Ele.me, JD, Meituan, and Douyin Race for the Booming On-Demand Pharmaceutical Retail Market

Recently, the fierce food delivery competition among the three major platforms—Ele.me, JD.com, and Meituan—has drawn nationwide attention. This battle has quickly extended to the pharmaceutical category, with Douyin’s instant retail service also announcing the recent opening of a self-onboarding channel for pharmacies offering one-hour delivery. Instant retail in the pharmaceutical sector is currently gaining significant momentum.

From the pharmaceutical O2O model of the past to today’s on-demand pharmaceutical retail, this business format is not a new phenomenon, butOver the past two years, instant retail in the pharmaceutical sector has indeed demonstrated rapid growth, occupying a pivotal position in the out-of-hospital pharmaceutical retail market.

As major internet platforms vie to strengthen their presence in instant pharmaceutical retail, with increased investment in traffic channels, product supply chains, and innovative marketing strategies, how will the landscape of the out-of-hospital pharmaceutical retail market change?

This round of large-scale food delivery wars has extended to pharmaceutical sales. Beyond preferential policies such as medication purchase subsidies and waived delivery fees, the most significant benefit for instant retail in the pharmaceutical sector lies in greater access to traffic resources.

Previously, the JD Health app had already established a primary entry point for its instant retail service, “Medicine Instant Delivery.” By 2025, as JD.com intensified its efforts in the food delivery sector, the “Instant Food Delivery” tag was prominently displayed on the homepage of the JD app. “24-Hour Medicine Delivery” also appeared in a prominent position on the first screen of the “Instant Food Delivery” channel, thereby granting “Medicine Instant Delivery” access to a significantly larger traffic pool.

Recently, Taobao and Tmall’s instant retail service “Hourly Delivery” was upgraded to “Taobao Flash Sale,” with a “Flash Sale & Food Delivery” tab added to the homepage of the Taobao app. Among the five major categories under “Flash Sale & Food Delivery” is “Medical Consultation and Pharmacy,” providing Ele.me Pharmacy with a prominent entry point.

Furthermore, Meituan recently launched its instant retail brand “Meituan Shangou,” drawing renewed attention to its pharmaceutical retail business.

The strategic allocation of traffic resources has yielded significant results. For instance, the surge in traffic for JD.com’s “Instant Delivery” service has driven a threefold increase in orders for JD Health’s “Instant Medicine Delivery,” with corresponding traffic continuing to grow steadily.

Not only food delivery platforms, but also social media platforms have become embroiled in the competition for the instant retail pharmaceutical market. In April 2025, Douyin Instant Retail announced the opening of a self-registration channel for pharmacies offering one-hour delivery services.

In fact, pharmaceutical O2O is not a new business model. More than a decade ago, various companies began to explore this space. After intense market consolidation, Dingdang Health has emerged as a listed company, and internet healthcare platforms such as Ping An Good Doctor have also entered the pharmaceutical O2O sector. To date, the concept has evolved from “pharmaceutical O2O” to “instant retail for pharmaceuticals,” placing greater emphasis on localized supply chains and fulfillment efficiency.Currently, there are several inevitable factors that have made the instant retail pharmaceutical market a contested arena for major tech companies.

First, instant retail is progressively expanding from high-frequency to low-frequency demand categories, entering a phase of full-category coverage that includes pharmaceuticals.

According to the "Report on the Development of the Instant Retail Industry (2024)" released by the Chinese Academy of International Trade and Economic Cooperation under the Ministry of Commerce, the category structure of instant retail continues to be optimized, gradually entering a stage of full-category coverage. It is rapidly expanding from existing major categories to cover various daily necessities, including digital appliances, maternal and infant products, cosmetics, pharmaceuticals and health care, pet supplies, footwear and apparel, among others.

Compared with other categories, the demand for purchasing medicines is low-frequency and scattered across different time periods. When instant retail achieves sufficient penetration in other categories, it can share the delivery costs of medicine orders and ensure delivery speed. Currently, the delivery efficiency of instant pharmaceutical retail has become highly competitive, with the fastest delivery time reaching just 9 minutes.

Second, under the trend of transformation in physical pharmacies, there is stronger momentum to actively embrace the instant retail business model.

According to data from Zhongkang Pharmacy Connect, the total number of pharmacies in China experienced negative growth in 2024 after years of rapid expansion, with nearly 40,000 stores closing throughout the year. The pharmacy industry is transitioning from the wild-west era of “land-grabbing” expansion into a survival-of-the-fittest elimination round where “the last one standing reigns supreme.”

As public information sources and shopping habits evolve, pharmacies face significant challenges in competing through network expansion and price wars amid homogeneous competition, making transformation urgent. Leveraging instant retail to rapidly reach consumers and enhance service experience has become a key channel for this transformation.

Third, with the development of internet healthcare, online platforms have established end-to-end services covering medical consultation, testing, diagnosis, and pharmaceuticals. When users purchase medications due to urgent needs, they can also access other related healthcare services.Currently, platforms such as JD Health and Meituan Medicine & Health can provide similar closed-loop services.

Furthermore, medical insurance schemes across China have opened online channels for purchasing medications. The integration of medical insurance payment will significantly accelerate the migration of consumers to these digital channels. This surge in traffic represents a key growth opportunity, compelling various platforms to treat on-demand pharmaceutical retail as a critical strategic battleground.

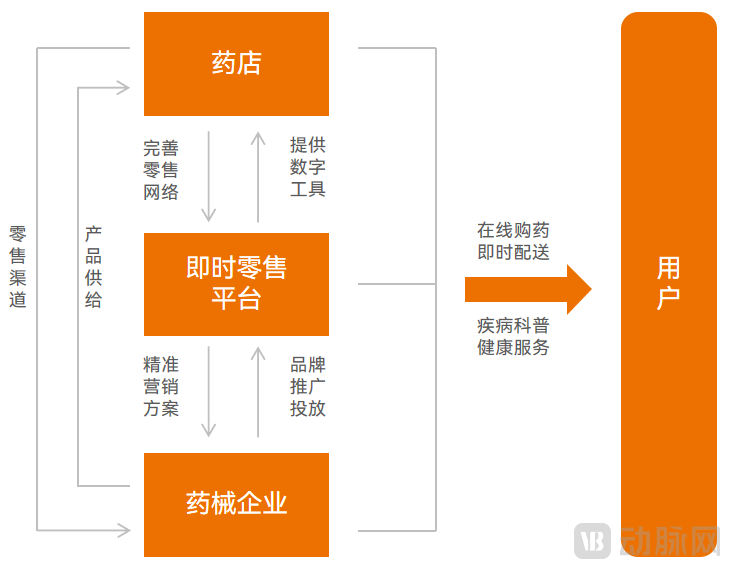

In the early pharmaceutical O2O model, pharmaceutical and medical device companies supplied products to pharmacies, which then listed these products for sale to consumers on pharmaceutical O2O platforms. Deliveries were fulfilled either through the platform’s logistics network or the pharmacies’ own delivery teams, making the overall process a unidirectional flow.In today’s on-demand pharmaceutical retail landscape, the tripartite collaboration among platforms, pharmaceutical and medical device companies, and pharmacies has become more deeply integrated. In particular, pharmaceutical and medical device companies can engage more substantially in this model, leveraging the on-demand retail system to drive brand promotion and boost product sales growth.

Collaboration Models Among Platforms, Pharmaceutical and Medical Device Companies, and Pharmacies as Key Participants in Instant Retail

Enabled by digital technology, precise tripartite collaboration has also become possible, as vividly illustrated by a case study.It is understood that on a certain instant retail platform, the search volume for Brand A of a male medication is significantly higher than that for Brand B, yet the actual sales volume of Brand B surpasses that of Brand A. Data analysis reveals that this discrepancy is primarily due to many pharmacies not listing Brand A’s products online. This insight provides precise guidance for pharmaceutical companies’ brand marketing strategies and pharmacies’ product selection decisions.

The battle for instant pharmaceutical retail among major platforms will inevitably lead to direct competition over resources such as users, pharmacies, and pharmaceutical and medical device companies. However, it is also important to recognize that competition coexists with innovation. Amidst intense rivalry, the industry has explored numerous innovative measures based on tripartite collaboration to more effectively expand growth channels for pharmaceutical and medical device products.

For example, instant retail platforms build brand influence for pharmaceutical and medical device companies through flagship stores.

In recent years, many pharmaceutical and medical device companies have launched B2C flagship stores on e-commerce platforms to sell products directly to consumers. In contrast, in the instant retail scenario, it is pharmacies scattered across various locations that provide products directly to users. What are the characteristics of these users and their purchasing behaviors?

What is the current level of brand awareness? How can brand influence among users be enhanced? In response to these questions, flagship stores for instant retail brands have emerged.

In 2024, at the 2024 Instant E-commerce Future Business Summit held in Shanghai, Ele.me, Taobao, Alipay, and Amap partnered with Kenvue, Haleon, AstraZeneca, and Bayer to launch “One-Hour Delivery” flagship stores for multiple pharmaceutical brands. Taking the Motrin flagship store on Ele.me Medicine as an example, the page intuitively showcases three classic Motrin products—medical fever-reducing patches, ibuprofen suspension, and ibuprofen suspension drops—along with their core features, and also provides links to nearby pharmacies.

JD Health is helping pharmaceutical companies serve their patients and build brand reputation through its “Instant Medicine Delivery” flagship store. The app interface shows that launched flagship stores feature multiple brands across categories such as dermatological medications, cold remedies, and nasal sprays. These flagship stores integrate online branding with offline pharmacy services and include membership management features.

Flagship stores on instant retail platforms provide pharmaceutical and medical device companies with a direct channel to reach consumers and communicate brand value, thereby helping them accumulate brand equity. They also enable companies to better understand user needs and preferences for urgent medication, facilitating further optimization of product offerings and marketing strategies.

Instant retail platforms can also foster collaborative partnerships with pharmaceutical and medical device manufacturers as well as pharmacies, thereby enhancing supply chain efficiency.

For consumers, instant retail is undoubtedly convenient: they can simply open an app, search for products, compare prices and shipping fees, and check delivery speeds before placing an order. Behind this convenience lies a supply chain system that is more complex than the traditional B2C model. In instant retail, a product must be searchable and in stock within the user’s Location-Based Services (LBS) grid to be purchasable, making a more efficient supply chain an imperative.

Integrating more stores and launching a diverse product range on instant retail platforms is a fundamental approach to strengthening local supply chains. According to information released by the “Meituan Pharmaceutical Ecosystem” WeChat official account, as of February 2025, Meituan Medicine and Health had connected with 250,000 pharmacies across China. It has also improved supply chain management efficiency through a tripartite co-construction model and optimized supply chain efficiency via the “Lightning Warehouse” model, which has become a core driver of growth.

JD Health has established an omni-channel supply chain integrating online and offline operations. Its online B2C channels include third-party marketplace merchants and its self-operated pharmacy, while its instant retail channels encompass partner pharmacies and self-operated stores. In 2024, JD Health piloted “Miao Song” (instant delivery) stores in Beijing, covering 80% of the city’s permanent residents. These instant delivery stores are set to expand nationwide, enabling pharmaceutical companies to achieve national coverage in instant retail through collaboration, without the need to build their own extensive sales networks.

Certainly, instant retail platforms can also integrate online and offline resources to build a tripartite collaborative marketing system, thereby creating blockbuster products.

Traditional pharmacy marketing, including discount promotions, free gifts, complimentary health services, and free clinics, has limited reach and growth potential. In contrast, on-demand retail platforms can create integrated marketing models with broader impact by leveraging digital tools to coordinate pharmacies and pharmaceutical companies.

Public information from the “Meituan Medicine Ecosystem” reveals that in 2024, Meituan Medicine and Health launched the HEALTH operational growth model. Among the numerous practical cases driven by this model, Meituan Medicine and Health provided end-to-end empowerment to a pharmaceutical company—covering operational analysis, supply optimization, marketing promotion, and sales conversion. This support helped boost the sales revenue of one of the company’s cough medicine products by 420%, enabling it to break through from lagging behind the overall market growth rate to leading its product category.

Amid the deepening collaboration across the pharmaceutical instant retail supply chain, third-party service providers have emerged.

Pharmaceutical and medical device companies typically incorporate online sales into their new retail channels. As previously mentioned, operating B2C flagship stores has become a standard practice in new retail. However, the distinctive feature of O2O (Online-to-Offline) lies in its span across traditional channels (pharmacies) and new channels (online platforms). In the process of engaging in O2O business, some pharmaceutical companies may encounter disagreements due to unclear responsibility allocation and cross-departmental collaboration challenges, leading to sluggish business progress. Third-party service providers can help resolve these issues.

For example, Meixing Technology leverages its partnerships with major instant retail platforms to provide pharmaceutical companies with modular solutions for instant pharmaceutical retail, including cross-category marketing, tripartite collaboration, new customer acquisition for brands or stores, trend analysis, and single-product breakthroughs.

Overall,Driven by various innovative initiatives, stakeholders in the instant retail pharmaceutical industry have shifted from point-to-point collaboration models to a value network ecosystem centered on sales growth and user service.

It is not only pharmaceutical and medical device companies that can achieve effective growth by leveraging instant retail,Instant retail services offered by brick-and-mortar pharmacies are experiencing increasingly significant growth, becoming a powerful driver for the expansion of online channels and new retail businesses.

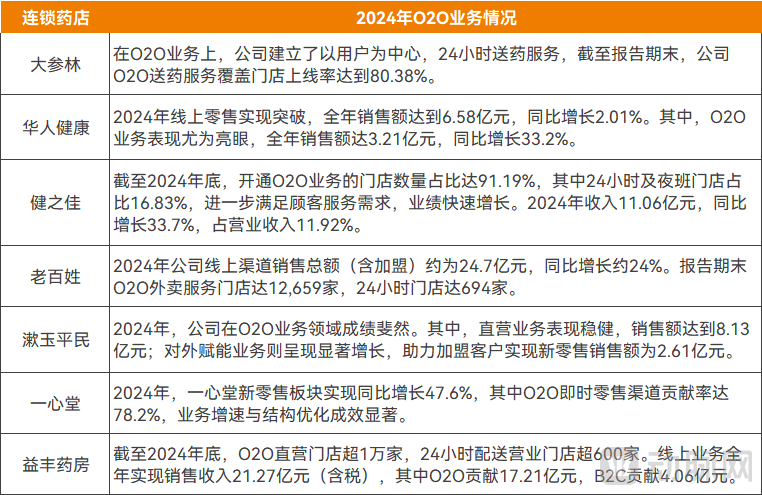

Leveraging its grid-based layout of over 10,000 offline stores nationwide, Yixintang’s new retail business precisely targets consumer needs in “urgent medication” and “privacy-sensitive medication” scenarios, while simultaneously expanding its non-pharmaceutical health product lines through instant retail channels, further strengthening fulfillment capabilities and coverage density in instant retail scenarios. In 2024, revenue from Yixintang’s new retail segment increased by 47.6% year-on-year, with the O2O instant retail channel contributing 78.2% of this growth.

As of the end of 2024, Yifeng Pharmacy operated over 10,000 direct-operated O2O stores, with more than 600 stores offering 24-hour delivery services. Key operational metrics for its new retail business—including picking turnaround time, delivery efficiency, order fulfillment rate, as well as labor productivity, product efficiency, and sales per square meter—have all shown continuous improvement. In 2024, the company’s online business generated RMB 2.127 billion in sales revenue, of which RMB 1.721 billion came from O2O channels, accounting for a significant 80.9%.

Huaren Health’s retail segment achieved a breakthrough in online sales in 2024, with full-year sales reaching RMB 658 million, a year-on-year increase of 2.01%. Notably, its O2O business delivered outstanding performance, with annual sales totaling RMB 321 million, representing a 33.2% year-on-year growth.

Instant retail platforms bring online traffic, digital tools, and business models to pharmacies; after achieving substantial sales growth, chain pharmacies will more actively embrace instant retail. According to forecasts by Menet, if online reimbursement under the national medical insurance scheme is fully liberalized, retail pharmacy...The share of instant retail in the physical pharmacy market will rise to 32.1%.

Revenue from Instant Retail Business of Listed Chain Pharmacy Companies, Source: Company Financial Reports

From the perspective of the platform market landscape, Ele.me, JD.com, and Meituan will continue to compete for the instant retail pharmaceutical market. In contrast, Douyin’s underlying logic differs significantly from that of the three major platforms:There is still room for improvement in delivery resources and speed. However, as Douyin controls a leading short-video platform that serves as a primary gateway for new media marketing, it remains to be seen whether it can build a closed-loop conversion pathway from content-driven product seeding for pharmaceuticals and medical devices to instant retail. Of course, given the stringent regulations governing pharmaceuticals and medical devices, content-led commerce is a double-edged sword; accordingly, Douyin has maintained a gradual opening strategy while implementing various platform rules.In any case, the growth of the instant retail market for pharmaceuticals has become a certain trend, and its impact on users' medication purchasing habits, channels for pharmaceutical and medical device products, and the digital transformation of pharmacies will become increasingly profound.

Due to the concentration of supply and demand and ample delivery resources in large cities, instant retail currently has a higher penetration rate in first- and second-tier cities.As major platforms allocate more resources and further diversify innovative collaboration models with pharmaceutical and medical device manufacturers, pharmacies, and third-party service providers, instant retail in the pharmaceutical sector will penetrate lower-tier markets, becoming a key growth driver for the out-of-hospital pharmaceutical retail market.