PeptiGrowth Biopharma Goes Public on HKEX with Lead GLP-1 Drug Nearing Commercialization

PegBio

Developer of Innovative Therapies for Chronic Diseases

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

YuanBio Venture Capital

Venture Capital Institution

Today, PegBio, a developer of innovative therapies for chronic diseases, listed on the Hong Kong Stock Exchange.

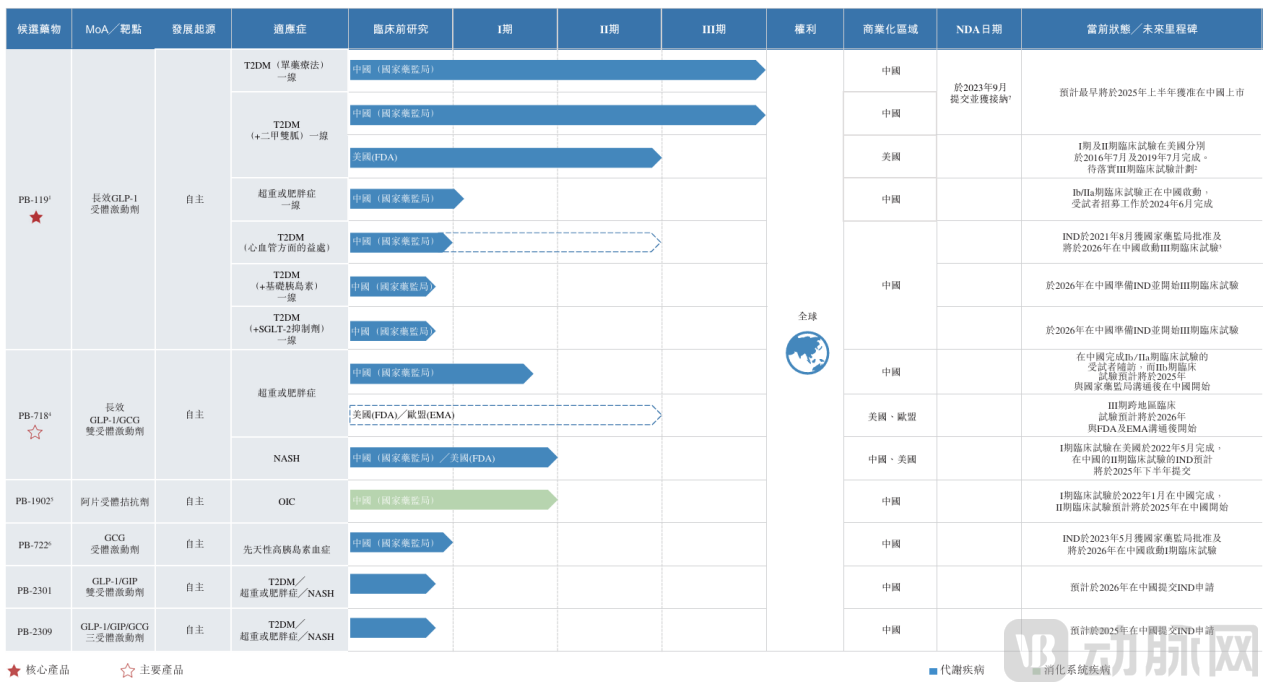

PegBio focuses primarily on the field of metabolic disorders. The company’s core product, the GLP-1 receptor agonist PB-119 (pegbinepatide injection), is expected to be launched in 2025 and is mainly indicated for first-line treatment of type 2 diabetes mellitus (T2DM) and obesity. Meanwhile, PegBio has also laid out five additional drug candidates in therapeutic areas including T2DM, overweight or obesity, non-alcoholic steatohepatitis (NASH), and congenital hyperinsulinism.

In the hotly contested T2DM and weight loss sector, PegBio is a star project in the primary market. The prospectus shows that before its IPO, PegBio completed nine rounds of financing between 2008 and 2023, with investors including YuanBio Venture Capital, Tigermed, Fujian Yingke Venture Capital, Qianhai, Legend Capital, and other well-known institutions and enterprises.

Previously, PegBio had submitted an IPO application to the STAR Market, but later shifted its listing venue to the Hong Kong Stock Exchange due to adjustments in its product R&D strategy and global business expansion. Now, as a company without any commercialized products generating revenue, PegBio has successfully achieved its IPO through Chapter 18A of the Hong Kong Stock Exchange Listing Rules.

The weight loss market is visibly booming, driven on one hand by robust consumer demand for healthy weight management solutions, and on the other by the high prevalence of obesity—a major risk factor for chronic conditions such as cardiovascular and cerebrovascular diseases, diabetes, and certain cancers. In response, the Chinese government has launched the “Year of Weight Management,” advocating for weight reduction through policy guidance.

However, market enthusiasm coexists with fierce competition. How will PegBio respond to the impending intense battle?

Although PegBio has not yet generated commercial revenue from its products, its core product is on the verge of regulatory approval for market launch.

Currently, PegBio has established a diversified pipeline comprising six candidate products, focusing on the treatment of common chronic and metabolic diseases such as type 2 diabetes mellitus (T2DM), overweight or obesity, non-alcoholic steatohepatitis (NASH), opioid-induced constipation (OIC), and congenital hyperinsulinism. The product pipeline is primarily centered around GLP-1, aiming to provide safe, effective, accessible, and convenient therapies with multiple benefits for patients with chronic and metabolic diseases.

PegBio’s Product Pipeline, Image Source: Prospectus

Among them,PB-119 is PegBio’s flagship product. As a long-acting GLP-1 receptor agonist, it is primarily indicated for first-line treatment of type 2 diabetes mellitus (T2DM) and obesity.

In early 2023, PB-119 completed two Phase III registrational clinical trials in China, including monotherapy and combination therapy for type 2 diabetes mellitus (T2DM); in September 2023, the National Medical Products Administration (NMPA) accepted the New Drug Application (NDA) for PB-119.

According to the prospectus, PB-119 is expected to receive NDA approval in 2025 for the treatment of type 2 diabetes mellitus (T2DM) and will be commercialized in China. Meanwhile, Phase Ib/IIa clinical trials of PB-119 for the treatment of obesity have been initiated, with subject enrollment completed in June 2024. PB-119 features a single-dose regimen without the need for dose titration, owing to its favorable safety profile and its ability to deliver rapid, significant, and sustained efficacy at relatively low doses.

In addition to type 2 diabetes mellitus (T2DM) and obesity, PegBio will explore the therapeutic potential of PB-119 in combination therapies to further expand its indications. For example, PegBio plans to initiate two additional Phase III clinical trials in China to evaluate PB-119 in combination with basal insulin or with SGLT-2 inhibitors; the Investigational New Drug (IND) applications for these two trials are currently being prepared. The company also plans to launch a Phase III clinical trial of PB-119 in China in 2026 to assess cardiovascular outcomes in patients with T2DM.

As PegBio's flagship product, PB-718 is a novel long-acting dual GLP-1/GCG receptor agonist primarily indicated for the treatment of obesity and NASH.

By simultaneously activating the GLP-1 receptor and the glucagon (GCG) receptor, PB-718 is designed to achieve synergistic effects that surpass the efficacy of either receptor agonist alone, characterized by significant weight loss and appetite suppression. Preliminary study results indicate that PB-718 can reduce lipid accumulation in the liver, thereby preventing hepatic inflammation and subsequent liver fibrosis. Currently, PB-718 has completed patient follow-up for its Phase Ib/IIa clinical trial in China for the treatment of obesity.

Meanwhile, PegBio has also developed PB-2301, a dual GLP-1/GIP receptor agonist, and PB-2309, a triple GLP-1/GIP/glucagon receptor agonist, for the treatment of type 2 diabetes mellitus (T2DM), overweight or obesity, and non-alcoholic steatohepatitis (NASH); both candidates are currently in the preclinical research stage.

Certainly, PegBio’s product pipeline is not limited to GLP-1. For instance, the company is developing PB-1902, an oral selective opioid receptor antagonist for the treatment of opioid-induced constipation (OIC), which aims to effectively alleviate opioid-induced gastrointestinal dysfunction without compromising the central analgesic effects of opioids. Another candidate, PB-722, a glucagon (GCG) receptor agonist for the treatment of congenital hyperinsulinism, has received FDA Orphan Drug Designation and has demonstrated its safety profile in various animal models.

In terms of technical platforms, PegBio has established an efficient target screening and molecular modifier platform, which includes three major functions: metabolic disease data collection, drug molecule design platform, and compound screening platform. Among them,The drug molecule design platform features polyethylene glycol (PEG) technology, which extends the half-life of compounds, enhances long-acting efficacy, improves compound stability, reduces immunogenicity, and lowers research costs.

Benefiting from this platform and PEG technology, the half-lives of the core product PB-119 and the main product PB-718 are extended, enabling a once-weekly dosing regimen to enhance patient convenience and adherence.

PegBio’s diversified product pipeline and efficient technology platform enable the company to not only cover the T2DM and weight-loss markets but also seize market opportunities in a broader range of chronic disease therapeutic areas.

As its core product PB-119 nears the commercialization stage, PegBio has also initiated its commercialization efforts.

The prospectus disclosed that in September 2024, PegBio entered into a commercialization partnership with a domestic pharmaceutical company for the Chinese mainland market.During the commercialization phase, PegBio will face direct competition from multiple drugs in the same class or with the same indications.

As of February 2025, there are 15 GLP-1 drugs approved in China for the treatment of type 2 diabetes mellitus (T2DM), and six drugs indicated for obesity. Among these, semaglutide and tirzepatide have established significant market influence.

GLP-1 Drugs Marketed in China for the Treatment of T2DM, Source: PegBio Prospectus and Public Corporate Information

Drugs Marketed in China for the Treatment of Obesity, Source: PegBio Prospectus and Public Corporate Information

Meanwhile, a cohort of drugs under development is on the verge of an explosion in successful outcomes.

According to incomplete statistics, as of February 2025, 20 GLP-1 drugs for T2DM have had their NDAs accepted or are undergoing Phase III clinical trials in China; NDAs for six GLP-1/GCG dual receptor agonists and other drugs with different mechanisms of action for T2DM have been accepted.

Regarding obesity medications, as of February 2025, there were more than 50 clinical-stage candidate drug pipelines in various forms in China. Among these, approximately 20 GLP-1 drugs were in the clinical development stage, along with three GLP-1/GCG dual receptor agonists.

Whether for the T2DM indication or the obesity indication, the intensity of competition at present and in the future is evident.

From a commercialization perspective, GLP-1 drugs for the type 2 diabetes mellitus (T2DM) indication focus on the in-hospital market through inclusion in the National Reimbursement Drug List. In contrast, weight-loss indications have not been approved for reimbursement; given the strong consumer-oriented nature of this segment, the focus is primarily on the out-of-hospital market (mainly referring to settings outside public medical institutions).

Currently, weight-loss medications have been rolled out across all channels outside hospitals. Offline, they are available in non-public medical institutions such as clinics, outpatient departments, and health examination centers. Online, mainstream pharmaceutical e-commerce platforms collaborate with medical institutions nationwide to open online appointment channels; patients can visit the corresponding facilities for consultation, medication pickup, and injection after making an appointment. Furthermore, online platforms partner with offline institutions to offer weight management packages that, in addition to the medications themselves, provide related laboratory tests and examinations, full-cycle weight management counseling, and nutritional products. Moreover, some GLP-1 weight-loss drugs have incorporated aesthetic medicine clinics into their marketing networks.

Overall, weight-loss drugs are expanding into various consumer healthcare scenarios across both online and offline channels, collaborating with medical institutions, internet healthcare and pharmaceutical platforms, and other stakeholders to jointly enhance market penetration; in this process, pharmaceutical companies are strengthening their brand influence through differentiated marketing strategies.

Facing the impending intense competition, PegBio has initially established its commercialization pathway.

The clinical value of a product is naturally its most fundamental competitive advantage.PegBio’s products offer comprehensive clinical benefits, including rapid, significant, and sustained efficacy; reduced dosing frequency and improved patient adherence; ease of use without the need for dose titration; and broad applicability across diverse patient populations.

PegBio disclosed in its prospectus that the pharmaceutical company with which it has entered into a commercialization partnership is an A-share listed company. Its business covers major domestic markets and provinces, including first-tier cities such as Beijing, Shanghai, and Guangzhou, as well as other key cities, and it has accumulated extensive experience in chronic and metabolic diseases. The company’s direct sales channel covers a large number of pharmacies nationwide, providing access to a broad network of terminal retail pharmacies across China. Therefore,Our partner’s marketing network can help PegBio’s core product, PB-119, achieve rapid market penetration.

Price is another key factor in market competition.PegBio stated in its prospectus that it plans to price PB-119 at a competitive level.This is primarily because the manufacturing process for PB-119 significantly reduces production costs while ensuring product quality. Additionally, PB-119 demonstrates efficacy at relatively low dose levels, enabling the company to adopt competitive pricing strategies and expand into underdeveloped regions of China and other emerging markets, thereby providing affordable medication to more price-sensitive patients.

Furthermore, PegBio plans to strive for inclusion in the National Reimbursement Drug List with appropriate pricing, thereby further enhancing product accessibility.

It is evident that PegBio has made preparations for its layout in both in-hospital and out-of-hospital channels. According to the use of proceeds disclosed in the prospectus, half of the funds raised from the IPO will be allocated to the commercialization and indication expansion of its core product, PB-119.

PegBio’s target market extends beyond China to include the vast overseas markets.

As early as 2021, PegBio submitted an IPO application to the STAR Market and subsequently responded to two rounds of inquiries from the Shanghai Stock Exchange. However, the STAR Market listing application was withdrawn in April 2022, and in 2023, the company shifted its listing destination to the Hong Kong Stock Exchange.

In response, PegBio stated in its prospectus that the aforementioned changes were primarily driven by its latest corporate strategy focusing on product research and development, leading to the voluntary withdrawal of its A-share listing application. To further expand the Company’s global business and considering that the Hong Kong Stock Exchange offers an international platform for accessing foreign capital and attracting a diverse base of overseas investors, the Company voluntarily decided to pursue a listing in Hong Kong.

From the perspective of overseas R&D progress, PegBio has achieved certain phased milestones.For example, the core product PB-119 has completed Phase II clinical trials in the United States for the treatment of type 2 diabetes mellitus (T2DM); the main product PB-718 has completed Phase I clinical trials in the United States for the treatment of non-alcoholic steatohepatitis (NASH); and the Phase III multinational clinical trial of PB-718 for overweight or obesity is expected to commence in 2026 following consultations with the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

The global T2DM and obesity market remains fiercely competitive.

On one hand, Novo Nordisk and Eli Lilly have formed a “duopoly in weight-loss drugs,” with their product revenues continuously hitting new highs.

In the first quarter of 2025, sales of Novo Nordisk’s weight-loss drug Wegovy reached DKK 17.36 billion (approximately USD 2.63 billion), a year-on-year increase of 85%; sales of its diabetes drug Ozempic reached DKK 32.721 billion (approximately USD 4.954 billion), a year-on-year increase of 18%.

During the same period, Eli Lilly’s diabetes formulation of tirzepatide, Mounjaro, and its weight-loss formulation, Zepbound, generated sales revenues of $3.84 billion and $2.31 billion, respectively, representing year-on-year growth of 113% and 346%.

Even so, the “duopoly” has lowered its overall performance expectations for 2025 in the face of increasingly fierce market competition.

On the other hand, among other companies that have globally deployed GLP-1 and other forms of weight-loss drugs, most are large multinational pharmaceutical corporations with strong R&D and financial capabilities, as well as robust internal commercialization teams, giving them significant competitive advantages.

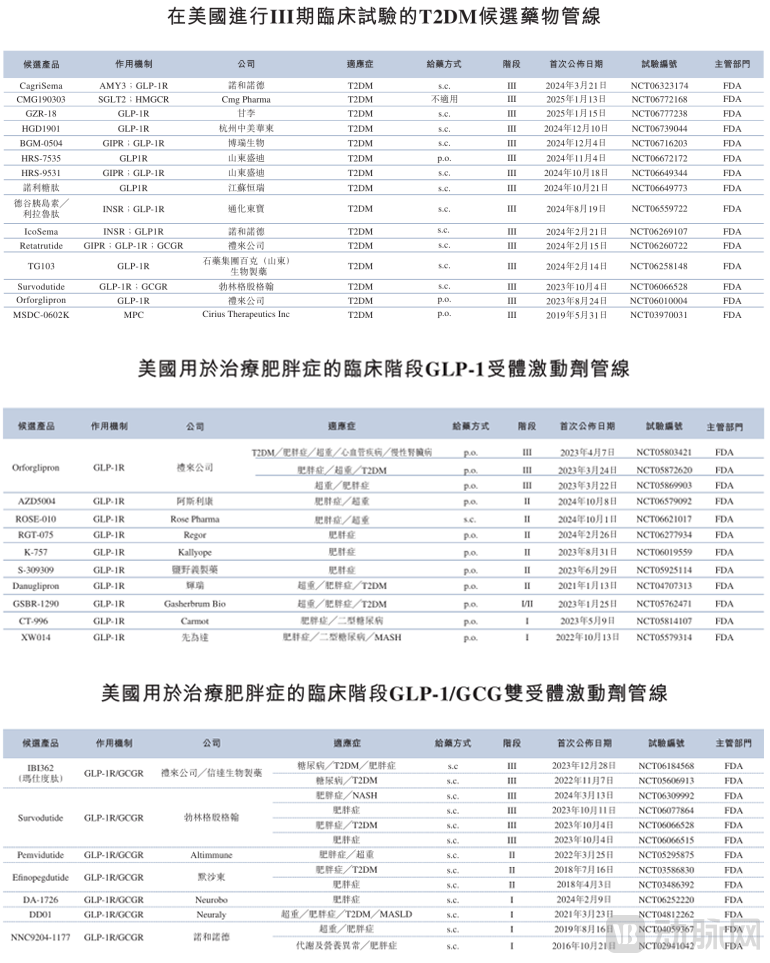

In addition to marketed products such as semaglutide, tirzepatide, and liraglutide, a large number of GLP-1 receptor agonists, GLP-1/GCG dual receptor agonists, and other products with different mechanisms of action remained in clinical development in the United States as of 2025.

T2DM and Obesity Therapeutics in R&D in the United States, Image Source: PegBio Prospectus

In overseas markets, PegBio plans to unlock the value of its assets through commercial collaborations with local partners.For example, to facilitate the development and commercialization of its core products, PegBio plans to finalize its clinical development strategy in the United States and collaborate with local partners to conduct Phase III clinical trials of PB-119 for the treatment of type 2 diabetes mellitus (T2DM). Following the completion of these Phase III trials, the company intends to formulate a detailed commercialization plan for PB-119 in the U.S. market.

Meanwhile, PegBio also plans to explore overseas markets in Belt and Road Initiative (BRI) countries, including those in the Middle East and South Asia, while continuously assessing local commercial prospects and regulatory requirements.

Numerous pharmaceutical companies are investing in the research and development of drugs for type 2 diabetes mellitus (T2DM) and obesity, aiming to provide more beneficial treatment regimens for the vast patient population. Amidst fierce market competition, these companies must also pursue innovation across all stages—including R&D, manufacturing, and marketing—to better balance pricing and profitability while controlling costs.

After a prolonged R&D period, PegBio is on the verge of commercialization, with IPO proceeds providing ample financial support for its commercial launch and subsequent research and development.Following the launch of its core product, it will be worth watching how PegBio enhances product accessibility at competitive prices and provides affordable medications to a broad patient base, as stated in its prospectus.