China Resources Sanjiu to Divest 51% Stake in Hubei JiuZhouTong Pharmaceutical Technology for RMB 10.86 Million

CR SANJIU

Pharmaceutical R&D, Production, Sales, and Related Health Service Provider

On May 13, 2025, listing information from the Shanghai United Assets and Equity Exchange showed that CR SANJIU (000999.SZ) was listing for transfer a 51% equity stake in Hubei Jointown Pharmaceutical Technology Co., Ltd., with a minimum transfer price of RMB 10.86 million and a disclosure period ending on June 10, 2025.

Image source: Shanghai United Assets and Equity Exchange

Image source: Shanghai United Assets and Equity Exchange

In fact, it has been only a week since CR SANJIU was last reported to be acquiring assets.

In early May, the listing information on the Shanghai United Assets and Equity Exchange still showed that CR SANJIU was listing for transfer its 49.8967% equity stake in Sanjiu (Anguo) Modern Traditional Chinese Medicine Development Co., Ltd., with a minimum transfer price of RMB 1.6215 million.

“CR Group” Divests Assets Again to Focus on Core Business

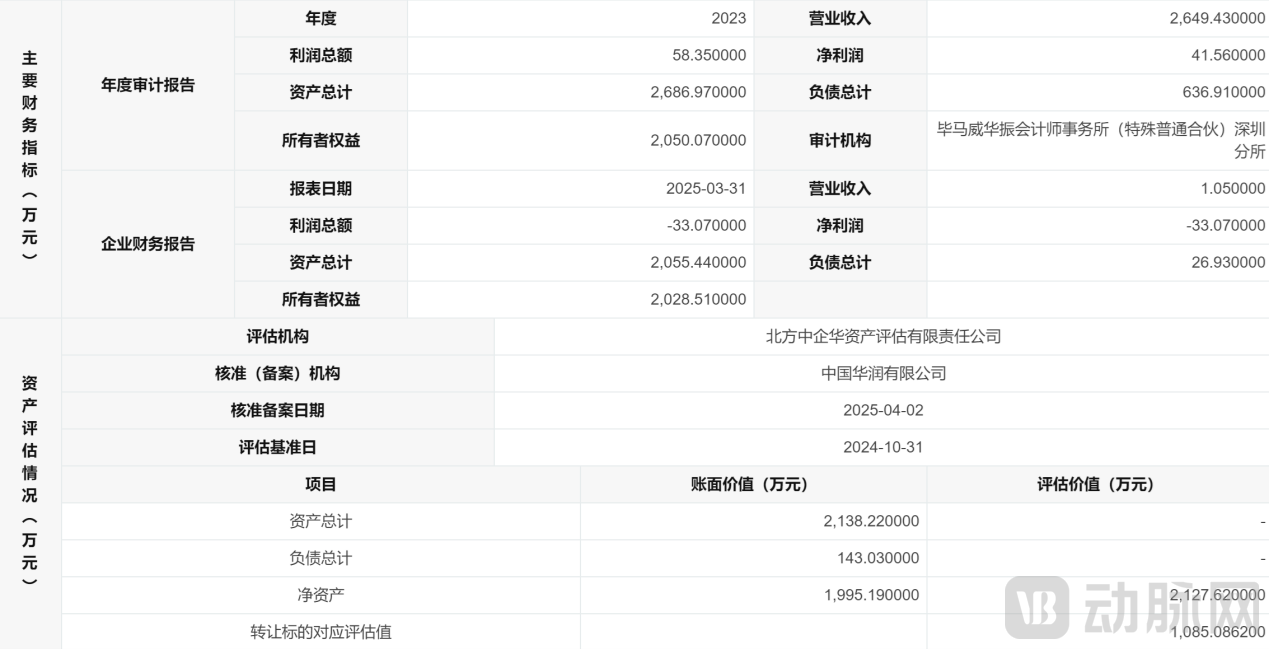

According to the listing information, Hubei Jointown Pharmaceutical Technology Co., Ltd. was established in 2021, with a registered capital of RMB 50 million. The legal representative is Zhou Han, and its business scope includes pharmaceutical wholesale, medical device operations, food sales, and internet-based drug information services, among others.

According to the listing information on the Shanghai United Assets and Equity Exchange, Hubei Jointown Pharmaceutical Technology Co., Ltd. is a subsidiary of CR SANJIU, with CR SANJIU directly holding 51% of its equity and Jointown Pharmaceutical Group holding 49%. As CR SANJIU’s shareholding meets the threshold for absolute control (more than 50%), it will no longer hold a controlling interest in the company upon the successful completion of this transfer.

CR SANJIU’s withdrawal this time is not only because the business of Hubei Jointown Pharmaceutical Technology Co., Ltd. does not fall within its core strategic layout, but more importantly due to the loss-making status of Hubei Jointown Pharmaceutical Technology. According to information from the Shanghai United Assets and Equity Exchange, in 2023, Sanjiu (Anguo) Modern Traditional Chinese Medicine recorded revenue of RMB 26.4943 million, a net profit of -RMB 330,700, total assets of RMB 21.3822 million, and total liabilities of RMB 1.4303 million. The main financial data for 2024 have not yet been disclosed.

Source: Shanghai United Assets and Equity Exchange

Source: Shanghai United Assets and Equity Exchange

After divesting non-core assets, CR SANJIU will undoubtedly be able to concentrate more resources and efforts on its core businesses, particularly in consolidating its leading position in the CHC (Consumer Health Care) and prescription drug sectors, thereby enhancing the competitiveness and profitability of its core operations. Therefore, this equity transfer represents not only a timely stop-loss measure for loss-making assets but also an inevitable strategic choice for CR SANJIU to focus on its main business.

As previously mentioned, this marks the second time in just one week that CR SANJIU has divested non-core assets. However, taking a longer-term view reveals that since the beginning of this year, the “China Resources” group has been more active and frequent in asset sales than in bold mergers and acquisitions.

On April 13, 2025, China Resources Boya Bio-pharmaceutical Group Co., Ltd. (“Boya Bio”) announced its intention to list for transfer an 80% equity interest in Boya Xinhe via the Shanghai United Assets and Equity Exchange. The initial listing price is approximately RMB 213 million (subject to the appraised value filed with the entity authorized by the state-owned assets supervision and administration authority). Upon completion of the equity transfer, Boya Bio’s shareholding in Boya Xinhe will decrease from 90.69% to 10.69%, and Boya Xinhe will no longer be included in the consolidated financial statements of Boya Bio.

In fact, Boya Xinhe’s revenue performance is similar to that of Sanjiu (Anguo) Modern Traditional Chinese Medicine Development Co., Ltd. and Hubei Jointown Pharmaceutical Technology Co., Ltd., as all three have been experiencing consecutive losses. The former incurred a loss of RMB 56.87 million in 2023 and RMB 34.62 million in 2024, becoming a non-core business burden for Boya Bio-pharmaceutical Group.

On the other hand, Jointown Pharmaceutical Group has not yet publicly announced any intention to sell its 49% equity stake in Hubei Jointown Pharmaceutical Technology Co., Ltd. Jointown Pharmaceutical Group is a technology-driven, full-chain comprehensive healthcare industry service provider. It was listed on the Shanghai Stock Exchange on November 2, 2010, and is currently the largest listed company in Hubei Province by revenue. Rooted in the broader health industry, the company’s core businesses span six major areas: digital pharmaceutical distribution and supply chain services; exclusive agency brand promotion; in-house pharmaceutical manufacturing and OEM services; new retail and franchise network operations (consumer-facing); consumer healthcare and technical value-added services; and digital logistics technology and supply chain solutions.

Navigating the Path of Chinese-Style MNC M&A?

According to VCBeat statistics, the China Resources Group alone spent over RMB 13 billion on mergers and acquisitions in 2024.

In its 2024 annual report, CR SANJIU stated that its strategic goal for the “14th Five-Year Plan” period is to strive to become an industry leader and double its operating revenue. The company will benchmark itself against world-class enterprises, refine its business layout, expand its core business into all areas of self-care, and focus on developing its product pipeline to empower its core business.

During the 14th Five-Year Plan strategic period, CR SANJIU will focus on implementing strategic initiatives such as integrating high-quality industry resources, strengthening international cooperation, and enhancing industrial competitive advantages; deeply advancing the SOE Reform Deepening and Upgrading Action to improve core corporate competitiveness and strengthen core functions.

Similar to overseas giants, China Resources Group has strengthened its “core” strategy through mergers and acquisitions (M&A), rapidly growing into a domestic pharmaceutical powerhouse. From Huayuan Group to Sanjiu Group, from Aonuo Pharmaceutical to Kunming Shenghuo, and from Shuanghe Pharmaceutical and Zizhu Pharmaceutical to Wandong Medical, China Resources Pharmaceutical Group has gradually built a carrier-grade pharmaceutical platform through acquisitions. This platform spans traditional Chinese medicine, innovative drugs, blood products, vaccines, and high-end medical devices, with business operations covering the entire industry chain.

However, China Resources Pharmaceutical Group’s bulk acquisitions have also triggered issues of horizontal competition. Specifically, the businesses of the acquired companies compete with those of other subsidiaries, leading to friction and redundant competition. This not only results in resource wastage but also hinders the group from leveraging its synergistic advantages.

For example, Kunming Pharmaceutical Group was merged into CR SANJIU in January 2023. Prior to this, Kunming Pharmaceutical Group’s business covered drug R&D, manufacturing, sales, and commercial wholesale, spanning multiple therapeutic areas including cardiovascular and cerebrovascular diseases, orthopedics, antimalarial treatments, gynecology, and gastroenterology. At that time, Kunming Pharmaceutical Group’s pharmaceutical distribution business competed with CR SANJIU’s existing operations, and its blockbuster product, Xuesaitong Soft Capsules, which generated over RMB 100 million in revenue, also competed with Shenghuo Pharmaceutical, a subsidiary of CR SANJIU.

The CR Group’s approach has been to divest, acquire, and integrate its business operations.

After CR SANJIU gained actual control of Kunming Pharmaceutical Group, it gradually divested the latter’s pharmaceutical distribution business and reduced its equity stakes in non-core businesses such as Fuda Pharmaceutical and Tian’an Pharmaceutical. This strategic shift enabled Kunming Pharmaceutical Group to focus on the healthy aging sector and pursue its strategic goals of becoming “a leader in the silver economy health industry, a premier provider of premium traditional Chinese medicines, and a leader in elderly health and chronic disease management.”

On the other hand, the divestiture of assets by companies under the China Resources (CR) group, particularly CR SANJIU, has also been linked to its stock price decline in the last quarter of 2024. CR SANJIU has long been known for its stability in the securities market, making the sudden drop in its share price a rare occurrence. Some market observers believe that the decline in CR SANJIU’s stock price may be related to the “expansion” of centralized procurement. The draft consultation paper on the 2024 annual centralized procurement of proprietary Chinese medicines issued by Anhui Province stated that “centralized procurement is planned for 35 varieties of proprietary Chinese medicines,” which, for the first time, included several over-the-counter (OTC) drugs. These include billion-yuan OTC proprietary Chinese medicine varieties such as Ganmaoling, Ganmao Qingre, Shaoer Feire Kechuan, and Qiangli Pipa Lu. As the manufacturer of the 999-branded Ganmaoling and Qiangli Pipa Lu, CR SANJIU’s profitability and ability to continue operations may therefore be impacted.

The decline in CR SANJIU’s stock price may also be attributed to issues arising from its frequent and aggressive mergers and acquisitions (M&A), particularly the accelerated pace of these deals over shorter timeframes. After all, sustained large-scale M&A activity can, to some extent, impair CR SANJIU’s asset quality. As market conditions shift, its underlying vulnerabilities have gradually come to light, leaving less room for maneuver.

In addition to addressing horizontal competition, the China Resources group has accelerated the integration of its traditional Chinese medicine (TCM) business through mergers and acquisitions. Meanwhile, against the backdrop of mounting pressure on the pharmaceutical industry, CR SANJIU has stated that it prioritizes the quality of external M&A activities.

From 2024 to the present, healthcare enterprises under the China Resources (CR) group have been actively acquiring assets throughout the year, while also frequently announcing divestitures. Nevertheless, with an increasing emphasis on the quality of external M&A, the CR group is likely to intensify its search for targets and will continue to prioritize investment and mergers and acquisitions as a key strategic focus in the future.

Perhaps, as the China Resources group, represented by CR SANJIU, achieves optimized resource allocation and synergies through a series of strategic M&A transactions and equity transfers, it will truly forge a Chinese-style path for multinational corporations’ growth through mergers and acquisitions.