Hinge Health IPO Surges Nearly 20% on Debut as $2.8B MSK Digital Health Leader Validates Digital Therapeutics

Hinge Health

Provider of Digital Treatment Solutions for Chronic Diseases

Sword Health

Digital Remote Physical Therapy Service Provider

Omada Health

Digital Health Management Platform

RecoveryOne

Rehabilitation Service Platform Provider

DarioHealth

Digital Therapeutics Platform Operator

Kaia Health

Digital Therapeutics Developer

May 22,Digital Therapeutics Company Hinge Health Lists on the New York Stock Exchange, offering 13.7 million shares in its initial public offering at $32 per share. The stock opened at $39.25, reached an intraday high of over $40, and closed the day at $37.56. Of the shares offered, approximately 8.5 million were sold by Hinge Health (with an additional approximately 5.1 million shares sold by existing shareholders), raising up to $273 million.

Hinge Health Rings NYSE Opening Bell on Listing Day (Screenshot from NYSE Official Website)

Rewinding to last May, Waystar set a new record for the largest IPO in the digital health sector since 2022, while Tempus AI, which went public shortly thereafter, briefly emerged as a leading high-volatility “meme stock.” However, since then, no other prominent digital health companies have listed on the U.S. stock market, and the industry’s recovery has failed to materialize as expected.

Hinge Health’s IPO breaks the nearly year-long drought of digital health listings on U.S. stock exchanges and holds promise as a self-validating milestone for digital therapeutics.Since the “three musketeers” of digital therapeutics—Pear Therapeutics, Better Therapeutics, and Akili Interactive—all exited the market following the digital health boom of 2021–2022, the prospects for digital therapeutics have been widely questioned. Hinge Health’s public listing demonstrates that digital therapeutics still hold significant value.

VCBeat Analyzes Hinge Health’s IPO Prospectus for Industry Reference

Hinge Health’s origins date back to January 2012, when co-founders Daniel Perez and Gabriel Mecklenburg jointly established Marblar in the United Kingdom, the predecessor of Hinge Health. In 2014, Marblar launched a digital rehabilitation program for knee and back pain, shifting its business focus to musculoskeletal (MSK) health issues.

At that time, both founders experienced severe musculoskeletal (MSK) issues and gained a deep understanding of the pain points in MSK rehabilitation during their 12-month recovery journey. They believed that emerging digital technologies could significantly enhance the quality, efficiency, personalization, and convenience of MSK rehabilitation, thereby greatly improving the patient experience.

In December 2014, this new model achieved its first milestone (the first MSK patient of Marblar experienced significant relief from knee osteoarthritis pain and reported an excellent user experience), subsequently demonstrating substantial potential.

Following the initial success of the new model, the two co-founders established Hinge Health in the United States in March 2016 and injected all equity and business operations of the original company into Hinge Health through a share exchange. Since then, a rising star has gradually emerged in the musculoskeletal (MSK) rehabilitation sector.

Starting in 2016, Hinge Health gradually became a favorite in the capital markets. In addition to its initial round of financing completed in 2014,Hinge Health’s other nine funding rounds began in 2016, with cumulative fundraising exceeding $800 million.。

Especially inIn 2021, Hinge Health completed two consecutive funding rounds within a single year, raising $300 million and $400 million, respectively. This propelled its valuation to a peak of $6.2 billion, cementing its position as the undisputed leader in the digital therapeutics sector for musculoskeletal (MSK) conditions.。

It is no surprise that Hinge Health has garnered such favor; musculoskeletal (MSK) conditions, which encompass more than 150 disorders affecting the human locomotor system, have long been a leading cause of disability worldwide and constitute the largest global disease burden. According to an analysis of the World Health Organization’s Global Burden of Disease data,Approximately 1.71 billion people worldwide suffer from musculoskeletal (MSK) disorders, and due to the rapidly accelerating trend of population aging.

Among these conditions, low back pain affects approximately 568 million people worldwide, making it the leading cause of disability in 160 countries and regions. The number of individuals affected by other conditions also exceeds 100 million, including fractures (436 million), osteoarthritis (343 million), other injuries (305 million), neck pain (222 million), and amputations (175 million).

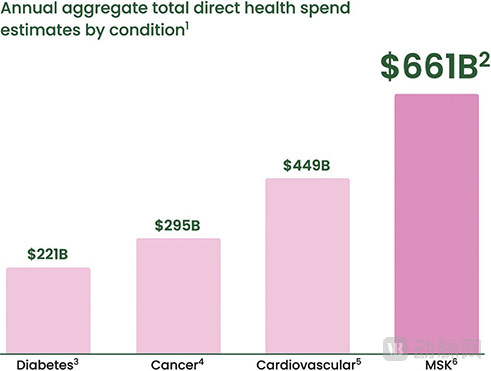

Direct medical costs attributable to MSK conditions in the U.S. exceed those of other diseases (screenshot from the prospectus)

The resulting healthcare costs are also quite exorbitant, as exemplified by the United States.Direct medical costs attributable to musculoskeletal (MSK) conditions reached $661 billion, surpassing those for cardiovascular disease, cancer, and diabetes, making MSK disorders the most costly health condition in terms of U.S. healthcare expenditures., accounting for over 10% of total U.S. healthcare expenditures.

Furthermore, Hinge Health stated in its prospectus that MSK health issues also generated an additional $624 billion in indirect costs, such as losses in worker productivity, bringing the total MSK burden in the United States to nearly $1.3 trillion.

For this very reason, MSK has consistently remained a key focus of capital investment in Europe and the United States. According to statistics,Since 2010, the U.S. market alone has invested as much as $38 billion in the musculoskeletal (MSK) sector.. This momentum has shown no signs of abating, even during the capital winter of recent years.

After securing ample funding, Hinge Health began to rapidly expand its business scope. In 2019, less than three years after entering the U.S. market, Hinge Health achieved a breakthrough by partnering with major national health plans.

As of the end of 2024, Hinge Health had more than 50 partners.

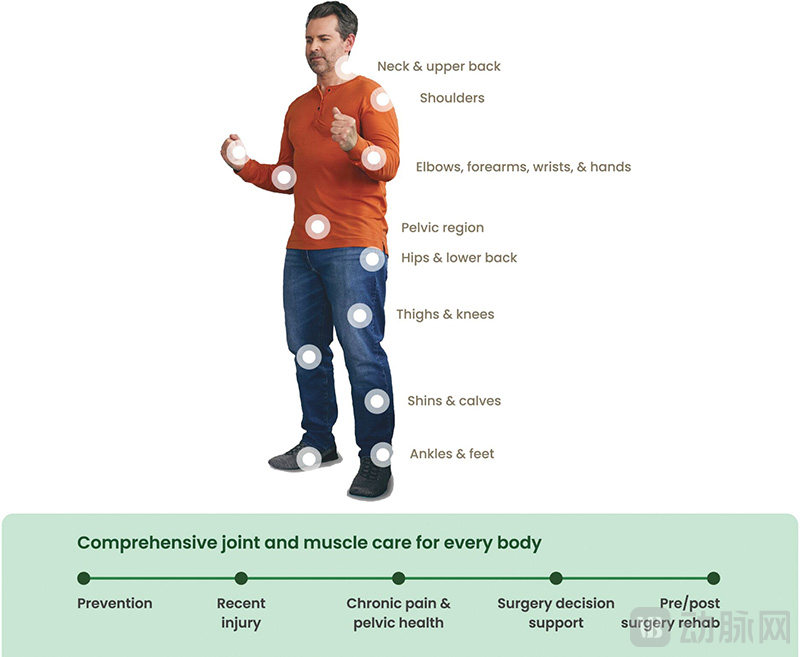

Hinge Health Covers MSK Health Issues Across 16 Body Regions

Meanwhile, Hinge Health’s focus on musculoskeletal (MSK) health has gradually expanded beyond its initial emphasis on knee and back pain. By the end of 2024, Hinge Health had covered MSK conditions affecting 16 anatomical regions, including the neck, upper back, shoulders, elbows, forearms, wrists, hands, lower back, hips, pelvic region, thighs, knees, shins, calves, ankles, and feet.

In addition to Hinge Health, prominent brands such as Sword Health, DarioHealth, Omada Health, Kaia Health, and RecoveryOne have also emerged in this field. Through their collective efforts, digital musculoskeletal (MSK) rehabilitation has gradually become an unstoppable trend.

Notably, Hinge Health places great emphasis on research and development, continuously upgrading its technology platform. Its two major acquisitions have focused on enhancing and expanding the technology platform, rather than mere business expansion.

Initially, Hinge Health’s digital therapeutics solution included accompanying wearable sensors and tablets. The wearable sensors provided real-time feedback and tracking during home-based rehabilitation, ensuring that patients’ exercise movements met standardized criteria and thereby guaranteeing the effectiveness of the rehabilitation training.

This type ofThe integration of wearable sensors has also been emulated by many subsequent entrants, becoming a hallmark of MSK digital therapeutics.。

However, this proprietary hardware approach entails high costs and relatively limited flexibility. Meanwhile, wearable sensors have also proven less than ideal for rehabilitation exercises involving small ranges of motion, such as those targeting the head, wrists, and hands. With continuous advancements in artificial intelligence and smartphone camera capabilities, Hinge Health has decided to adopt an alternative approach to address this challenge.

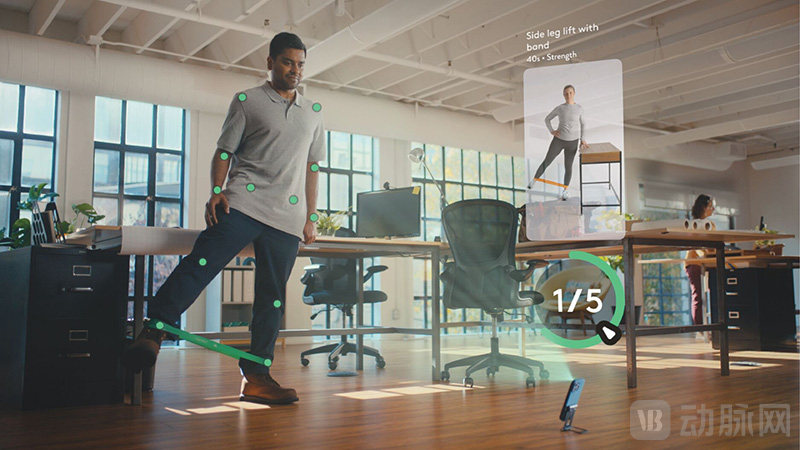

In September 2021, Hinge Health acquired wrnch. The company’s 3D motion tracking technology enables full-body movement tracking comparable to that used in the sports and film industries. Building on wrnch’s existing technological foundation, Hinge Health subsequently developed TrueMotion technology.

TrueMotion can utilize the camera on a patient’s smartphone or tablet to perform 3D human motion capture of rehabilitation exercises, and provide comparative feedback on over 100 anatomical reference points via artificial intelligence, thereby guiding patients through complex therapeutic exercises.

TrueMotion uses smartphone cameras to perform 3D motion tracking of rehabilitation exercises

In mid-2023, Hinge Health began piloting TrueMotion, officially launching it in January 2024 and discontinuing the legacy wearable sensor-based solution for new users.In November 2024, Hinge Health announced it would cease updating software for its legacy products and fully transition to TrueMotion technology, which is hardware-free.。

Hardware-free TrueMotion technology reduces costs, enhances the recognition of subtle movements, and improves the convenience and accessibility of Hinge Health services.. The prospectus explicitly stated that the migration of the technology platform played a key role in cost reduction, with the ratio of selling expenses to revenue dropping significantly from 33.7% in 2023 to 23.2% in 2024, while the gross profit margin increased from 66.3% in the previous year to 76.8%.

Furthermore, TrueMotion’s capability to track over 100 body points provides enhanced data collection capabilities compared to its predecessor. This data is collected and used to further train artificial intelligence, thereby enabling the generation of more optimized rehabilitation plans.

Hinge Health’s application of artificial intelligence extends beyond this. As early as 2021, the company developed HingeConnect, a platform capable of integrating personal health information. Through an analysis of historical data, Hinge Health found that approximately 85% of musculoskeletal (MSK) healthcare costs were actually incurred by around 23% of high-risk patients. The integration of AI enables HingeConnect to identify these high-risk patients at the earliest stage and optimize benefit plans accordingly.

Furthermore, Hinge Health has kept pace with the generative AI trend by introducing its Care Team Assistant, a generative AI tool, in July 2024. This tool automates routine tasks such as message generation, data integration, and profile review. According to the prospectus, after implementing this tool, the care team’s expenses for daily operations like message generation decreased by approximately 32% within one quarter compared to previous levels.

In addition to leveraging artificial intelligence, Hinge Health is also introducing more MSK treatment modalities to enhance its services, andAcquired the medical device brand Enso, known for relieving MSK conditions with non-invasive electrical stimulation, in March 2021.。

The use of electrical stimulation to alleviate musculoskeletal (MSK) symptoms has a long history; however, traditional non-invasive devices deliver only low-frequency electrical stimulation, offering limited pain relief. Although high-frequency electrical stimulation can provide more immediate and sustained pain relief, it typically requires surgical implantation of the stimulation device.

Enso’s high-frequency neuromodulation technology has achieved a technological breakthrough by delivering high-frequency pulses in a non-invasive manner. Attached to the skin surface over the painful area via adhesive pads, the device can alleviate pain within seconds without the risk of drug addiction. Clinical trials have demonstrated that this device reduces pain by 56% and provides clinically effective relief for 86% of patients who do not require medication or surgery.

The acquisition of Enso has made Hinge Health the only musculoskeletal (MSK) digital health platform that owns such a solution in-house, widening its lead over other MSK digital health companies. Meanwhile, it continues to optimize its offerings—by late 2024, it launched the next-generation Enso Model 3, with costs reduced by approximately 75% compared to the initial Model 1.

The application of these digital technologies has significantly enhanced the efficiency of musculoskeletal (MSK) treatment, holding substantial significance for addressing MSK health-related issues. In its prospectus, Hinge Health also noted that, taking TrueMotion technology as an example, it can reduce the time required for rehabilitation therapy by care teams by approximately 95%.

For clients, implementing digital MSK rehabilitation solutions also delivers a strong return on investment.Hinge Health’s 2023 Employer Reimbursement Study shows that customers achieve an approximate return on investment (ROI) of 2.4x, calculated by dividing the average cost savings of $2,387 per member over 12 months by the cost of participating in the health plan.。

In terms of its business model, Hinge Health primarily sells one-year service subscriptions to employers, representing a typical B2B2C model. On the sales front, there are two approaches: clients can either subscribe directly through Hinge Health’s direct sales team or access services through health plans that partner with Hinge Health.

Under the latter model, clients can retain their existing contracts with partnered health plans and pay only for participating employees, thereby significantly streamlining cumbersome processes such as contract execution, procurement, security reviews, onboarding, and billing.

Under this model, customers receive services more rapidly. The prospectus indicates that most contracts sold by partners are implemented within 40 to 100 days. In 2023, the vast majority of Hinge Health’s contracts were distributed through partners. By the end of 2024, 79% of its revenue was derived from partner-led distribution.

For this very reason, partnerships with large health plans are critical for Hinge Health. As previously mentioned,As of the end of 2024, Hinge Health had partnered with more than 50 health plans, including the top five national health plans and the top three pharmacy benefit management (PBM) programs by market share. Its top three partners were all large national health plans, accounting for over 40% of its revenue.。

Self-insured employers (large enterprises, state and local governments, and labor unions) have historically been Hinge Health’s primary customer base. In recent years, it has also been expanding into commercial insurance, Medicare, and Medicaid markets. By the end of 2024, Hinge Health had signed contracts with more than 2,250 clients, among whichIncluding 49% of Fortune 100 companies and 42% of Fortune 500 companies, with over 530,000 signed members.。

Compared with the situation at the end of 2023 (1,657 clients and over 370,000 members),Hinge Health saw a 36.1% increase in its customer base and a 43.7% growth in its member count over the past year., with impressive growth rates. Given that its business model ties revenue strongly to customer and member counts, this expansion has also driven revenue growth. Nevertheless, the prospectus notes that its current achievements capture less than 5% of the potential market, underscoring the vast market opportunity for musculoskeletal (MSK) health issues.

However, Hinge Health’s partnerships are typically structured as three-year, non-exclusive agreements (although Hinge Health is the sole digital MSK provider in the vast majority of these health plans), and partners may terminate the contract at any time upon notice. In extreme scenarios, these risks may warrant attention.

The good news is that Hinge Health’s services have been well received to date.As of the end of 2024, Hinge Health has retained all partners since its inception (except those acquired), with a 12-month customer retention rate as high as 98% and a net dollar retention rate reaching 117%.(Revenue comparison for the same customer cohort during comparable periods, thereby reflecting business renewal, expansion, contraction, and churn), with a Net Promoter Score (NPS) of 87 (out of 100), indicating extremely high customer satisfaction.

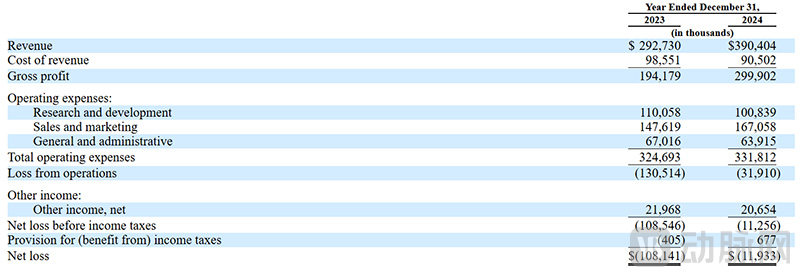

Hinge Health Financial Statements

Hinge Health achieved approximately $390 million (RMB 2.8 billion) in revenue in 2024, a year-on-year increase of 33.4% from 2023; gross profit reached $299 million, surging by 54.4% year on year.. After deducting operating expenses, which remained largely flat compared to 2023, Hinge Health reported a net loss of nearly $12 million in 2024, bringing it close to profitability.

In 2023, its net loss still amounted to $108 million, indicating significant progress.

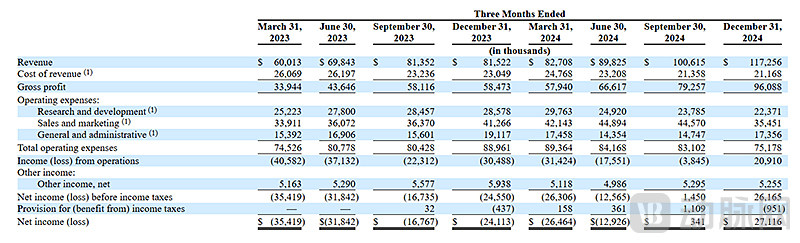

Hinge Health Financial Statements for the Last Eight Quarters

Based on the quarterly financial reports from the past eight quarters, Hinge Health’s revenue has demonstrated a relatively stable growth trend. Revenue in the second half of the year is significantly higher than in the first half, which aligns with the disclosure in its prospectus that the second half is typically the peak period for concentrated customer contract signings.

Interestingly, Hinge Health significantly reduced its various expenses in the fourth quarter of 2024, a move that appears deliberately designed to present more attractive pre-IPO financial statements. More importantly, however, was its steadily growing revenue, which enabled the company to achieve a net profit of $27 million for the quarter.

The prospectus shows that Hinge Health still has $45 million in cash on hand, and with the $273 million raised from this IPO, Hinge Health will have sufficient funds to support its business expansion plans in the future. According to the prospectus, Hinge Health will further expand its customer and member base by tapping into more fully insured health plans and public insurance programs such as Medicare. It will also provide additional services to existing customers, including fall prevention for the elderly and women’s pelvic health. In addition, Hinge Health plans to intensify its efforts in international expansion.

Hinge Health’s IPO not only marks the resurgence of digital health initial public offerings on the U.S. stock market over the past year, but also underscores the significant growth potential of MSK (musculoskeletal) conditions. A review of its prospectus reveals that Hinge Health’s digital therapeutics have demonstrated strong market performance and hold considerable market promise. This development offers valuable insights for China’s digital therapeutics industry as well. In fact,MSK Digital Therapeutics Has Gradually Become an Important Branch of Domestic Digital Therapeutics in Recent Years。

Of course, the MSK rehabilitation industry in China is still in its early stages, with a significant gap remaining compared to the market maturity seen in the United States. Meanwhile, it remains considerably challenging for domestic players to replicate Hinge Health’s B2B2C model at this stage.

However, with rising economic standards and growing health awareness, sports and fitness are rapidly gaining popularity in China. According to projections by the General Administration of Sport of China, the number of people regularly engaging in physical exercise is expected to exceed 630 million by 2035, with a significant increase in professionalism compared to the past. The incidence rate of sports injuries among the exercising population is approximately 10%–20%, meaning that around 100 million people will require rehabilitative treatment for sports injuries in the future.

In this field, China lags significantly behind the global advanced level; however, from another perspective, the market potential is substantial. Therefore,Although still in its infancy, sports rehabilitation is widely regarded as a promising sector poised to become the next major frontier alongside medical aesthetics and dentistry.。

This could become the catalyst for the rise of MSK digital therapeutics in China.

Whether we can carve out a commercialization path for MSK digital therapeutics that is uniquely our own remains to be seen.