Shouhui Group, a Rising Star in Health Insurance, Goes Public with Nearly RMB 4 Billion Revenue Over Three Years

Another Listed Company Joins the Online Insurance Intermediary Industry!

On May 30, Shouhui Group Co., Ltd. officially listed on the Hong Kong Stock Exchange under the stock code “2621.HK.” At the close of trading that day, the company’s share price stood at HK$6.61 per share, representing a decline of 18.19% and falling below its initial public offering price of HK$8.08 per share. Its total market capitalization reached HK$1.496 billion.

Founded in 2015, Shouhui Group is a Chinese life insurance intermediary service provider dedicated to offering online insurance solutions to policyholders and insured individuals through its life insurance transaction and service platform.

According to Frost & Sullivan, based on the total premiums of long-term life insurance in 2023, Shouhui Group is the second-largest online insurance intermediary service provider in China, holding a 7.3% market share; based on the first-year premiums of long-term life insurance in 2023, Shouhui Group is also the second-largest online insurance intermediary service provider in China.

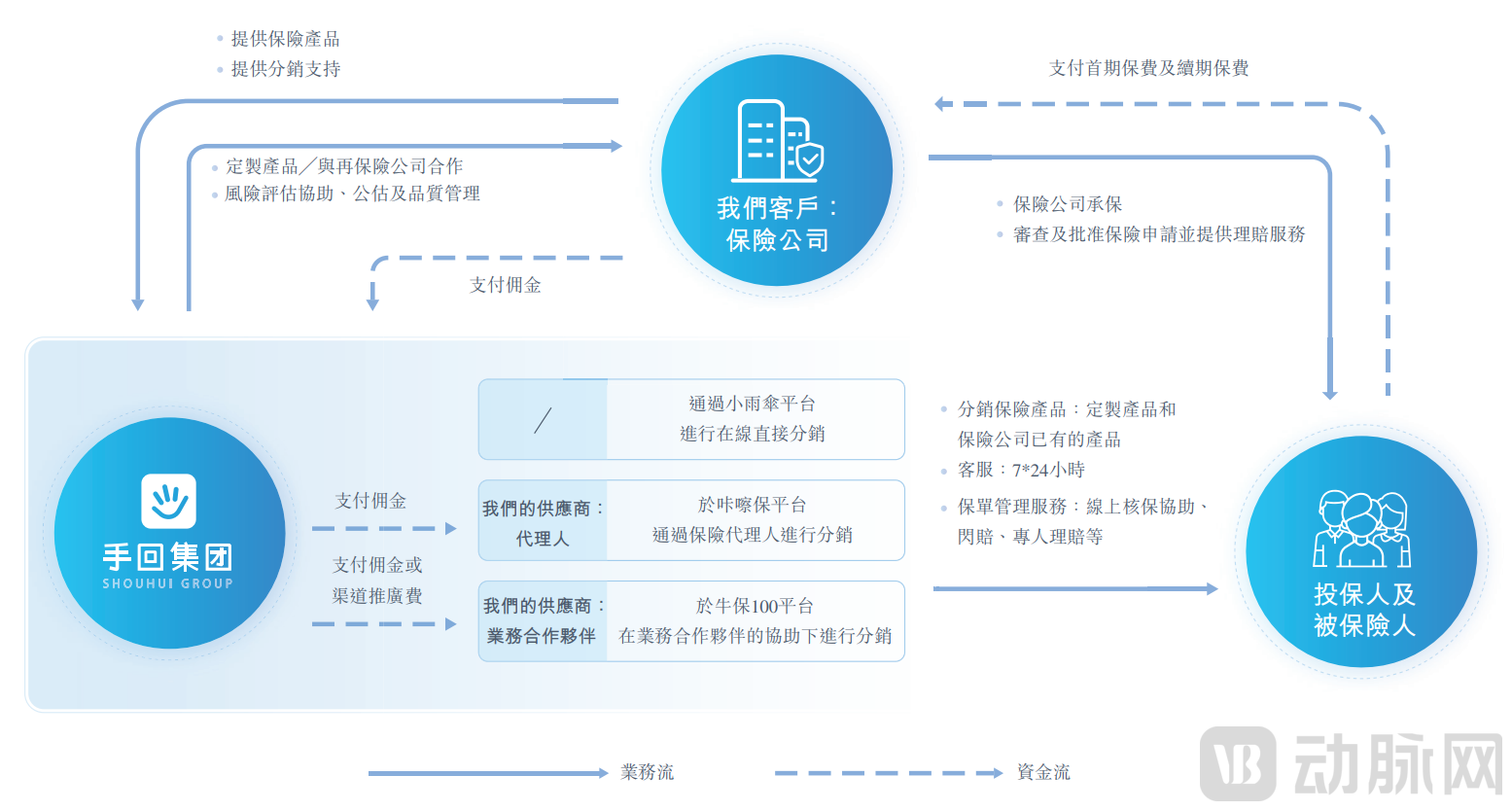

Shouhui Group’s digital transaction and service solutions for individual life insurance are distributed through three channels facilitated by its three major platforms: Xiaoyusan, Kacha Bao, and Niubao 100. These include online direct distribution via the Xiaoyusan platform, agent-based distribution through the Kacha Bao platform, and distribution with the assistance of business partners on the Niubao 100 platform.

As of December 31, 2024, Shouhui Group had partnered with over 110 insurance companies, distributing more than 1,900 products (including 280 customized products), cumulatively serving 3.5 million policyholders and covering over 5.8 million insured individuals, while incubating 14 proprietary IPs. As of the same date, 1.6 million policyholders and 2.4 million insured individuals held valid policies issued by the company.

Business Structure of Shenzhen Muchenglin Technology Co., Ltd. Source: Screenshot from the prospectus

Business Structure of Shenzhen Muchenglin Technology Co., Ltd. Source: Screenshot from the prospectus

In terms of revenue, according to the prospectus, the company’s operating revenues from 2022 to 2024 were RMB 806 million, RMB 1.634 billion, and RMB 1.387 billion, respectively. During the same period, Shouhui Group’s gross profit margins were 34.8%, 33.8%, and 38.1%, respectively; its adjusted net profits were RMB 75 million, RMB 253 million, and RMB 242 million, respectively, with adjusted net profit margins of 9.3%, 15.5%, and 17.4%, respectively.

During this period, Muchenglin Group received investments from renowned institutions including Xintian Venture Capital, Sequoia China, Matrix Partners China, Tasly, and Noah Holdings.

China’s online insurance intermediary market has exhibited rapid growth in recent years. According to Frost & Sullivan, the market size of China’s life insurance intermediaries reached RMB 237 billion in 2023, with the share of online channels continuing to rise. The online life insurance market is projected to surpass RMB 2 trillion by 2028, representing a compound annual growth rate (CAGR) of 29.7%. However, this sector faces multiple structural challenges, which Shenzhen Muchenglin Technology Co., Ltd. cannot avoid as a participant in the market.

Policy Compliance Curbs Wild Profit Growth.“Alignment of Reported and Actual Practices” Policy

As an online life insurance intermediary, Shouhui Group’s revenue is primarily derived from commissions paid by insurance companies as a percentage of premiums. The “integration of reporting and banking” policy has led to a significant decline in first-year commission rates for intermediary platforms, driving down the overall average first-year commission rate across various insurance products from 34.8% in 2022 to 26.2% in 2024. Specifically, the average first-year commission rate for long-term life insurance products decreased from 34.6% in 2022 to 21.5% in 2024, while that for long-term health insurance and other products dropped from 40.6% to 30.3%. This has placed considerable pressure on the profitability of its core business.

Squeezed by Traffic Giants.Traditional insurance companies are accelerating the development of their own online channels, while internet giants such as Tencent’s WeSure and Ant Group’s Ant Insurance leverage the massive traffic entry points of WeChat and Alipay to precisely reach users through social and payment scenarios, thereby seizing market share. Faced with fierce competition from both established incumbents and disruptive tech players, Muchenglin Group has attempted to drive traffic through content marketing on platforms like Douyin and Xiaohongshu via its subsidiaries, including Xiao Yu San, Kacha Bao, and Niu Bao 100. However, its overall traffic volume and user coverage remain relatively limited, necessitating greater resource allocation for traffic acquisition and marketing promotions, which results in high customer acquisition costs. This is evident from the prospectus: in 2024, Muchenglin Group’s promotional expenses reached RMB 322 million, accounting for 23.2% of its total revenue.

A single business model creates a growth bottleneck.Reliance on commission income is a “common ailment” among insurance intermediaries. Shenzhen Muchenglin Technology Co., Ltd. derives over 99% of its revenue directly from insurance transaction commissions, with technical service revenue accounting for less than 1%. On one hand, excessive dependence on a single business line makes the company vulnerable to policy changes and market fluctuations; even slight variations in commission rates can significantly impact financial performance. On the other hand, while the company’s technical services—such as Flash Claims and Intelligent Underwriting—demonstrate a degree of innovation, they have not yet formed a second growth curve due to limitations in their business model and R&D investment. Although insurance technical service revenue grew by 61.6% year-on-year in 2024, the absolute amount remained below RMB 10 million, having no substantive effect on the overall revenue structure.

This extreme business skew can be largely attributed to two factors. First, limitations in the business model: Shenzhen Muchenglin Technology Co., Ltd.’s technology investments primarily serve its internal operations, such as optimizing platform user experience and improving commission collection efficiency, rather than extensively exporting technical capabilities to external parties, resulting in a lack of external commercialization. Second, insufficient investment in R&D resources: In 2024, R&D expenses amounted to RMB 48 million, accounting for 3.5% of revenue, which prevented the scaling of its technology services.

Returning to the core business, Muchenglin Group should be well aware of its shortcomings. Breaking free from the shackles of commission dependency and seeking new growth drivers have become its core strategies.

Shenzhen Muchenglin Technology Co., Ltd. offers the solution of “customization capabilities + scenario-based coverage.”

In terms of customization, Shouhui Group has adopted a dual-pronged strategy of deep collaboration and in-house IP incubation. As of December 31, 2024, Shouhui Group had partnered with over 110 insurance companies, covering more than 70% of life insurers in China. It has cumulatively distributed over 1,900 products, including more than 280 customized offerings. Currently, there are 306 products on sale, and the company has successfully incubated over 14 IPs. Through joint development with insurance companies, its customized products span various categories, including long-term life insurance, long-term critical illness insurance, long-term medical insurance, other long-term insurance, and short-term insurance.

For instance, the high-value flagship child accident insurance product “Xiao Wan Tong No. 6,” targeted at young families, has garnered significant attention. Similarly, the Super Mary critical illness insurance series has distributed approximately 330,000 policies, with cumulative total premiums reaching RMB 3.6 billion and first-year premiums amounting to RMB 573 million from 2022 to 2024.

In terms of scenario-based coverage, Shouhui Group leverages its platforms—Xiaoyusan, Kacha Bao, and Niubao 100—to reach both B-end and C-end customers. Meanwhile, it is actively pursuing external collaborations to build an “Insurance + Health” ecosystem. By enhancing service value-added offerings to break free from reliance on commissions, the group aims to transform its role from a “traffic intermediary” to a “service enabler.”

In April 2025, Shenzhen Muchenglin Technology Co., Ltd. (Muchenglin Group) and Distinct HealthCare officially signed a strategic cooperation agreement. The two parties will jointly develop customized “healthcare + insurance” products, integrate their online and offline medical resources, and create cost-effective solutions covering the full lifecycle of health management. This collaboration aims to effectively combine the quality of medical services with the efficiency of insurance payments, thereby providing users with personalized health protection services.

For Shouhui Group, this collaboration facilitates its transformation from a traditional insurance intermediary into a comprehensive health service platform, expanding its business scope, enhancing market competitiveness, and improving user stickiness and satisfaction. It enables the company to provide more complete and higher-quality health protection services, while also injecting new growth momentum into its development in the health insurance market.

In May, Muchenglin Group and Qingsong Health Group established a deep strategic partnership. By leveraging data interoperability and complementary capabilities, the two parties aim to break the traditional binary structure of insurance “underwriting–claims” and build a comprehensive value loop encompassing “health risk identification, health financial protection, and proactive health management.”

This collaboration marks a significant step for Shenzhen Muchenglin Technology Co., Ltd. in expanding from its standalone insurance business into the comprehensive health insurance services sector, helping to strengthen its health insurance service chain and enhance the depth and breadth of its offerings. Meanwhile, by leveraging Easy Health Group’s extensive user base and network of medical professional partnerships, Muchenglin can further expand its market coverage, boost brand awareness and market influence, and drive sustained growth and innovative development of its business.

Since 2025, the insurtech sector has witnessed a surge in IPO filings: companies such as Muchenglin Group, Qingsong Health Group, Qingmin Shuke, Hengguang Holdings, Yuanbao, and iYunbao have intensively submitted prospectuses to the Hong Kong and U.S. stock markets, bringing the total number of insurtech firms and intermediaries awaiting listing to eight. This wave of IPOs reflects the industry’s profound transformation pressures and the restructuring of its development logic.

Behind the wave of collective IPOs, cyclical capital pressures are particularly pronounced.Insurtech companies founded around 2015 have generally entered a 5–7 year investment recovery period. In 2025, these enterprises are coinciding with a critical window for capital exit, with the return demands of Limited Partners (LPs) imposing hard constraints. Since its establishment in 2015, Shenzhen Muchenglin Technology Co., Ltd. has completed multiple rounds of financing and filed for listing with the Hong Kong Stock Exchange three times, reflecting the urgency of exit under the constraints of valuation adjustment mechanisms (VAMs).

Exit channels are narrowing, the M&A market is cooling, leaving IPOs as the only option.In 2024, the scale of M&A transactions in the insurance intermediary industry declined year-on-year. Small and medium-sized institutions not only lacked the strength to go public independently but also faced pressure from the Matthew effect created by leading enterprises through capital, technology, and ecosystem building. In this context, an IPO has become the only strategic choice for leading institutions to achieve equity liquidity and join the first tier of the industry.

The Dual Squeeze of Policy Compliance and Profitability Models.The escalation of regulatory policies constitutes a third driving force. The comprehensive implementation of the “integration of reporting and conduct” policy directly undermines the foundation of traditional commission income, while rising compliance costs create a dual squeeze. Taking insurance intermediaries as an example, they generally face a “scissors gap” between declining commission rates and increasing compliance investments, making it urgent to replenish cash flow through IPO financing and secure a strategic buffer period for business transformation.

It is often said that the insurance industry is caught in a “rat race,” the essence of which is a vicious cycle of homogeneous competition. The current domestic insurance market exhibits two major characteristics:

First, the business structures of most enterprises are heavily reliant on traditional commission-based revenue, while high-value-added segments such as technical services and data empowerment have yet to achieve scaled output.

Second, although leading institutions have begun to deploy technologies such as AI-driven pricing and intelligent underwriting, the overall depth of innovation still lags behind that of overseas insurtech companies. This development bottleneck is driving a structural shift in the key factors of industry competition—from a race for channel resources to a technology-centric competition centered on AI capabilities.

For instance, in the underwriting process, machine learning models enable dynamic risk assessment, breaking through the static limitations of traditional underwriting rules. In claims processing, intelligent systems leverage image recognition and big data cross-verification to multiply processing efficiency. More critically, AI-driven pricing engines based on user behavior data empower insurers to build precise, personalized pricing capabilities tailored to each individual. These technological breakthroughs directly enhance service premium potential, helping institutions escape the quagmire of price wars and instead establish differentiated barriers in dimensions such as risk assessment accuracy and service response speed.

Amid the trend of “disintermediation,” intermediaries must redefine their value coordinates. How can they create value that insurers cannot replicate? How can they convert traffic advantages into ecosystem moats? Perhaps only by leveraging technology to reduce transaction costs and extending ecosystems to enhance service added value can they establish irreplaceability amid turbulence.

The successful IPO of Muchenglin Group is certainly a cause for celebration and congratulations, but it also reflects the collective anxiety among Chinese insurtech intermediaries amid receding capital flows and industry transformation. Whether the company can leverage its IPO to break away from a single business model and build a sustainable ecosystem may serve as a key case study for observing industry-wide changes. VCBeat will continue to monitor this development closely.

References:

[1] “The Vanishing Million: How the Insurance Industry Fell from Grace After Its ‘Golden Age’” — P&C Insurance Perspectives

[2] “Insurance Intermediaries Flock to HKEX for IPOs: How Close Is Shouhui Group, Parent Company of ‘Xiaoyusan’, to Going Public?” Jiemian News

[3] “[IPO Watch] Shouhui Group: Third Filing with HKEX, Achieves Revenue in 2024” Mianbao Finance

[4] "Shouhui Group Passes HKEX Listing Hearing: Technology-Enabled Sales of Over 1,900 Insurance Products, with 2024 Revenue Reaching Approximately RMB 1.4 Billion" IPO Zaozhidao