Hanbon Sci-Tech Soars 102% on IPO Debut: China's Chromatography Leader Breaks Foreign Dominance

Yesterday, Hanbon Technology, the leading domestic manufacturer of liquid chromatography systems, successfully completed its initial public offering (IPO) on the STAR Market. On its first day of trading, Hanbon Technology closed at RMB 48.23 per share, surging 102.461% in a single day, with a total market capitalization reaching RMB 4.057 billion.

Hanbon Technology’s core business involves the research, development, and manufacturing of liquid chromatography systems for small-molecule and large-molecule drugs, providing separation and purification equipment, consumables, application technical services, and related technical solutions to the pharmaceutical, life sciences, and other sectors. This market has long been dominated by overseas companies, with domestic enterprises only recently gaining a firm foothold.

The key to breaking through lies in mastering core technologies. After 27 years of dedicated effort, Hanbon Technology has gradually overcome various technical challenges in chromatographic separation and purification, achieving linear scale-up of sample separation and purification from gram, tens-of-grams, and hundreds-of-grams scales to the kilogram scale. Its related products and technologies have been applied to the research, development, and production of pharmaceuticals and natural products, including antibodies, recombinant proteins, vaccines, insulin, peptides, contrast agents, and antibiotics.

Furthermore, Hanbon Technology is continuing its R&D efforts in chromatography packing materials/media and plans to establish an industrialization base for these products. This initiative aims to further enhance the profitability of its “equipment + consumables + services” model and open up new revenue streams.

Leveraging the aforementioned advantages, Hanbon Technology achieved sustained growth even during the economic downturn. From 2022 to 2024, Hanbon Technology’s operating revenues were RMB 480 million, RMB 610 million, and RMB 690 million, respectively; its net profits attributable to shareholders of the parent company were RMB 38.5596 million, RMB 51.4975 million, and RMB 79.3382 million, respectively. During the reporting period, the company’s compound annual growth rate (CAGR) for operating revenue reached 19.75%, while the CAGR for net profit attributable to shareholders of the parent company was 43.44%.

According to the prospectus, the funds raised by Hanbon Technology in this IPO will be used to expand production capacity, including investment in projects such as the annual production of 1,000 units of liquid chromatography separation equipment, the construction of a chromatography separation equipment R&D center, and the annual production of 2,000 units (sets) of laboratory chromatography separation and purification instruments.

For the entire medical industry, the rise of Jiangsu Hanbon Science & Technology Co., Ltd. holds unique significance. Due to the relatively late start of China’s high-end pharmaceutical equipment sector, core production equipment required for domestic drug R&D and manufacturing—such as preparative chromatography systems—has long relied on imports. This has kept equipment procurement and maintenance costs persistently high, directly impeding the upgrading and development of the pharmaceutical industry.

Amid the current crisis of deglobalization, China’s medical manufacturing industry requires upstream core instrument manufacturers, such as Jiangsu Hanbon Science & Technology Co., Ltd., to expedite technological breakthroughs and achieve self-sufficiency in component production. This will ensure the steady development of the pharmaceutical and medical device manufacturing system within a relatively secure supply chain environment, ultimately breaking through the industry’s capacity ceiling.

Hanbon Science & Technology’s Path to Breakthrough: Attributable to Technological Innovation and Early Strategic Layout

A liquid chromatography system comprises over 3,000 components, all of which are precision parts. To complete the system design, it is essential to fully consider the compatibility among these intricate components. For instance, the tubing within a liquid chromatograph is extremely narrow; developers must prevent liquid from adhering to and stagnating on the tube walls, and thus need to apply a pressure differential across the tubing to drive fluid flow. To ensure the normal operation of this system, considerable effort must be devoted to materials and manufacturing processes to guarantee the toughness of the tube walls.

Furthermore, achieving consistent mass production of liquid chromatographs is a critical challenge that domestic enterprises must overcome. Only through continuous adjustment and refinement of every component and process under precise manufacturing techniques can exceptional and stable overall performance be ensured.

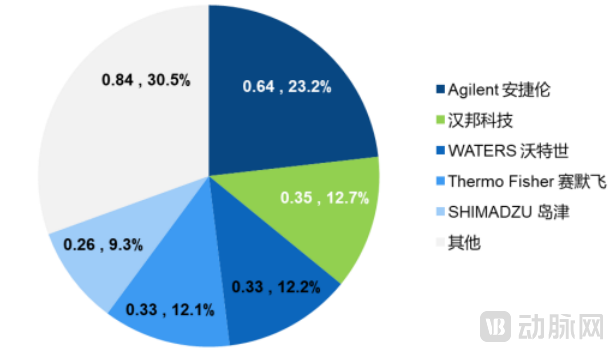

Therefore, the technological barriers that Hanbon Technology has built over several years are key to its success in capturing and sustaining market share. According to Frost & Sullivan data, the total market size for liquid chromatography equipment (including both production-scale and laboratory-scale) in China exceeded RMB 2.7 billion in 2023. Agilent held the largest share at 23.2%, while Hanbon Technology ranked second with approximately 12.7% market share, driven by rapid growth in the production-scale liquid chromatography separation equipment segment, thereby surpassing overseas brands such as Waters, Thermo Fisher Scientific, and Shimadzu.

Market Share of Major Competitors in China’s Liquid Chromatography Equipment (Chemical Drugs) Market (2023)

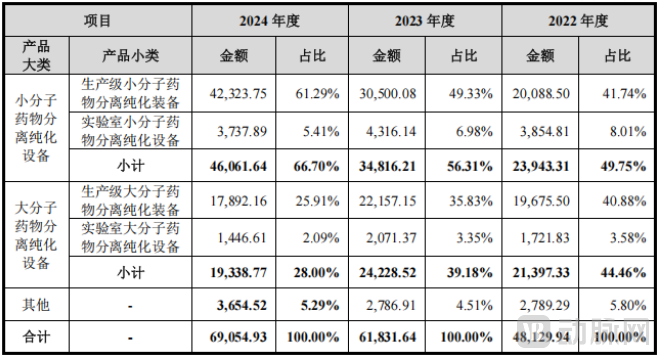

Hanbon Technology’s pipeline can be further segmented into separation and purification equipment for small-molecule drugs and that for large-molecule drugs. These two business lines are currently the pillars of Hanbon Technology, with a combined revenue of RMB 654.0041 million in 2024, accounting for 94.6% of its total revenue.

Revenue from Hanbon Technology’s Core Business Segments (Source: Prospectus)

Production-grade small-molecule equipment is Hanbon Technology’s fastest-growing business segment over the past two years, maintaining a growth rate of over 40% annually from 2022 to 2024.

The growth momentum for such equipment is primarily driven by the need to expand production capacity for GLP-1 peptide drugs. Relevant data indicate that the global market size for GLP-1 drugs is projected to exceed $90 billion by 2030. In China, semaglutide, liraglutide, and other variants have entered late-stage clinical trials, spurring a surge in demand for equipment from Jiangsu Hanbon Science & Technology Co., Ltd.

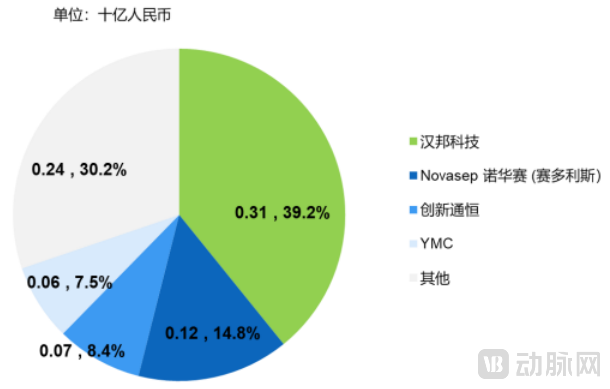

It is reported that Hanbon Technology’s CS-Prep series of industrial preparative liquid chromatography systems have been deployed in the production lines of companies such as Gan & Lee Pharmaceuticals and Asymchem. In 2023, revenue from equipment related to peptide drugs accounted for 59.8% of the total.

Market Share of Major Competitors in China's 2023 Production-Grade Small Molecule Liquid Chromatography System Market

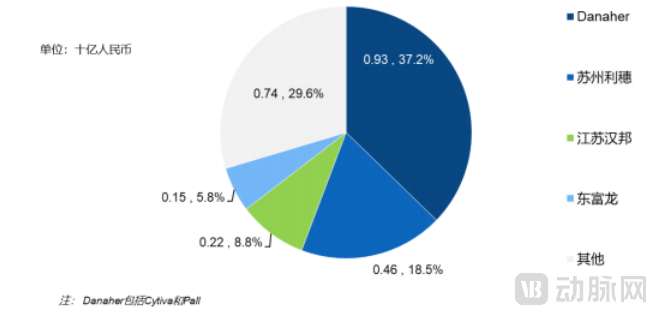

In the realm of production-grade macromolecule equipment, brands under Danaher, such as Cytiva and Pall, hold a leading position in both international and domestic markets due to their advanced technological expertise and early market entry. They offer comprehensive end-to-end equipment solutions for upstream and downstream manufacturing, along with customized complementary products including culture media, consumables, and resins, making it challenging for competitors to break through.

Furthermore, influenced by the anticipated correction in expectations and reduced investment among pharmaceutical and CXO companies, the overall market for chromatography systems within the production-grade macromolecule equipment sector (accounting for approximately 70% of the total market) experienced a slight price decline, a reduction in customer orders, and a modest contraction in overall market size in 2023 compared to 2022.

Data from the prospectus shows that although Hanbon Technology’s market share in the production-scale macromolecular chromatography system market has changed little over the past three years, its revenue has maintained a growth rate of over 20%, indicating continued opportunities for breakthroughs in the future.

Market Share of Major Competitors in China's Production-Grade Macromolecule Chromatography System Market in 2023

Revisiting Early Strategic Deployment. In addition to Jiangsu Hanbon Science & Technology Co., Ltd., numerous domestic enterprises are also striving for breakthroughs in the field of separation and purification, even attempting to establish fully localized equipment setups and conduct component testing.

In the long run, this strategic layout is expected to help China’s pharmaceutical industry further strengthen its voice in the global market and circumvent sanctions such as tariffs and bans. However, in the short term, not every biopharmaceutical company is willing to risk its high-value-added active pharmaceutical ingredients (APIs) in such endeavors.

Therefore, Hanbon Technology’s ability to take the lead in the current separation and purification market is inseparable from its forward-looking layout initiated in the last century, which allowed ample time for the market to affirm its technology. However, as China’s mass spectrometry supply chain gradually matures, Hanbon Technology must also build new barriers to cope with emerging challenges from domestic competitors.

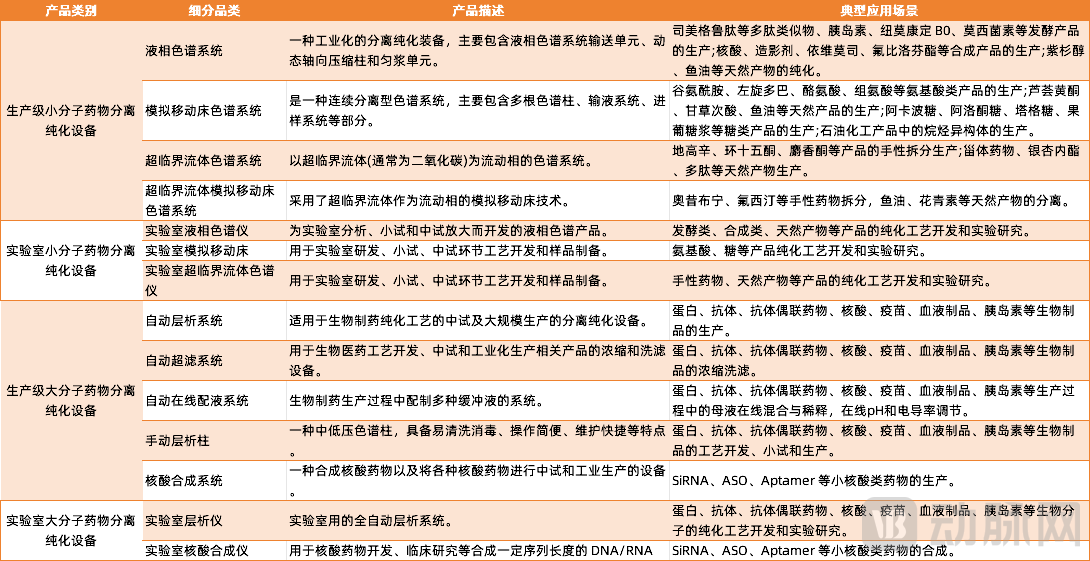

Hanbon Science & Technology’s Complete Pipeline

Hanbon Science & Technology’s Complete Pipeline

Despite maintaining sustained and robust growth during the reporting period covered in its prospectus, Jiangsu Hanbon Science & Technology Co., Ltd. still faces potential risks under the current macroeconomic environment.

On the one hand, influenced by factors such as adjustments in downstream market demand for biopharmaceuticals and intensified competition among domestic brands, the selling prices and gross profit margins of large-molecule drug separation and purification equipment are showing a downward trend. If future demand for capacity expansion in the downstream biopharmaceutical market weakens, or if industry competition intensifies leading to a decline in product selling prices, or if costs rise due to factors such as increasing raw material prices, the gross profit margins of Hanbon Technology’s main products, particularly large-molecule drug separation and purification equipment, face the risk of decline, thereby affecting the company’s performance.

On the other hand, although Hanbon Technology has consistently maintained its leading market share in China’s production-scale small-molecule liquid chromatography system market, its market share was already high, reaching 39.2% in 2023, leaving limited room for further growth. Consequently, future revenue growth is likely to be driven primarily by the expansion of the overall market size.

To address the aforementioned challenges, Hanbon Technology’s current strategy focuses on expanding the scope of product applications and accelerating overseas expansion. Notably, in its international markets, Hanbon Technology reported overseas operating revenues of RMB 29.4181 million, RMB 87.8044 million, and RMB 178.7022 million in 2022, 2023, and 2024, respectively. These figures accounted for 6.11%, 14.20%, and 25.88% of its total operating revenue, demonstrating a trend of rapid year-over-year growth.

According to the prospectus, Hanbon Technology’s domestic customers are primarily pharmaceutical R&D and manufacturing enterprises, while its overseas customers include integrators of pharmaceutical production line equipment, rare earth producers, and others. Currently, Hanbon Technology has secured overseas clients such as India’s INTECH ANALYTICAL INSTRUMENTS and Norway’s REETEC AS, and is poised to further expand its international presence in 2025.

In recent years, a growing number of investment institutions have turned their attention to the core equipment and key components in the upstream segment of the pharmaceutical and medical device industries. By partnering with these high-tech enterprises, they are helping China’s high-end medical manufacturing sector break through bottlenecks and achieve comprehensive localization.

Today, the success of Jiangsu Hanbon Science & Technology Co., Ltd. further demonstrates that upstream enterprises in medical manufacturing are capable of breaking through in technological competition, achieving both full domestic substitution across the entire industrial chain and individual corporate profitability.

During the development of Hanbon Science & Technology from 2012 to 2022, we saw the presence of top-tier investment institutions such as Zero2IPO, Legend Capital, and Sequoia Capital, as well as the support of industry leaders like Tofflon and WuXi AppTec.

Jiangsu Hanbon Science & Technology Co., Ltd.'s Financing History

It is hoped that more manufacturers of core equipment and critical components in need of capital will receive support from investment institutions in future development, thereby accelerating the process of domestic substitution and driving the entire industry toward a higher level.