From Sales Halving to a 67.5% Surge: Why the Medical Equipment Market Can't Claim a 'Boom'

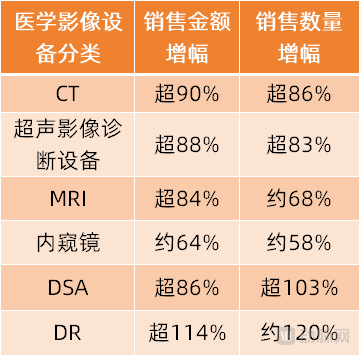

In the first quarter of 2025, sales of medical imaging equipment in China surged, with a year-on-year increase of 78.43%. By sales revenue, DR systems increased by over 114% year-on-year, CT scanners by over 90%, ultrasound imaging equipment by over 88%, and DSA systems by over 86%. In terms of sales volume, DR systems rose by approximately 120% year-on-year, DSA systems by approximately 103%, and CT scanners by approximately 86%.

(Market Performance of Various Products in Q1 2025; Data Source: Yizhuang Shusheng)

The near-doubling of growth has led some industry insiders to mistakenly believe that “medical equipment orders have surged,” prompting them to promote the notion of a “booming medical equipment market.” However, this is not the case. Data analysis alone reveals that the substantial year-over-year increases in both sales revenue and volume are attributable to the low base effect from the same period last year.

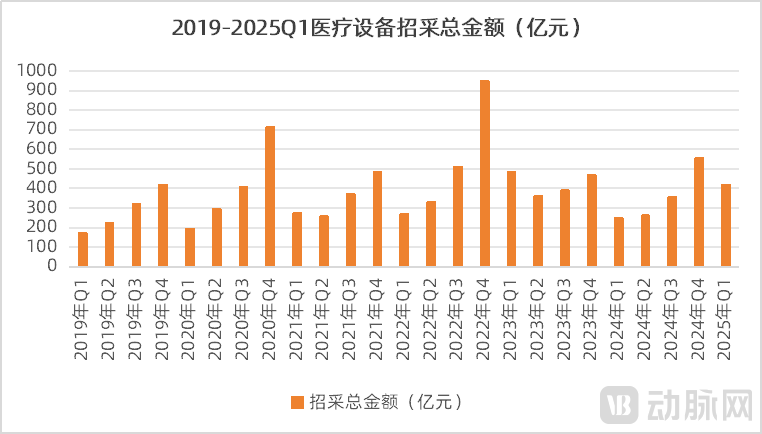

According to statistics from Zhongcheng Shuke, the total value of medical equipment procurement bids rose by 79.93% year-on-year in the first quarter of 2023, marking rapid growth; in the first quarter of 2024, the total procurement value dropped sharply by 48.35%, with sales volume nearly halved, significantly lowering the base; in the first quarter of 2025, the total value of medical equipment procurement bids increased by 67.5% year-on-year.From a long-term perspective, the total procurement amount for medical equipment in the first quarter of 2025 remained lower than that in the first quarter of 2023.

(Data source: Zhongcheng Shuke)

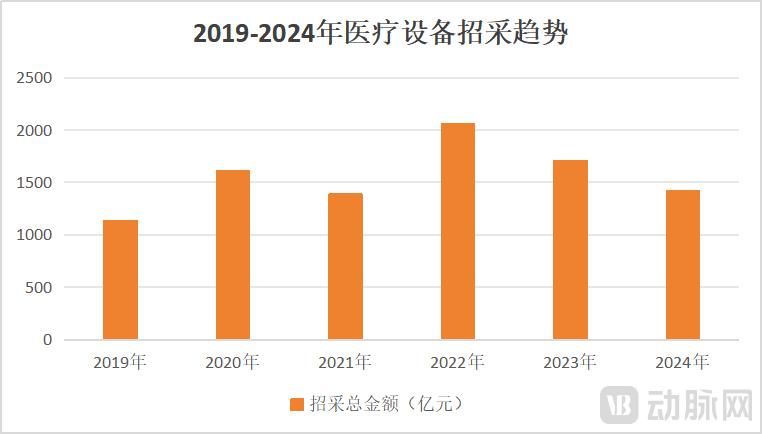

From a long-term perspective, the medical device market has not yet fully taken off and remains in a recovery phase.。

Looking back at the past few years, 2022 marked a peak in the medical device market, driven primarily by policy initiatives.

First, new healthcare infrastructure initiatives have unleashed demand for hospital construction and stimulated the procurement of medical equipment. Since 2020, the state has successively issued policy documents such as the “Plan for Strengthening Public Health Prevention, Control, and Treatment Capabilities,” the “Opinions on Promoting High-Quality Development of Public Hospitals,” the “Action Plan for Promoting High-Quality Development of Public Hospitals (2021–2025),” and the “Work Plan for Enhancing the Comprehensive Capabilities of County Hospitals under the ‘Thousand Counties Project’ (2021–2025).” These policies require hospitals to address resource shortcomings and enhance treatment capabilities, thereby giving rise to a new wave of healthcare infrastructure development.

In 2021, four ministries and commissions jointly issued the “Implementation Plan for the Construction of a High-Quality and Efficient Medical and Health Service System during the 14th Five-Year Plan Period,” which calls for the establishment of several National Medical Centers with appropriately forward-looking planning.Configuration of Large-Scale Medical Equipment, develop smart hospitals and databases for major diseases.

For the national and provincial regional medical centers whose construction is being accelerated, the state requires them to focus onStrengthening the Procurement of Medical Equipment, informatization and research platform construction, establishment of telemedicine and education platforms, and acceleration of the intelligent transformation and upgrading of diagnostic and treatment equipment.

The “Thousand Counties Project” Work Plan for Enhancing the Comprehensive Capabilities of County Hospitals (2021–2025) requires that at least 1,000 county hospitals across China achieve the medical service capacity level of tertiary hospitals, thereby improving their diagnostic and treatment capabilities for common diseases, frequently occurring illnesses, and major conditions such as cancer. This necessitates that county-level hospitals purchase and upgrade medical equipment, including medical imaging devices.

These policies explicitly call for strengthening the allocation of medical equipment, particularly in areas with weak infrastructure, where significant gaps in medical equipment and service capacity remain to be addressed.

In 2022, the aforementioned policies were successively implemented.This has spurred a new wave of “new healthcare infrastructure” development in China. Meanwhile, pent-up demand from the pandemic period has been released, accelerating the procurement of medical equipment such as medical imaging devices.

Second, following the release of demand, the state has helped hospitals address funding challenges through various loan policies. In addition to annually planned subsidy funds, instruments such as local government special-purpose bonds for healthcare and phased fiscal interest-subsidized loans have provided ample sources of financing for new healthcare infrastructure. According to Mindray’s annual report: the local government special-purpose budget for healthcare was only RMB 33 billion in 2019; this amount rose to approximately RMB 285 billion in 2020, and the issuance scale exceeded RMB 350 billion in 2022, marking a significant increase.

In September 2022, the National Health Commission further facilitated the upgrading and renovation of medical equipment through interest-subsidized loans, involving a total fund of RMB 200 billion. Following the release of this policy, interest-subsidized loans became a significant source of funding for medical equipment procurement. Medical equipment companies promptly launched corresponding product solutions, stimulating a substantial surge in procurement spending. For instance, the total value of medical equipment tenders and procurements in the fourth quarter of 2022 increased by approximately 95.67% year on year.

Overall,In 2022, driven by the dual engines of new healthcare infrastructure development and financial support, the procurement value of China’s domestic medical device market surged.。

In the first half of 2023, new healthcare infrastructure development continued to exert a significant driving effect on the procurement of medical equipment.. In particular, the state has issued multiple policies to continuously promote the allocation of medical imaging equipment, driving substantial volume growth in the medical device market.

In March 2023, the National Health Commission released the “Catalogue for the Administration of Licensing for the Allocation of Large Medical Equipment (2023),” removing CT scanners with 64 slices or more and MR systems with 1.5T or higher from the regulated categories, thereby further unleashing procurement demand that had previously been constrained by allocation permits.

In June 2023, the National Health Commission issued the “Notice on the 14th Five-Year Plan for the Allocation of Large-Scale Medical Equipment.” The Plan indicates a substantial increase in the number of large-scale medical equipment units to be allocated during the 14th Five-Year Plan period: the planned number of PET/MR systems is 141, representing an 83% increase over the previous period; the planned number of PET/CT systems is 860, a year-on-year increase of 56%. The Plan also significantly lowers the allocation thresholds. For instance, the previous infrastructure requirement for PET/MR—namely, at least three MR scanners and one PET/CT system—has been revised to require at least one MR scanner and one PET/CT system. These adjustments and changes are driving the continued expansion of the medical imaging equipment market.

Supported by policy, the procurement amounts for medical equipment in the first and second quarters of 2023 increased by 79.9% and 10% year-on-year, respectively.。

However, in the second half of 2023, the medical device market took a sharp downturn.. In July 2023, the National Health Commission, together with the Ministry of Public Security and eight other departments, launched a year-long nationwide campaign to address corruption in the pharmaceutical and healthcare sectors. During the same month, provinces formulated local anti-corruption rectification plans for the pharmaceutical industry and actively advanced various centralized governance initiatives.

Affected by the anti-corruption campaign in the pharmaceutical and healthcare sectors, domestic medical equipment bidding processes have been widely postponed, and academic activities have been canceled or delayed, delivering a significant shock to the market for medical imaging and other equipment.

Furthermore, in the fourth quarter of 2023, the issuance of special-purpose bonds for healthcare was temporarily suspended, hindering the advancement of new healthcare infrastructure and further exacerbating the downturn in the medical equipment market, particularly for modalities such as medical imaging.

Compounded by the surge in medical equipment procurement during the same period in 2022 (driven by interest-subsidized loan policies), which raised the base figure, the total value of medical equipment tenders and procurements in the second half of 2023 declined significantly year-on-year.The total procurement amount for medical equipment in the third and fourth quarters of 2023 decreased year-on-year, respectively.23.53%、50.68%。

For the full year of 2023, the medical imaging equipment market exhibited a trend of “rising first and then falling,” with the total amount of public procurement for medical imaging devices reaching approximately RMB 119.7 billion, a year-on-year decrease of 17.4%.

The impact of anti-corruption efforts in the pharmaceutical and healthcare sector persisted into 2024. Although the government introduced policies such as medical equipment upgrades, anti-corruption measures had a more direct impact on hospital procurement.。

In 2024, the anti-corruption campaign in the pharmaceutical and healthcare sector continued to deepen. In March, the National Health Commission issued the "Opinions on Strengthening Inter-departmental Law Enforcement Coordination for Medical Supervision." In April, six departments, including the National Healthcare Security Administration, jointly released the "Notice on Launching Special Rectification Campaigns Against Violations and Irregularities Involving Medical Insurance Funds." In May, fourteen ministries and commissions, including the National Health Commission, jointly issued the "Notice on Printing and Distributing the Key Points for Correcting Unhealthy Practices in Pharmaceutical Procurement and Sales and Medical Services in 2024," comprehensively deploying the work to rectify misconduct in the medical field for the year.

Under the joint crackdown by various departments, China’s disciplinary inspection and supervision agencies filed a total of 877,000 cases in key sectors such as finance, energy, pharmaceuticals, and tobacco in 2024. Detention measures were imposed on 38,000 individuals, and 889,000 people received Party disciplinary or administrative sanctions, including 60,000 individuals involved in the pharmaceutical sector.

Affected by the anti-corruption campaign in the pharmaceutical and healthcare sectors, many hospitals have suspended or delayed the procurement of various medical devices. In the first three quarters of 2024, the total value of tender procurements for medical equipment continued to decline sharply,Year-on-year decrease respectively48.35%、27.82%、9%。

A research report by Guosen Securities shows that the total winning bid amount for medical equipment nationwide in the first half of 2024 was only RMB 52 billion, a year-on-year decrease of 35%. Among these, magnetic resonance imaging (MRI), computed tomography (CT), and ultrasound equipment saw a 40% year-on-year decline; endoscopes, patient monitors, and other devices experienced a 50% year-on-year drop.Sales of each category of medical devices have nearly halved.。

Amid the anti-corruption campaign in the pharmaceutical sector, the state has also issued multiple policies to support the allocation of medical equipment.. In March 2024, the State Council issued the Action Plan for Promoting Large-Scale Equipment Renewal and Consumer Goods Trade-In. The Plan points out that by 2027, investment in equipment across sectors including industry, agriculture, construction, transportation, education, culture and tourism, and healthcare will increase by more than 25% compared with 2023 levels. In the healthcare sector, medical institutions are encouraged to accelerate the renewal and upgrading of medical equipment such as medical imaging systems, radiotherapy devices, remote diagnosis and treatment platforms, and surgical robots.

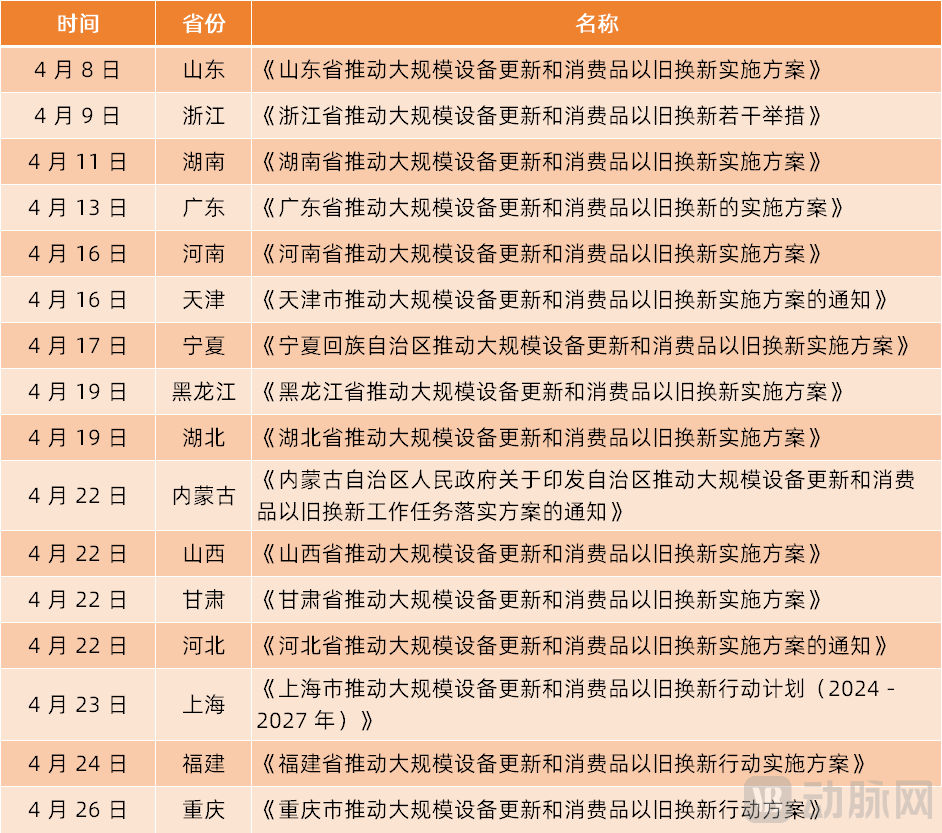

Following the release of this plan, provinces and municipalities across China took swift action. As of June 18, all provinces (including municipalities directly under the Central Government and autonomous regions) had issued their corresponding implementation plans.

(Review of Policy Documents on Large-Scale Equipment Renewal and Consumer Goods Trade-In Programs in Selected Provinces)

In accordance with the implementation plans for equipment renewal and trade-in programs across various provinces, medical equipment such as medical imaging systems, radiotherapy devices, remote diagnosis and treatment systems, and surgical robots will become key areas for upgrading. For instance, Ningxia has planned to increase its investment scale by more than 7% compared to 2023 by the end of the year, promoting the renewal of medical equipment and the renovation and improvement of hospital wards. Hubei Province has planned that by 2027, it will annually renew 300 units/sets of equipment, including CT scanners, MRI machines, digital radiography (DR) systems, color Doppler ultrasound devices, and linear accelerators, while also renovating 10,000 hospital beds.

Constrained by the impact of anti-corruption campaigns in the pharmaceutical sector and the lagged effects of equipment renewal policies (due to procedural factors), the medical device market remained in decline throughout the first three quarters of 2024, leading to the perception that “the medical device industry has entered a winter period.”

In July 2024, the National Development and Reform Commission (NDRC) and the Ministry of Finance issued the “Several Measures on Intensifying Support for Large-Scale Equipment Renewal and Trade-In of Consumer Goods,” allocating approximately RMB 300 billion in ultra-long-term special sovereign bond funds to bolster large-scale equipment renewal and consumer goods trade-in programs. These funds began to be disbursed sequentially around September.

In the fourth quarter, initiatives for medical equipment upgrades and trade-in programs finally began to be implemented gradually.The total value of medical equipment procurement bids this quarter reached RMB 55.5 billion, representing a year-on-year increase of 18.46% and a 56.45% increase from the third quarter.. After two consecutive years of decline, the medical device market finally achieved year-on-year growth for the first time in the fourth quarter of 2024。

Despite a 16% year-on-year decline in the total value of medical equipment procurement bids throughout 2024, the industry remains optimistic that “spring has arrived,” driven by the accelerated implementation of policies supporting equipment upgrades and trade-in programs.。

In 2025, the medical device market accelerated its recovery. According to data from Yizhuang Shusheng, sales of medical imaging equipment in China increased by 78.43% year-on-year in the first quarter.

Although this high-growth figure benefited from the low base in Q1 2024, and sales for that quarter remained below those of Q1 2023, the growth is still commendable: it dispelled the gloom of the market downturn and fired the starting shot for growth in the medical device market.

The medical device market rebounded in the first quarter of 2025, primarily driven by the following factors:

First, bidding and tendering activities have returned to normal, releasing pent-up demand. The anti-corruption campaign in the pharmaceutical sector, which began in 2023, led to the suspension or postponement of bidding projects related to medical equipment. However, as time has passed, bidding and tendering processes across various regions have resumed their normal operations. This has triggered a surge in previously delayed routine procurement bids and new healthcare infrastructure projects, thereby accelerating the bidding and procurement of medical equipment.

Second, the trade-in program for medical equipment and the large-scale implementation of medical equipment renewal and procurement plans across various provinces and municipalities. For instance, Sichuan Province issued a procurement announcement in late December 2024, with a budget of RMB 437 million to purchase 380 units (sets) of CT scanners, DR systems, color Doppler ultrasound devices, and other medical equipment; Hebei Province released an announcement in October 2024, with a budget of RMB 644 million to procure CT scanners, DR systems, color Doppler ultrasound devices, and other equipment...

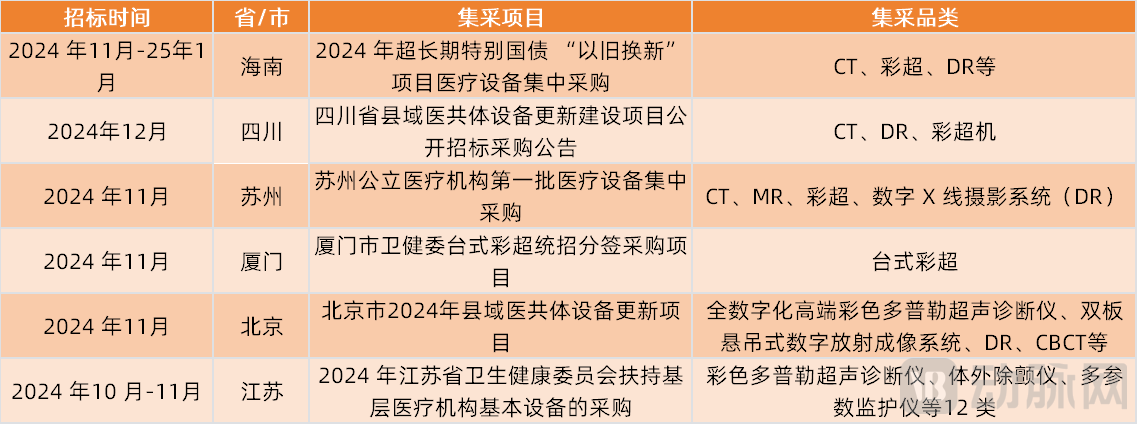

Meanwhile, the state has also promoted the renewal of medical equipment through centralized volume-based procurement, shortening relevant cycles and accelerating implementation. For instance, certain medical equipment renewal projects included in centralized procurement, which commenced in the fourth quarter of 2024, were awarded and implemented in the first quarter of 2025. This has expedited the execution of medical equipment renewal initiatives.

(Partial Centralized Procurement Projects for Medical Equipment Updates Starting in the Fourth Quarter of 2024)

Driven by the aforementioned factors, the medical device market rebounded rapidly in the first quarter of 2025. With the large-scale implementation of projects for upgrading and replacing medical equipment, the market is projected to experience robust growth this year.。

Notably, in this rapidly growing market, county-level regions have become a core battlefield that cannot be overlooked.。

In January 2025, the National Development and Reform Commission stated that it would allocate RMB 10 billion this year to support the development of closely integrated county-level medical communities, enabling county hospitals and township health centers to upgrade medical equipment such as CT scanners, ultrasound systems, and hemodialysis machines.

Previously, in the "Action Plans for Large-Scale Equipment Renewal and Trade-In of Consumer Goods" issued by various provinces, many provinces and municipalities proposed strengthening support for the development of primary healthcare service capabilities and the tiered diagnosis and treatment system, and continuously improving the conditions of primary medical equipment at the county level. For example, Gansu Province's "Action Plan for Large-Scale Equipment Renewal and Trade-In of Consumer Goods" requires that by 2027, the compliance rate for equipment configuration in medical and health institutions below the county level shall reach 100%; Zhejiang Province requires carrying out medical equipment renewal with a focus on the county level, aiming for a 100% compliance rate for equipment configuration in medical and health institutions below the county level by 2027.

In addition, the accelerated tendering and implementation of centralized procurement projects for medical equipment upgrades, with county-level medical consortia as the main entities, have made them a significant segment of the medical equipment market. For example, Sichuan Province released the “County-Level Medical Consortium Equipment Upgrade and Construction Project (Second Round),” planning to procure a total of 73 CT and DR units with a budget of approximately RMB 150 million; Ningxia issued the “Close-Knit County-Level Medical Consortium Equipment Replacement and Upgrade Project,” planning to procure 26 CT and MRI units with a budget of around RMB 120 million. As of now, provinces including Heilongjiang, Henan, Hubei, Hunan, and Hebei have all launched tenders for county-level medical equipment upgrades.

According to VBInsight’s calculations, the first batch of equipment updates is expected to drive medical device procurement totaling RMB 60 billion, of whichCounty-level medical community procurement scale is approximately RMB 18 billion, accounting for about 30%。

Unlike previous procurement methods, current procurement for county-level medical communities is primarily conducted through centralized volume-based bidding. Undoubtedly, this will disrupt the existing market landscape for primary healthcare medical equipment, with each round of centralized procurement reshaping local markets to varying degrees.

For example, in the centralized procurement tender for DR equipment under the county-level medical community in Sichuan Province, Perlove Medical and Angell Technology respectively won the bids for dual-panel ceiling-mounted DR systems (County-Level Configuration I) and dual-panel ceiling-mounted DR systems (Township-Level Configuration I). Meanwhile, the top three companies by market share in other DR equipment segments failed to secure any bids.

In centralized procurement programs, various small and medium-sized enterprises are poised to neutralize the brand advantages of industry leaders and secure bids through competitive low pricing. However, leading medical device manufacturers have also launched mid- to low-end product lines and are actively participating in county-level centralized procurement.

As competition in the medical device market intensifies, medical device products are expected to see continued price reductions under centralized procurement, gradually phasing out laggard companies and product lines.