Global Oncology R&D Trends at AACR 2025: Target Landscape, Institutional Strategies, and AI Integration

Author: Zhang HongyuPh.D. Candidate in Biological and Pharmaceutical Engineering, Zhejiang University

As precision medicine and technological innovation continue to evolve, oncology drug development is undergoing profound restructuring. The global research landscape has become increasingly clear, ranging from target focus and disease area distribution to institutional participation models and technological pathways. Particularly following the pooled analysis of studies presented at the 2025 AACR Annual Meeting, core trends have gradually emerged: traditional targets remain dominant, emerging targets are achieving accelerated breakthroughs, institutional roles are becoming more specialized, and AI technology is comprehensively permeating drug discovery and diagnostic/therapeutic prediction processes.

This industry research is based on the complete abstract data released at AACR 2025, systematically reviewing three key dimensions of global oncology R&D: (1) hotspots in disease and target research, (2) institutional types and technological trends, and (3) the integrated application of AI in oncology research. By categorizing and analyzing over 7,100 articles presented at AACR 2025, this report aims to help readers quickly grasp the core focal points of global oncology R&D, the differentiated strategic layouts across regions and institutions, the translational pathways for emerging targets, and the practical scenarios enabled by AI technologies.

Part I: Global Hotspots in Oncology Research

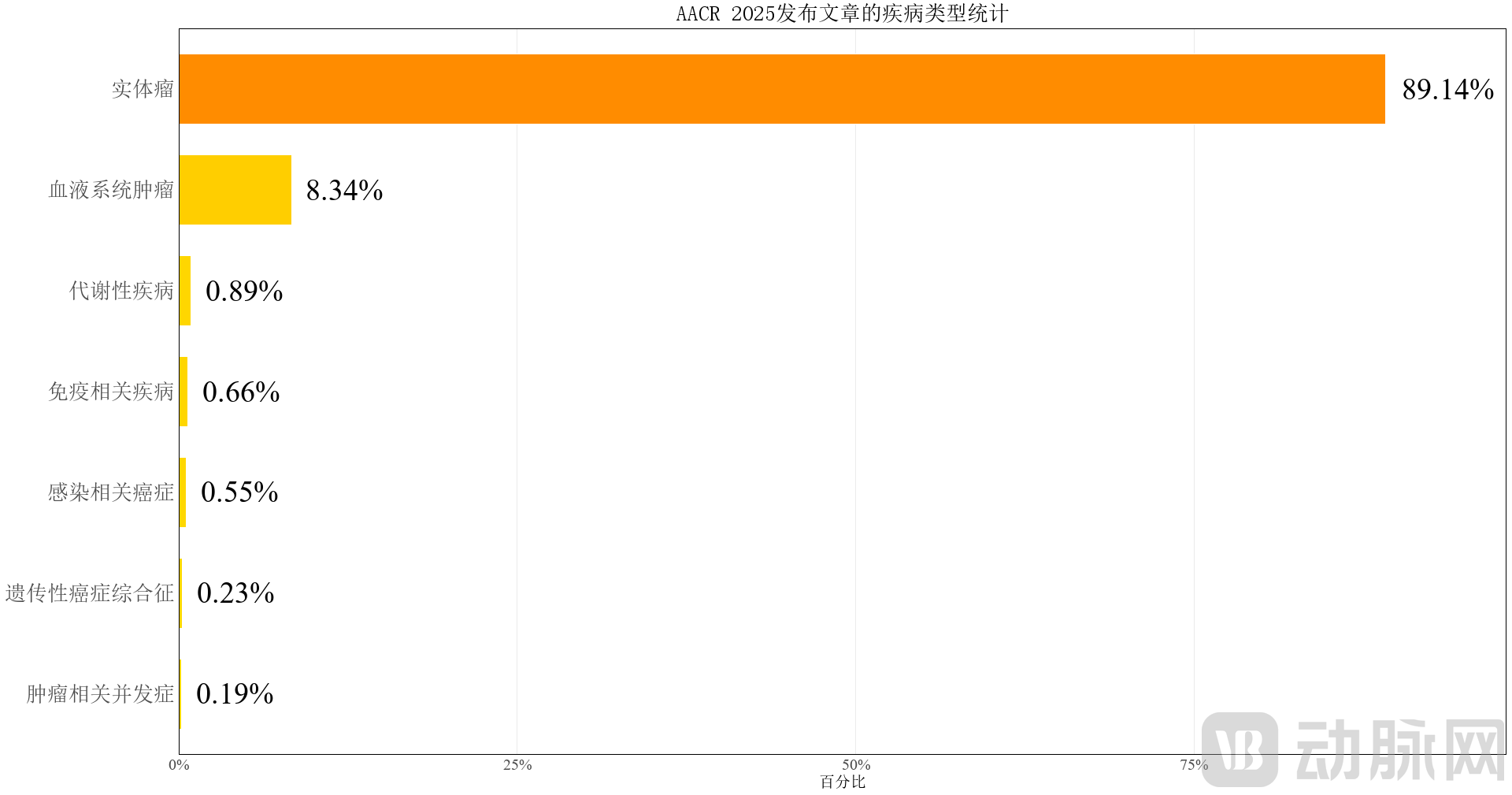

1.1 Solid tumors are the primary focus of research, followed by hematologic malignancies

According to the research statistics released at the AACR 2025 Annual Meeting, solid tumors accounted for as high as 89.14% of studies, far exceeding hematologic malignancies (8.34%) and other disease categories (such as metabolic diseases at 0.89% and immune-mediated diseases at 0.66%).[1]. This research landscape aligns with the global cancer burden. The GLOBOCAN 2020 report indicates that solid tumors, such as lung cancer, breast cancer, and colorectal cancer, account for more than 60% of new cancer cases.[2], solid tumors remain the core focus of current anti-tumor drug development and basic research.

Source: Compiled from data by PharmCube based on information from the AACR 2025 conference website.

1.2 Alignment Between the Distribution of Research Focus in Systemic Oncology and Clinical Burden

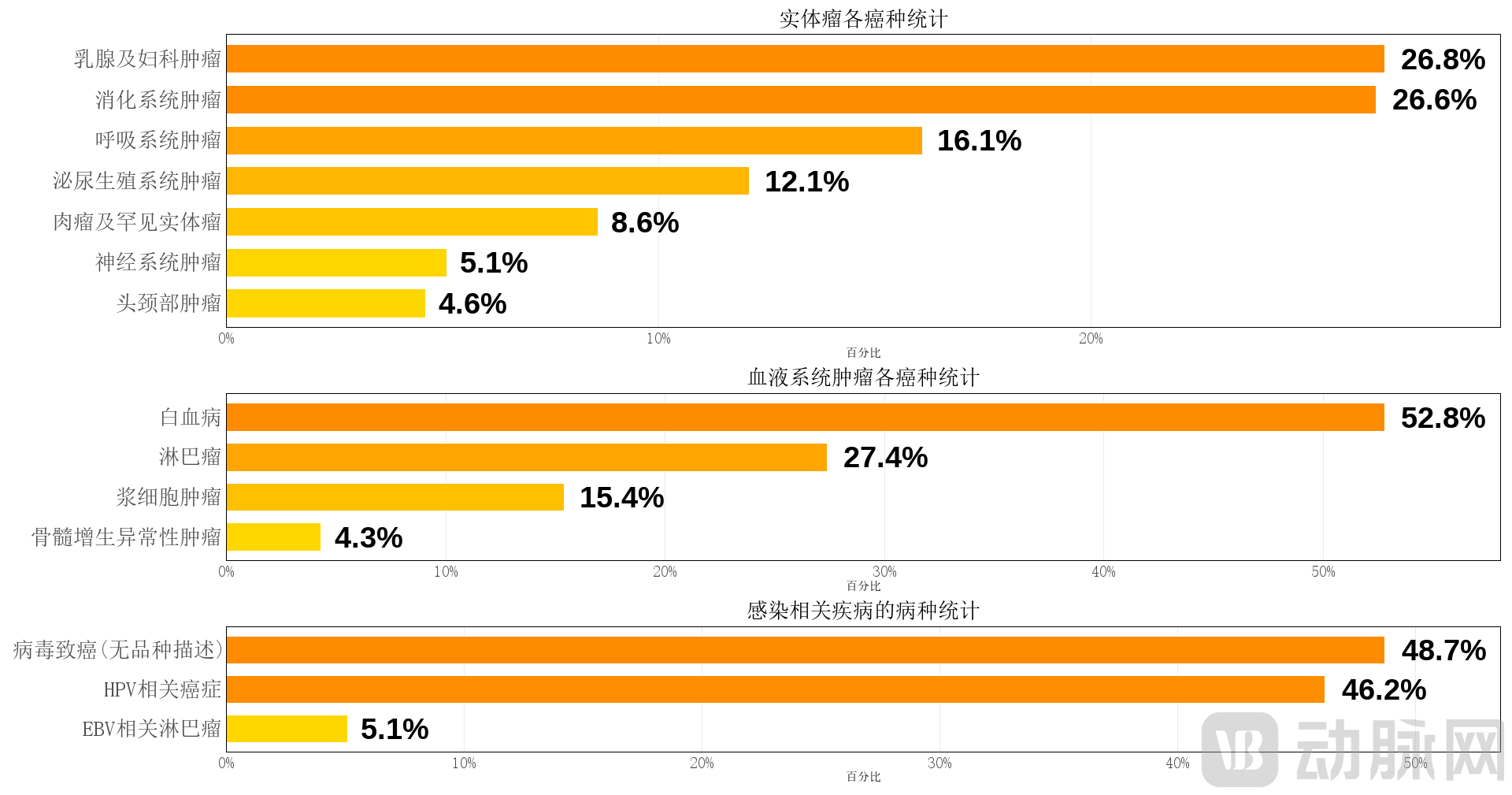

Further classification of solid tumors revealed that breast and gynecological tumors (26.7%) and digestive system tumors (26.7%) were the most extensively studied, followed by respiratory system tumors (16.1%) and urogenital system tumors (12.1%).[1]This aligns broadly with the global ranking of high-incidence cancers, where breast cancer is the most common malignancy in women (accounting for 11.7%), followed by colorectal cancer and lung cancer.[2]。

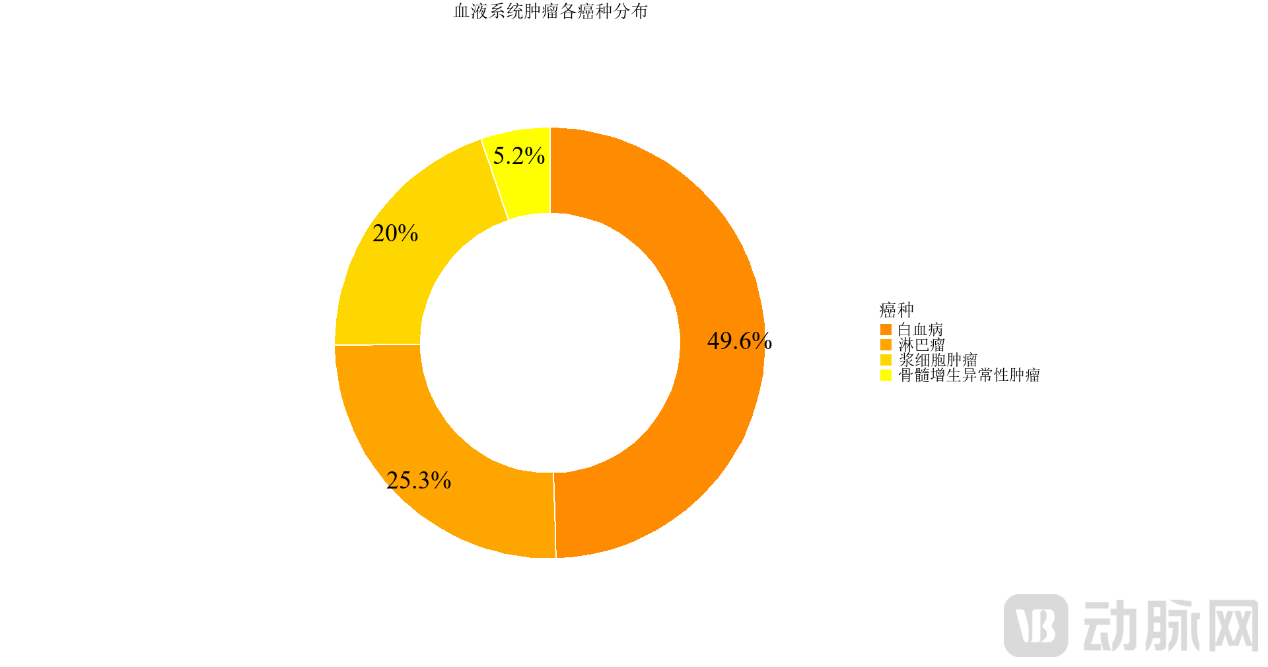

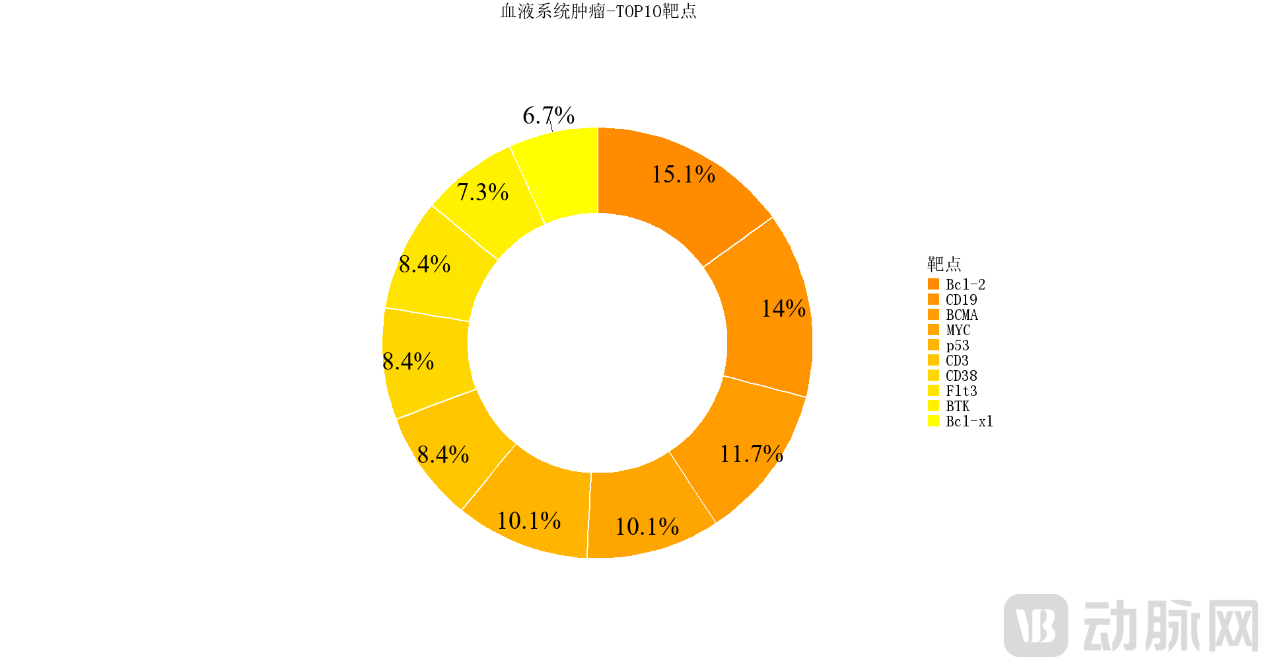

Among hematologic malignancies, leukemia research accounts for 52.8%, significantly outpacing lymphoma (27.4%) and plasma cell neoplasms (15.4%). In recent years, breakthroughs in targeted strategies such as CAR-T, BiTEs, and Bcl-2 inhibitors have driven the rapid evolution of leukemia treatments, resulting in a dual-track advancement of cellular therapies and targeted drugs.

In the field of infection-related diseases, research on the carcinogenic mechanisms of HPV dominates (46.2%), far exceeding that on EBV (5.1%). In recent years, the research focus has shifted from prophylactic HPV vaccines to the development of therapeutic vaccines and combination immunotherapies, which have demonstrated potential in the treatment of tumors such as cervical cancer and head and neck cancer.

Source: Compiled by PharmCube based on information from the AACR 2025 conference website

In metabolic diseases, research has focused on tumor susceptibility in the context of type I/II diabetes (36.4%) and obesity (30.3%), while other conditions such as hypercholesterolemia (15.2%) and insulin resistance (6.1%) account for a relatively smaller proportion of studies. Epidemiological studies have confirmed that obesity and type II diabetes significantly increase the risk of developing pancreatic cancer and colorectal cancer.[3], suggesting that metabolic imbalance is a significant background factor in tumorigenesis and provides new directions for early screening and intervention.

In research on immune-related diseases, autoimmune diseases (41.3%) and inflammatory bowel disease (IBD, 23.9%) have received the most attention. Patients with IBD have more than twice the risk of colorectal cancer compared to the general population.[4], the role of chronic inflammation in remodeling the tumor microenvironment has become a research hotspot. Such studies help further elucidate the association between immune regulation and tumorigenesis. In research on hereditary cancer syndromes, Lynch syndrome (64.3%) is the primary focus, with its early screening and risk management for colorectal and endometrial cancers already incorporated into clinical guidelines. Research on hereditary tumors emphasizes early intervention and personalized prevention and control strategies for high-risk populations. Studies on tumor-related complications focus predominantly on treatment-related toxicities (71.4%), such as cytotoxicity and immune-related adverse events, which are far more prevalent than radiation-induced fibrosis (28.6%). With advancements in therapeutic technologies, complication management has increasingly become an indispensable component in optimizing clinical protocols.

Source: Compiled by PharmCube based on information from the AACR 2025 Annual Meeting website

Source: Compiled by PharmCube based on information from the AACR 2025 Annual Meeting website

1.3 A Clear Trend Toward Refined Research on Cancer Subtypes

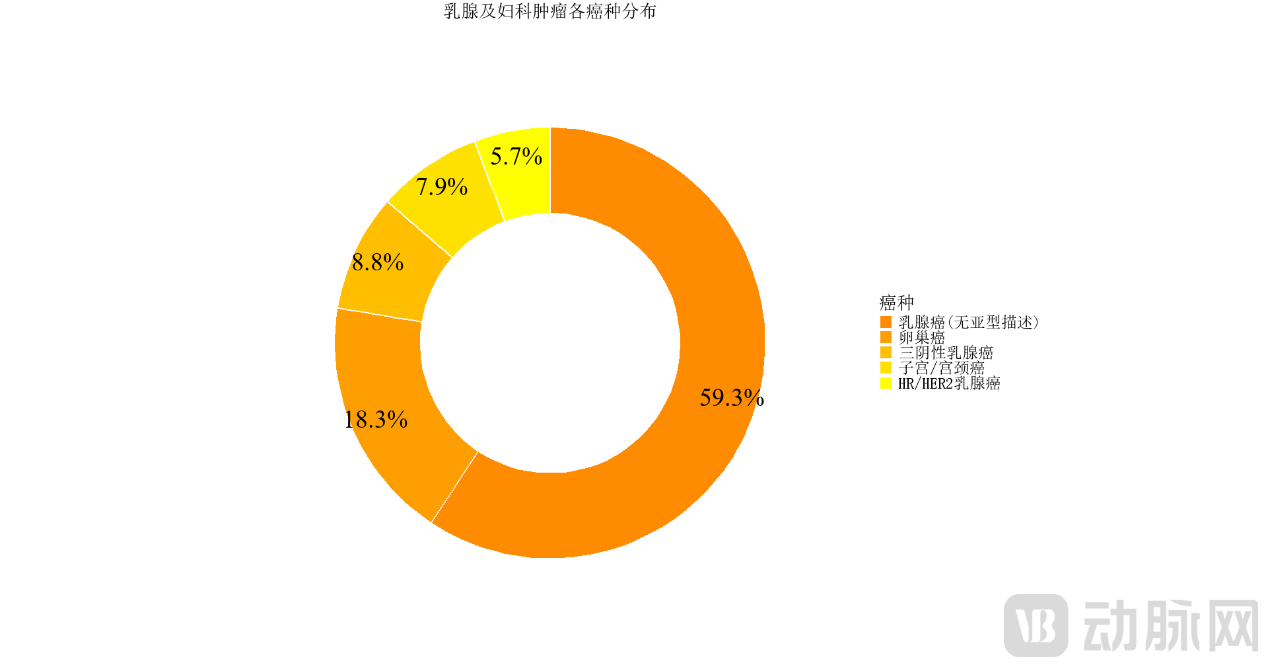

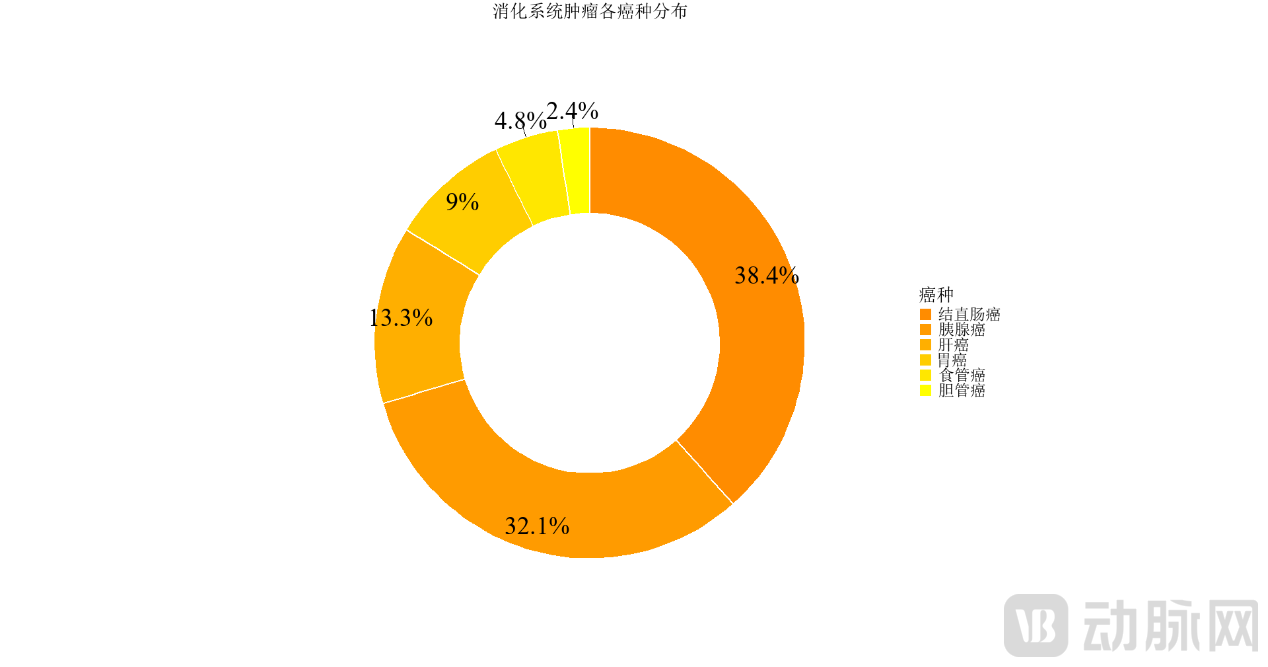

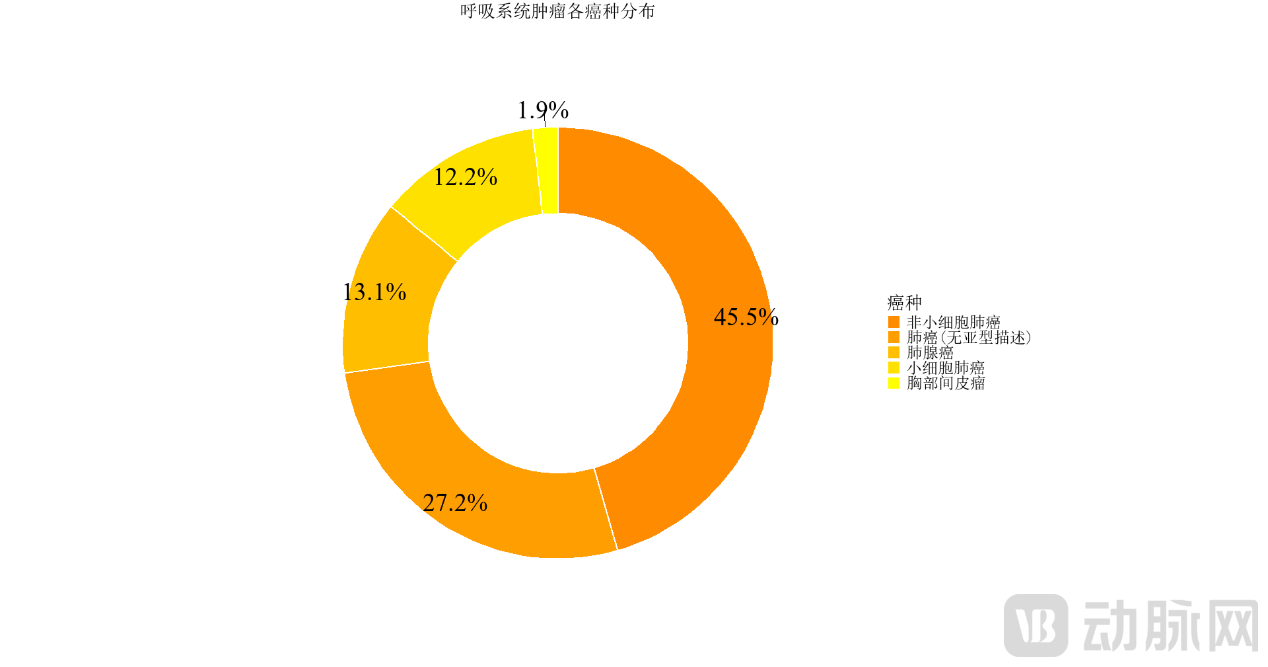

In breast and gynecologic oncology, breast cancer research accounts for 59.3%, representing the primary area of focus, followed by ovarian cancer (18.3%) and triple-negative breast cancer (TNBC, 8.8%). Due to the absence of hormonal receptors and HER2 targets, TNBC is currently seeing active exploration of T cell–directed therapies and antibody–drug conjugate (ADC) strategies.[5]Research on breast cancer subtypes is progressively advancing from molecular classification toward precision targeted therapy combined with immunotherapy. In digestive system tumors, colorectal cancer (38.4%) and pancreatic cancer (32.1%) are the primary focuses of research. Pancreatic cancer, with a five-year survival rate below 10%, is widely regarded as a key challenge in the fight against "refractory solid tumors." Research interest in liver cancer (13.3%) and gastric cancer (9%) is also steadily increasing. In respiratory system tumors, non-small cell lung cancer (NSCLC, 45.5%), lung adenocarcinoma (13.1%), and small cell lung cancer (SCLC, 12.2%) are the main subjects of study, with classic targets such as EGFR mutations and ALK fusions continuing to attract significant attention.

Source: Compiled by PharmaCube based on information from the AACR 2025 Annual Meeting website

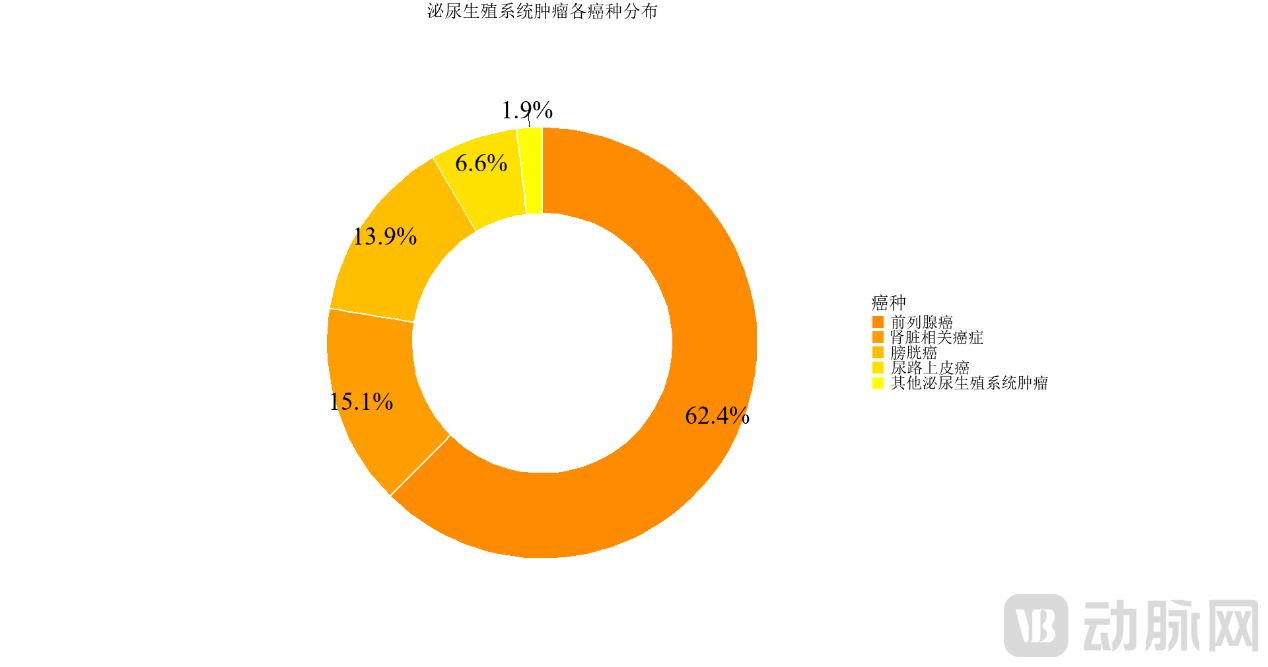

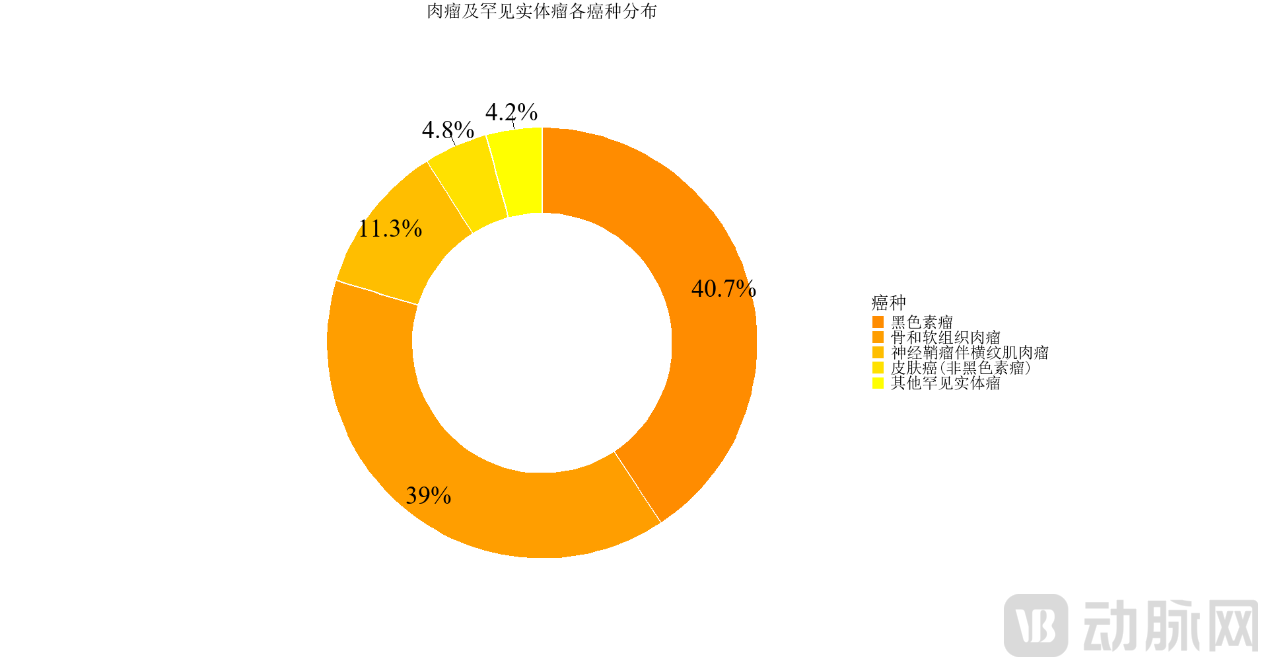

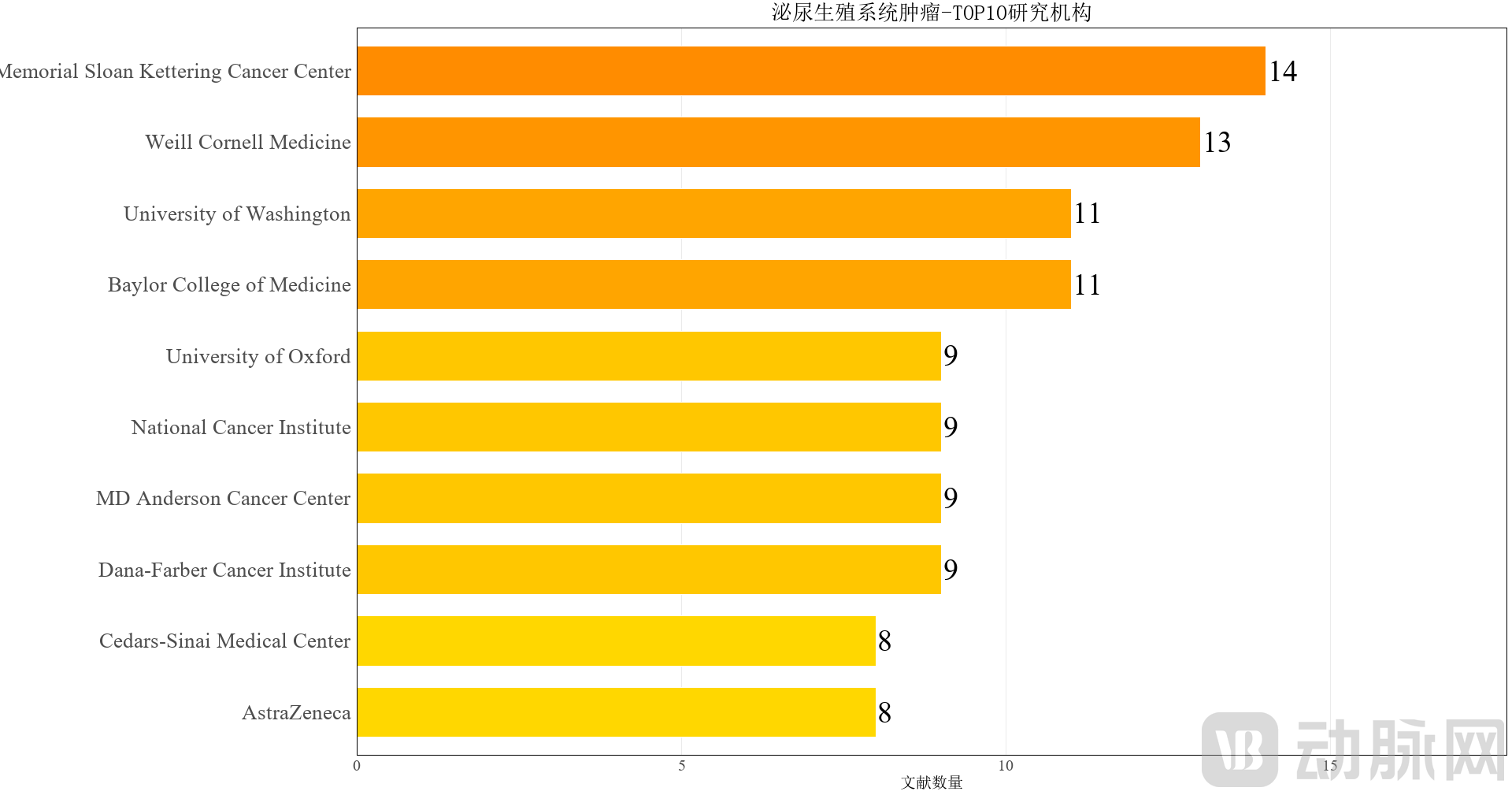

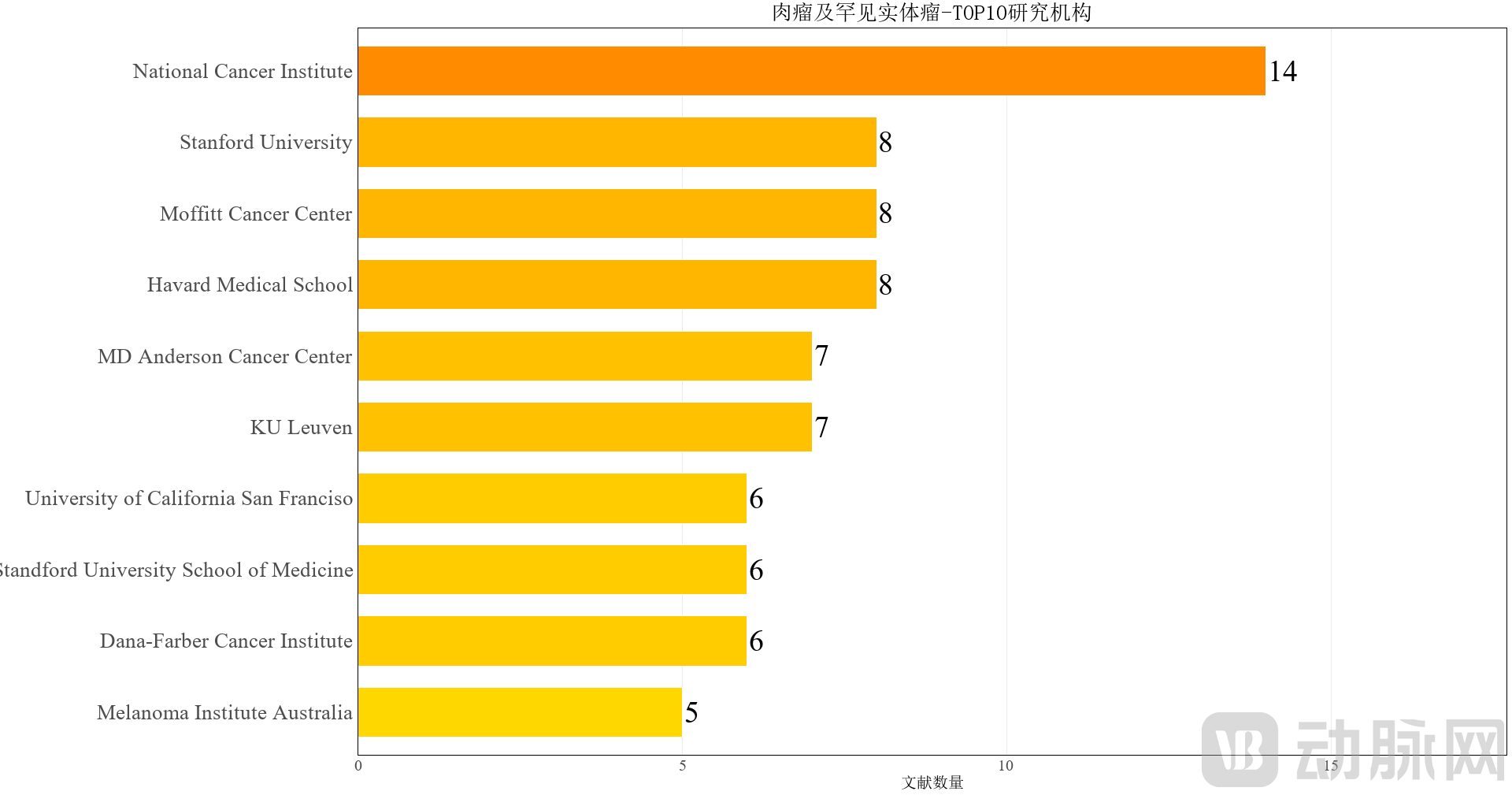

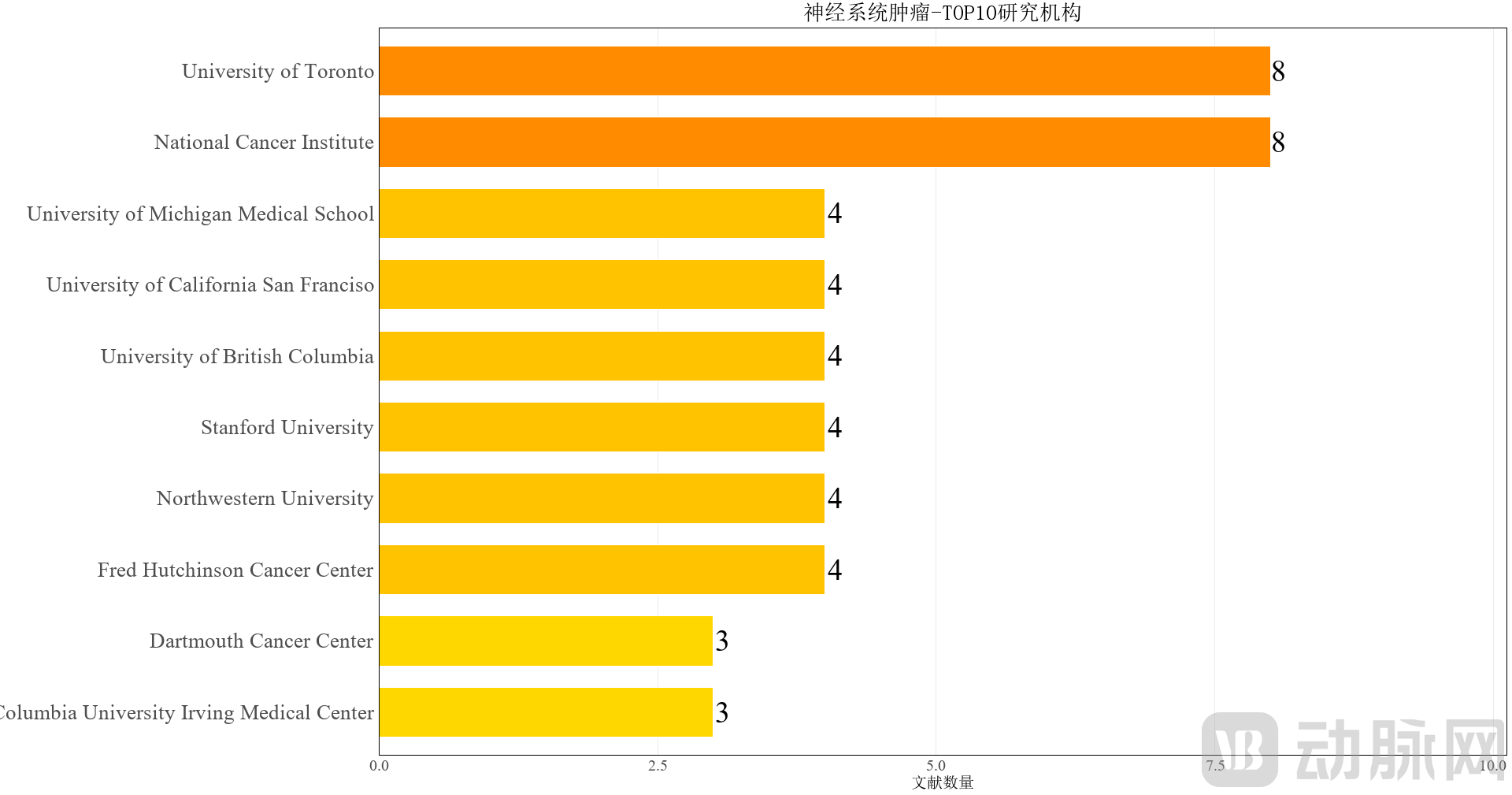

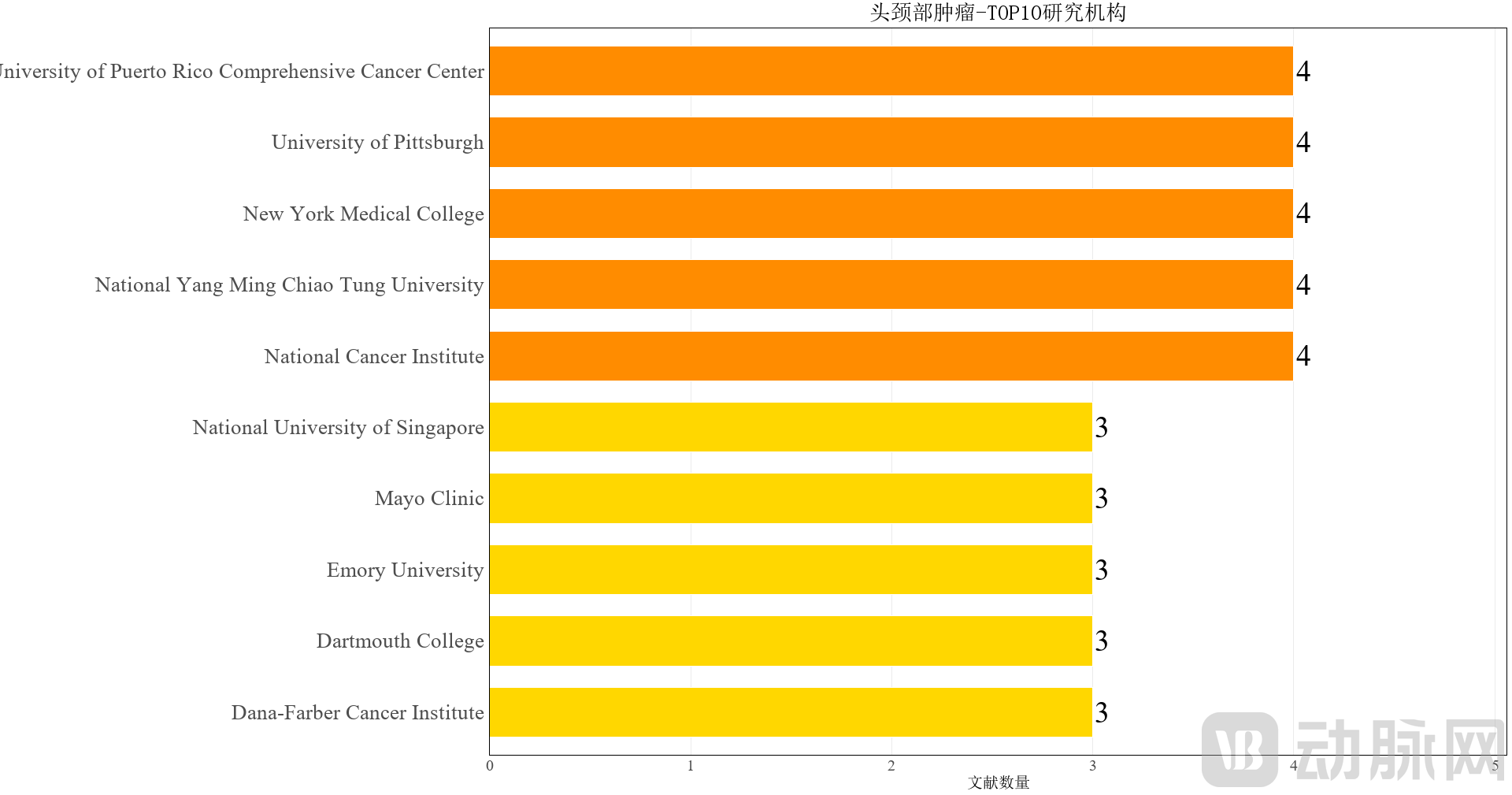

Among genitourinary tumors, prostate cancer accounts for the largest proportion of research (62.4%), followed by renal cancer (15.1%) and bladder cancer (13.9%). Achievements related to PSMA-targeted radioligand therapy and AR helicase inhibitors have been granted FDA Priority Review designation.[6], the dual-targeting strategy against AR and PSMA has become a focal point in prostate cancer treatment. Furthermore, research on sarcomas, nervous system tumors, and head and neck cancers is each focused on rare targets, specific molecular alterations, and immune-related mechanisms. Hematologic malignancies remain dominated by leukemia (49.6%) and lymphoma (25.3%), with increasing attention being paid to rare subtypes, thereby driving further diversification and precision in therapeutic approaches and biomarkers.

Source: Compiled by PharmaCube based on information from the AACR 2025 Annual Meeting website

1.4 Top 10 Targets Research: Concurrent Advancement of “Broad-Spectrum Core + System-Specific” Approaches

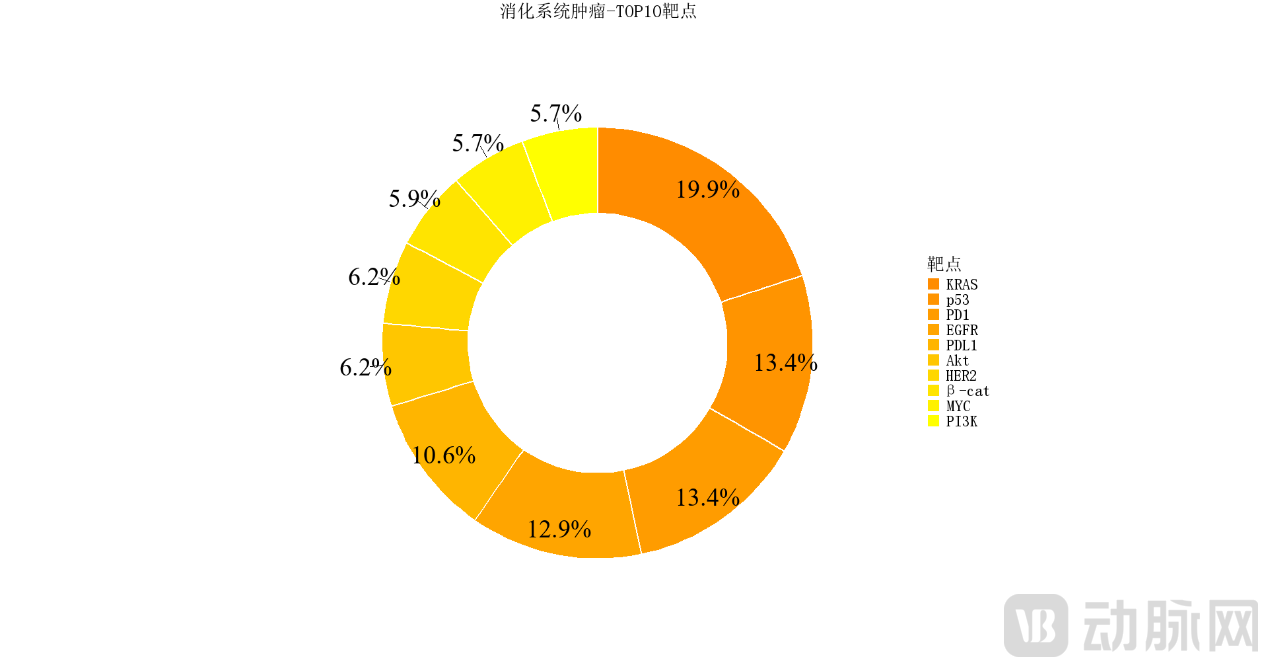

Therapeutic targets in digestive system tumors encompass traditional driver genes (KRAS, EGFR, TP53), immune pathways (PD-1/PD-L1), and key signaling pathways (PI3K/AKT, β-catenin), reflecting a developmental trend toward the combination of targeted therapy, immunotherapy, and signaling pathway inhibition. KRAS is a core driver gene in pancreatic ductal adenocarcinoma and colorectal cancer. The combination of the KRAS G12C inhibitor sotorasib with panitumumab has received FDA approval for the treatment of metastatic colorectal cancer harboring KRAS G12C mutations.[7]. TP53 is the most frequently mutated tumor suppressor gene, with a significantly elevated mutation rate in digestive system tumors.[8]. PD-1/PD-L1 inhibitors have been proven effective as first-line therapy for MSI-H/dMMR colorectal cancer; in the KEYNOTE-177 trial, pembrolizumab improved survival and tolerability.[9]。

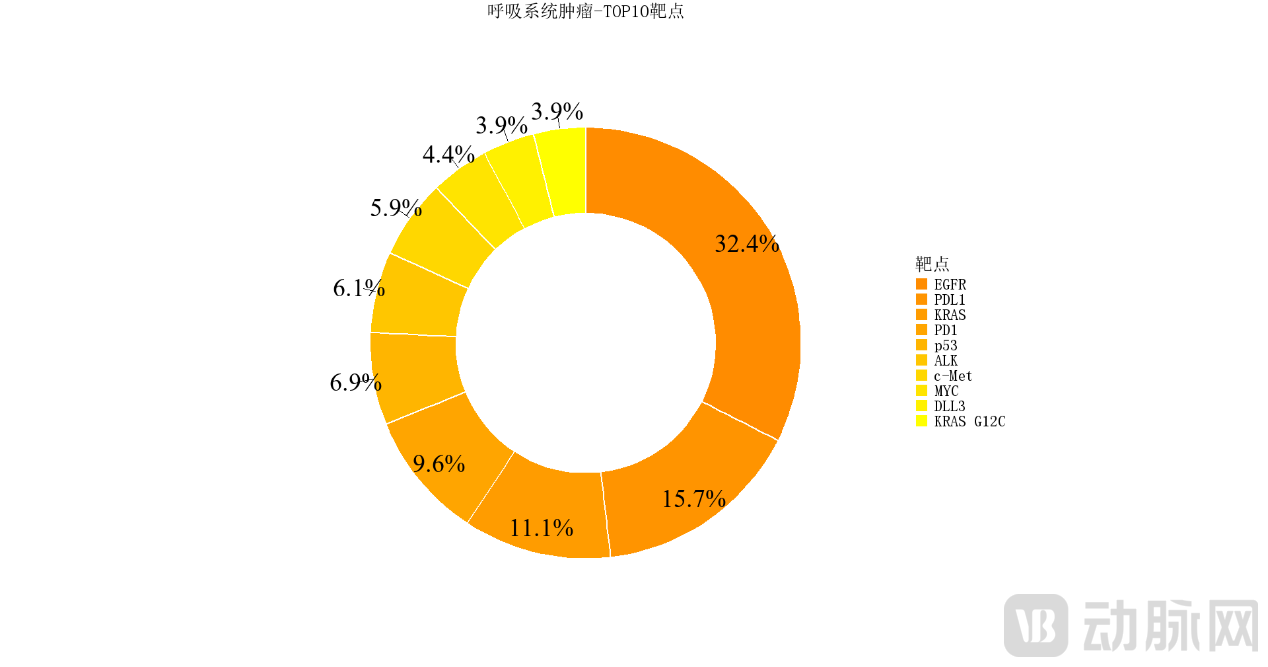

Lung cancer treatment continues to focus on traditional targets such as EGFR and KRAS, while also incorporating immunotherapeutic strategies and novel targets like DLL3. The approval of third-generation EGFR TKIs (e.g., lazertinib) in combination with the antibody amivantamab has ushered in the era of “TKI + antibody” therapy.[10]. KRAS G12C inhibitors were the first to gain approval for NSCLC, with indications expanding to other subtypes. DLL3 is a specific target in small cell lung cancer, and bispecific antibodies and CAR-T therapies are demonstrating potential in early-stage clinical trials.

Source: Compiled from data by PharmCube based on information from the AACR 2025 Annual Meeting website.

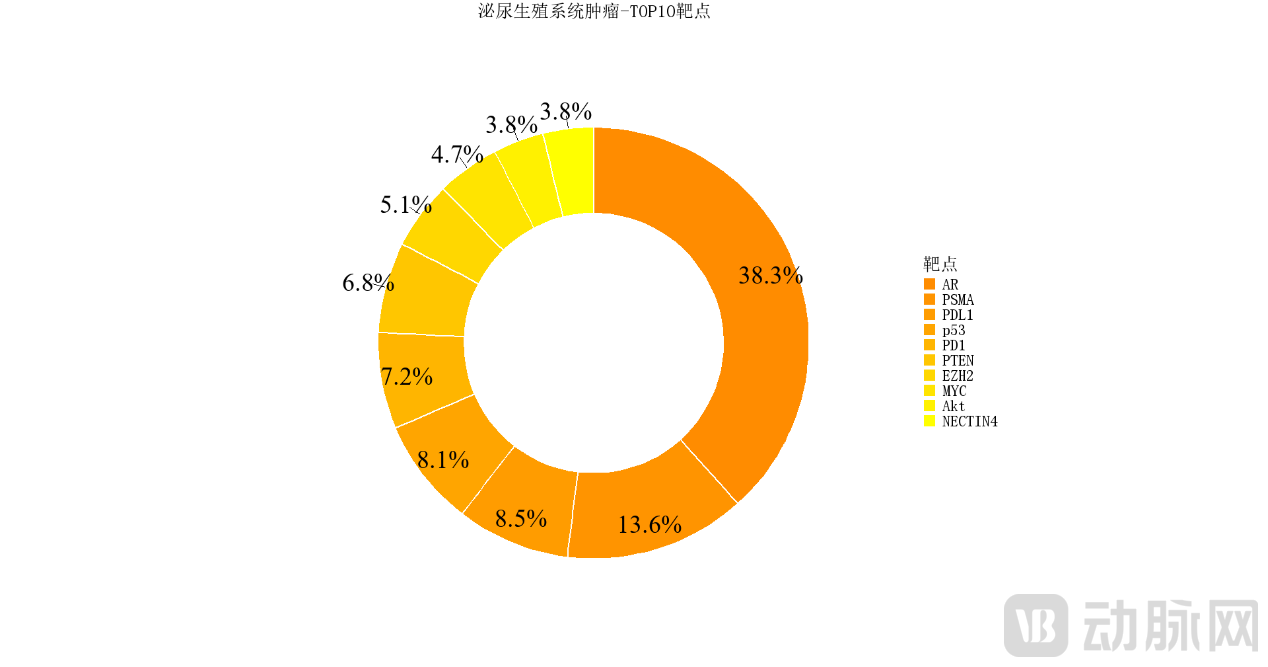

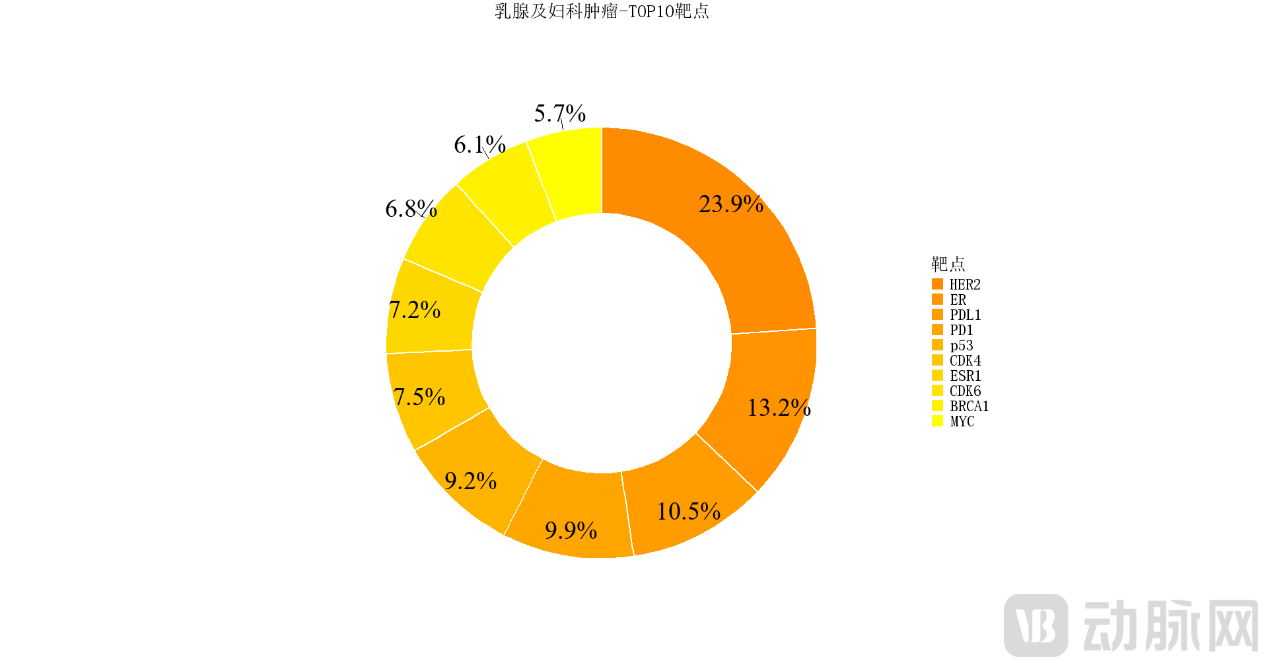

In genitourinary oncology, AR and PSMA serve as core targets for prostate cancer, with expansion to PD-L1 and Nectin-4. Pluvicto®(PSMA-targeted radioligands) have been approved for mCRPC [11]. Nectin-4–targeted antibody-drug conjugates (ADCs), such as enfortumab vedotin, have demonstrated significant clinical benefits in bladder cancer. Breast and gynecologic cancers employ a combination strategy targeting signaling pathways, DNA repair, and immunity, with HER2 (23.9%) and ER (13.2%) being the two core targets.

Source: Compiled from the AACR 2025 conference website and data from PharmCube.

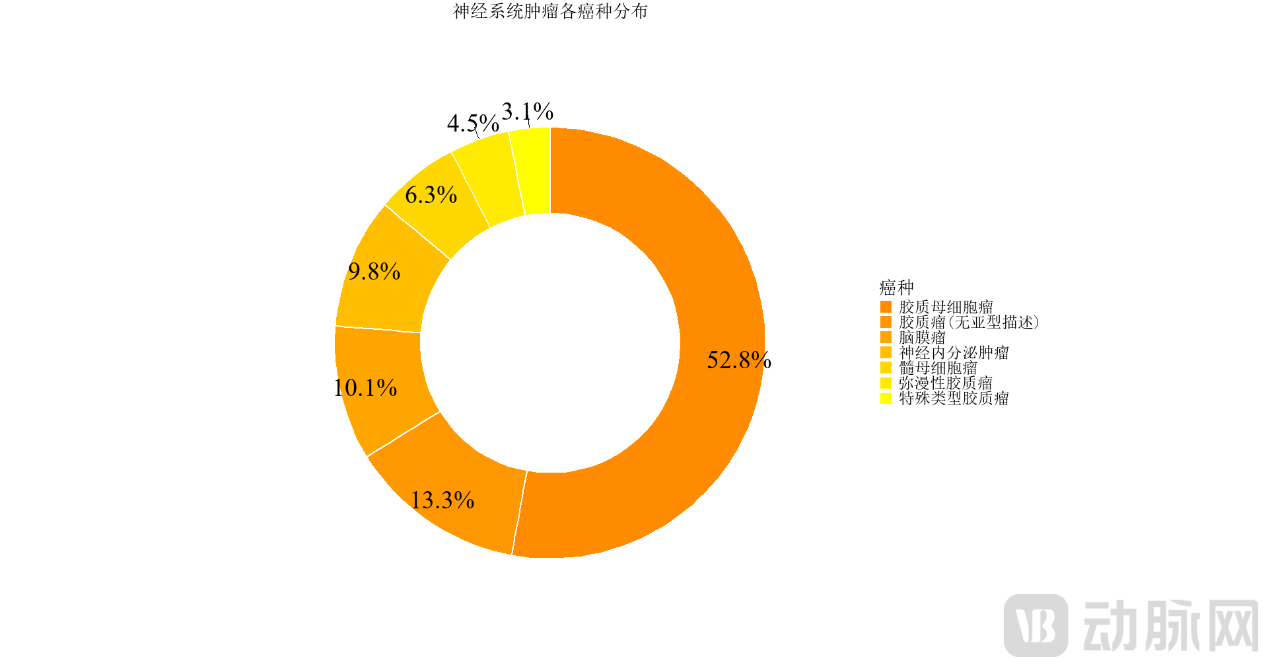

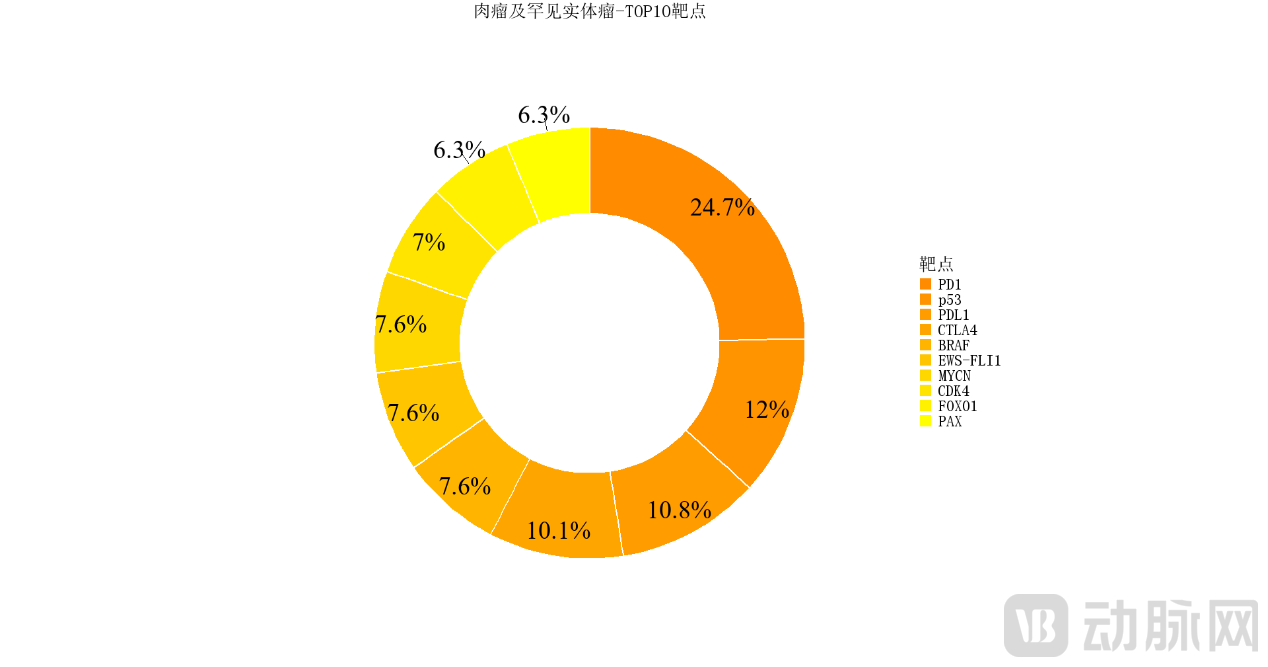

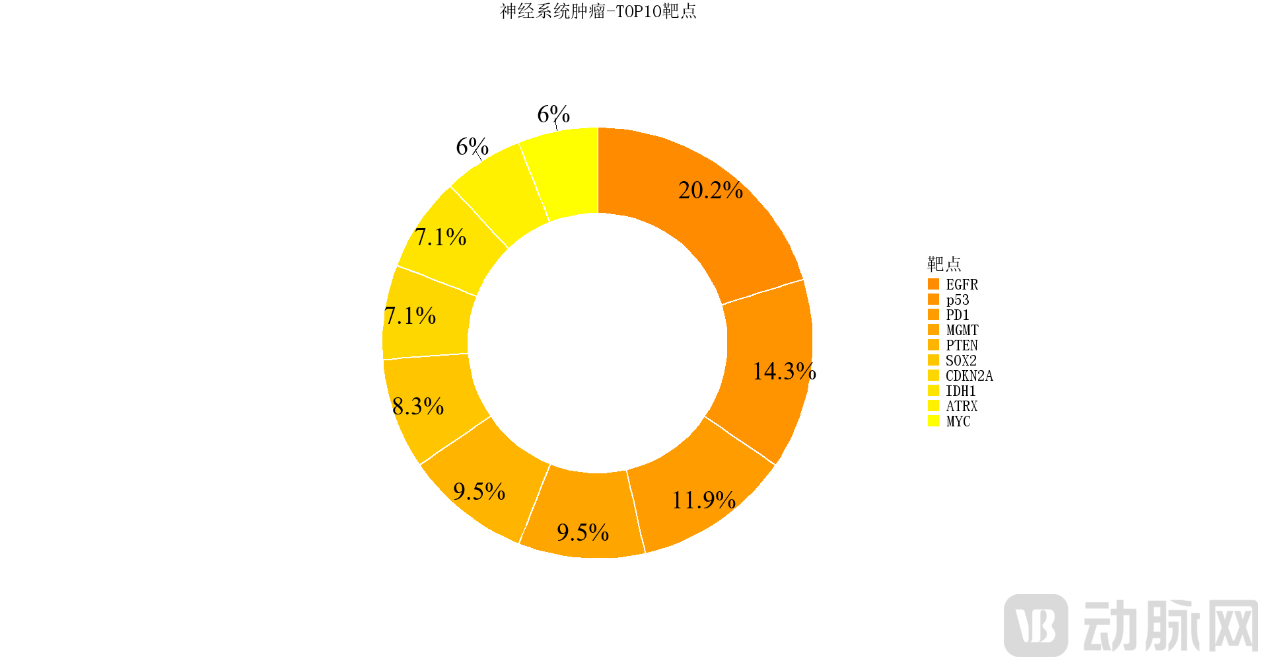

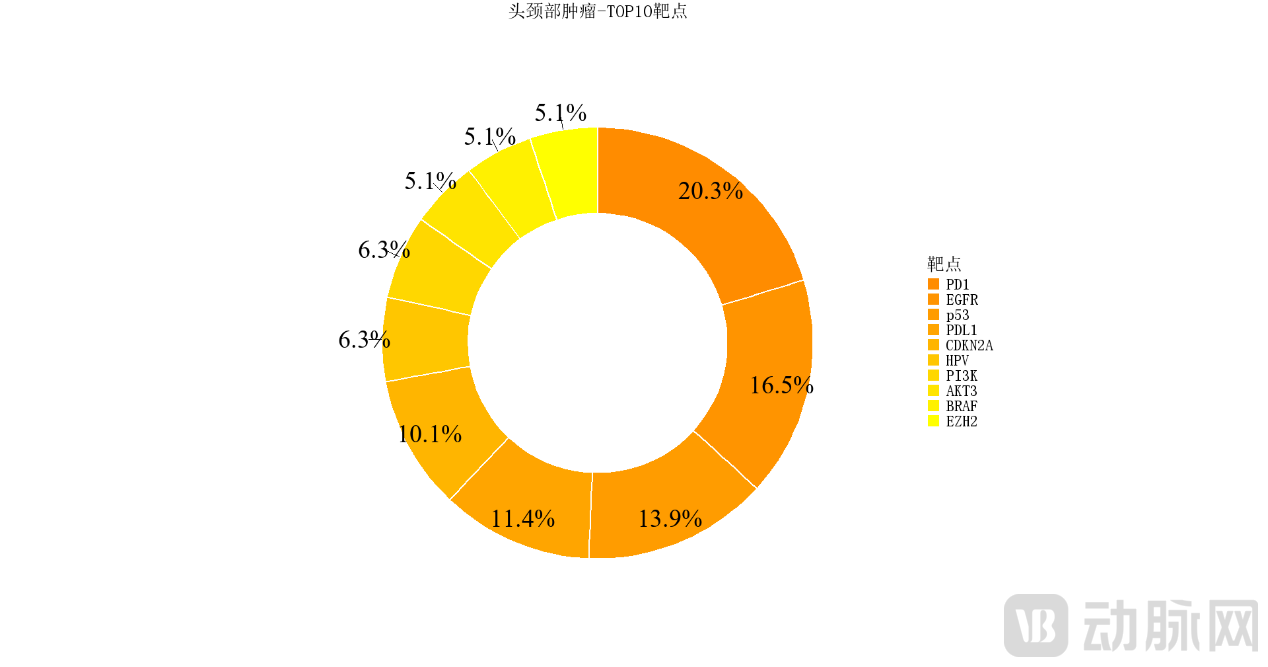

Rare solid tumors focus on immune checkpoints and fusion proteins, with EWS-FLI1 in Ewing sarcoma emerging as a key candidate target. PD-1 (24.7%), p53 (12%), and CTLA-4 (10.1%) rank among the most studied targets. BRAF is widely targeted in melanoma, and combination therapy with PD-1 and CTLA-4 inhibitors has become the standard of care. Neurological tumors primarily target EGFR, p53, MGMT, and IDH1 to construct precise therapeutic combinations. Head and neck tumors combine immune targets with viral antigens, exploring epigenetic pathways. Hematologic malignancies focus on Bcl-2 regulation, CD19/BCMA CAR-T cells and bispecific antibodies, as well as the BTK/FLT3 signaling pathways.

Source: Compiled from data by PharmCube, based on information from the AACR 2025 Annual Meeting website

In summary, p53 and PD-1/PD-L1 rank among the top 10 targets across all six major systems, demonstrating broad therapeutic applicability. KRAS and EGFR serve as core targets in both the digestive and respiratory systems, reflecting their shared mechanisms in solid tumors. Meanwhile, each system also presents unique targets: AR/PSMA are limited to prostate cancer; EWS-FLI1 is specific to Ewing sarcoma; MGMT/IDH1 are focused on the nervous system; CD19/BCMA target hematologic malignancies; and HPV antigens are concentrated in head and neck cancers. These findings clearly reveal the “commonality plus specificity” structure of tumor-targeted therapy.

1.5 Insights: Distribution of Top 3 Systemic Oncology Targets and Technological Trends

Digestive system tumors (gastrointestinal, hepatobiliary, pancreatic, etc.): Representative targets include traditional ones such as EGFR, HER2, KRAS, BRAF, PI3K, and VEGF; emerging targets like Claudin18.2 and GPC3 are gaining attention in gastric cancer and liver cancer.[1]. For example, the Claudin18.2 antibody zolbetuximab has been approved for gastroesophageal adenocarcinoma[12], corresponding studies have been frequently reported at conferences such as AACR. KRAS mutations (particularly G12C/G12D) are highly prevalent in pancreatic and colorectal cancers. While KRAS G12C inhibitors have already been marketed, novel G12D inhibitors (such as zoldonrasib and MRTX1133) are demonstrating efficacy in preclinical studies and Phase I trials.[13,14]Immune checkpoints (such as PD-1/PD-L1) and novel antibody-drug conjugate (ADC) targets (such as HER2 and TROP2) also constitute major areas of research focus. Overall, targeted drug development for gastrointestinal tumors continues to prioritize traditional targets such as EGFR, HER2, and KRAS, while actively exploring the potential of emerging targets including Claudin 18.2, GPC3, and FGFR2 (in cholangiocarcinoma).

Respiratory System Tumors (Primarily Lung Cancer): Key targets include traditional ones such as EGFR, ALK, ROS1, BRAF, MET, RET, KRAS, and the immune checkpoints PD-1/PD-L1; meanwhile, emerging targets such as HER2 mutations, NRG1 fusions (HER3-related), TIGIT, and DLL3 have also appeared. A typical example is lung cancer: the third-generation EGFR inhibitor (e.g., lazertinib) has received FDA approval in combination with the bispecific antibody amivantamab.[15]; The KRAS G12D inhibitor zoldonrasib demonstrates preliminary clinical activity[16]; The HER3-targeted bispecific antibody zenocutuzumab (for NRG1 fusion tumors) has achieved a clinical breakthrough[17]In the realm of new drug development, research focus is expanding from traditional targets such as EGFR and ALK to KRAS variants, HER2/HER3 signaling pathways, and combination inhibition involving various immune pathways. This indicates that the distribution of therapeutic targets in lung cancer exhibits a trend of “parallel development of established and novel targets.”

Genitourinary Tumors (Prostate, Bladder, Kidney, etc.): Prostate cancer has traditionally targeted the androgen receptor (AR); recently, PSMA (prostate-specific membrane antigen) radionuclide therapy received FDA approval (Pluvicto™).[18], demonstrating the therapeutic potential brought by new targets. In bladder cancer research, FGFR3 mutations/fusions are common, with corresponding targeted drugs such as pemigatinib having received approval; Ras/MAPK and PD-1 immune targets also occupy a significant position in clinical trials. For kidney cancer, VEGF/VEGFR (anti-angiogenic) and mTOR pathways remain classic targets, while recent years have seen strategic expansion into immune checkpoints and novel targets such as HIF-2α inhibitors (e.g., belzutifan). Overall, in genitourinary tumors, traditional targets still dominate (such as AR, VEGFR, and FGFR), but research interest in new targets (PSMA, HIF-2α, and various immune checkpoints) is rising significantly.

1.6 Insights: Traditional vs. Emerging Targets: R&D Momentum and Innovation Potential

Traditional Targets (KRAS, EGFR, p53, etc.): These targets have been extensively studied over many years and continue to dominate current R&D efforts. The KRAS family serves as a typical example; in recent years, G12C inhibitors (sotorasib, adagrasib) have successfully reached the market, shifting the research focus toward other variants such as G12D. For instance, zoldonrasib, the first oral KRAS G12D inhibitor, has demonstrated objective responses in patients with non-small cell lung cancer (NSCLC) harboring KRAS G12D mutations.[16]; MRTX1133 Induces Profound Tumor Regression in Pancreatic Cancer Models[14]. EGFR-targeted therapy remains a hot topic in lung cancer research, with next-generation EGFR inhibitors combined with bispecific antibody regimens having entered clinical trials and received approval.[15]. As a classic tumor suppressor gene, direct targeting of p53 remains challenging; current research is increasingly focused on p53 gene compensation therapies or interventions in related pathways (such as MDM2). In terms of pharmaceutical companies’ strategic portfolios, large pharmaceutical firms are continuously advancing upgraded drugs and combination therapies for these classic targets, such as multi-target inhibitors and novel antibody-drug conjugates.

Emerging Targets (BCMA, PSMA, CD19, etc.): Research activity on these targets has increased significantly in recent years, demonstrating substantial innovation potential. In hematologic malignancies, for example, BCMA-targeted therapies (CAR-T and bispecific antibodies) have become a focal point in the treatment of multiple myeloma. P-BCMA-ALLO1, a novel allogeneic CAR-T product developed by Roche/Poseida, demonstrated an overall response rate of 91% in patients with relapsed/refractory multiple myeloma.[19], demonstrating superior efficacy compared to single-target approaches. PSMA-targeted strategies have shown remarkable performance in prostate cancer, and ^177Lu-PSMA radionuclide therapy (Pluvicto) has been approved for advanced metastatic prostate cancer and is being expanded to first-line applications.[18]. For B-cell lymphoma, targeting of CD19 continues to advance through innovative technologies such as CAR-T and dual-target CAR-T therapies; the collaboratively developed bispecific CD19/CD20 CAR-T has achieved the first clinical application of allogeneic dual-target CAR-T therapy.[19]. Research on these new targets is typically advanced in parallel with novel therapeutic platforms (such as CAR-T, bispecific antibodies, ADCs, and multispecific inhibitors), making them a hot topic of discussion at conferences such as AACR. Furthermore, technological trends including ADCs, cancer vaccines, and CRISPR-based immunotherapies are injecting new momentum into research on both traditional and novel targets, spurring greater innovation.

1.7 Insights: Profile of the Top 10 Research Institutions

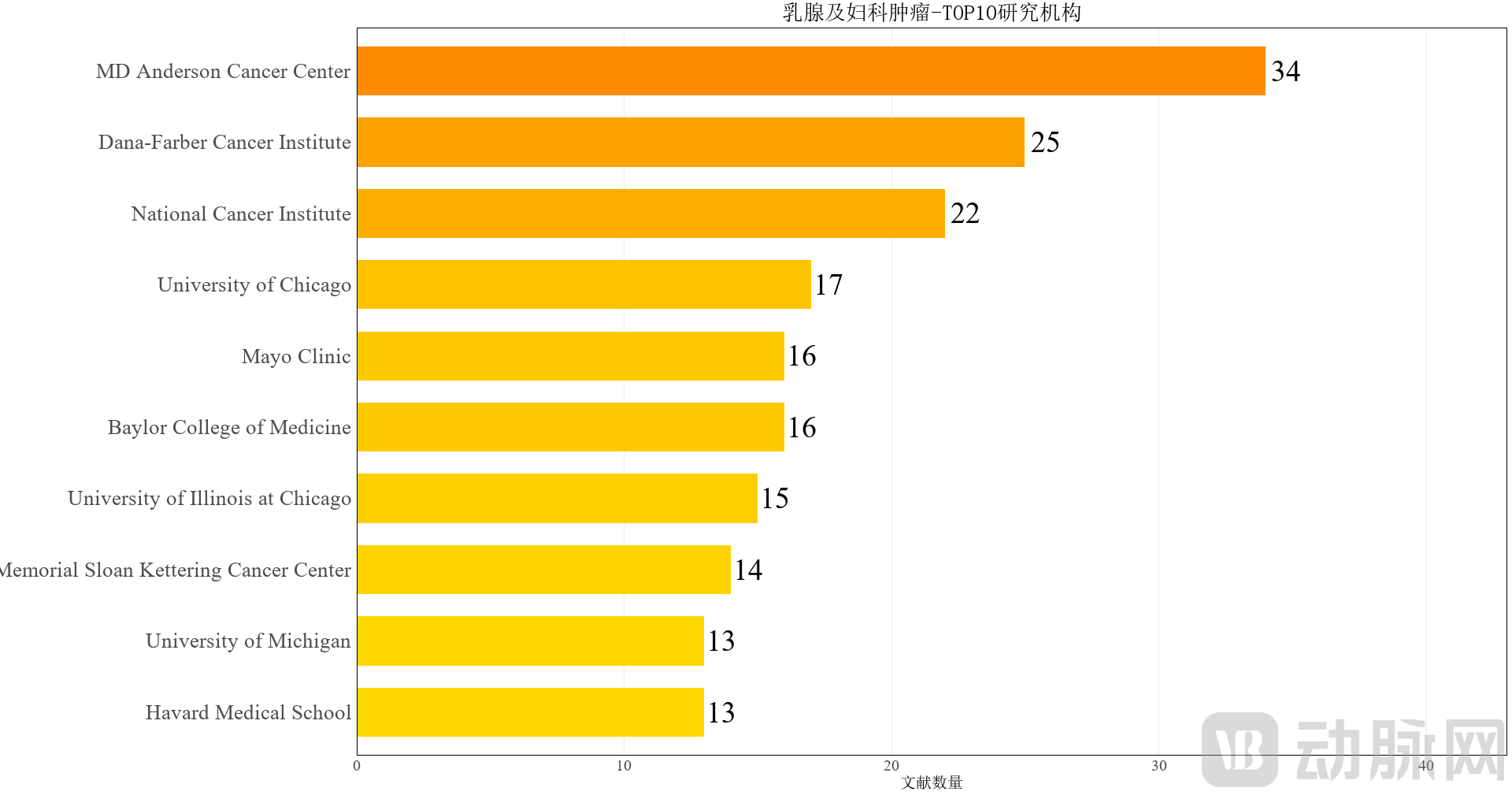

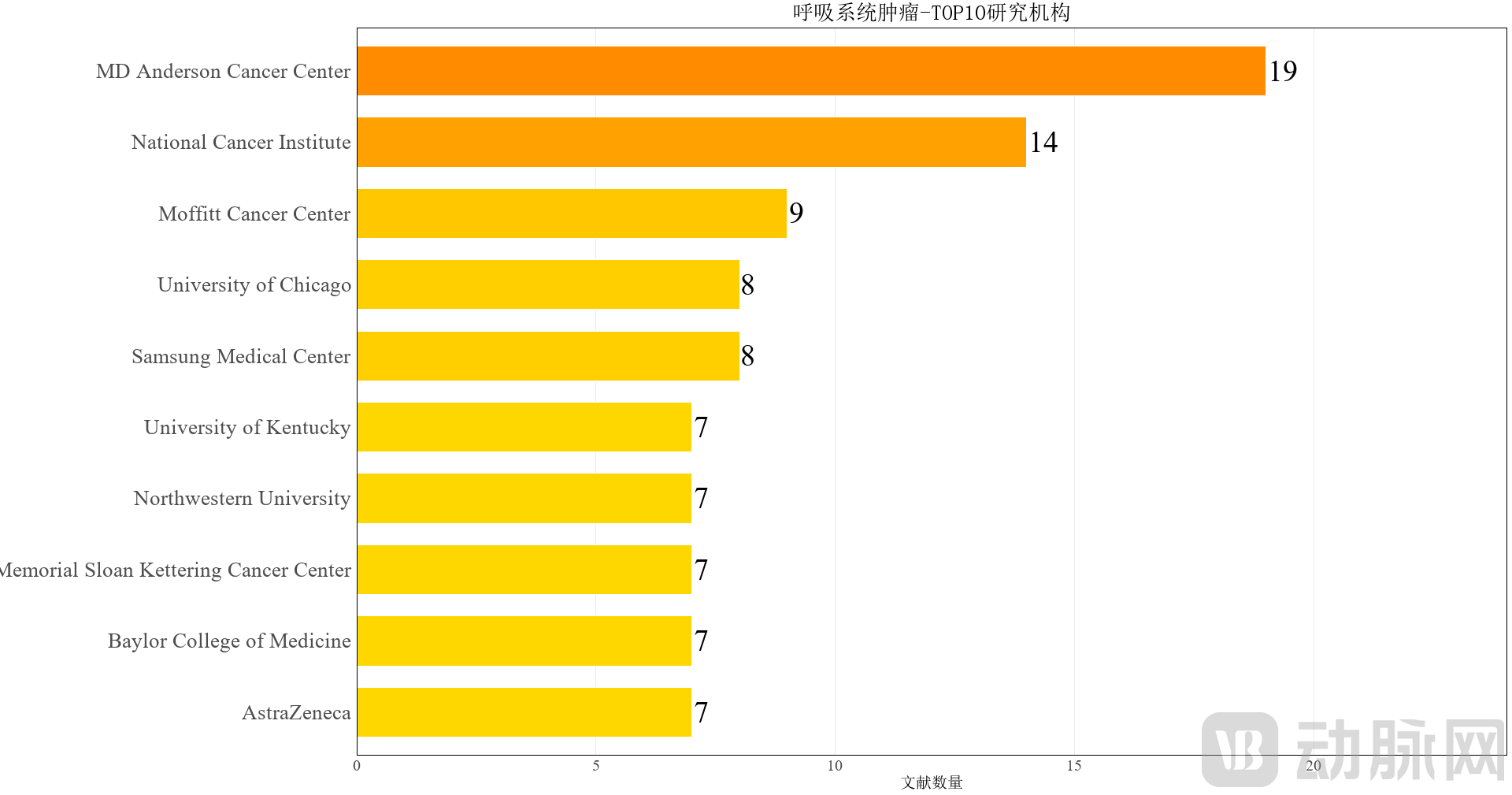

The top-ranking institutions at AACR 2025 primarily include MD Anderson Cancer Center, Memorial Sloan Kettering Cancer Center (MSKCC), Dana-Farber Cancer Institute, Johns Hopkins University, and the NCI/NIH. These centers often possess multidisciplinary integrated platforms and abundant clinical resources. For instance, the immunotherapy research group led by MSKCC reported on the use of neoadjuvant therapy with the PD-1 antibody dostarlimab in mismatch repair-deficient (MMRd) solid tumors, with 80% of patients requiring no surgery after completing treatment.[20]; his team also received an AACR award in recognition of their contributions to the MSK-IMPACT genomic sequencing platform[21]. MD Anderson continues to advance research in areas such as PARP inhibitor–immunotherapy combinations and digital twin models, presenting early data from a trial of the PARP inhibitor plus PD-1 combination therapy in patients with BRCA mutations.[20]. Dana-Farber maintains a leading position in the treatment of various diseases, including head and neck cancer, lung cancer, and breast cancer. Key research focuses include neoadjuvant immunotherapy for HPV-negative head and neck cancer and combined pathway inhibition for KRAS-mutant lung cancer.[22]as well as combination regimens for overcoming drug resistance in breast cancer. The common strengths of these institutions lie in their robust scientific research capabilities, multi-center clinical trial networks, and interdisciplinary collaboration (such as the integration of immunology, genomics, and clinical research), which have enabled them to achieve prominent representation in AACR publications.

Source: Compiled by PharmCube based on information from the AACR 2025 conference website

Part II: Types of R&D Institutions, Regional Distribution, and Innovation Landscape

2.1 Institutional Types and Regions: Universities Lead, with North America as the Core

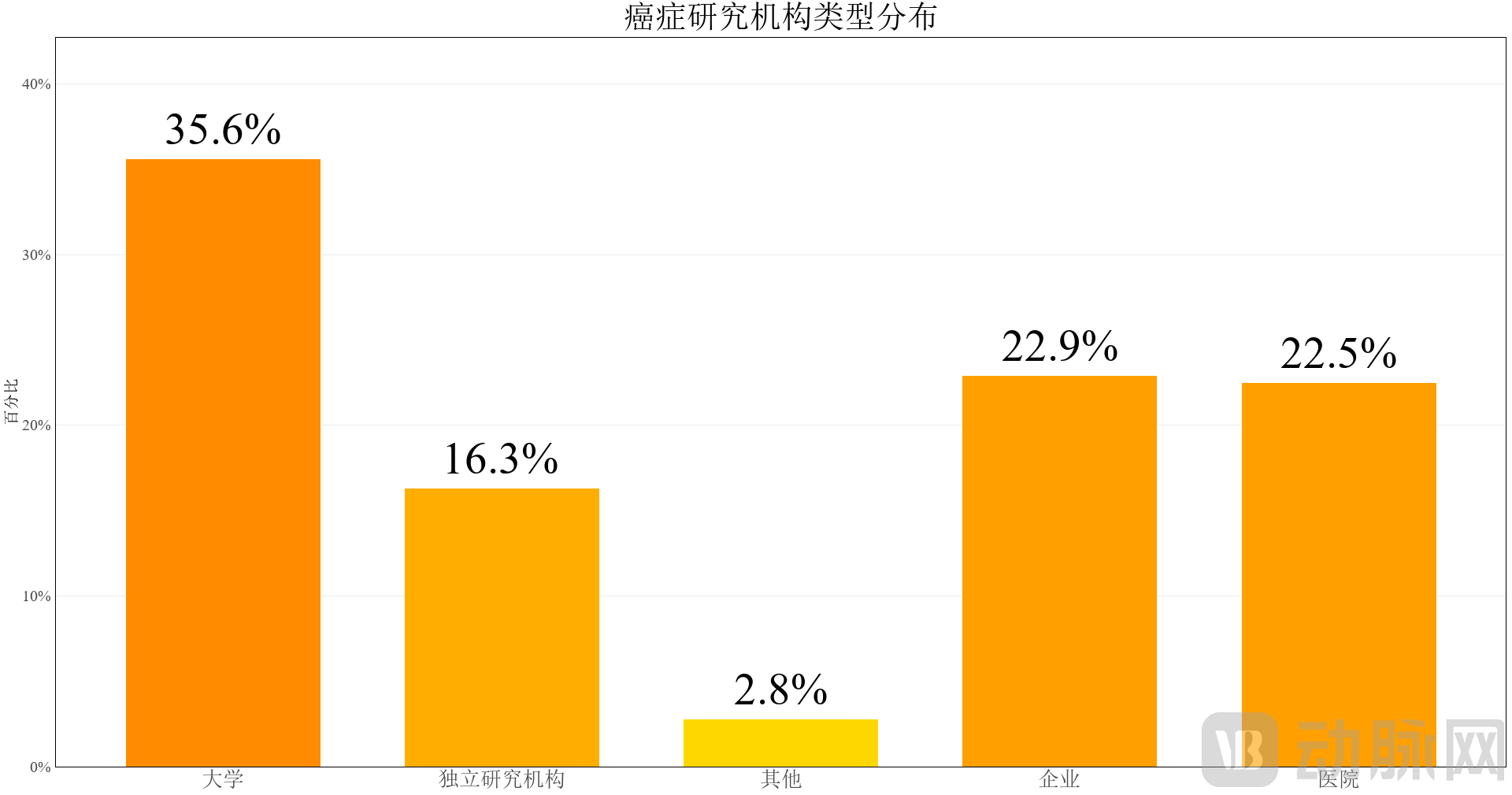

Among the research data disclosed at the AACR 2025 conference, academic institutions dominated with a share of 35.6%, highlighting their pivotal role in basic research and the exploration of innovative pathways. Enterprises and hospitals accounted for 22.9% and 22.5%, respectively, reflecting a dual-engine structure driven by industrial translation and clinical validation as core forces in oncology R&D. Independent research institutions comprised 16.3%, demonstrating their supportive role in methodology, platform development, and fundamental biology.

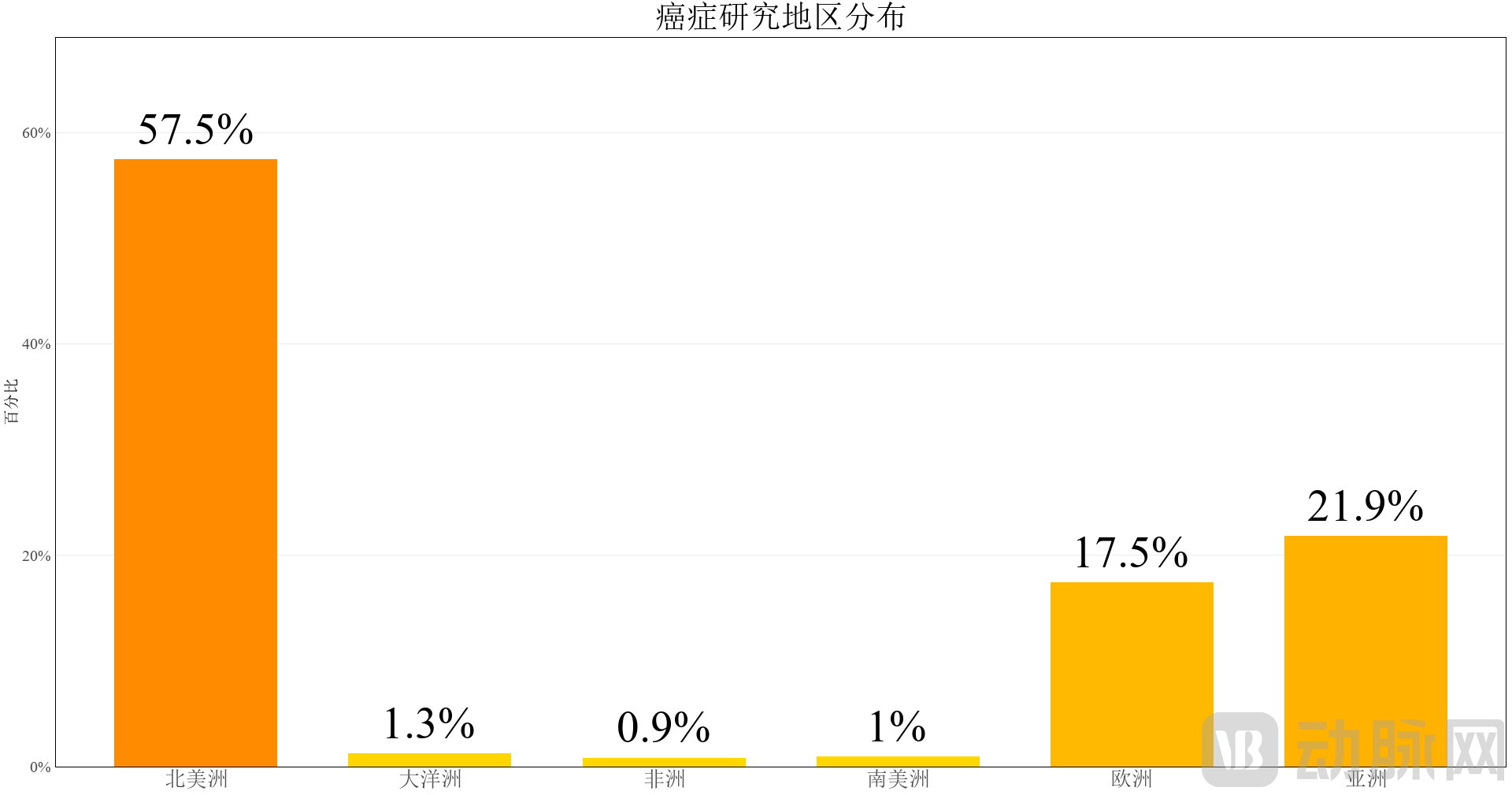

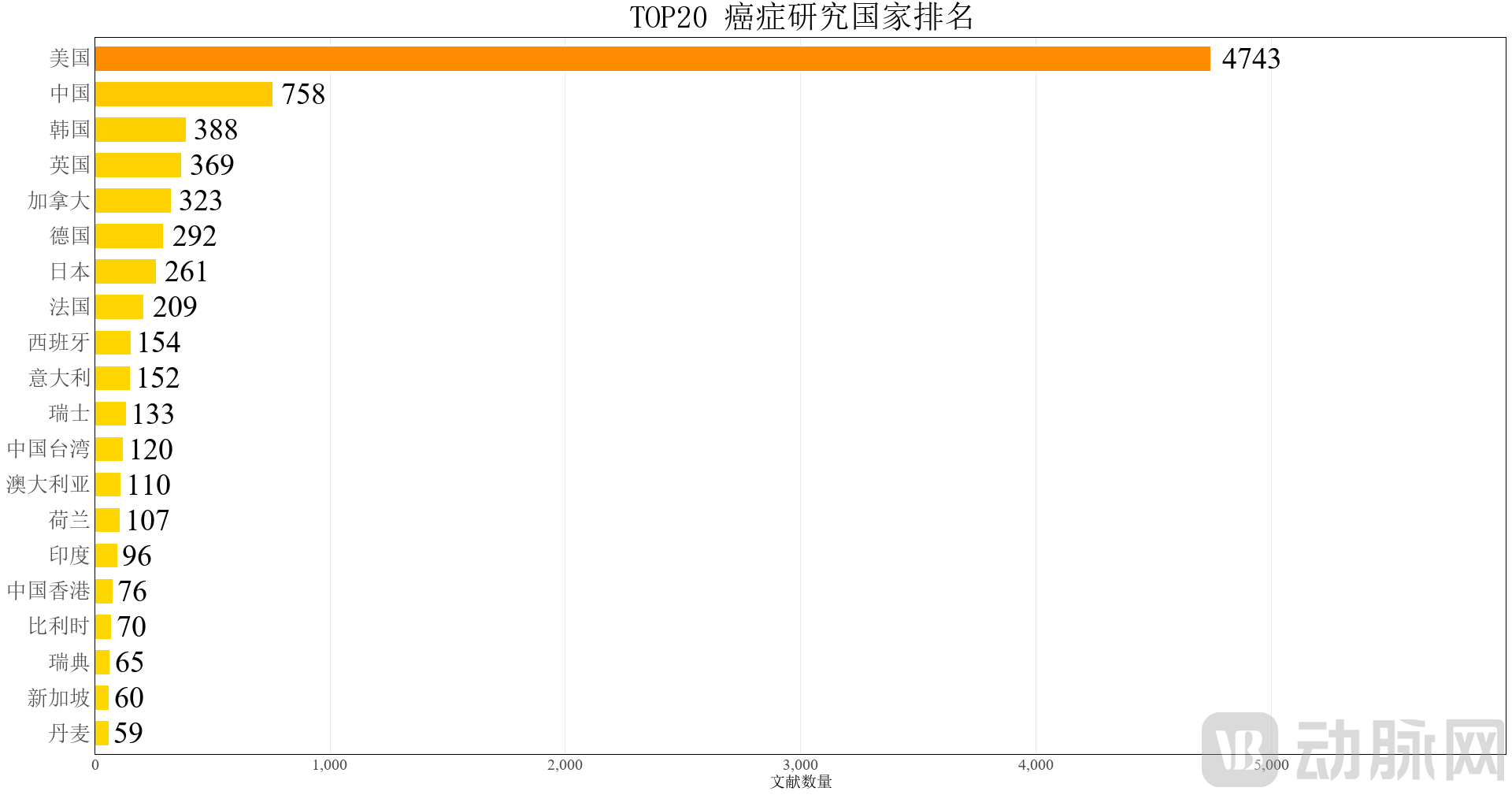

In terms of regional distribution, North America firmly holds its position as the global hub for oncology research, accounting for 57.5% of the total. U.S. research institutions have published more than 4,700 studies, far surpassing any other country and securing the top spot globally. Asia (21.9%) and Europe (17.5%) follow closely behind. China ranks second worldwide with 758 published studies, followed by South Korea with 388. The United Kingdom, France, Germany, Spain, and Italy all rank among the top ten globally, representing regions in Europe with high levels of attention and investment in cancer research, which strongly correlates with their respective population sizes. In contrast, Oceania (1.3%), South America (1.0%), and Africa (0.9%) account for relatively small shares, indicating that there is still significant potential for geographic expansion and collaboration in oncology research worldwide.

Source: Compiled by PharmCube based on information from the AACR 2025 Annual Meeting website

2.2 Trends in Drug Development: Dual-Core Drive by Antibodies and Small Molecules, with Accelerated Expansion of New Modalities

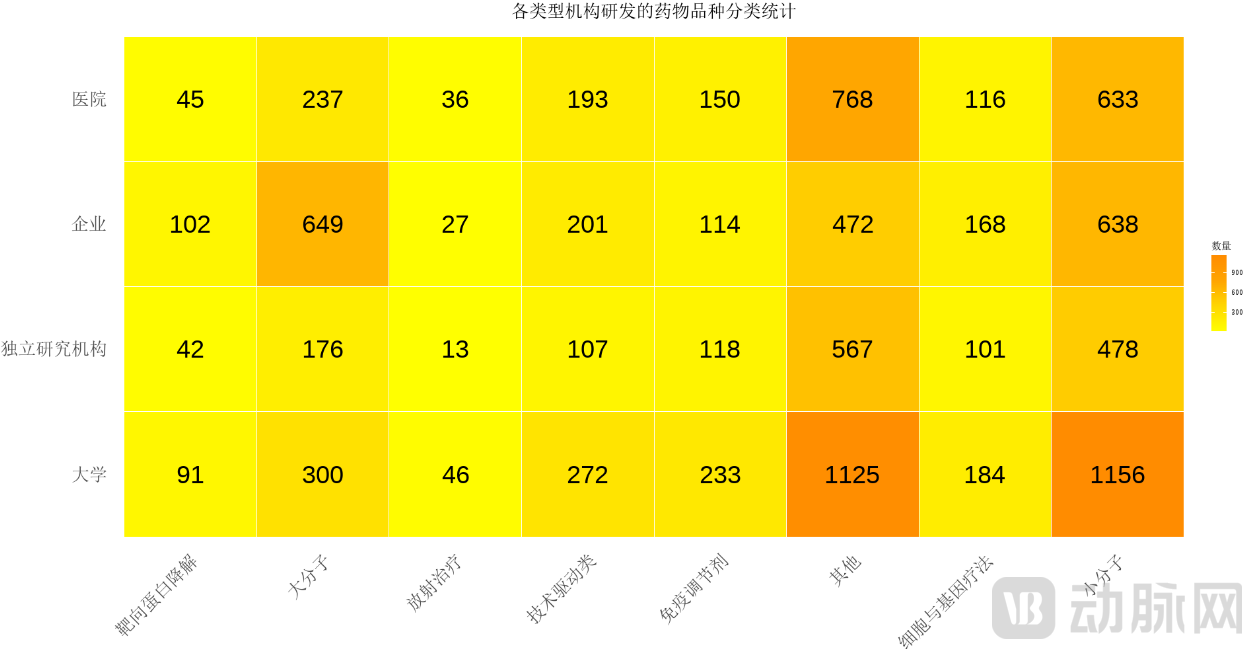

Universities, enterprises, hospitals, and independent research institutions share a common framework in oncology drug R&D pathways characterized by “dual-core (small molecule + large molecule) dominance and platform technology integration,” while exhibiting distinct characteristics in their specific layouts. Universities tend to focus primarily on small molecules (accounting for approximately 40%), with about 30% concentrated on TKIs and traditional targeted therapies, and another 25% focused on cutting-edge platforms such as ADCs, bispecific antibodies, PROTACs, and AI-assisted screening, reflecting their dual advantages in basic research and technology validation. Enterprises demonstrate a balanced structure comprising “30% small molecules + 20% antibodies + 20% ADCs + 10% immune checkpoint inhibitors,” while rapidly advancing the commercialization of emerging mechanisms such as targeted protein degradation and radioligand therapies (10%). Hospital institutions focus more on clinical applications, prioritizing antibody drugs (25%) and immunomodulators (15%), complemented by small molecules (30%) and cell/gene therapies (10%), reflecting their dual emphasis on first-line treatments and CAR-T platforms. Among research institutions, “other” innovative platforms rank first (accounting for approximately 35%), followed by small molecules (30%) and ADCs (15%), with a greater emphasis on high-throughput target screening and mechanistic innovation.

Overall, while consolidating their traditional pathways, the four types of institutions are accelerating their deployment of emerging multimodal and cross-platform therapies, indicating that oncology drug R&D is evolving toward a dual-drive strategy of “targets + platforms.”

Source: Compiled by PharmCube based on information from the AACR 2025 Annual Meeting website

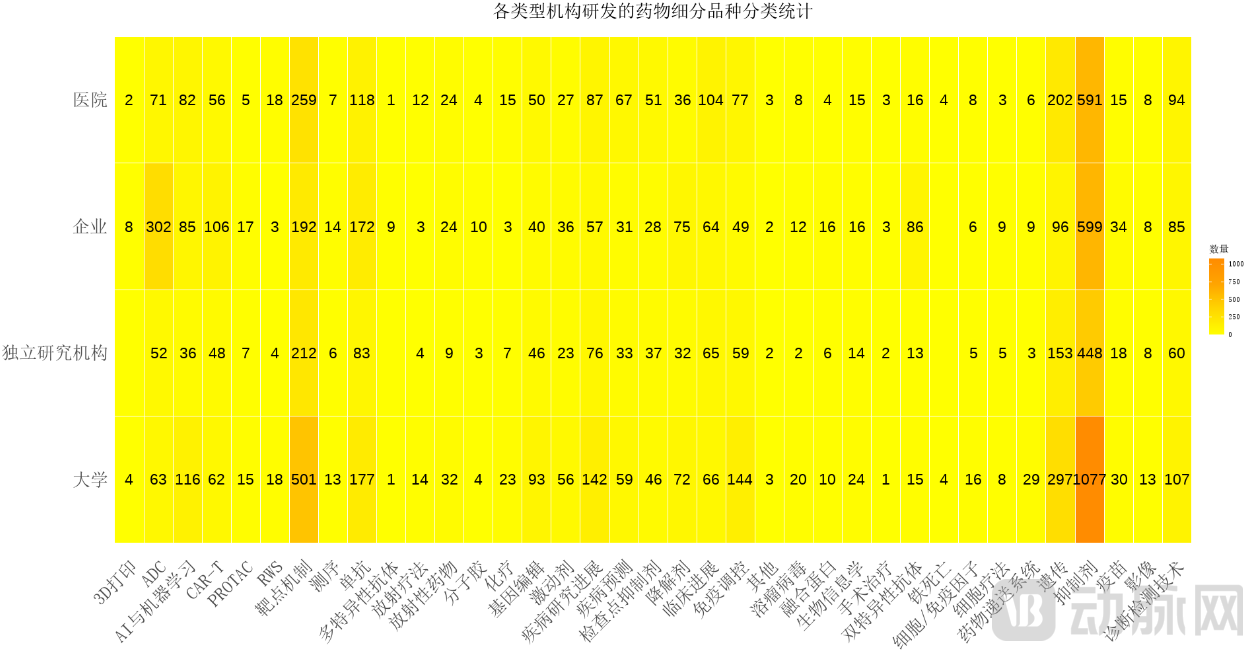

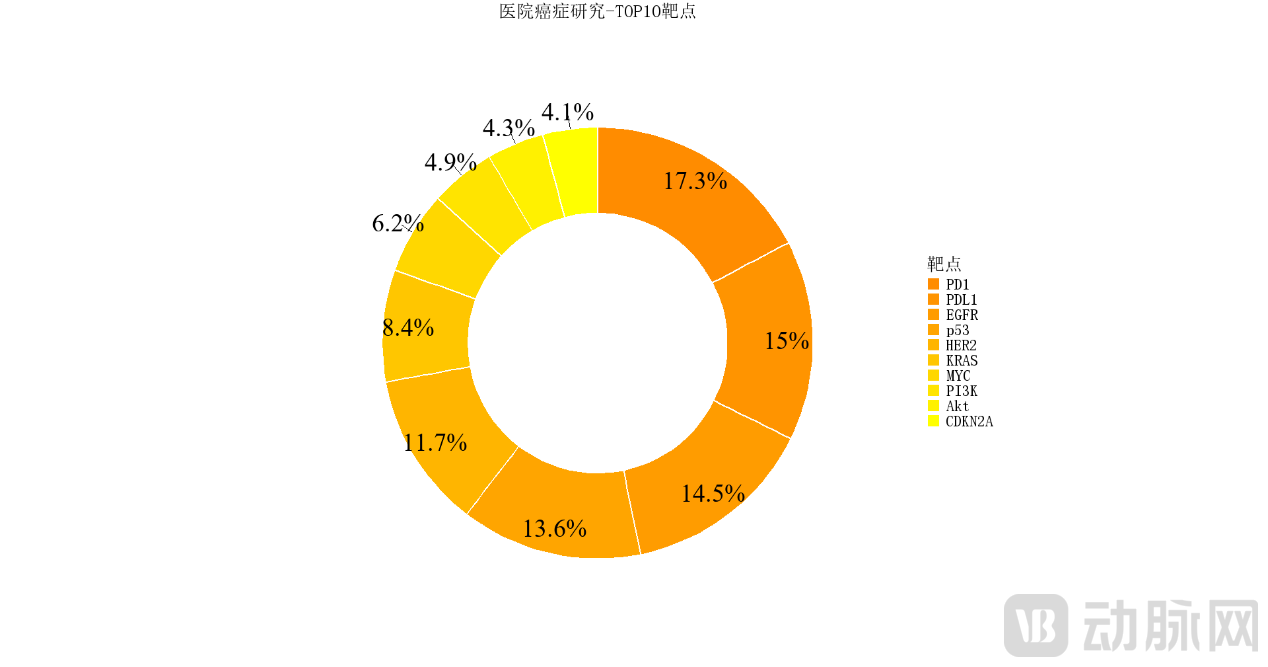

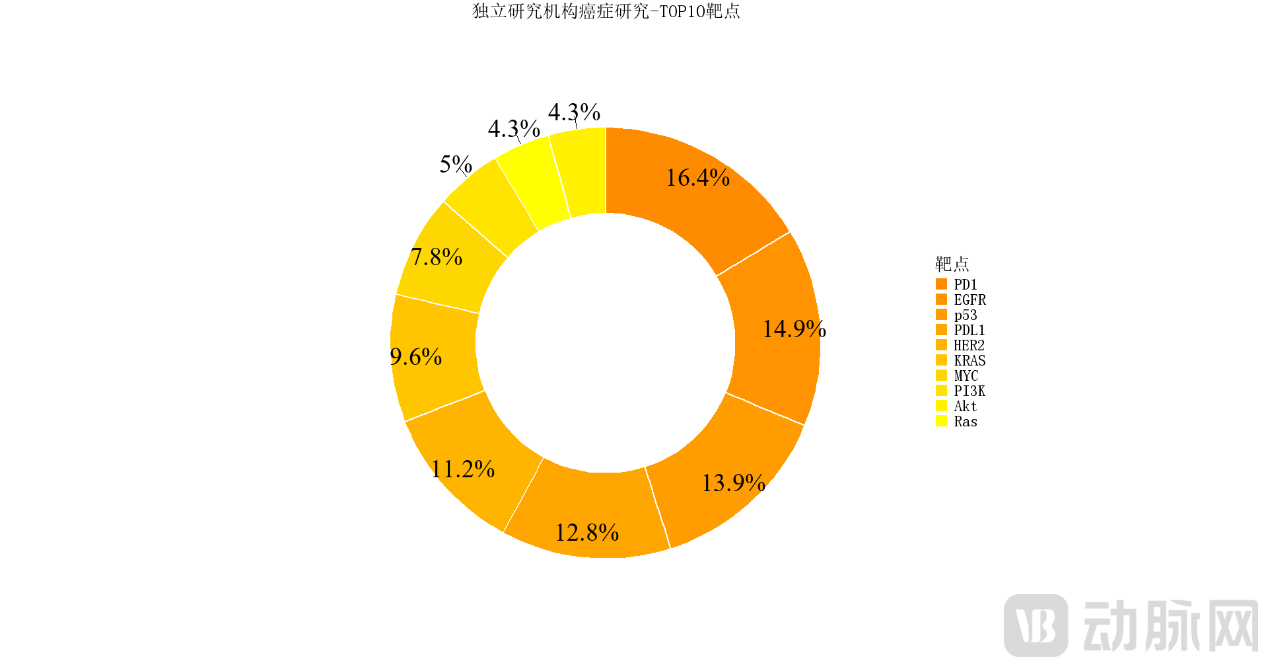

2.3 Analysis of the Top 10 Targets Focused on by Various Types of Institutions

In terms of target selection, PD-1, PD-L1, EGFR, HER2, KRAS, and p53 are core targets of common interest to various institutions, reflecting the long-term strategic importance of immune checkpoints and driver mutation sites in cancer therapy. Universities tend to explore fundamental biological targets such as MYC, AR, Akt, and PI3K, highlighting their academic depth in research on signal transduction, cell cycle regulation, and endocrine tumor mechanisms. Pharmaceutical companies focus on immune-related targets like CD3, TROP2, and CTLA-4, strategically positioning themselves in emerging therapeutic modalities with clear commercial potential, including bispecific antibodies, CAR-T cell therapy, and antibody-drug conjugates (ADCs). Hospitals prioritize targets closely associated with patient stratification and clinical translation, such as CDKN2A, demonstrating their advantage in bridging basic research and clinical practice.Research institutions are focusing on key nodes in signaling pathways such as Ras and Akt, strengthening mechanistic analysis and early validation of tumor dependency mechanisms.

Source: Compiled by PharmaCube based on information from the AACR 2025 Annual Meeting website

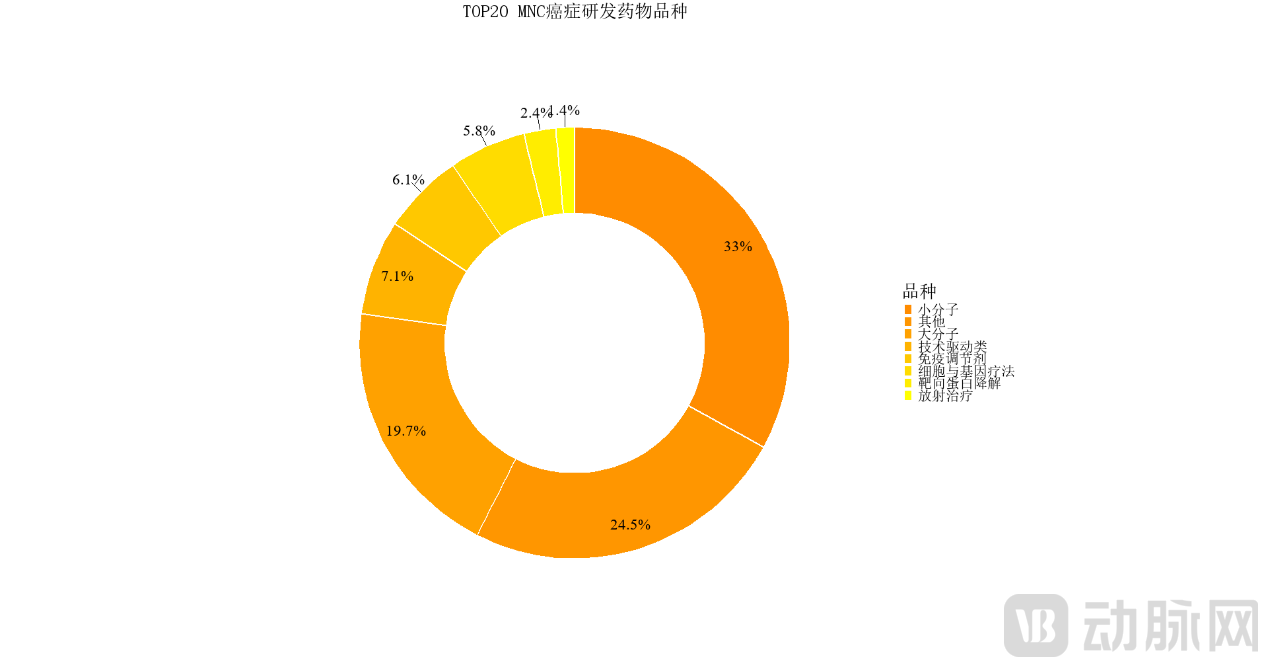

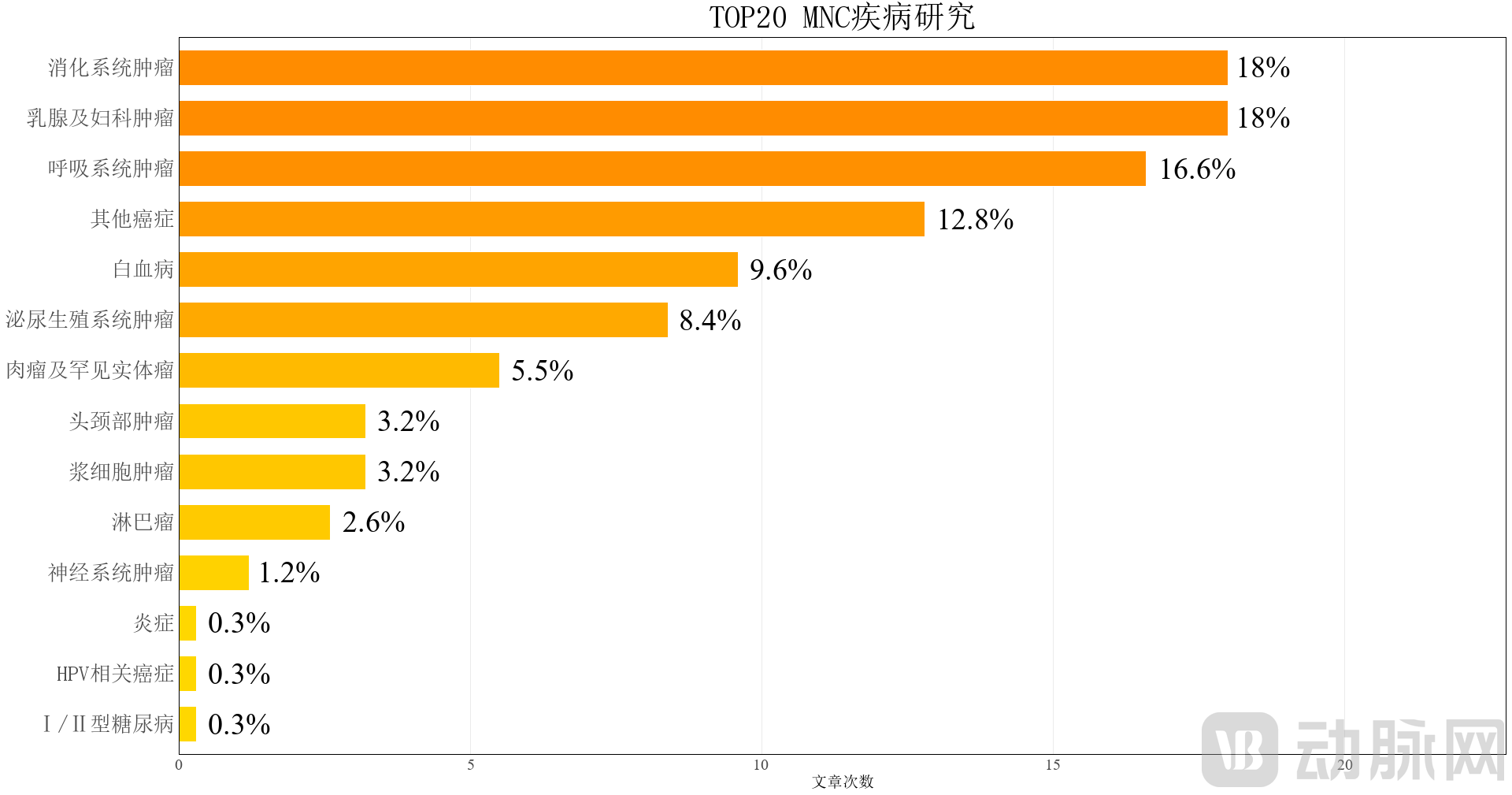

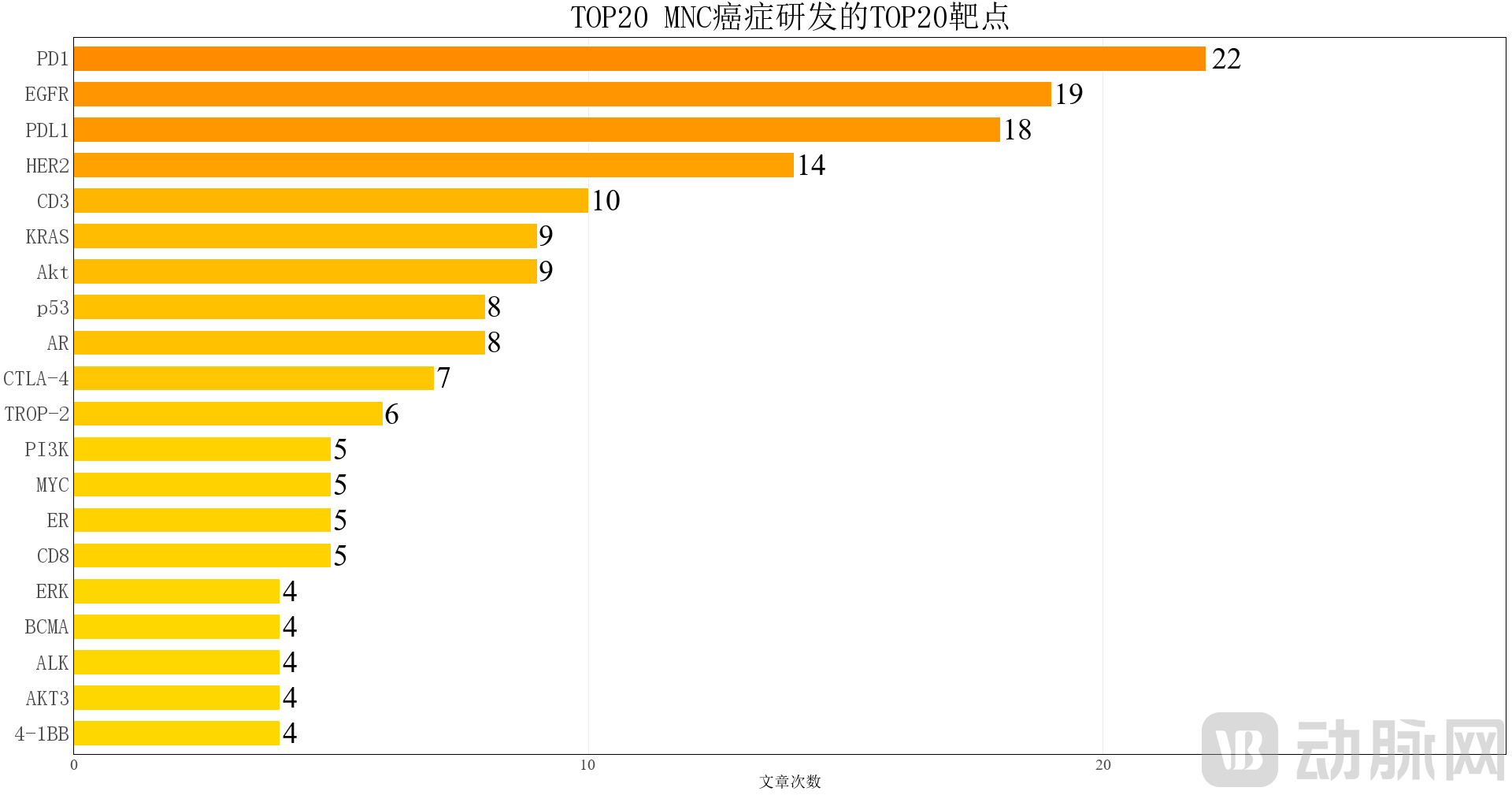

2.4 R&D Trends of the Top 20 Global MNCs

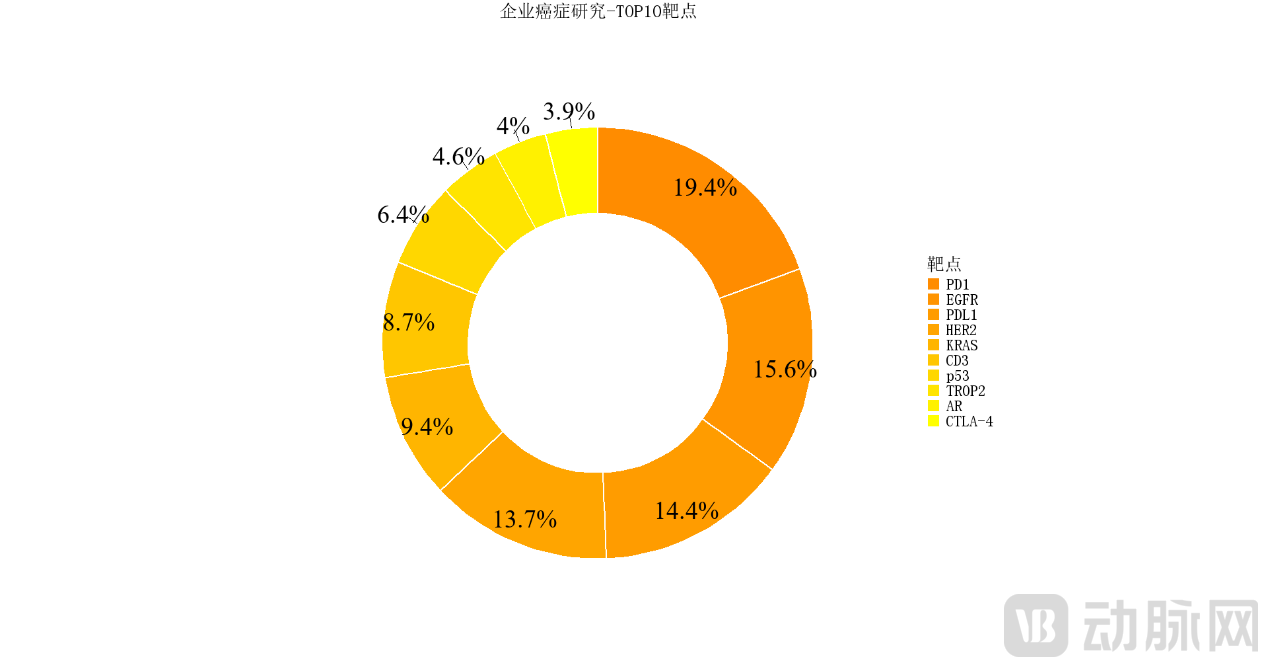

Among the top 20 global multinational pharmaceutical companies (MNCs), small-molecule drugs remain dominant (33%), while the proportions of large-molecule biologics (19.7%) and technology-driven therapeutics (7.1%) continue to rise, reflecting an evolution in R&D models from traditional single-platform approaches toward multi-technology integration. In terms of disease-area focus, gastrointestinal cancers, breast and gynecological cancers, and respiratory cancers are the three key priority areas, accounting for 18%, 18%, and 16.6%, respectively, aligning with the high global burden of these tumors. Regarding target selection, the frequent targeting of PD-1, EGFR, PD-L1, and HER2 (with 22, 19, 18, and 14 instances, respectively) underscores their central role in dual-pronged strategies combining immunotherapy and targeted therapy.

Table: List of the Top 20 Global MNCs

Source: Compiled based on information released by U.S. Pharmaceutical Executive

Source: Compiled from the AACR 2025 conference website and data from PharmaCube.

In terms of representative drugs, Roche’s selective ER degrader giredestrant (for HR+/HER2– breast cancer) has entered Phase III trials; AstraZeneca’s HER2-ADC Enhertu and Imfinzi are continuously expanding their indications in breast and lung cancers; Novartis’ radioligand therapy Pluvicto (targeting PSMA) has improved efficacy in prostate cancer and has been launched on the market.[23]. Furthermore, Johnson & Johnson’s EGFR/MET bispecific antibody Rybrevant combination regimen and Pfizer’s BRAF inhibitor Braftovi also demonstrate the clinical value of target synergy strategies. In terms of emerging technology platforms, Arvinas’ BCL6-targeting PROTAC (ARV-393) has entered Phase I clinical trials, while Bristol Myers Squibb’s AR degrader CC-199 is advancing through preclinical development.[24-27]; Casgevy, a CRISPR gene-editing therapy jointly developed by Vertex and CRISPR Therapeutics, was approved for marketing in the UK in 2023, becoming the first CRISPR-based oncology product and signaling that targeted therapy is entering a new era of gene-level intervention [28]. Furthermore, collaborative explorations by multiple pharmaceutical companies across CAR-T, antibody-drug conjugates (ADCs), and targeted protein degradation platforms are reshaping the paradigm of next-generation cancer treatment.

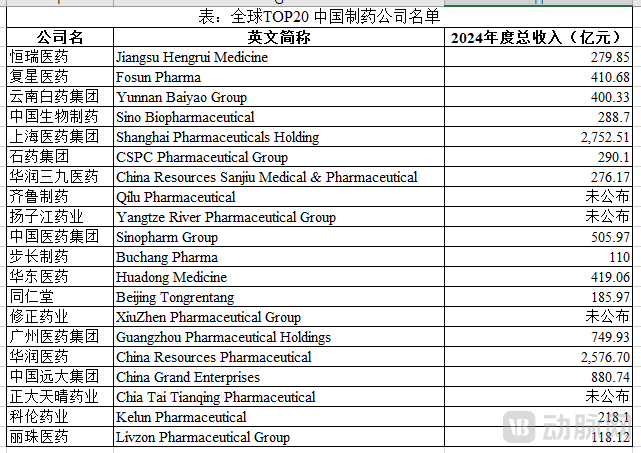

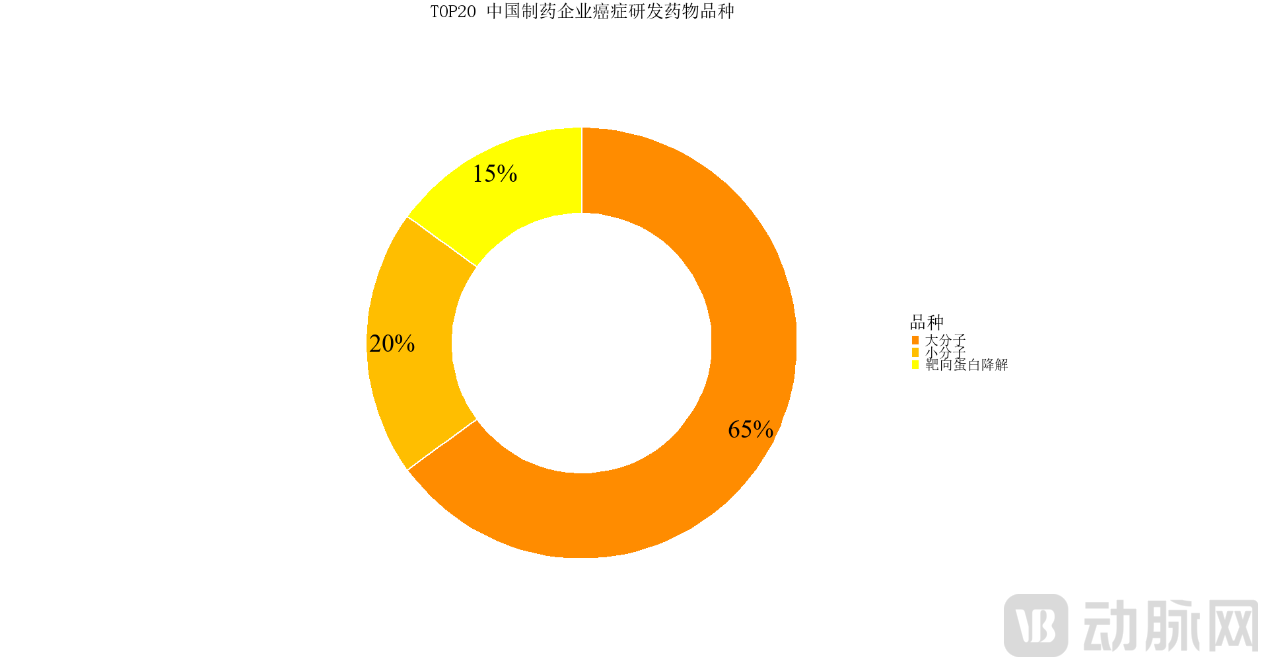

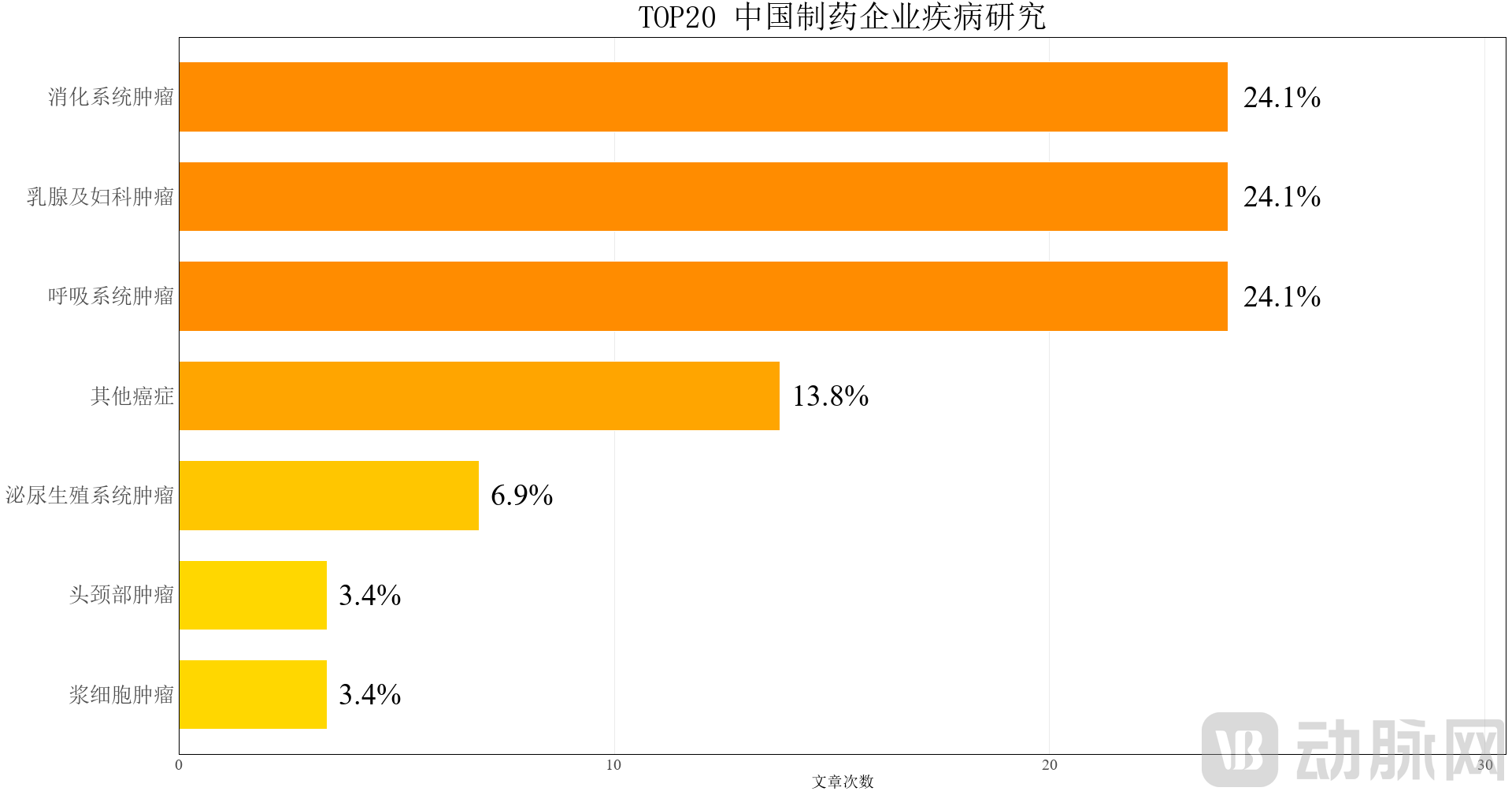

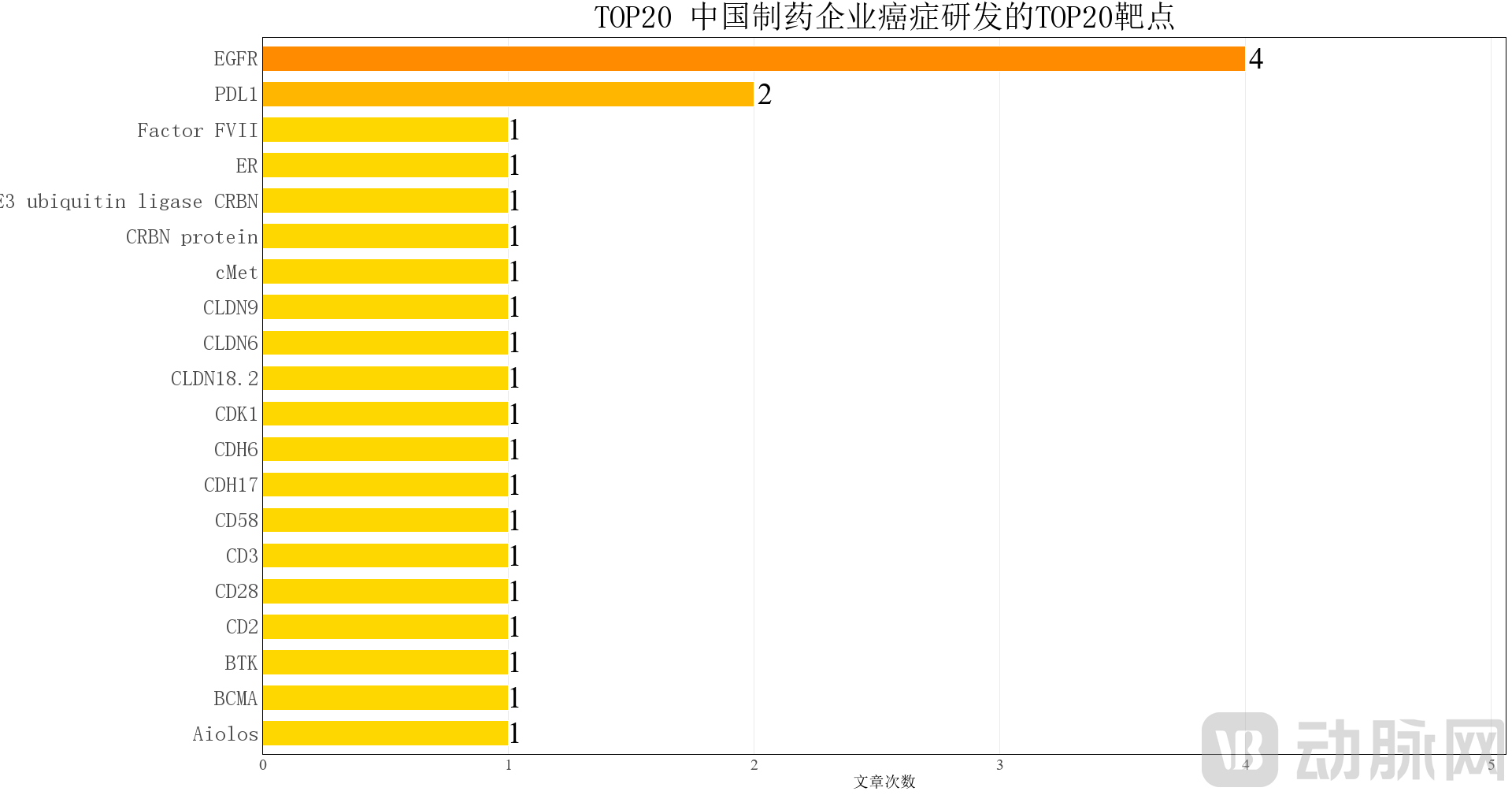

2.5 R&D Trends Among China’s Top 20 Pharmaceutical Companies

China’s leading pharmaceutical companies have risen rapidly in recent years, demonstrating an R&D landscape characterized by “biologics dominance + breakthroughs in emerging technologies.” Statistics show that their investment in large-molecule drugs (such as antibodies and fusion proteins) accounts for up to 65% of their drug portfolio, establishing R&D advantages in product formats including monoclonal antibodies, bispecific antibodies, and antibody-drug conjugates (ADCs). The proportion of targeted protein degradation therapeutics has reached 15%, reflecting active strategic deployment in novel mechanism-based drugs, with particular reserves beginning to accumulate in the areas of PROTACs and molecular glues. In terms of indication selection, gastrointestinal cancers, breast and gynecological cancers, and respiratory system cancers are equally prioritized focus areas, each accounting for 24.1%, aligning closely with the high-incidence trends observed in China’s cancer epidemiology. At the target level, EGFR and PD-L1 were mentioned four times and two times, respectively, indicating sustained attention to classic therapeutic targets.

Table: Top 20 Chinese Pharmaceutical Companies

Source: Compiled from Sohu Medicine, U.S. Pharmaceutical Executive, and financial reports of listed companies

Source: Compiled from the AACR 2025 conference website and data from PharmaCube.

In recent years, Chinese pharmaceutical companies have continuously enhanced their capabilities in original innovation. Taking Hengrui Medicine as an example, its HER2-ADC SHR-A1811 has been included in the National List of Breakthrough Therapy Designations, and the company has more than 10 differentiated ADC projects currently in clinical development.[29]Huadong Medicine focuses on gastrointestinal tumor antigens; for instance, its dual-target ADC VBC108, targeting CDH17 and CLDN18.2, demonstrates the potential for synergistic activation of dual pathways.[30]. In the field of immunotherapy, the launch of cadonilimab, the first domestically produced PD-1/CTLA-4 bispecific antibody, marks the entry of domestic combination immunotherapy strategies into a stage of mature clinical application.[31]. In the field of PD-1 monoclonal antibodies, leading companies such as Junshi Biosciences and Innovent Biologics have established stable pipelines; furthermore, fusion proteins (such as efgartigimod alfa) and CAR-T/ADC projects are also advancing rapidly under the logic of “domestic substitution.”[32]According to statistics from PharmCube, between 2016 and 2023, China’s top 20 pharmaceutical companies cumulatively obtained approval for 88 new drugs, of which 64% focused on oncology, 41% were independently developed, and 59% were acquired through licensing and collaborations.[33]. This indicates that while meeting domestic market demand, Chinese pharmaceutical companies are advancing toward higher-level original innovation through international cooperation and platform development.

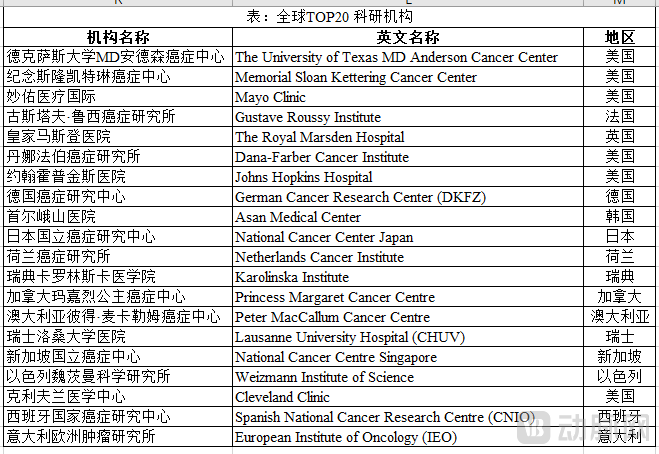

2.6 Research Trends of the Top 20 International Scientific Research Institutions

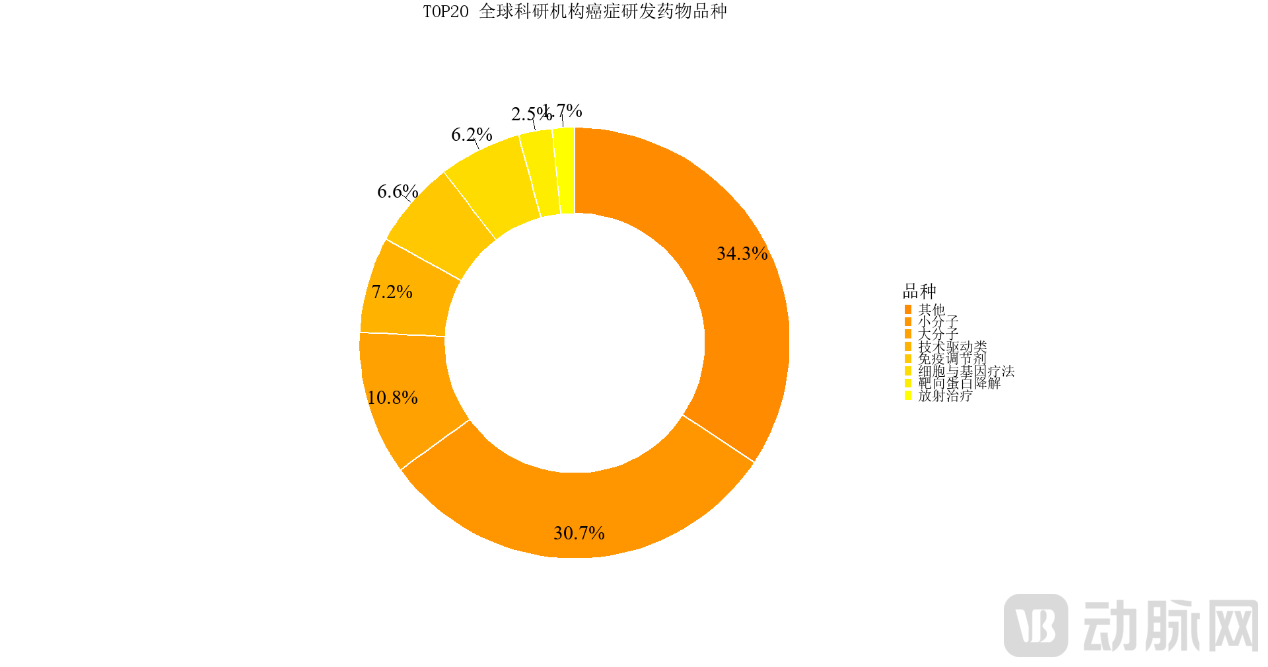

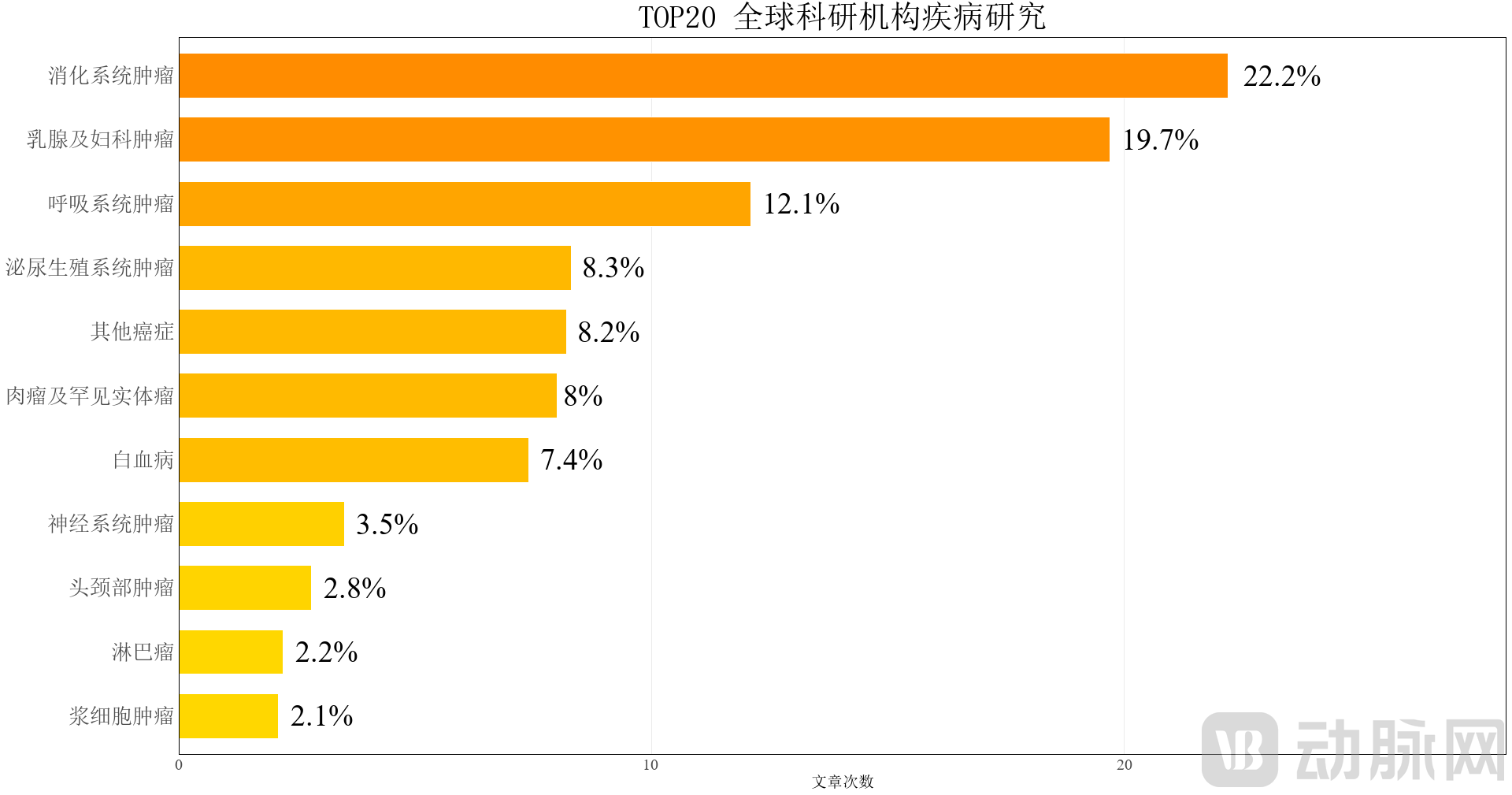

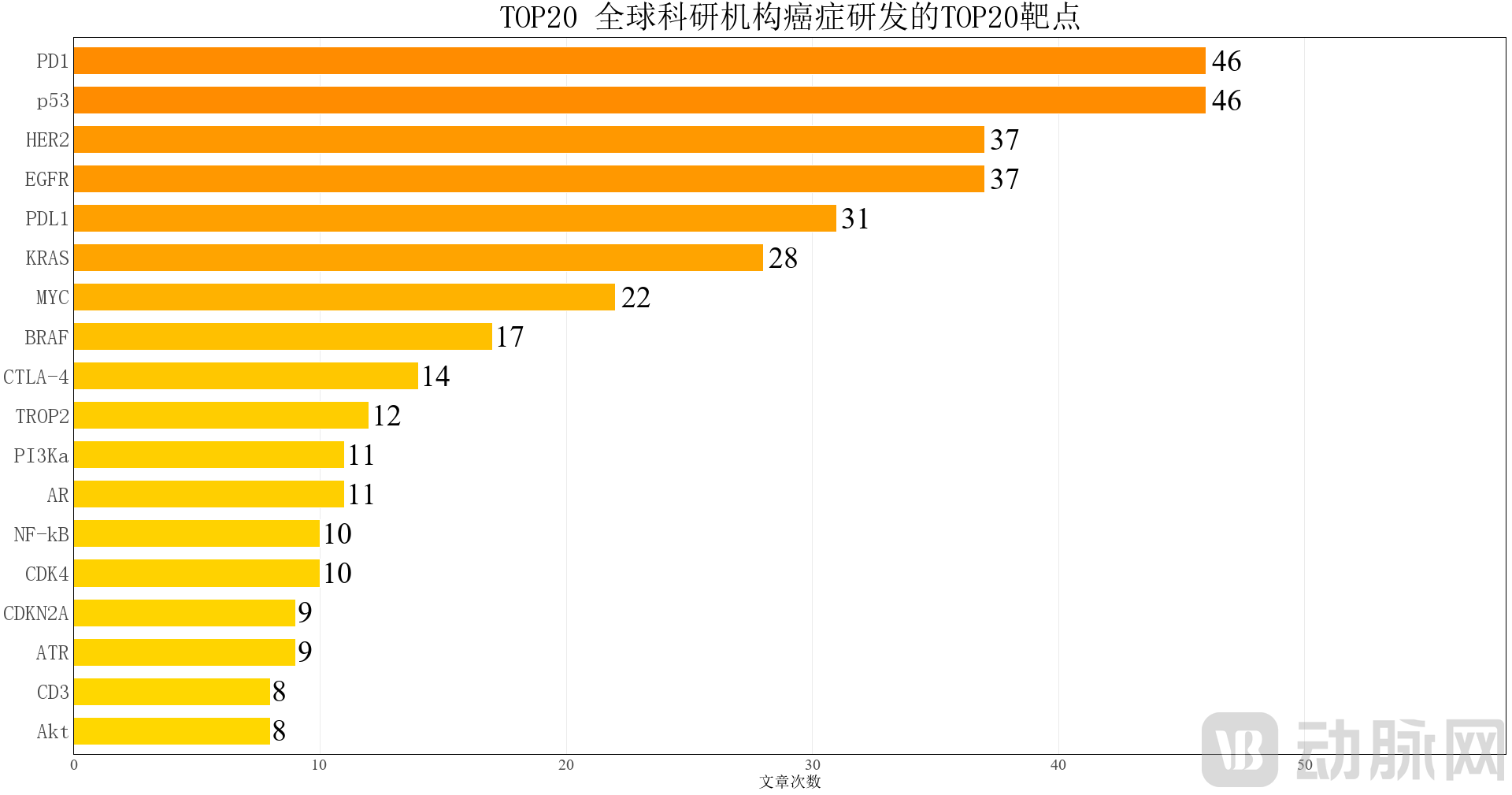

Leading global research institutions are demonstrating strategic characteristics of platform-based and diversified drug development. In terms of drug types, small-molecule and large-molecule drugs account for 30.7% and 10.8%, respectively; technology-driven approaches (such as protein degradation and delivery systems) represent 7.2%; while immunomodulators and cell/gene therapies account for 6.6% and 6.2%, respectively. This forms a multimodal layout centered on target mechanism research and oriented toward platform integration. Regarding disease focus, digestive system tumors (22.2%), breast and gynecological tumors (19.7%), and respiratory system tumors (12.1%) rank as the top three, reflecting that research institutions prioritize high-incidence, high-mortality cancer types in alignment with epidemiological trends. At the target level, PD-1 and p53 are the most frequently studied targets (each mentioned 46 times), highlighting their foundational role in research on the immune microenvironment and genomic stability mechanisms.

Table: Top 20 Global Research Institutions

Source: Compiled from information on globally authoritative cancer treatment institutions published by Newsweek and Statista.

Source: Compiled by PharmCube based on information from the AACR 2025 conference website

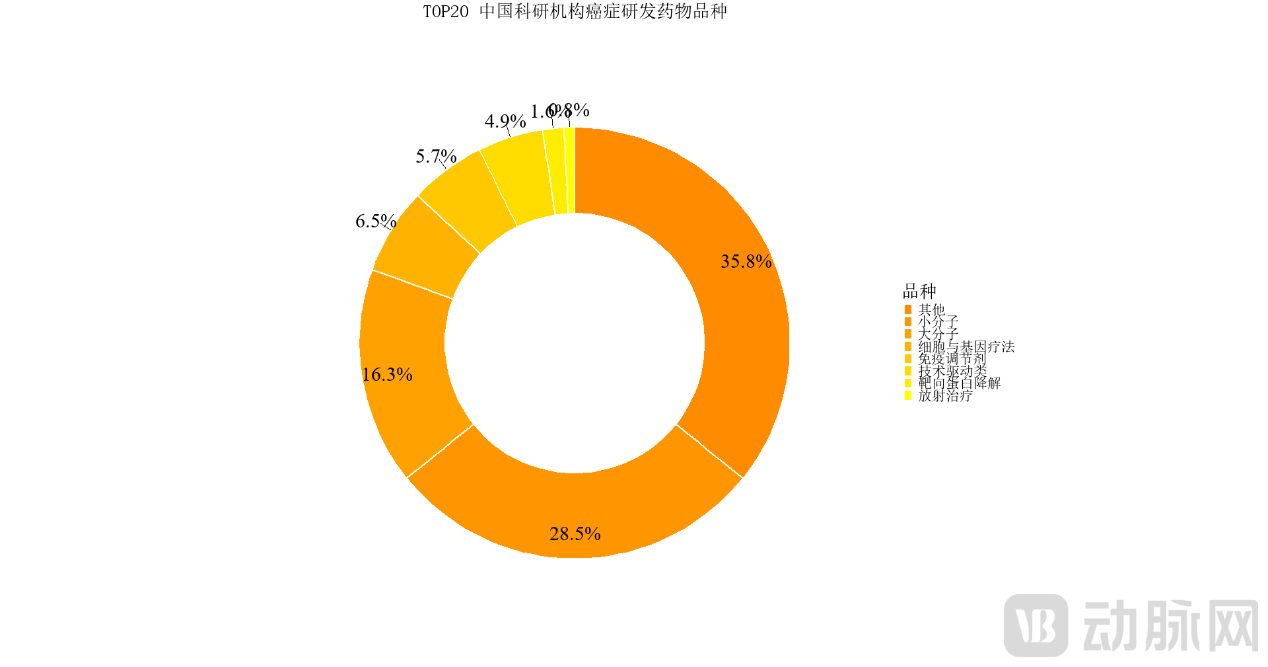

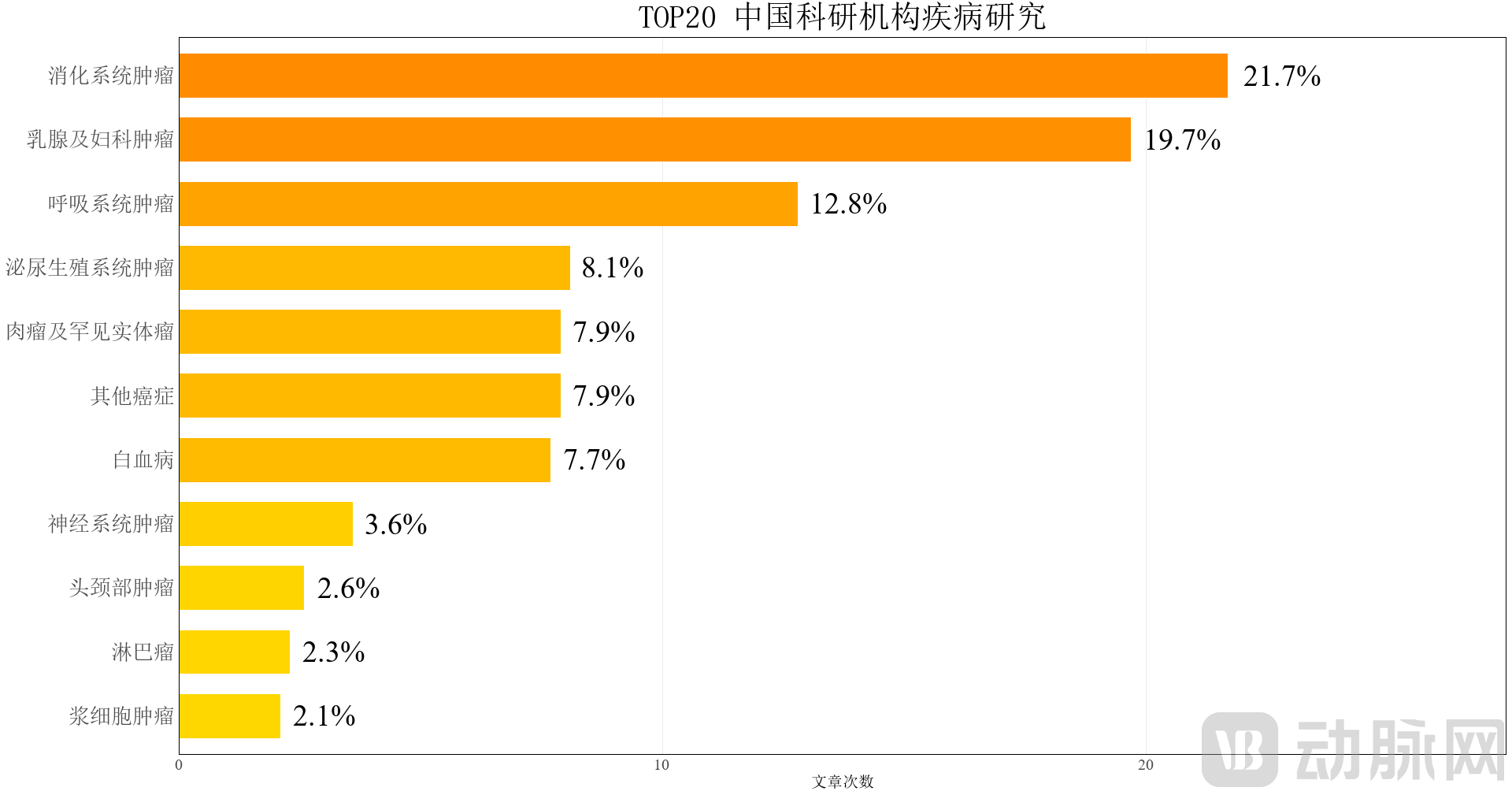

2.7 Research Trends of the Top 20 Chinese Research Institutions

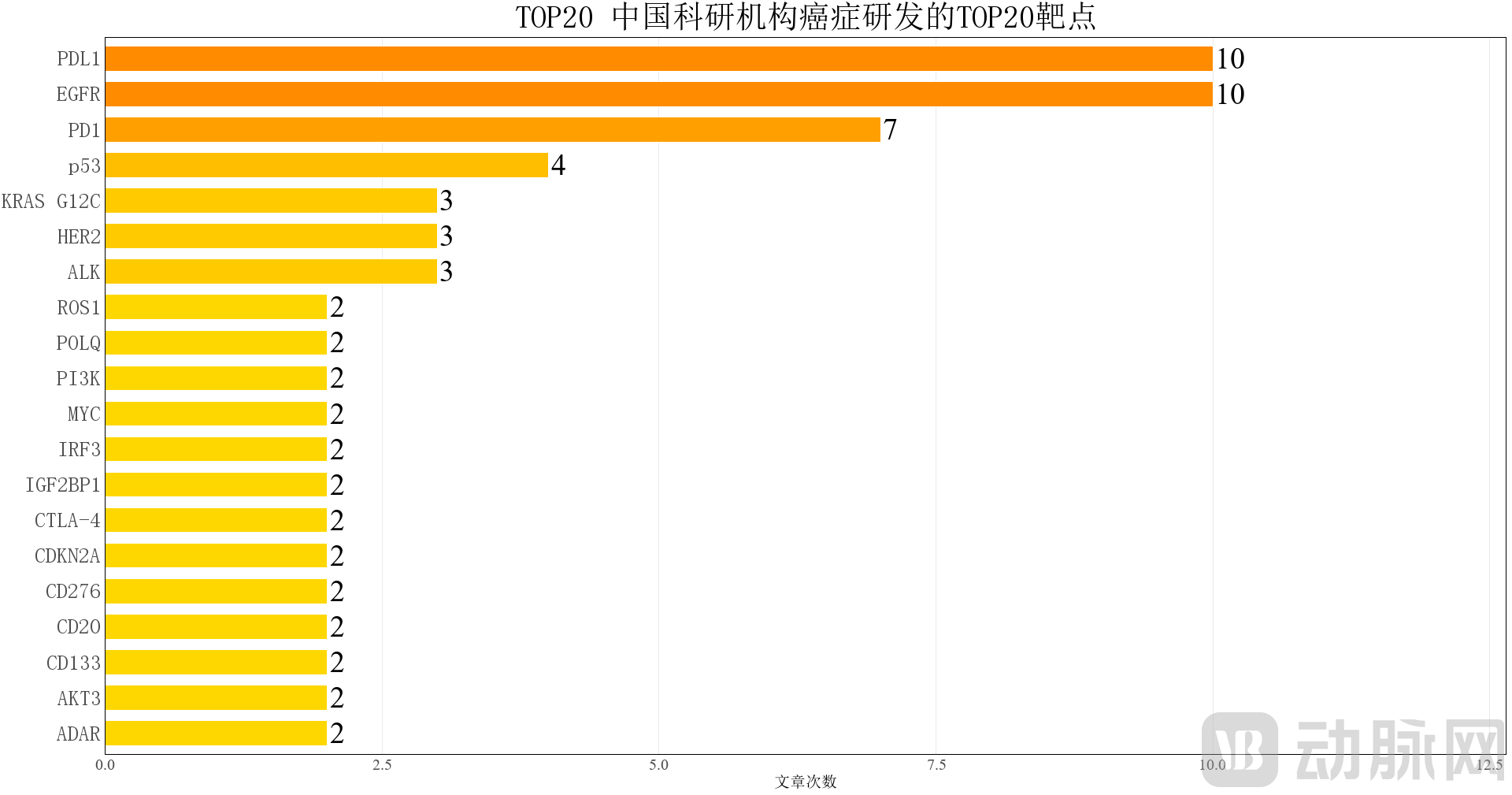

China’s top research institutions are also demonstrating a trend toward diversified platforms and deepened mechanisms in oncology drug research. In terms of drug types, small molecules remain dominant (28.5%), while the proportions of large molecules (16.3%) and cell/gene therapies (6.5%) are increasing year by year, reflecting rapid adoption of cutting-edge therapeutic approaches. Regarding disease focus, digestive system tumors (21.7%), breast and gynecological tumors (19.7%), and respiratory system tumors (12.8%) continue to be the primary areas of interest, with research priorities aligned with international trends. In target selection, PD-L1 and EGFR are tied for first place (each mentioned 10 times), indicating sustained interest and in-depth investigation into immune checkpoints and classic driver genes.

Table: Top 20 Research Institutions in China

Source: Compiled from information released in the "2023 China Hospital Rankings" by the Institute of Hospital Management, Fudan University, and the "2024 China Health Statistics Yearbook."

Source: Compiled from data by PharmCube based on information from the AACR 2025 Annual Meeting website.

Insight: Analysis of Target Research Trends at Leading International and Chinese Scientific Research Institutions

International research institutions are widely applying CRISPR screening, multi-omics integration, and AI-assisted identification to promote the systematic development of new target discovery frameworks. The “Cancer Dependency Map” project, launched by the Wellcome Sanger Institute in the UK in collaboration with EMBL-EBI, has established a target prioritization scoring system across more than 300 cancer models through CRISPR knockout screening of 20,000 genes.[34]The NCI-led CPTAC project has identified over 2,800 potential druggable targets through integrated proteomic and transcriptomic analysis.[35]. AI is also widely used in molecular network modeling and target prediction, playing a foundational role in precision treatment strategies[36]. Such outcomes are mostly released in the form of open data sharing and promoted for industrial translation through alliances such as Open Targets.

Chinese research institutions have also rapidly adopted the aforementioned tool systems, with some teams systematically conducting CRISPR screening, single-cell transcriptome sequencing, and AI-assisted drug target prediction.[37]At the policy level, the National Major New Drug Creation Special Project promotes a tripartite collaborative effort among clinical practice, laboratories, and enterprises. International resources such as the CPTAC database are also gradually becoming accessible to China, facilitating the sharing of target resources and localized exploration.

2.8 Commonalities and Differences: A Comparison of Global and Chinese R&D Layouts

In terms of commonalities, global and Chinese research institutions are converging in their focus on therapeutic targets and platform technologies. They are extensively studying core targets such as PD-1/PD-L1, EGFR, and HER2, and implementing drug innovations through various modalities, including antibody-drug conjugates (ADCs), bispecific antibodies, and cell therapies. Both are actively integrating technical approaches such as proteomics, AI algorithms, and CRISPR screening to facilitate the efficient translation of basic research into drug development.

In terms of differences, leading international research institutions and pharmaceutical companies leverage global resources to secure earlier positions in high-barrier targets such as KRAS, BCL6, and SMARCA2/4, while extending into future technologies like PROTACs and CRISPR-based therapies. Chinese institutions initially focused on the path of "domestic substitution," entering the market through mature targets such as PD-(L)1. In recent years, they have shifted toward exploring differentiated antigens like CDH17 and GPC3, as well as AI-driven target screening, forming a combined strategy of "domestic accessibility + localized breakthroughs." Furthermore, multinational corporations promote simultaneous global development, whereas Chinese teams center on the local market, gradually aligning with international standards and clinical trial networks.[38]。

Overall, the R&D systems in China and abroad are increasingly converging in terms of target layout and technology adoption, yet they differ in strategic focus: international institutions emphasize systematic approaches and breadth, while Chinese teams leverage speed and flexible mechanisms to accelerate differentiated innovation, building a dual-path framework of “catching up” and “breaking through.”

Part III: The Global Landscape of AI-Enabled Oncology Research

3.1 Regional and Institutional Profiles

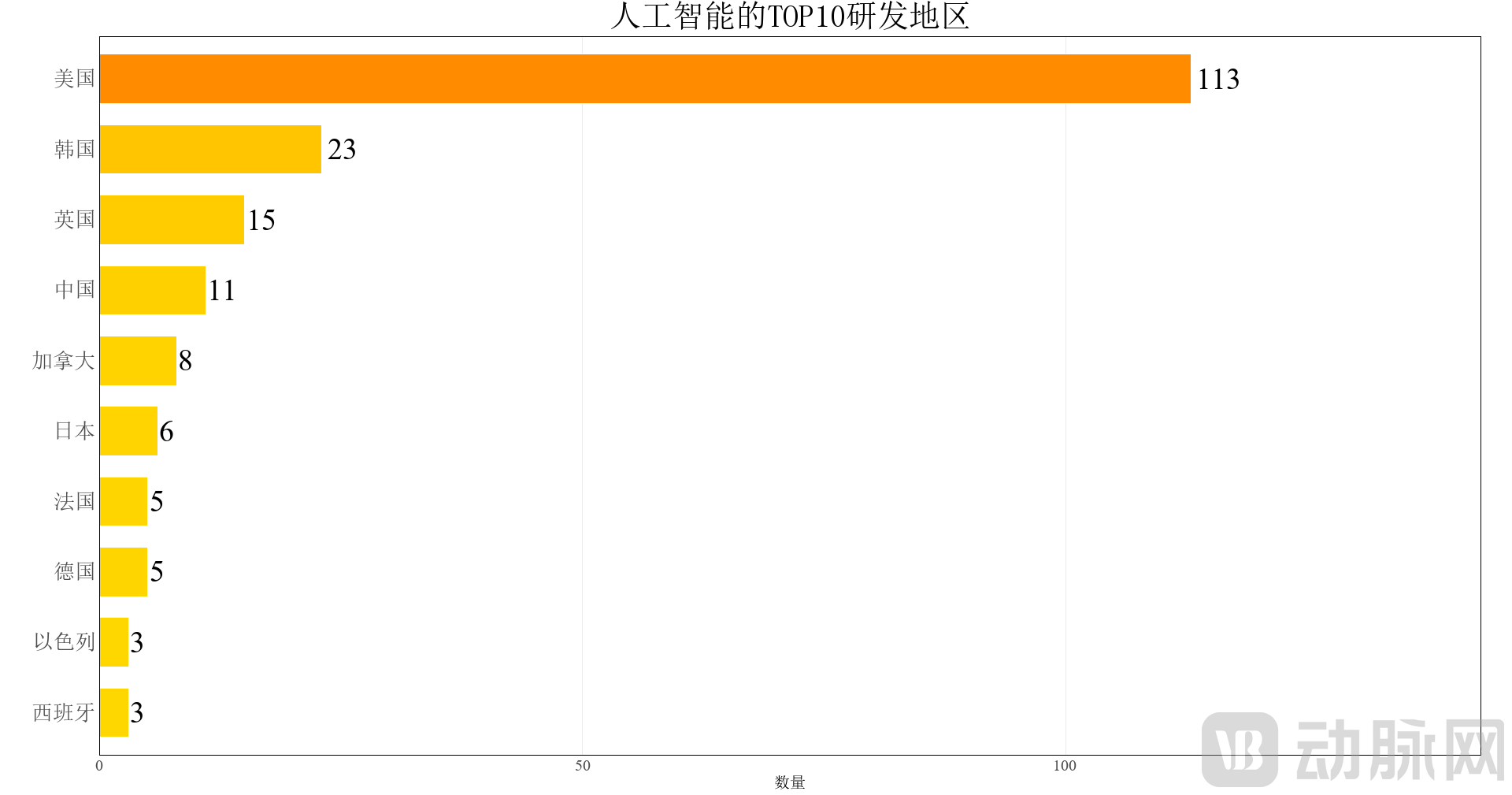

At the AACR 2025 Annual Meeting, research presentations highlighted artificial intelligence (AI) as a key technological engine driving precision oncology. Overall, the United States maintains an absolute lead in AI-driven cancer research, with a total of 113 related abstracts published, accounting for more than half of the global total. This continues its dominant position in traditional target development and institutional output.[39]South Korea (23 papers) and the United Kingdom (15 papers) ranked second and third, respectively, reflecting the growing policy support and R&D investment in AI healthcare technologies by Asian and European countries. China ranked fourth with 11 papers; compared to its regional share in traditional oncology research (21.9% in Asia), there is still significant room for improvement in the AI field.

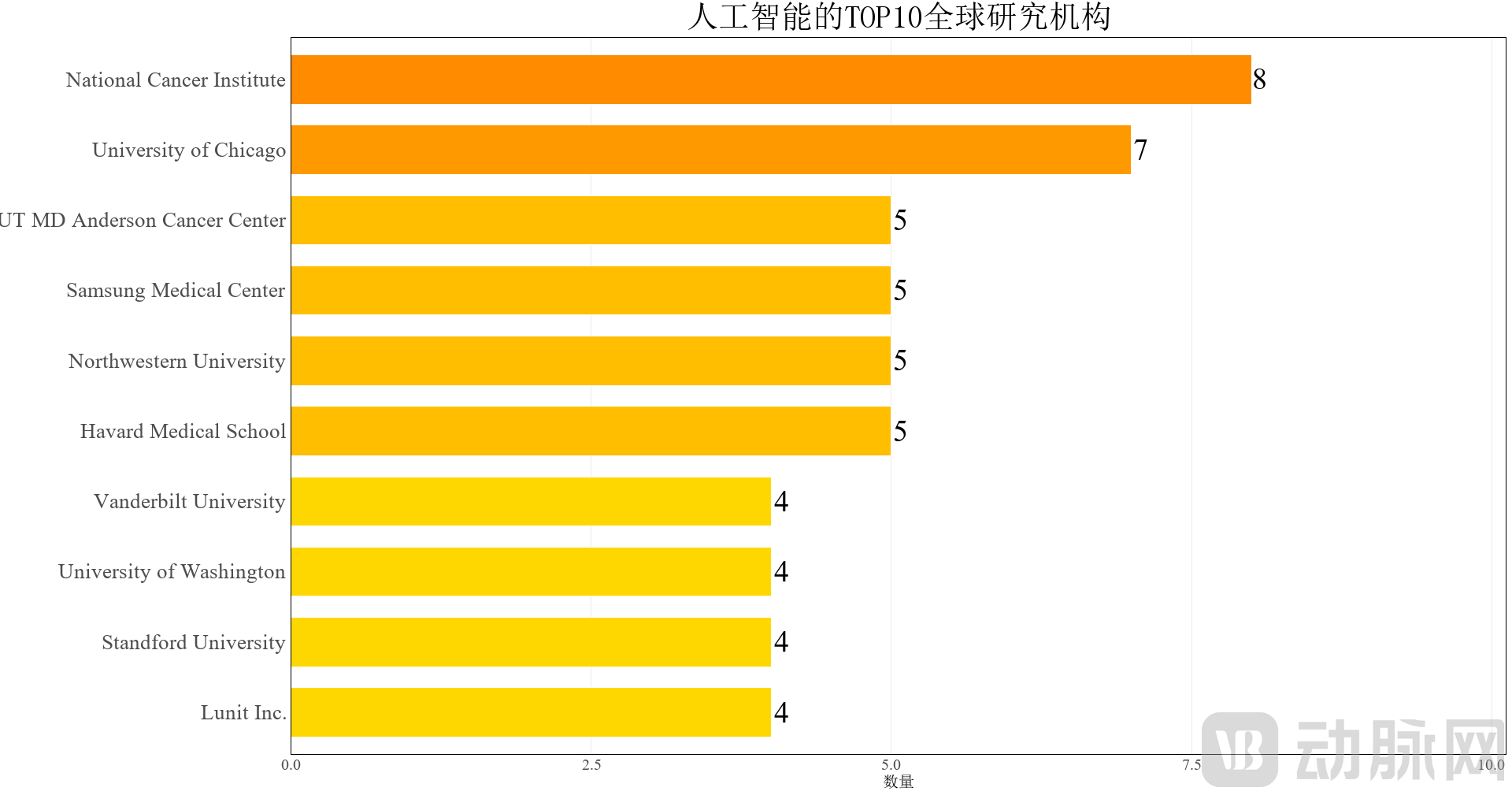

In terms of institutions, the U.S. National Cancer Institute (NCI, 8 papers) and the University of Chicago (7 papers) are the most prolific contributors to AI-driven oncology research, maintaining their high level of activity in traditional immune target research. MD Anderson Cancer Center and Samsung Medical Center demonstrate the multimodal integration capabilities of clinical institutions in data-driven medicine: the former established the Institute for Data Science in Oncology (IDSO), developing a deep learning-based automated HER2 scoring system and an AI model for lung cancer prognosis.[40], while the latter has partnered with KAIST to build an AI digital pathology platform and advance multimodal imaging research, covering core disease areas such as the respiratory and digestive systems.[41]. These institutions share the common characteristics of possessing highly structured medical data and multidisciplinary collaboration mechanisms, providing a solid foundation for the clinical translation of AI models.

Source: Compiled from the AACR 2025 Annual Meeting website and data from PharmCube.

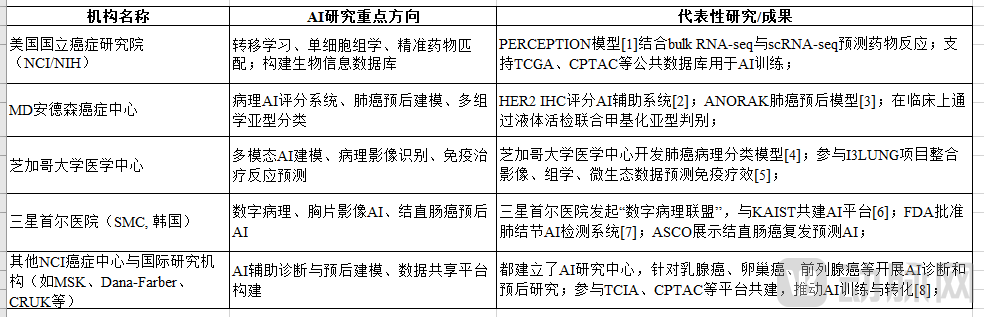

Table: Cases of AI R&D Layout by Leading Institutions in the Past Three Years

Source: Compiled from information on the AACR 2025 conference website, the National Cancer Institute, PubMed, and institutional websites.

3.2 Focus on Disease Areas

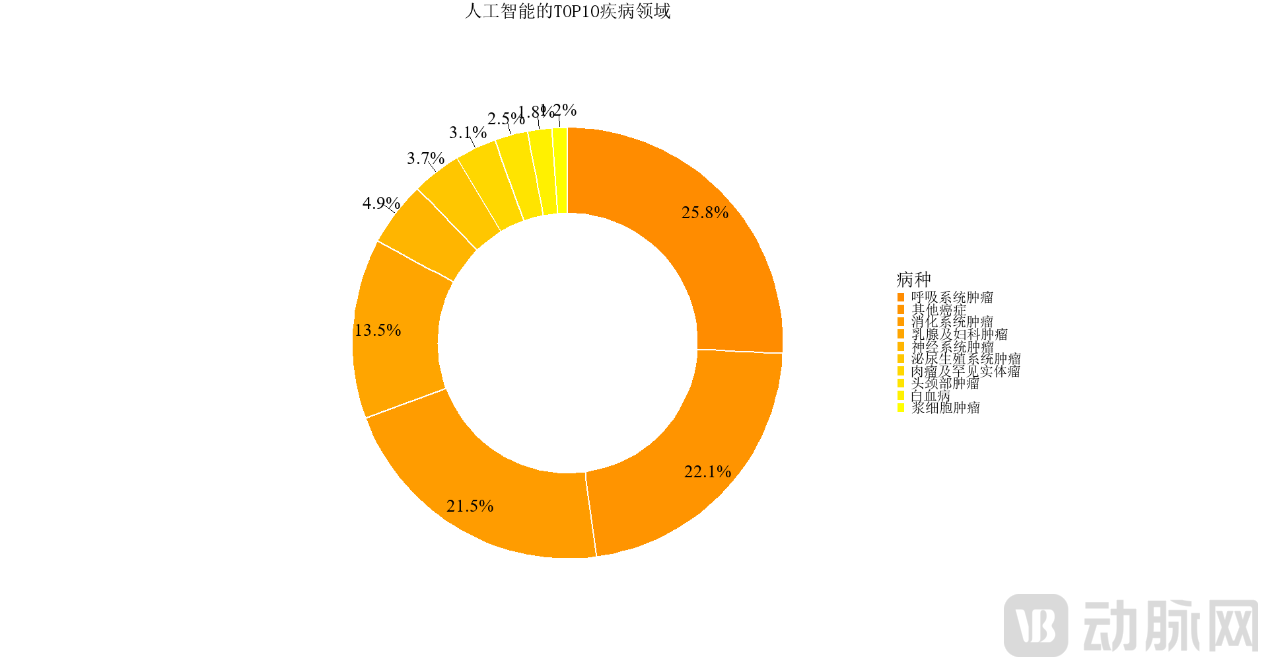

In disease research, AI applications are concentrated on high-incidence cancer types: respiratory system tumors rank first (25.8%), aligning with the high prominence of NSCLC in traditional research (16.1%); digestive system tumors (21.5%) are closely associated with high tumor mutational burden cancers such as colorectal and pancreatic cancer; although breast and gynecological tumors (13.5%) account for a slightly lower proportion than in traditional research (26.8%), the clinical implementation of AI-assisted systems, such as HER2 expression scoring, indicates that AI adoption in this field is still in a phase of accelerated penetration.

Source: Compiled from data by PharmaCube based on information from the AACR 2025 Annual Meeting website.

3.3 Characteristics of AI Research Targets

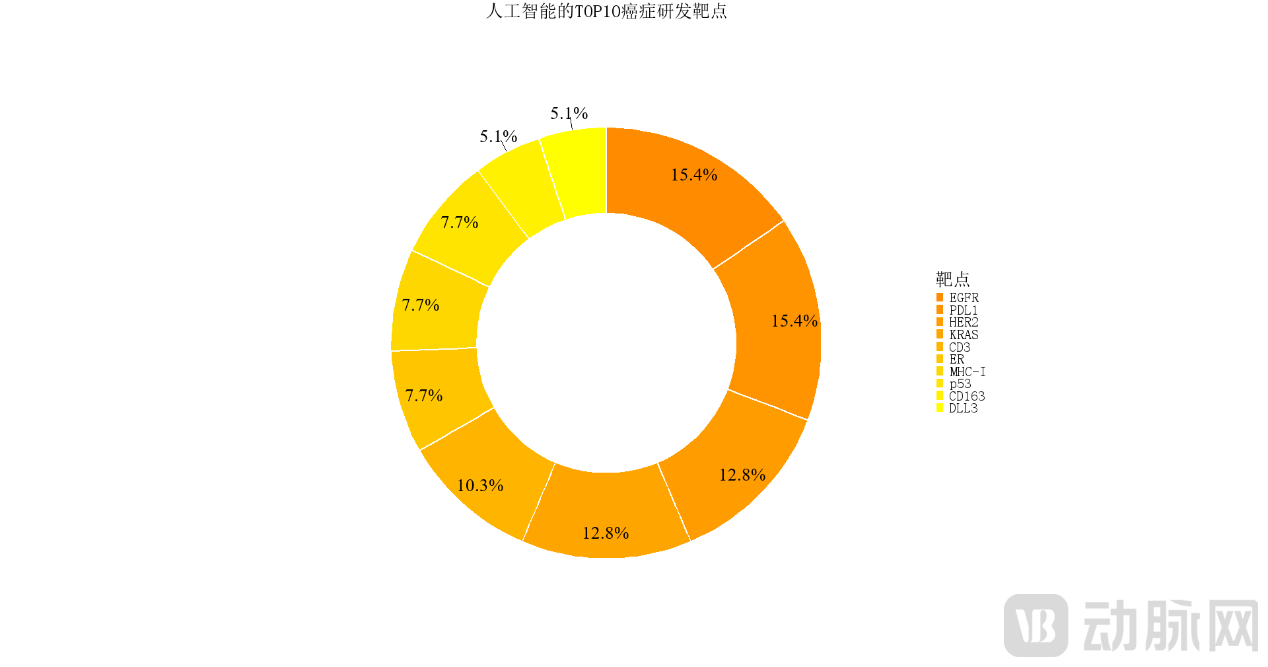

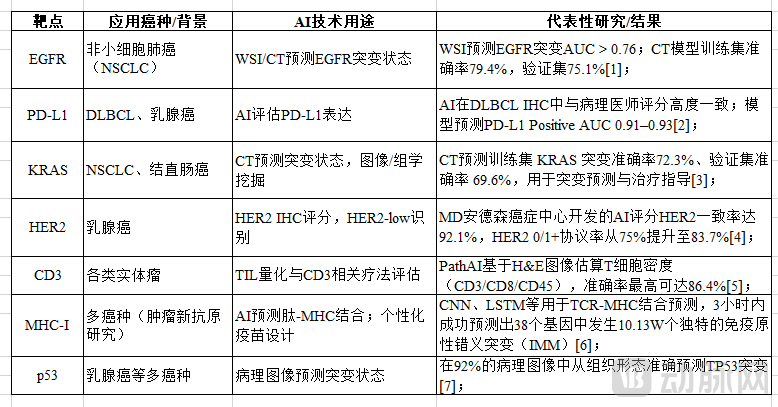

At the target level, AI research has focused most heavily on EGFR and PD‑L1 (both at 15.4%), aligning closely with the traditional research hotspots identified in Sections II and III. This indicates that AI tools are being leveraged to enhance phenotypic recognition and therapeutic efficacy prediction for these classic targets. AI applications are also active in HER2 and KRAS (each at 12.8%), particularly in lung cancer and colorectal cancer, where deep learning models are employed for non-invasive prediction of gene mutation status.[40,42]Furthermore, the significant rise in immune-related targets such as CD3 (10.3%) and MHC-I (7.7%) marks AI’s expanding capabilities in modeling the tumor immune microenvironment and exploring antigen presentation mechanisms. The emergence of less common targets like DLL3 (5.1%) suggests that AI is being utilized for the discovery of rare targets and identification of patient subpopulations, thereby supporting the early development of emerging therapies such as BiTEs or CAR-T cells.[43]。

Table: Top 10 AI R&D Cases for Drug Targets

Source: Compiled from information on the AACR 2025 conference website, as well as the PMC and PubMed literature databases.

In summary, AI’s presence in oncology research at AACR 2025 has permeated multiple levels, encompassing mainstream institutions, core therapeutic targets, and high-incidence cancer types. Current AI models primarily integrate multi-omics data, pathological imaging, and clinical information to achieve quantitative assessment of complex biological features and molecular phenotypes, enable stratified prediction of disease characteristics, and promote cross-learning and intelligent synergy across multimodal data. Compared with traditional approaches, AI empowerment is driving the evolution of cancer therapeutics and drug development toward a paradigm of “precise target discovery plus intelligent clinical matching.” Its penetration into key areas such as early cancer prediction, patient selection, and precision treatment will reshape future models of clinical oncology research and drug development.

In summary, global oncology drug R&D has entered an era driven by the triad of “targets + platforms + intelligence.” The landscape has evolved from a target profile dominated by solid tumors to differentiated explorations of new technology platforms by multinational pharmaceutical companies and research institutions. Meanwhile, Chinese pharmaceutical companies have progressed from domestic substitution to achieving breakthroughs in innovative targets, while AI technology has empowered and reshaped both classic and emerging targets. By 2025, the oncology research ecosystem has exhibited characteristics of systemic transformation.

In the future, the “pan-systemic” nature and “system-specific” characteristics of therapeutic targets will jointly form the main axis of clinical strategies. Institutional collaboration will accelerate the closed-loop efficiency from basic research to translational applications. The integration of AI and multi-omics will become an indispensable computational engine for oncology research. This report aims to provide the industry with robust data analysis and trend interpretation, empowering various stakeholders to make forward-looking decisions and establish strategic positioning in target selection, technology planning, and international collaboration.

Zhang Hongyu

Ph.D. Candidate in Biological and Pharmaceutical Engineering, Zhejiang University

Sun Yat-sen University, Master of Management

Master of Finance, Grenoble École de Management (Government-Sponsored Study Abroad)

Personal Profile: Ph.D. candidate in Biomedical Engineering at Zhejiang University, specializing in AI-assisted precision oncology screening and drug design and development; previously worked within Ping An Group, Hengjian Financial Holdings, and GF Securities, engaging in primary equity and debt investment and financing for biotechnology and healthcare institutions. Possesses an interdisciplinary background spanning AI, precision medicine, and finance, with dual perspectives on cutting-edge medical R&D and capital operations. Focuses on AI-enabled precision medicine and new drug development, emphasizing technology transfer and market application. (WeChat ID: 18927501292)