Hengrui Medicine Surges 33% in Hong Kong IPO, Valuation Exceeds HK$380 Billion

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Hillhouse

Long-Term Structural Value Investment Institution

Hengrui Pharma’s Hong Kong Stock Exchange Listing Ceremony (Photo provided by the company)

Pharmaceutical “Leader” Hengrui Pharma Ignites Market with HKEX Listing!

Hengrui Pharma raised HK$9.89 billion in its Hong Kong IPO, with an issue price of HK$44.05 and an opening price of HK$57. As of press time, the share price stood at HK$58.6, pushing its market capitalization above HK$380 billion.

Hengrui’s IPO also featured a star-studded lineup of cornerstone investors, with renowned institutions such as the Government of Singapore Investment Corporation (GIC), Invesco, UBS Global Asset Management (UBS-GAM), Hillhouse Capital, and Boyu Capital subscribing to the cornerstone tranche.

Hengrui Pharma’s HKEX Listing Underscores Its Global Ambitions. Hengrui Pharma’s listing on the Hong Kong stock exchange serves as a springboard for its internationalization, aiming to diversify financing channels to secure additional capital while advancing its global strategy.

Hengrui Pharma has long held its position as the leading pharmaceutical company in China, repeatedly achieving transformation and upgrading through forward-looking strategic foresight. The company recognized the importance of internationalization at an early stage, first proposing its internationalization strategy in 2005 and establishing it alongside “technological innovation” as the two foundational pillars of its corporate strategy, a commitment consistently highlighted in its annual reports. However, over the past two decades, Hengrui’s internationalization efforts have yielded results below expectations, particularly in the global expansion of its innovative drugs.

Sun Piaoyang, Chairman of Hengrui Pharma, stated at an industry conference that, based on industry cases, Mindray already derives one-third of its sales revenue from overseas markets, which is a highly significant milestone. For Hengrui, actively pursuing internationalization is an unwavering strategy. However, data from the past three years show that Hengrui’s overseas sales account for less than 5% of its total revenue, indicating that achieving internationalization remains a formidable challenge for the company.

In 2024, Hengrui Pharma achieved operating revenue of RMB 27.985 billion, with overseas revenue of RMB 716 million and net profit attributable to shareholders of the listed company amounting to RMB 6.337 billion.

Hengrui Pharma is dissatisfied with its own international performance. In the current innovative drug industry, internationalization capability has become a core dimension in valuation systems and a key factor in expanding profit expectations.

Driven by Domestic and Overseas Demand, Hengrui Pharma Is Accelerating Its Global Expansion. How Will Hengrui Pharma Speed Up Its Internationalization After Listing on the Hong Kong Stock Exchange?

Hengrui Pharma’s appetite for capital is not particularly strong; its Hong Kong listing is primarily aimed at paving the way for internationalization. Hengrui has stepped up its international investments, driven on one hand by performance pressure resulting from the volume-based procurement of generic drugs, and on the other by the underwhelming domestic commercialization of its innovative drugs. Internationalization has thus become an imperative strategic path.

On the path to the internationalization of innovative drugs, Hengrui Pharma has taken detours. In its early stages, Hengrui’s strategy involved conducting overseas clinical trials independently, a model characterized by long cycles, high costs, and significant uncertainty. In the United States, the cost of Phase I clinical trials for an oncology drug can reach tens of millions of U.S. dollars, with Phase II and Phase III trials incurring even higher expenses.

Conducting clinical trials overseas is not only capital-intensive but also highly uncertain. Hengrui Pharma’s flagship combination therapy, “PD-1 + apatinib,” was submitted to the U.S. Food and Drug Administration (FDA) for marketing approval twice as a first-line treatment for patients with unresectable or metastatic hepatocellular carcinoma. The applications were based on global multicenter Phase III clinical trials, yet both were rejected.

Over the past three years, Hengrui Pharma has begun to adjust its overseas expansion strategy, continuously partnering with major corporations and large funds to promote the international commercialization of its innovative drug pipeline, pursuing a three-pronged approach comprising license-out deals, NewCo formations, and independent global expansion. Currently, business development (BD)-driven overseas expansion, such as license-out transactions and NewCo models, is Hengrui’s primary focus.

Since 2018, Hengrui Pharma has entered into 13 out-licensing transactions with global partners. In the past three years, the company has authorized eight out-licensing deals involving 16 molecular entities, with a total potential transaction value of approximately $14 billion and total upfront payments of approximately $600 million.

The results of international collaborations were immediate, rapidly generating financial returns. In 2024, Hengrui Pharma received upfront payments of €160 million and $100 million, recognizing revenue equivalent to approximately RMB 2 billion, with licensing income becoming the primary driver of Hengrui’s performance growth in 2024.

There is currently no mature path for the internationalization of Chinese pharmaceutical companies. At this stage, Hengrui Pharma has explored a strategy of partnering with collaborators in the early stages of pipeline development to amplify value through clinical development; in the late-stage clinical phase, it partners with multinational corporations (MNCs) to leverage their resources and financial advantages in the United States, thereby realizing greater commercial value for its pipeline.

This model also aligns with the current backdrop of active M&A and restructuring in the overseas pharmaceutical industry, while China’s biopharmaceutical sector is mired in a “winter.”

After receiving the upfront payment for the overseas business development (BD) of innovative drugs, securing subsequent R&D milestone payments and sales royalties tests the product's competitiveness. With the upfront payment received, which pipelines in Hengrui Pharma’s current overseas BD portfolio are poised to generate sustained revenue?

First, weight-loss drugs are expected to be sold to multinational corporations (MNCs) to achieve high returns.Hengrui Pharma has licensed three weight-loss drug pipelines to Kailera Therapeutics through a NewCo structure, acquiring a 19.9% equity stake in the latter. The competitive edge of these three pipelines lies in their distinct mechanisms: HRS-7535 is a novel oral small-molecule GLP-1 receptor agonist with advantages in administration; HRS-9531 is a novel dual GLP-1/GIP receptor agonist administered once weekly; and HRS-4729 is a long-acting injectable peptide that acts as a triple GLP-1/GIP/glucagon (GCG) receptor agonist. Among these three candidates, one product is already undergoing Phase III clinical trials. If all goes well, Kailera’s first drug is expected to reach the market ahead of its competitors.

Kailera has been strategizing its sale to a multinational corporation (MNC) since its inception. Ron Renaud, the CEO hired by Kailera, and Bain Capital, which spearheaded the formation of this NewCo, both have proven track records in facilitating MNC acquisitions of biotech firms. Ron Renaud has successfully sold three biotech companies for a total of $16 billion. If the weight-loss market remains hot, this NewCo is poised to deliver substantial returns for Hengrui Pharma.

A cardiovascular drug is also poised to become a blockbuster product for Hengrui Pharma in overseas markets.In recent years, Hengrui Pharma has increased its R&D investment in therapeutic areas beyond oncology, including autoimmune diseases, cardiovascular and metabolic disorders, and central nervous system (CNS) conditions. In 2025, Hengrui licensed HRS-5346, a lipoprotein(a) [Lp(a)] inhibitor for cardiovascular disease, to Merck & Co. This lipid-lowering drug not only brings Hengrui potential milestone payments totaling $1.77 billion but also targets a substantial market, with the global lipid-lowering drug market exceeding $30 billion.

Global pharmaceutical giants are heavily betting on Lp(a) inhibitors. The most advanced candidate is Novartis’s siRNA drug, which is currently in Phase III clinical trials. Eli Lilly has deployed multiple technological approaches to develop Lp(a)-targeted therapies. AstraZeneca secured the licensing rights for CSPC Pharmaceutical Group’s oral Lp(a) inhibitor, YS2302018, with an upfront payment of $100 million. Hengrui Pharma’s HRS-5346, an investigational oral small-molecule Lp(a) inhibitor, is currently undergoing Phase II clinical trials in China.

Although siRNA drugs demonstrate potent lipid-lowering effects, typically reducing Lp(a) levels by more than 90%, HRS-5346 is an oral small-molecule Lp(a) inhibitor that offers greater advantages in terms of cost and patient adherence. This could enable Hengrui Pharma to prevail in fierce competition and generate sustained returns for the company.

ADC drugs are in the first tier, becoming the vanguard of global expansion.Hengrui Pharma’s two ADC drugs are also poised to generate substantial overseas revenue. Hengrui has licensed its innovative Claudin 18.2-targeting ADC, SHR-A1904, to Merck, and its innovative DLL3-targeting ADC, SHR-4849, to IDEAYA Biosciences.

Claudin 18.2 is highly expressed in a variety of tumors, particularly in gastric cancer/gastroesophageal junction adenocarcinoma (GC/GEJC). China has a large population of gastric cancer patients, with new cases accounting for 37.0% of the global total, making it the primary market for Claudin 18.2-targeted therapies upon their launch.

DLL3 is expressed in a variety of solid tumors, including small cell lung cancer (SCLC), neuroendocrine tumors (NET), non-small cell lung cancer (NSCLC), and melanoma. This asset has the potential to be developed into multiple global pipelines.

Hengrui Pharma is in the first tier of global DLL3 ADC developers.SHR-4849 has initiated Phase I clinical trials in the United States. The payload of SHR-4849 is a topoisomerase inhibitor (TOPOi), which has demonstrated promising efficacy in preliminary single-agent clinical validation for small cell lung cancer (SCLC). The licensor, IDEAYA Biosciences, also places significant emphasis on SHR-4849; its acquisition of Hengrui Pharma’s DLL3 ADC is intended to be used in combination with its synthetic lethal small molecules for the treatment of SCLC. This product is also poised to compete in the global market, generating sustained returns for Hengrui Pharma.

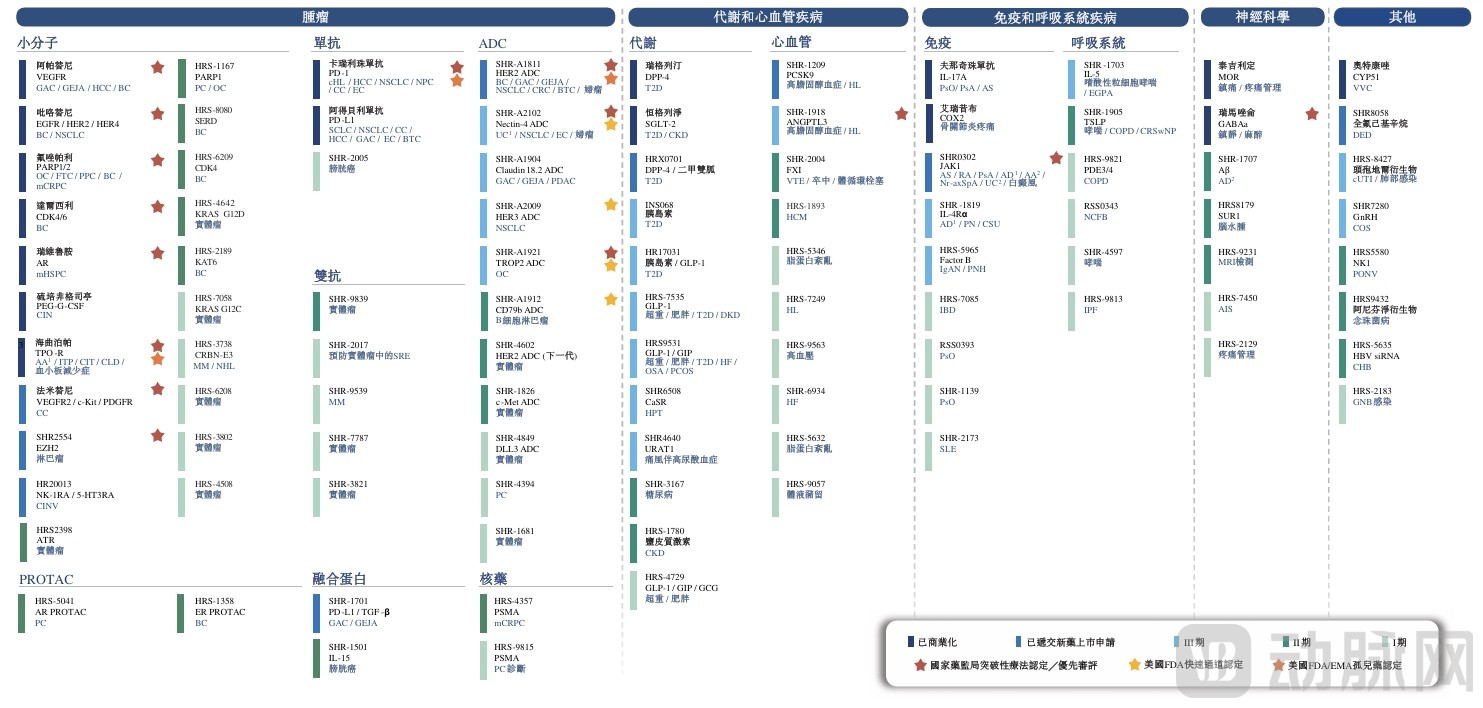

In addition to returns from its licensed pipeline, Hengrui Pharma is likely to continue pursuing business development (BD) opportunities. The company boasts a robust pipeline reserve in currently hot BD sectors, including oncology, autoimmune diseases, and metabolic disorders. After years of investment, Hengrui Pharma has established a substantial innovative drug pipeline. Currently, more than 90 independently developed innovative products are in clinical development, with over 30 innovative drugs in pivotal clinical trials or later stages. For instance, in the field of oncology, Hengrui has built a comprehensive toolkit capable of developing high-quality cancer therapeutics across various novel modalities, basically covering major cancer types worldwide.

Hengrui Pharma’s Marketed New Molecular Entity (NME) Drugs and Candidate NME Drugs in Clinical and Later-Stage Development

As business development (BD) overseas initiatives yield returns, market concerns about this model have also emerged.

Although the business development (BD) overseas model provides domestic biopharmaceutical companies with a fast track to internationalization, enabling them to secure substantial cash flows and avoid the hefty development costs associated with certain clinical stages, it also carries risks such as the loss of core assets, imbalanced revenue-sharing ratios, and ambiguities in intellectual property ownership. Moreover, for Hengrui Pharma, market expectations for its global expansion extend beyond merely acting as a contract developer for foreign pharmaceutical companies.

Relying solely on business development (BD) for overseas expansion may limit Hengrui Pharma’s growth ceiling; in the long run, the company still needs to build its own independent global capabilities.

This Hong Kong stock listing serves as Hengrui Pharma’s preparation for building its independent global expansion capabilities. The listing will enhance the company’s corporate image and international visibility, attract more international talent, accelerate the development of its overseas teams, and strengthen its integration with overseas capital markets.

Following its listing on the Hong Kong stock exchange, Hengrui Pharma will allocate the proceeds to build new production and R&D facilities in both the Chinese and overseas markets. The company currently has more than 20 ongoing overseas clinical trials. In the long run, these assets are expected to generate overseas revenue for Hengrui in the future.

As its portfolio of innovative products expands, Hengrui Pharma plans to increase its production capacity in China and upgrade existing manufacturing facilities to ensure they meet or exceed applicable GMP standards, including EU GMP, US cGMP, and ICH quality guidelines. Meanwhile, the company intends to establish production bases in key global markets to strengthen its manufacturing capabilities. By setting up overseas production facilities, Hengrui aims to further optimize its supply chain and reduce costs associated with clinical trials, regulatory approval, and commercialization in relevant markets.

The current BD strategy is also laying the foundation for long-term independent global expansion. By leveraging BD partnerships to enter overseas markets, companies can reduce the financial burden of internationalization, enhance global brand visibility, gain worldwide recognition for their innovative technology platforms, and accumulate experience in global clinical development and commercialization.

“Built to Last” mentions that visionary companies have core purposes that remain unchanged and specific goals and strategies that adapt to the times. This aligns perfectly with the business philosophy of Sun Piaoyang, who has steered Hengrui Pharma for many years. Sun Piaoyang once firmly stated, “I have always adhered to a single principle in running my business: keeping pace with the times!”

Internationalization remains Hengrui Pharma’s unwavering core objective, while business development (BD) for global expansion serves as a responsive, adaptive goal. Leveraging its Hong Kong stock exchange listing, Hengrui—imbued with a gene for keeping pace with the times—is embarking on the next phase of its strategic layout.

In 2025, the first fully domestically developed ECMO (Extracorporeal Membrane Oxygenation) system, independently created by Hengrui Medical, a subsidiary of Hengrui Pharma, officially received market approval from the National Medical Products Administration. High-end medical devices represent one of Hengrui’s strategic focus areas. Hengrui Medical has made in-depth investments in high-value consumables such as oncology intervention, peripheral intervention, and neurointervention. It is researching and developing medical equipment for life support, imaging support, and interventional support, while proactively entering frontier fields such as drug delivery devices, continuously expanding its product pipeline and building market advantages.

With Hengrui Pharma’s official listing on the Hong Kong Stock Exchange on May 23, this leading Chinese innovator in pharmaceuticals has taken a pivotal step in its internationalization strategy. Leveraging the Hong Kong stock platform, Hengrui has not only secured strong endorsement from international capital but will also accelerate the implementation of its dual-engine strategy of “innovation + globalization.” From successful business development (BD) transactions to breakthroughs in high-end medical devices such as ECMO, Hengrui is building comprehensive competitiveness across the entire industry chain, spanning both pharmaceuticals and medical devices.

References:

Peak Dialogue! Returning from Retirement, Breaking the Rat Race, and Going Global: Lü Mingfang Asks Sun Piaoyang All the Questions Pharma Professionals Want to Know... — E-Drug Manager

The Full Story of Hengrui’s “Variations” in Internationalization — E-Drug Capital Circle

This Pharma Company Is Betting Big on a Chinese Ozempic Rival——Forbes