (such as inspection and testing, or research and development) are also expanding their presence across scenarios through bidirectional strategic layouts.Each enters the market through similar underlying operational modules, leveraging in-depth scenario understanding and unmet market needs to further enrich their product matrices and capture greater market share.

In the long term, in-house R&D capabilities constitute the core competitiveness and economic moat.Requirements have been imposed on vendors’ in-house research and development capabilities for both hardware and software.Software-wise,What determines the differentiation and competitiveness of laboratory automation middleware is the vendor’s profound understanding of automated equipment and application scenarios, coupled with close communication, interaction, and collaboration with numerous customers on the front lines. AI is poised to be the core element determining future competitiveness.

Hardware-wise,It is essential to have in-house developed, platform-based development capabilities for the underlying modules, enabling the rapid assembly of customized automated products tailored to diverse customer requirements. After the deployment of automated equipment, it is necessary to ensure stable and precise operation by promptly adjusting equipment parameters or implementing other context-specific designs based on the actual conditions of the laboratory.

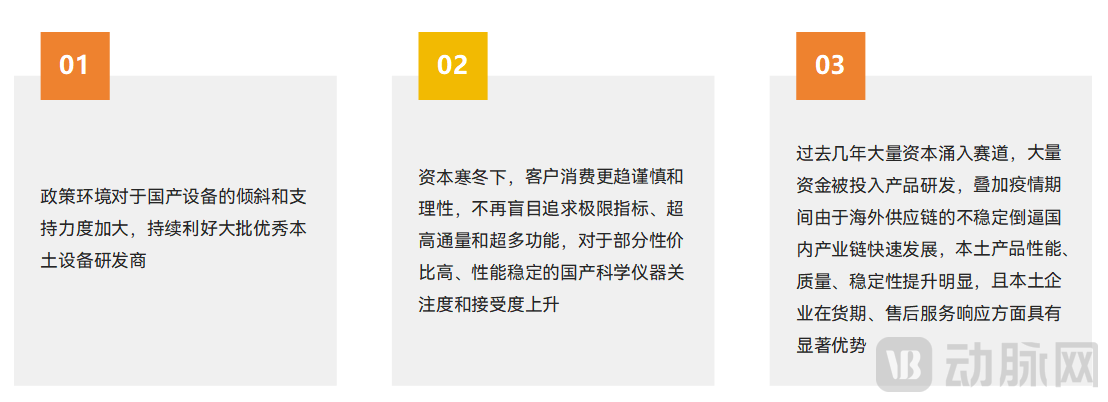

Amid the capital winter, demand for domestic substitution has risen against the trend, with national policy support and geopolitical influences further accelerating this shift.

Post-pandemic capacity clearance and reduced downstream demand in sectors such as life sciences have impacted the upstream manufacturing sector, but the process of domestic substitution is steadily accelerating.Although high-end laboratory automation instruments are still dominated by foreign enterprises, the market share of certain domestic instrument brands is showing a relative upward trend from the perspective of market structure development. Due to space limitations, a detailed analysis will not be elaborated here.

Analysis of the Main Reasons for the Rise in Market Share of Certain Categories of Domestically Produced Automated Instruments

Data source: Public information, research interviews; chart by VBInsight.

For some customers who are not fully familiar with laboratory automation equipment, domestic automation manufacturers also serve as consultants for solution planning. In the construction of automated laboratories in the testing and inspection sector, grassroots service providers are generally price-sensitive, which presents significant opportunities for domestic manufacturers.

Currently, companies that have established large-scale fully automated laboratories, such as Insilico Medicine, are paying close attention to high-quality domestically produced laboratory automation equipment, particularly domestic testing devices capable of high precision. The project team at the Guangzhou Bio Island Laboratory has also publicly stated that its next key focus will be on the independent research and development and deployment of automated laboratory equipment. The primary objective is to achieve substitution with domestically produced equipment, realizing full localization from solution design and software development to the construction and commissioning of hardware. On this basis, the team aims to drive independent innovation and technological iteration in China.

Business Expansion Strategies for Laboratory Automation Companies

Data sources: Public information, research interviews; chart by VBInsight.

Seeking New Business Growth Points: The Path to Global Expansion Heats Up

As the capabilities of domestically produced automated equipment continue to improve, many laboratory automation companies are intensifying their overseas expansion in pursuit of greater market growth. These efforts have yielded strong performance, with overseas markets now contributing significantly to the revenue of some enterprises, even becoming their primary source of income.

For instance, in the first half of 2024, MGI Tech’s gene sequencer business generated RMB 320 million in overseas revenue and secured its first customer for non-sequencing automation products, Appolon Biotek. Benyao Technology has also publicly disclosed that its business now covers multiple regions, including Europe, North America, and Asia-Pacific. For Nayo Bioscience, a developer of automated instruments, overseas customers have contributed the majority of its main revenue over the past two years. According to research, the same automated equipment commands higher prices abroad than in China, offering greater product premium margins. This provides companies with stronger incentives to invest in research and development innovation.

For laboratory automation manufacturers, expanding overseas is not only an inevitable choice to break through the bottlenecks of the domestic market but also a strategic move to seize opportunities arising from the restructuring of the global industrial chain, policy dividends, and technological upgrades.

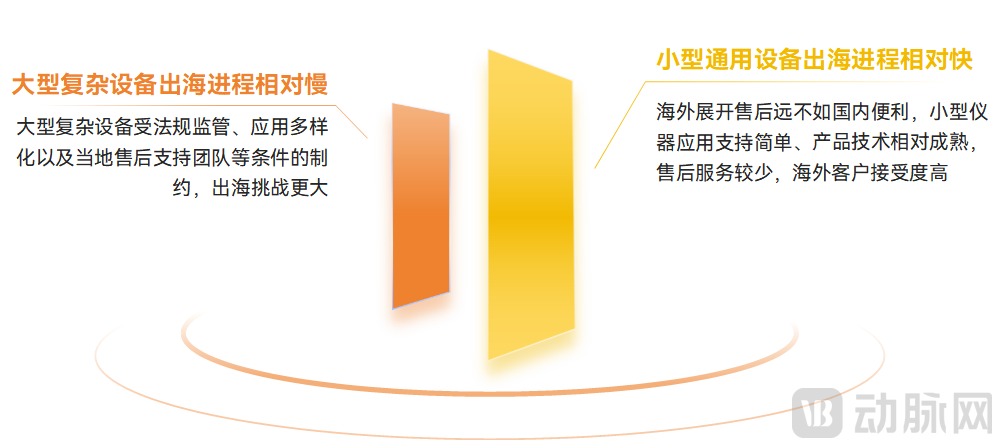

From the perspective of overseas expansion categories for laboratory automation equipment, small general-purpose automated instruments and basic equipment have been expanding overseas at a relatively faster pace, while large-scale complex equipment has been progressing more slowly.

Small general-purpose equipment is expanding overseas at a relatively faster pace than large, complex equipment.

Source: Public information, research interviews; chart by VBInsight

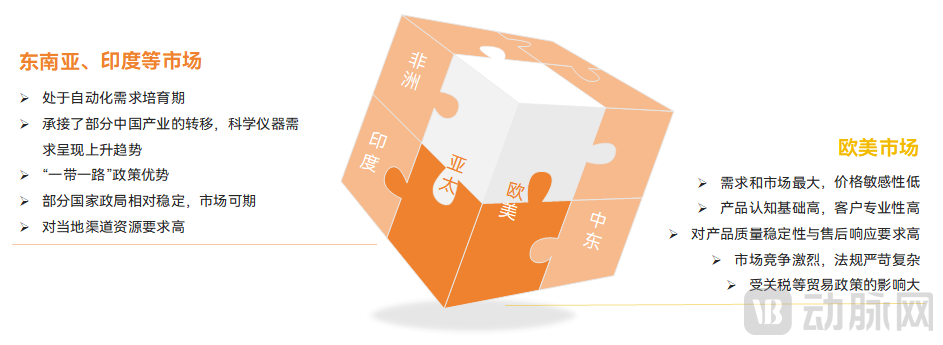

Overseas destinations are diverse, ranging from Europe to the Asia-Pacific region, including countries and regions such as India and the Middle East.For domestic automation manufacturers in the early stages of global expansion, Europe and the United States are not necessarily the primary target markets. Markets such as Southeast Asia and India have absorbed part of the industrial transfer from China, with scientific instrument demand on the rise. These local markets are still in the phase of cultivating automation demand, requiring simultaneous efforts in customer education and product optimization.

Additionally, countries in the Middle East and other regions exhibit lower price sensitivity, making these markets attractive destinations for companies with local resources. There is significant demand in Russia and other countries for integrated hardware-software solutions. Meanwhile, demand for cost-effective scientific instruments is on the rise in Latin America, Africa, and other regions.

In terms of business models, unlike in European and American markets, markets in the Middle East, Southeast Asia, and other regions impose higher demands on channel resources, requiring enterprises to strategically allocate their operations based on their own accumulated resources.

Analysis of the Characteristics of Overseas Destination Markets for Laboratory Automation Products

Data sources: Public information, survey interviews; chart by VBInsight

Significant variations in regulatory policies, market demands, and cultural backgrounds across different countries and regions impose stringent requirements on enterprises’ capabilities in product research and development, registration and certification, and marketing.Based on research interviews, VBInsight has summarized the key success factors for global expansion as follows:

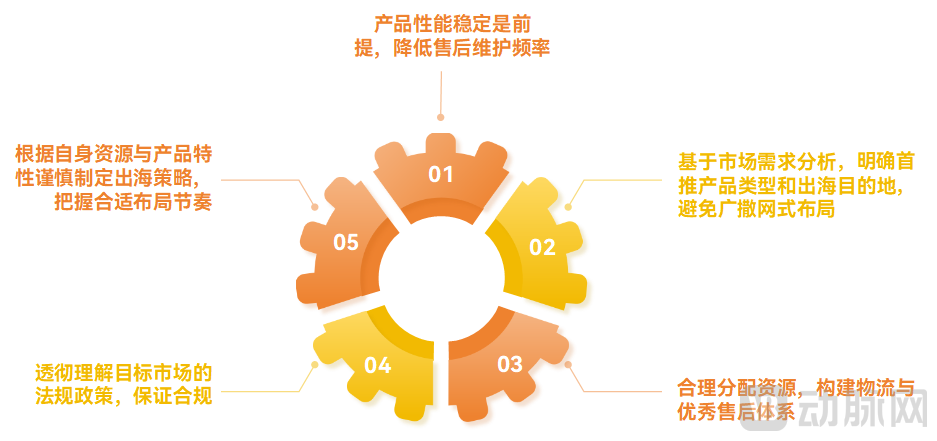

First, product robustness and stability are prerequisites for global expansion, serving to reduce the likelihood of after-sales issues. Second, it is crucial to clearly define the initial product lineup and target export destinations, avoiding a scattered, unfocused approach. Companies should determine their market positioning based on market demand analysis to identify flagship products, while distinguishing go-to-market strategies for simple versus complex devices. Meanwhile, enterprises must simultaneously establish logistics networks and high-quality after-sales service systems. This involves deciding whether to build local teams or dispatch a lean, expert team for management, based on the company’s specific circumstances. After-sales maintenance plans must be comprehensive, and mechanisms for equipment parts replacement should be planned in advance. Finally, regulatory compliance is key to successful market entry. Companies must thoroughly understand the laws and policies of target markets, actively prepare the necessary documentation, and ensure products smoothly pass registration and approval processes.

Strategies and Recommendations for the Global Expansion of Automation Products

Source: Survey interviews; chart by VBInsight

How to Pace Global Expansion Is Crucial—Companies should not act rashly or “go global for the sake of going global.” Each enterprise must carefully formulate its strategy based on its own resources and product characteristics to mitigate operational risks and achieve sustainable overseas business expansion. Establishing core competitive advantages in the domestic market, where R&D investment is second only to that of the United States, remains the foundation for outstanding companies to plan their long-term development paths.

1Current Pain Points, Market Demand, and Industrial Solutions in the In Vitro Diagnostics Sector

Hospital laboratories are highly automated, creating a fiercely competitive "red ocean" market, while third-party testing offers numerous entry opportunities.

In terms of demand, clinical laboratories in tertiary hospitals are the primary users of automation lines, but installation demand is gradually emerging in secondary hospitals and independent clinical laboratories (ICLs).Currently, many county-level people's hospitals and secondary hospitals in China are actively introducing automated laboratory assembly lines following expansion and renovation projects. Secondary hospitals will become the primary market for domestically produced assembly line installations over the next 3–5 years.

Apart from the hospital market, judging by the maturity of laboratory automation development, less than 20% of clinical testing laboratories in China have achieved fully automated assembly lines.There are still significant market opportunities for testing and inspection institutions, such as the Centers for Disease Control and Prevention (CDC), enterprise quality control departments, drug regulatory authorities, customs, and forensic appraisal centers.

Clinical mass spectrometry is transitioning from “semi-automated” to “fully automated,” with multiple processes in urgent need of automation upgrades.

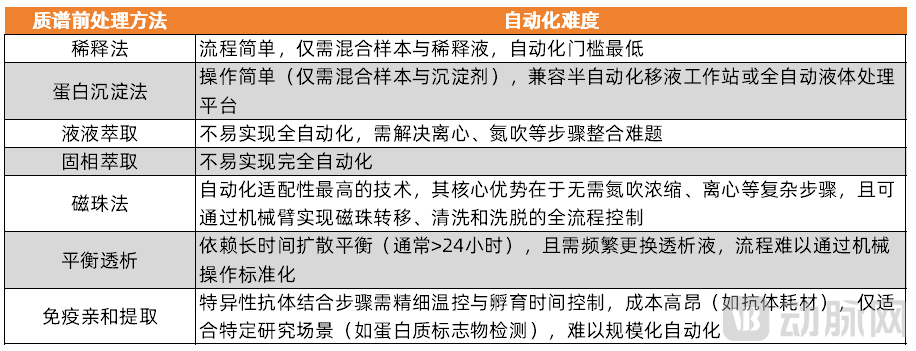

The automation of pre-analytical processing for mass spectrometry is highly challenging, resulting in a limited number of existing market products that can meet customers’ automation needs. Developing fully automated integrated mass spectrometry systems presents significant technical difficulties. Different types of clinical samples require distinct pre-analytical methods, which vary in operational steps and complexity, thereby posing varying levels of challenges for automation.

Automation Difficulty Corresponding to Different Mass Spectrometry Sample Preparation Methods

Data Source: Compiled from public information, research interviews; chart by VBInsight.

Furthermore,Due to the mismatch in “pace” between sample pretreatment and mass spectrometry detection, it is challenging to develop fully automated integrated mass spectrometry systems. The inherent limitations of liquid chromatography–mass spectrometry (LC-MS) technology are a significant factor currently hindering the advancement of automation in clinical mass spectrometry.

Currently, the market for automated mass spectrometry instruments is dominated by semi-automated products, represented by liquid handling workstations and automated sample preparation systems.Market automation product development remains imperfect, with many unmet needs, such as mainstream external(Relatively Low Proportion of Clinical Applications)Mass Spectrometry Technology(MALDI-TOF MS, ICP-MS, etc.)Pre-automated processing instruments are still lacking.

To achieve the ultimate goal of developing fully automated mass spectrometry integrated systems, the industry is exploring numerous approaches and solutions, such asIt is more appropriate to develop automated pre-treatment methods or to develop new separation technologies.Magnetic bead-based methods, as an emerging star among mass spectrometry pre-treatment techniques, have opened up new avenues for achieving high-level automation in mass spectrometry.

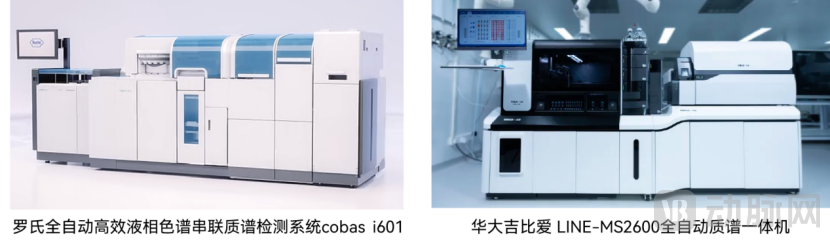

The fully automated mass spectrometry integrated systems launched by Roche and BGI Genomics (Huada Gene) are both based on the magnetic bead method.

Image source: Public information

By upgrading pre-treatment methods to better suit automated equipment, in addition to replacing solid-phase extraction with magnetic bead-based methods, current advancements include substituting traditional liquid-liquid extraction with supported liquid extraction (SLE) and replacing supernatant pipetting with positive-pressure filtration.

The emergence of new separation technologies, such as ion mobility technology,Higher efficiency and greater stability are expected to replace chromatography, addressing the current limitations faced by this technique and accelerating the development of mass spectrometry automation. Furthermore,By simplifying or omitting the liquid chromatography separation process(LC-MS/MS system detection level) can also enhance the degree of automation, thereby improving stability and detection throughput.In addition to developing higher levels of integration (i.e., all-in-one instruments), automation technologies for mass spectrometry sample preparation are also evolving toward broader compatibility (multi-technology convergence) and intelligent upgrades (AI-driven).

In addition to breakthroughs in automated sample pretreatment technologies, many other steps still need to be further addressed to meet automation requirements.such as the development of maintenance technologies for new instruments,For example, automatic cleaning of the ion source and automatic replacement of chromatography columns to achieve automated instrument maintenance;Breakthroughs in Automated Data Analysis Technology——Develop novel data analysis technologies, integrating AI to automate data analysis and more.

2Current Pain Points, Market Demand, and Industrial Solutions in the Field of Drug R&D

Numerous issues in traditional drug R&D experimental operations constrain the industry's rapid development, while automation offers significant advantages

Traditional pharmaceutical laboratory operations are cumbersome and time-consuming in sample processing, resulting in poor experimental reproducibility, disorganized data management, and difficulties in analysis. Automated laboratories can eliminate resource-intensive manual labor, reduce human error, and improve experimental reproducibility, thereby significantly enhancing the efficiency of drug discovery and development. Empowered by information software and intelligent hardware, these systems improve the quality of experimental data generation, facilitate data analysis and management, and ultimately increase the success rate of drug R&D.

By integrating automation systems with advanced data analytics and machine learning capabilities, the goal of continuous optimization of laboratory processes can be achieved. The latest generation of automated laboratories enables simultaneous testing on both human and animal models, thereby alleviating, to some extent, the critical shortage of R&D data in certain specialized subfields.

Leveraging the continuous stream of high-quality R&D data generated in laboratories, combined with large-scale research data from public databases that have undergone rigorous cleaning, AI technologies can facilitate the rapid discovery of novel molecular structures and therapeutic targets, a process known as Artificial Intelligence Drug Discovery (AIDD).

Applications of AI in Various Stages of Drug Development

Data Sources: Public information, research interviews; Chart by VBInsight

The research and development of automated solid weighing and dispensing instruments is highly challenging,To address unmet market needs, domestic companies including USTC, Zhengcong Technology, and Guangzhou Biaozhi Future have leveraged their expertise in precision mechanical design,Capabilities in technologies such as AI machine vision have enabled the development of multiple domestically produced automated solid weighing systems, breaking foreign monopolies and patent blockades.

However, despite the development of automated solid dispensing equipment with varying weighing ranges and application scenarios both domestically and internationally, many challenges remain.The future industry still needs to develop a richer variety of automated solid dosage weighing products around unmet market demands.Solid handling also faces challenges such as high customization requirements, prohibitive costs, and insufficient purchasing power. Furthermore, the level of automation in chemical synthesis remains relatively low; the complex sample conditions involved in synthesis demand more sophisticated integration capabilities.

The development of automated solid weighing equipment still faces numerous challenges and significant room for improvement.

Source: Compiled from public information; chart by VBInsight

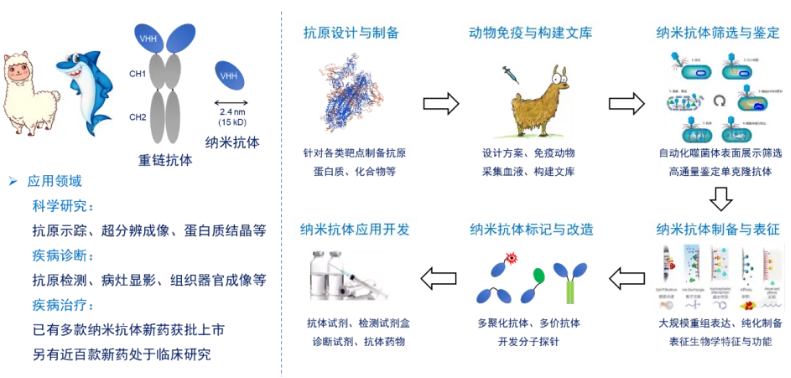

Automation Technology Efficiently Empowers the Screening, Synthesis, and Engineering of Nanobodies

Nanobodies (Nb), as a novel class of antibody molecules, demonstrate significant application potential in drug development, disease diagnosis, and therapy due to their unique structures and properties. However, traditional nanobody research methods are constrained by lengthy cycles, cumbersome procedures, and high costs, which limit the development and application of nanobodies. The integration of AI technology and automation provides robust support for the efficient screening, synthesis, engineering, and detection of nanobodies. This not only enhances the efficiency and accuracy of nanobody screening but also makes their synthesis and engineering more efficient and convenient, leading to increasingly widespread applications in nanobody research.

Intelligent Automated High-Throughput Nanobody Screening and R&D

Source: Publicly available information

ButThe application of automated systems in nanobody research requires further exploration and optimization to better meet practical needs, while the complexity and high cost of these systems also demand improved solutions from the industry.

Automation + AI-Enabled Organoid Drug Screening to Address Non-Standardization and Quality Control Issues in Traditional Construction

Organoids and Organ-on-a-Chip technologies are regarded as disruptive biomimetic models at the core of drug development, owing to their ability to highly simulate and recapitulate human physiological environments and complex responses. These technologies not only significantly improve the accuracy of predicting clinical drug efficacy, accelerate experimental processes, and reduce drug development costs, but also provide AI models with training data that closely approximate real human physiological conditions. This addresses the "data distortion" bottleneck inherent in traditional cell models (which reflect only monolayer cell characteristics) and animal experiments (where interspecies differences lead to misjudgment of drug toxicity in over 80% of cases).

However, traditional organoid construction methods rely on manual laboratory operations, which are time-consuming and labor-intensive. Furthermore, due to the inherent heterogeneity and stochastic nature of organoids, their cultivation faces significant challenges in standardization and quality control. To enable large-scale and efficient organoid culture, companies such as Heiyu Science and Jiashiteng have deeply integrated AI, microfluidics, and automation technologies. They have successively launched various automated organoid culture systems that achieve full-process automation of organoid experiments. These systems facilitate one-click intelligent execution of complex workflows, including the incubation, standardized construction, real-time imaging observation, AI-assisted high-throughput drug screening, and data output of 3D in vitro models (organoids/assembloids/vascularized microtissues).

Overall, automated, high-throughput organoid culture systems can promote the standardization of organoid culture, enhance product reproducibility and consistency, increase throughput, and reduce costs. Meanwhile, automated organ-on-a-chip handling equipment can significantly reduce the complexity for downstream customers in using organ-on-a-chip technologies, thereby facilitating their rapid adoption and widespread application.The overall level of automation in the fields of organoids and organ-on-a-chip remains relatively low, and there is a continued need for further development of mature, practical, and cost-effective instrumentation.

Anticipating greater flexibility, precision, stability, and compliance, with AI and machine vision reducing operational error rates and lowering the barrier to entry.

Currently, there is no dominant player in the laboratory automation industry. One reason for this is that laboratory needs are highly diverse, making it difficult for a single company to develop a comprehensive suite of automated equipment capable of meeting the requirements of laboratories across various fields and scenarios.

For automated equipment in the field of biopharmaceutical R&D, the industry has put forward some optimization expectations:

IncludingAccelerate the formulation of industry standards for automated laboratories, enhance product stability, flexibility, and precision handling capabilities, upgrade automated process control, equipment monitoring, and troubleshooting functions based on cutting-edge technologies such as machine vision, reduce equipment operation error rates, leverage AI to facilitate efficient interaction between equipment and researchers, lower the barrier to entry for operators, and better align with operators’ thinking patterns and habits.。

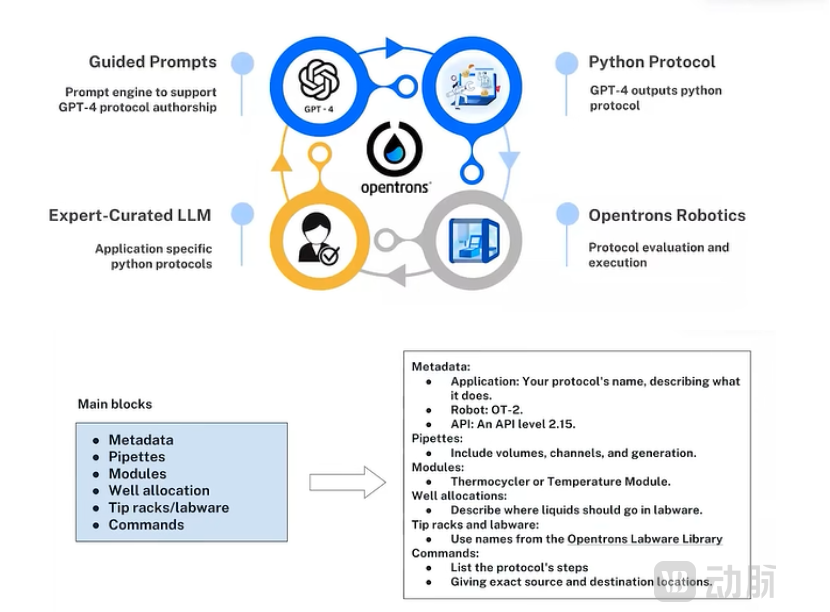

Leveraging open-source APIs and documentation, fine-tune the GPT language model via RAG with a specialized knowledge base to generate precise protocols.

Image source: opentrons

Other features pending upgrade, includingCurrently, most automation tasks remain at the microliter scale. How can we leverage new technological pathways to meet customer demands for nanoliter-level operations? How can we bridge the gap with imported products in terms of equipment data compliance?These are all areas where domestically produced equipment needs improvement and effort.

Overall, for laboratory automation companies, commercial considerations inevitably prioritize meeting the demand for high-volume flagship products with broader application scenarios and higher usage frequency, followed by more specialized product categories required in niche scenarios.

The development of AI is equally fraught with challenges and requires a long-term commitment. Currently, generative AI applications are primarily concentrated in the realm of human-computer interaction. Achieving more complex applications and functionalities in the field of laboratory automation will undoubtedly require greater investment of effort, resources, and time from the industry. For startups with limited resources and bandwidth, it is essential to calibrate the pace and intensity of their deployment of frontier technologies according to their own strengths and characteristics. Teams with strong software/AI backgrounds tend to focus more heavily on AI initiatives, while some larger enterprises are engaging in deeper and more proactive AI exploration. For the majority of domestic R&D companies specializing in automation equipment, meeting customer demands for equipment stability, consistency, and ease of use remains their primary objective.

Current Pain Points, Market Demand, and Industrial Solutions in the Field of Synthetic Biology

Given that research in synthetic biology generally requires relatively mild reaction conditions and primarily involves liquid-phase reactions, China’s current industrial technologies in pipetting are well-suited to meet laboratory needs, ranging from varying experimental throughputs to different reagent measurement and ratio requirements.

For standardized experimental procedures such as molecular cloning, cell culture, gene synthesis, and strain screening and testing, the industry has already developed relevant automation solutions. Highly acclaimed product lines include media aliquoting systems, pre-treatment equipment for microbial detection, strain isolation systems, and colony picking systems or devices. Companies including MegaRobo Technologies, Xuanren Technology, Hanze Di, Dibio, and Manson Biotech have launched a series of competitive solutions tailored to synthetic biology scenarios, thereby meeting the diverse needs of synthetic biology research.

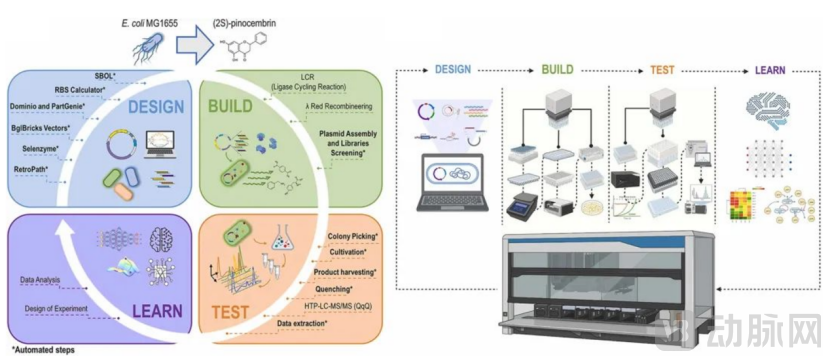

The “Design-Build-Test-Learn” iterative cycle in synthetic biology is inherently compatible with automation and AI technologies

Image source: Public information

Overall, in the Build phase of synthetic biology, automation is relatively easy to achieve due to the many commonalities; however, the Test phase involves significant uncertainty owing to the diversity of testing and characterization methods, thereby posing greater challenges for the development of automated strain testing platforms.

Current Pain Points, Market Demand, and Industry Solutions in the Field of Gene Sequencing

In recent years, NGS technology has been widely applied in clinical settings. However, due to the complexity of NGS testing workflows, there is currently a significant shortage of trained personnel capable of performing these intricate procedures. Automation technology has injected new vitality into the widespread adoption of NGS.

One of the key factors constraining the mature application and widespread adoption of NGS is its low level of automation.

Data source: “Expert Consensus on Automation and Routine Implementation of Clinical Next-Generation Sequencing”; chart by VBInsight

From Standalone Instruments to Automated Workflows, NGS Automation Solutions Have Become Increasingly Diverse in Recent Years.In the early years, the market was dominated by imported brands, including Hamilton, Beckman, and Tecan; later, domestic brands began to enter the market.

In the NGS testing workflow, library preparation is an indispensable yet the most complex and labor-intensive step, and the quality of library preparation directly impacts sequencing quality. To achieve automation in library preparation, international companies such as Tecan, Beckman Coulter, Roche, Agilent, and Opentrons have launched automated library preparation systems. Meanwhile, domestic enterprises in China, including Aometai, Nuoyou Biology, Ausenomics, HanZandi, and Medic, have also introduced high-quality automated library preparation instruments.

To address the “last mile” challenges faced by customers in diverse scenarios, companies have developed automated library preparation products with distinct advantages, leveraging their deep understanding of specific application contexts. For instance, cartridge-based automated library preparation meets the need for flexibility.Companies such as 3D Medicines, Jieyi Biotechnology, Magigene, and MGI Tech have successively launched cartridge-based automated library preparation systems.

Representative Cartridge-Based Automated Library Preparation Systems Currently on the Market

Image source: Compiled from public materials; graphic by VBInsight

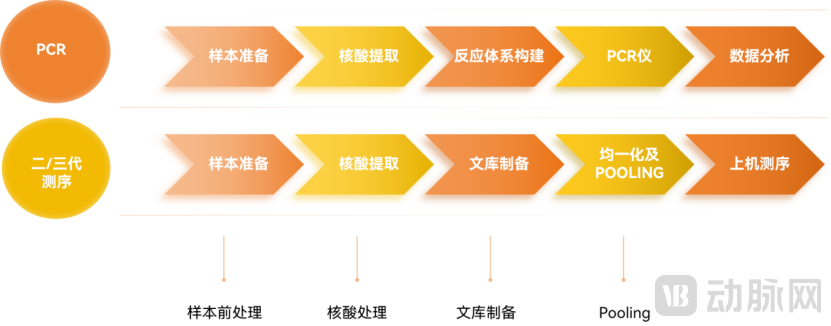

NGS Experimental Workflow

Data source: Health Watch Corner; chart by VBInsight

After library preparation and prior to sequencing on the instrument,Typically, critical steps such as quantification, normalization, and pooling are also required. Transferring libraries processed by library preparation instruments to other devices increases procedural complexity and may introduce new errors. In response to this need, companies including Boju Technology, Naiyou Biology, HanZanDi, and Omegatek have successively launched automated library preparation systems with integrated nucleic acid quantification capabilities.

Representative Automated Library Preparation Instruments with Nucleic Acid Quantification Capabilities Currently on the Market

Image source: Compiled from public materials, chart by VBInsight

The Ideal Form of Sequencing: “Sample In, Results Out,” Which Integrates Nucleic Acid Extraction, Library Preparation, Sequencing, and Analysis. Many Manufacturers Both Domestically and Internationally Have Already Achieved This, and the Future Trend Is Further Miniaturization.

However,Due to the extensive and complex applications of next-generation sequencing (NGS), there are significant differences in automation needs across various application domains and user groups. Different user segments and business requirements impose unique demands and expectations on the implementation of automation technologies., therefore, on the path toward the ultimate ideal form of NGS, a diverse range of automated sequencing products will inevitably emerge.

Many aspects of automation upgrades still require optimization,Such as the balance achieved by automated library preparation instruments between flexibility and high compatibility to accommodate multiple assays; the improved accuracy of the fluorescence quantification module in automated library preparation systems and its seamless integration with control systems; further enhancement of automation levels in nucleic acid extraction, purification, and library preparation, particularly in quality control, hybridization, and the preparation of elution reagents and consumables; meeting timeliness requirements in the pooling step, including multi-sample pooling, multi-volume handling, and random-access pipetting; and control of cross-contamination rates across all stages from sample collection and processing to library preparation and sequencing. Leveraging their advantage in efficient local collaboration with domestic customers, Chinese manufacturers can seize market opportunities.

Ultimately, the development of high-quality automated equipment is not solely the responsibility of instrument manufacturers; it requires coordinated efforts across multiple industry stakeholders, including upstream suppliers, downstream customers, and companies in related fields such as reagents, consumables, and software. Only by gaining deep insights into customer needs can we ensure that technological applications are maximally aligned with their actual requirements. Companies specializing in automated equipment can explore collaborative opportunities to achieve mutual success.

The above is an excerpt from the main content of the report. To obtain the full report, please scan the QR code to add our assistant and initiate a conversation upon connection. The report will be officially released on-site at the Medical Device Design and Manufacturing Forum during VCBeat’s “2025 VBEF Future Healthcare Top 100 Exhibition.”

Special Acknowledgments (in order of research interviews):

Cheng Hao – Partner at Shengshan Capital, Kong Linghe – Vice President of Investment at Zhongping Capital, Qu Zhihu – Head of the Automated Laboratory at Insilico Medicine, Zhang Na – Chief Operating Officer at Hanze Diagnostics, Luo Junkui – Founder of Naiyou Biotech, and other unnamed corporate representatives and investors