Consumer Healthcare Sector Reports Worst-Ever Q1 Performance Amid Industry-Wide Collapse

Eyebright Medical

Ophthalmic Medical Product R&D Provider

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

CHANGCHUN HIGH-TECH

Pharmaceutical R&D Developer

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Aier Eye Hospital

Ophthalmology Medical Chain Institution

Recently, consumer healthcare companies have successively disclosed their first-quarter reports; you never know until you look, and when you do, it’s quite a shock.With very few exceptions, nearly all have experienced a precipitous decline.。

Figure 1. Revenue and Net Profit Data of Consumer Healthcare Companies in Q1 2025 (Chart by VCBeat)

Figure 1. Revenue and Net Profit Data of Consumer Healthcare Companies in Q1 2025 (Chart by VCBeat)

Taking net profit, a key indicator, as an example,Not only did the vast majority show a downward trend, but the magnitude of the decline was also significant, with as many as seven companies experiencing drops exceeding 40%., and after a significant contraction,Many consumer healthcare companies currently report net profits of less than RMB 100 million, with a significant number having historically shifted from profitability to loss.. A typical example is Wantai Bio, the vaccine business of former richest man Zhong Shanshan, which reported a net profit attributable to shareholders of the listed company of -52.777 million yuan in the first quarter, a year-on-year decrease of 141.98%.

However, vaccines are not an isolated case,From medical aesthetics, ophthalmology, and dentistry to pharmaceutical retail, branded traditional Chinese medicine, and growth hormones, the leading companies across all sub-sectors of consumer healthcare delivered their worst-ever “report cards” in the first quarter of 2025.For instance, Haohai Biological Technology in the medical aesthetics sector saw its revenue and net profit decline simultaneously for the first time in a single quarter during Q1. Eyebright Medical in the ophthalmology sector was not spared either, with its Q1 net profit dropping by 10.05%, marking the first year-on-year decline in profits in nearly 20 quarters. Similarly, CHANGCHUN HIGH-TECH, known as the “Pharmaceutical Giant of Northeast China,” reported a 5.66% decrease in revenue and a 44.95% drop in net profit in Q1, representing its first simultaneous decline in both revenue and net profit in two decades.

Amid the market winter, it is nothing new for businesses to struggle. However, this marks the first time that consumer healthcare—a sector synonymous with high growth and exorbitant profits—is facing such severe hardship. What, then, are the reasons behind this?Why Has Consumer Healthcare, Once the Creator of Countless Performance Miracles, Fallen to Such a State Today?

The Collapse Had Early Warning Signs

The Comprehensive Collapse of Consumer Healthcare Was Not Built in a Day.

Taking the most representative sector of medical aesthetics as an example, Bloomage Biotech began its decline as early as 2023, with its net profit attributable to shareholders dropping by 39% year-on-year. However, this did not attract much attention at the time, as Imeik and Haohai Biological Technology were still maintaining high growth momentum. In 2023, Imeik’s revenue increased by 47.99%, while Haohai Biological Technology’s revenue rose by 24.59%, both reaching historical highs. Yet, after entering 2025, Imeik and Haohai Biological Technology also lost their momentum, with significant contractions in both revenue and net profit.

It is not only the medical aesthetics sector that has experienced a growth stall; the highly anticipated “golden eyes and silver teeth” sectors have also faltered. As for dentistry, needless to say, it has been mired in a wave of clinic closures in recent years.As of 2024, the closure rate of chain dental hospitals across China has reached as high as 30%.. The ophthalmology sector is similarly in decline; taking Aier Eye Hospital as an example, its revenue growth rate in 2024 hit a new low since its listing 16 years ago, while its net profit excluding non-recurring items recorded its first year-on-year decline since going public.

Amid the widespread downturn, one question is growing increasingly loud:What Are the Underlying Reasons for the Collective Slump in Performance Across the Consumer Healthcare Sector?

First and foremost, of course, is “consumption downgrading,” which is almost a common ailment across all consumer sectors.. In fact, the explosive growth of consumer healthcare has primarily stemmed from middle-class families, who once pursued beauty regardless of cost, driving rapid expansion in the sector over a short period. However, as the economy slows, they have become more budget-conscious, prioritizing essential household expenditures and gradually reducing spending on aesthetic-focused services such as medical aesthetics and dental care.

Secondly, fierce industry competition has led to a significant decline in market prices, further squeezing profit margins.Taking Juvederm Ultra as an example, its market price peaked at RMB 5,000–9,000 per syringe. However, with the proliferation of competing products, Juvederm Ultra was compelled to adopt a price-reduction strategy to retain market share. During the 2023 Singles’ Day shopping festival, its price dropped significantly to RMB 1,999, and in the past two years, it has even hit a rock-bottom price of RMB 980. The underlying reason lies in its relatively low technological barriers; once confronted with a surge of new products, its first-mover advantage is rapidly diluted, leaving it with no choice but to pursue a “low-price strategy.”

Then, the overdevelopment of the existing market has led the industry into a bottleneck phase.. Taking the nine-valent HPV vaccine as an example, it was extremely scarce in the first few years after its market launch. In Shenzhen, over 200,000 people participated in the monthly lottery for the vaccine, yet the success rate was as low as 1.7%. In their eagerness to secure a dose, many customers even traveled specifically to Hong Kong and Macau for vaccination. Despite prices being driven up to exorbitant levels of over RMB 10,000 per dose, the majority remained willing to pay.

However, the good times did not last long, as the nine-valent HPV vaccine quickly fell into the awkward situation of “inventory backlog.” Taking Zhifei Biological Products as an example, its batch release volume for the nine-valent vaccine reached 36.5508 million doses in 2023, while actual sales were only 27.4906 million doses, resulting in inventory as high as 42.096 million doses. This led to a scenario of “walk-in vaccinations” in many parts of China. The primary reason for this situation is that most eligible women in China who intended to receive the vaccine have already been vaccinated. According to estimates by Guojin Securities,By the end of 2023, the cumulative HPV vaccination coverage rate in China (based on women aged 9–45) had approached 20%, up from just 3% two years earlier.。

The final factor is policy, primarily influenced by centralized procurement and regulatory oversight.Let’s start with centralized volume-based procurement (VBP). Taking Eyebright Medical as an example, as the first domestic manufacturer of high-end refractive intraocular lenses (IOLs), the company has maintained a high-growth trajectory since its listing. However, following the implementation of the national VBP for IOLs in 2024, the winning bid price for its products dropped from RMB 3,200 per lens to RMB 2,200 per lens, a decrease of 31%. This directly led to a slowdown in the growth rate of revenue and gross profit from its surgical services business in the first quarter of this year. He Shi Eye Hospital has also been significantly impacted by VBP. The price of its refractive surgery in Beijing has fallen from around RMB 20,000 to the current RMB 17,000, while prices in other cities are even lower; for instance, the price in Guizhou has approached RMB 11,000.

Next, let us discuss regulation, which is undoubtedly the most profound change felt by consumer healthcare companies in recent years, particularly in the medical aesthetics sector, a “hard-hit area.” In 2024, the National Medical Products Administration (NMPA) revised the Guidelines for Registration Review of Hyaluronic Acid-Based Injectable Fillers for Plastic and Cosmetic Use, requiring strengthened review of clinical trial data; meanwhile, the State Administration for Market Regulation (SAMR) cracked down on false advertising in medical aesthetics, investigating and penalizing violations such as “manufacturing appearance anxiety.” This has directly led to“Compliance Costs”The significant market launch, as it requires greater investment in physician training and product certification. Taking Jinbo Bio as an example, its selling expenses increased by 56.73% year-on-year in 2024, further eroding profits.

It is not difficult to see that,Amid factors such as centralized procurement, consumption downgrading, and market competition, the growth momentum of consumer healthcare—once a “cash cow”—has slowed significantly, with some segments even grinding to a halt.。

The Future of the “Diversification” Path Remains Uncertain in the Wake of Forced Restructuring

In the past few years,A key theme in consumer healthcare is “transformation,” namely, the development of a second growth curve, which is primarily driven by pressure on financial performance.. Taking the “Three Musketeers” of hyaluronic acid as an example, they began to rapidly expand into the botulinum toxin and collagen fields through mergers and acquisitions at an early stage. In the following years, they successively entered popular sectors such as photoelectric medical aesthetics and weight loss.However, in terms of actual performance, its strategic effectiveness has fallen far short of expectations.。

Figure 2. China’s botulinum toxin market currently exhibits a “six-player” landscape (Chart by VCBeat)

Figure 2. China’s botulinum toxin market currently exhibits a “six-player” landscape (Chart by VCBeat)

This is partly due to the slow progress of the pipeline., taking Imeik as an example, its key projects—such as botulinum toxin, second-generation thread lifts, and semaglutide injection—are currently still in clinical trials or the regulatory approval stage. At that time, there were already many mature competing products on the market, meaning that it not only lacked a first-mover advantage but also faced intense industry competition after launch; therefore, its profit margins are unlikely to see substantial improvement.

On the other hand, it stems from acquisitions and mergers at high premiums, which have resulted in substantial cost burdens.. Taking Imeik as an example, the company recently acquired an 85% stake in South Korea’s REGEN at a price 13 times higher than the market value to quickly address gaps in its product portfolio, thereby securing production rights for AestheFill, known as the “baby face needle.” However, it is worth noting that Jiangsu Wuzhong has already obtained the exclusive distribution rights for AestheFill in China. Consequently, Imeik will need to rebuild its sales channels in the later stage, casting doubt on the potential synergies.

It is not only the medical aesthetics sector that has fallen into a vicious cycle of expansion; the ophthalmology field is also caught in this trap. In recent years, to rapidly seize market share and scale up, companies including Aier Eye Hospital, Huaxia Eye Hospital, and Purui Eye Hospital have actively pursued mergers and acquisitions. Taking Aier Eye Hospital as an example, by the end of 2024, its number of domestic hospitals had expanded from 215 in 2022 to 352. Although this strategy generated substantial revenue, it also incurred significantly higher operating costs, directly leading to the first-ever decline in Aier Eye Hospital’s net profit excluding non-recurring items in 2024.

In response, a senior investor in the consumer healthcare sector remarked, “While M&A-driven expansion can boost revenue and profits in the short term, it also entails challenges such as integration difficulties, debt risks, and management complexities. Once revenue growth slows and fails to cover the costs of expansion, this can quickly translate into financial pressure for the enterprise.。”

In fact,The Path of “Diversification” for Consumer Healthcare Companies Is Not Limited to Expansion but Also Includes Developing New Indications; However, Its Market Performance Has Been Equally Unsatisfactory at the Current Stage。

Taking the nine-valent HPV vaccine as an example, on April 15, 2025, Wantai Bio disclosed an announcement stating that “Phase III clinical trials of the nine-valent HPV vaccine for males have been initiated, with the first subject enrolled.” However, this news did not trigger a significant market reaction, standing in sharp contrast to the substantial market upheaval caused by the approval and launch of the nine-valent HPV vaccine several years ago.

Growth hormone faces a similar issue. Although the vast majority of its applications in China remain focused on pediatric short stature, it also plays a significant role in reproductive health, burn treatment, and anti-aging. Taking GeneScience Pharmaceuticals as an example, the indications for its recombinant human growth hormone powder for injection have increased to 11. However, at present, apart from pediatric short stature, other indications contribute little to improving financial performance.

In response, a senior investor analyzed the reasons behind this, “In fact, within the same application domains, such as anti-aging, there are already numerous mature products available, and growth hormone has not demonstrated significant superiority in terms of specific efficacy. Furthermore, from the perspective of market acceptance, growth hormone has long been associated with pediatric short stature; patients find it difficult to link it with anti-aging or even burn treatment, and are therefore unwilling to pay for it.。”

It is evident that although consumer healthcare companies are currently generating revenue through various channels, the results have been minimal at this stage. In fact, some have even fallen into a profitability trap due to the substantial costs associated with their transformation.

The Era of Windfall Profits Is Over: The Future Will Belong to “Technology-Driven” Players

According to statistics from Yuekai Securities,China's Consumer Healthcare Market Reaches Trillion-Yuan Scale. Among these, the market size for specialized medical fields such as ophthalmology, stomatology, and assisted reproduction reached RMB 382.62 billion, and is projected to reach RMB 605.88 billion by 2025; the market size for the medical aesthetics sector reached RMB 226.7 billion, and is expected to reach RMB 352.9 billion by 2025. This indicates that the overall development potential of consumer healthcare remains substantial.

At the same time, the industry also needs to clearly recognize that,The consumer healthcare sector is unlikely to replicate the high-growth miracle of the past decade, primarily because the underlying industry logic has subtly shifted.. In the past, due to strong market demand coupled with information asymmetry,VeryMany consumer healthcare companies have been able to reap easy profits and create one performance miracle after another simply by relying on marketing blitzes.。

However, as market demand gradually approaches saturation and the industry continues to develop rapidly, this “golden age” has come to an end, and a harsh new cycle is descending.All must delve deeper into the industry and pursue growth and future prospects through refined operations.. Specifically, this is reflected in three key dimensions:Deepening Innovative Technologies, Establishing Differentiated Services, and Controlling Customer Acquisition Costs。

There is no need to elaborate on the technical aspect; it simply involves enhancing therapeutic efficacy through R&D or continuously launching new, groundbreaking products.For instance, the viral popularity of treatments such as PLLA-based “baby face” injections, CaHA-based “girl” injections, PDRN “salmon” injections, and hydroxyapatite fillers in recent years is essentially the result of technological innovation, successfully applying mature technologies from other fields to medical aesthetics. This trend is further corroborated by R&D investment data: in 2024, the R&D expenditure growth rates of the “Big Three” hyaluronic acid manufacturers remained around 10%, with Imeik reaching as high as 21.41%.

Then, in terms of differentiated services, since consumer healthcare generally involves low technical barriers, product homogenization is quite severe. Consequently, standing out often requires incurring higher sales costs. However, differentiated services can effectively alleviate this pressure.On the one hand, by targeting different application areas and user groups, taking Giant Biogene as an example, the company focuses on the field of collagen and has currently reserved nearly 10 types of recombinant collagen, which has resulted in positive feedback on its performance. In 2024, both the revenue and net profit growth rates of Giant Biogene exceeded 40%.

On the other hand, it involves creating distinct differentiation in specific services.Taking Aier Eye Hospital as an example, in recent years, it has successively launched personalized services such as “initial consultation by physicians and one-on-one compassionate care,” “global remote follow-up examinations and lifelong eye health management,” and the “Aier Eye Hospital Myopia Surgery Quality Control System.” The underlying objective is self-evident: to refine service delivery, better serve patients, and thereby cultivate a strong brand effect.

Lastly, controlling customer acquisition costs is mentioned, which is primarily achieved by adopting new technologies or accessing new market channels to maximize benefits within an effective budget.. Taking a chain of ophthalmology clinics as an example, after embedding AI technology for customer acquisition, its customer contact retention rate increased from 38% to 60%, while the cost per person decreased from RMB 200 to RMB 68, and the ROI (return on investment) rose to 42%.

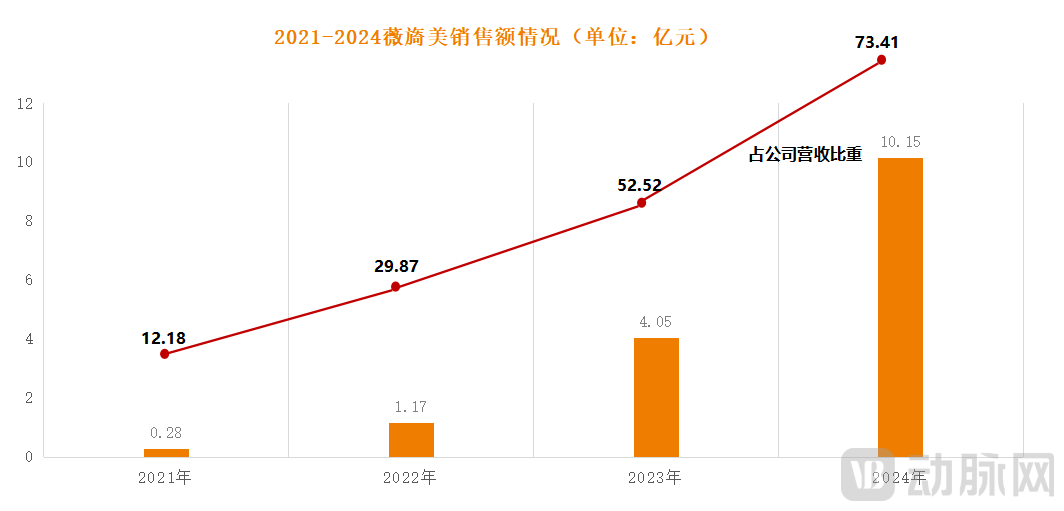

Figure 3. Sales Performance of Jinbo Bio’s Weiyimei (Chart by VCBeat)

Figure 3. Sales Performance of Jinbo Bio’s Weiyimei (Chart by VCBeat)

Furthermore, emerging platforms are also helping consumer healthcare enterprises reduce customer acquisition costs and improve efficiency. A prime example is Xiaohongshu (Little Red Book). According to Deloitte’s “2024 Annual Insights Report on China’s Medical Aesthetics Industry,” 88% of medical aesthetics consumers currently obtain information from Xiaohongshu, which has clearly driven substantial traffic to the platform. In June 2024, sales of Weiyimei officially surpassed one million vials, a milestone to which Xiaohongshu contributed significantly. Not only were nearly 100 products sold on the platform, but Weiyimei also consistently ranked first in mention rate within shares related to recombinant collagen, thereby generating substantial revenue.

In fact,The explosive growth of consumer healthcare in the past has, to some extent, prematurely exhausted demand for the coming years.. But as the market gradually returns to rationality, consumer healthcare companies are required to rapidly complete their transformation:Transitioning from the emerging market model, characterized by extensive practices and heavy reliance on marketing, to the mature market model, defined by refined management and dependence on repeat purchases.。

This is an unprecedented challenge, and of course, a once-in-a-lifetime opportunity.

1. “Consumer Healthcare: Accelerating Collapse?” – Anji Observation;

2. “The Great Collapse of Consumer Healthcare: The Blood-and-Tears Saga from HPV Vaccines to Growth Hormones—Who Can Survive This ‘Mountain of Corpses and Sea of Blood’?” — Yidaoshe;

3. “Consumer Healthcare Grinds to a Halt: The ‘Blue-Chip Aesthetic Medicine’ Stock Endures Hard Times, and the ‘Golden Eyes, Silver Teeth’ Sectors Lose Their Luster” — China Times.