New Opportunities for Life Sciences Firms Are Hidden in Real Estate

“Amid the intensifying ‘involution’ and the wave of cost reduction and efficiency enhancement in the life sciences industry, if life sciences companies can align with market trends and rationally leverage real estate resources, they will not only reduce property costs but also effectively facilitate the translation of business outcomes, playing a pivotal role in attracting and retaining talent.”Yu Zeren, Senior Director of Life Sciences Real Estate at JLLAs stated.

JLL is a global leader in real estate professional services and investment management. In 2007, it established a life sciences industry service platform to provide specialized, customized strategic insights and solutions for government agencies, industrial park platforms, innovative enterprises, and investors both in China and abroad.

At the main forum of the VCBeat VBEF Top 100 Future Healthcare and Medicine Exhibition on May 10,Yu ZerenDrawing on insights and service experience with global life sciences enterprises, this analysis examines the development trajectory of China’s life sciences industry from a real estate perspective and shares the latest trends in the global life sciences real estate market for 2025.

Life science real estate is an emerging niche sector within the life sciences industry. It integrates the high-end demands of biopharmaceuticals, gene technology, and medical devices, driving technological innovation and industrial commercialization in life sciences through specialized space operations.

Although this sector is still in its early stages in China, the value proposition of life science real estate has been further strengthened by the continuous intensification of national biopharmaceutical policies, the growing demand for scalable space driven by breakthroughs in Chinese biotechnology, and the active biopharmaceutical business development (BD) transactions that are prompting companies to transition from an “asset-light” model to one focused on “R&D-intensive” operations.

Yu Zeren pointed out that it is precisely based on this soil of industrial transformation,In China, the life sciences industry and real estate sector have transcended traditional supply-demand dynamics, forming an interdependent community for synergistic development.

Among them,Industry Demand Drives Real Estate Innovation.The rapid development of the industry is compelling traditional real estate to break away from the “space leasing” mindset and shift toward a specialized operational approach centered on “industry empowerment.” By providing customized facilities and ensuring regulatory compliance, real estate developers enable enterprises to focus on core R&D rather than infrastructure construction, thereby accelerating the efficiency of technology transfer.

Meanwhile, real estate value is also feeding back into industrial development.Real estate, as the second-largest cost item for life sciences companies after labor costs, can form a closed loop of cost reduction and efficiency improvement through refined operational management, becoming an important support for enterprises to build core competitiveness.

Data also reflects the recognition by life sciences companies of the value-enhancing role of real estate. According to JLL’s “2024 Global Future of Office Survey,” which conducted in-depth research on 2,300 companies across 25 countries and regions worldwide, including a sample of 145 life sciences enterprises: 47% of respondents expressed their desire to reduce operating costs by optimizing their real estate strategies. For instance, they aim to generate cash flow by leasing or selling idle facilities such as laboratories and warehousing and logistics centers, or by transforming real estate assets into financial products to attract investment.

And this bidirectional empowerment has further become manifest.A Prominent Feature of Life Science Real Estate: Strong Industrial Agglomeration Attributes. Life sciences companies rely heavily on ecosystem collaboration and tend to choose locations that are resource-intensive and conducive to cooperation.

Taking the HUB at RTP in Durham, the largest life sciences park in the United States, as an example, the area leverages the scientific research resources of the Massachusetts Institute of Technology (MIT) to build a complete industrial chain through the organic integration of functional platforms, clinical hospitals, and transportation hubs. Biopharmaceutical companies in this region can share R&D equipment and instantly access clinical resources, rapidly overcoming technical barriers and significantly shortening the new drug development cycle.

In China, one-stop industrial clusters encompassing R&D, clinical trials, manufacturing, and distribution have taken shape in areas such as Shanghai Zhangjiang, Suzhou BioBay, and Shenzhen Pingshan. These clusters have significantly shortened supply chain radii, providing an efficient innovation environment for enterprises in the biopharmaceutical and medical device sectors.

Three-Element Site Selection,Improving the Efficiency of R&D Resource Allocation in Life Sciences Enterprises

The Rise of Life Sciences Real Estate Is Essentially an Extension of the “Space-as-a-Service” Industrial Logic.As real estate transitions from a “space provider” to a “strategic enabler,” site selection, as the initial step, has become pivotal for enterprises to reconstruct their competitiveness.

JLL has long supported multinational corporations (MNCs) in expanding within the Chinese market, accumulating profound industry insights and extensive experience in localized services. Yu Zeren illustrated the site-selection logic for life sciences enterprises by citing a case study on an MNC’s facility network planning in China.

The company has established its R&D base in Zhangjiang, Shanghai, leveraging the region’s abundant talent and scientific research resources to enhance R&D efficiency and innovation capabilities. Meanwhile, it has located its manufacturing operations in cities across Jiangsu and Zhejiang provinces, where operational costs are relatively lower, to control overall production costs. Additionally, the company has set up presences in regions with special market access policies, such as Hainan and the Guangdong-Hong Kong-Macao Greater Bay Area, to accelerate market expansion.

Based on this, we can clarify the core logic behind site selection for life sciences companies: carefully crafting a “combination” of locational advantages centered on key dimensions such as talent, economic strategy, and market access policies.

First is the advantage of talent aggregation.In knowledge-intensive industries such as life sciences, R&D talent has evolved from a fundamental resource into an engine of innovation. The quality of regional talent reserves can directly confer first-mover advantages in areas such as target discovery and clinical translation.

Second is nationwide coordinated deployment.Build a competitiveness matrix through differentiated resource allocation, such as establishing innovation R&D centers in first-tier cities, constructing large-scale production bases in second- and third-tier cities, and setting up cross-border healthcare hubs at border ports, to enhance overall innovation synergy efficiency and market coverage capabilities.

Then, closely align with the direction of favorable policies.Policy is a core variable in site selection, directly impacting cost structure and long-term potential. Enterprises need to precisely match regional differences in tax incentives, approval efficiency, and subsidy levels to build a value loop of "policy lowland - cost optimization - industrial highland."

Overall, by leveraging the aforementioned site selection strategies, life sciences enterprises can precisely match optimal locations to the needs of different business segments. This approach enables them to maximize talent and economic strategic advantages while reducing cost inputs, ultimately driving the sustainable development of their operations.

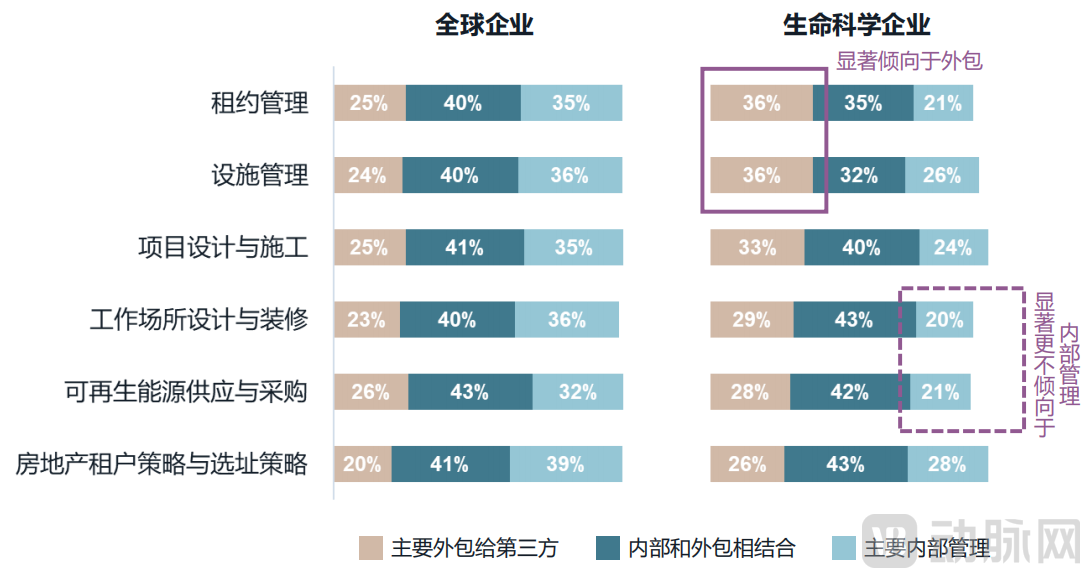

Yu Zeren noted that, much like the enabling value of CXOs to the life sciences industry, life sciences outsourcing services are gradually expanding beyond business process segments into real estate domains such as asset management and facility operations, driven by the trend toward specialized division of labor within the industry.

Data from the “2024 Future of Work Survey” shows that life sciences companies are more inclined to partner with third-party real estate service providers across multiple dimensions of real estate management, including lease administration, facility management, and project design and construction.

This forward-looking anticipation of the trend is precisely why JLL strategically entered the life sciences industry at an early stage.

After 18 years of industry experience, JLL currently has 3,800 life sciences experts worldwide, providing global life sciences clients with real estate service solutions covering the entire corporate lifecycle, including strategic planning, site selection, construction, facility management, valuation, and asset disposition.

In addition to serving the needs of multinational corporations (MNCs) in China, as mentioned earlier,Leveraging its global network, JLL provides cross-border real estate services to support Chinese enterprises in their overseas expansion, offering one-stop solutions that include market entry strategies and site selection and implementation.

Yu Zeren stated that, as a professional industry enabler, JLL positions itself as “the most specialized real estate partner in the life sciences sector.” By deeply understanding the unique characteristics of the industry, JLL empowers life sciences companies to focus more on core R&D and innovation, while providing expert real estate support in key areas such as talent attraction, technology transfer, and commercialization.

Looking ahead, as the life sciences industry continues to evolve, real estate will assume an increasingly critical role in corporate development. By striking a balance between cost reduction and efficiency enhancement on one hand, and strategic investment on the other, institutions with full-lifecycle service capabilities will empower life sciences companies to navigate economic cycles, achieving a dual leap in both spatial value and commercial value.