ASCO Witness: Chinese Innovative Drugs Break Into the Global First Tier

2015–2025: ASCO Witnesses the Rise of China’s Innovative Drugs

ASCO is the largest and most academically influential conference in the global oncology field, with numerous cutting-edge data and findings released annually. The 2025 ASCO Annual Meeting opened on May 30 in Chicago.

10 years ago,At ASCO, there was only one oral presentation from China, namely the FOWARC study led by Professor Wang Jianping of the Sixth Affiliated Hospital of Sun Yat-sen University. Meanwhile, the number of Late-Breaking Abstracts, which have drawn significant attention from the international market, stood at zero.

It is understood that ASCO’s oral presentations are subject to rigorous review criteria. Selected studies must demonstrate significant innovation, offer novel breakthroughs or important advances in the field of oncology, and provide findings that guide clinical practice.

For example, the FOWARC study, led by Professor Wang Jianping, is the first phase III randomized controlled trial worldwide to explore the efficacy of neoadjuvant chemotherapy alone in locally advanced rectal cancer. Based on this study and subsequent follow-up data, the National Comprehensive Cancer Network (NCCN) has currently incorporated selective radiotherapy after neoadjuvant chemotherapyWriting Guidelines, making it one of the standard treatment options, thereby optimizing the preoperative treatment paradigm for locally advanced rectal cancer.

Late-Breaking Abstracts are among the most highly anticipated forms of research presentation at the ASCO Annual Meeting. They feature special reports on studies with significant breakthroughs, cutting-edge findings, and the potential to profoundly impact clinical practice, making selection extremely competitive. Unlike other studies whose data are released in advance, the pivotal data from Late-Breaking Abstracts are primarily presented live at the ASCO conference, drawing widespread attention from the medical community.

Ten years later,A total of 73 Chinese studies were presented as oral presentations at ASCO 2025, setting a new historical record. Additionally, 11 Chinese studies were selected for the prestigious Late-Breaking Abstracts.

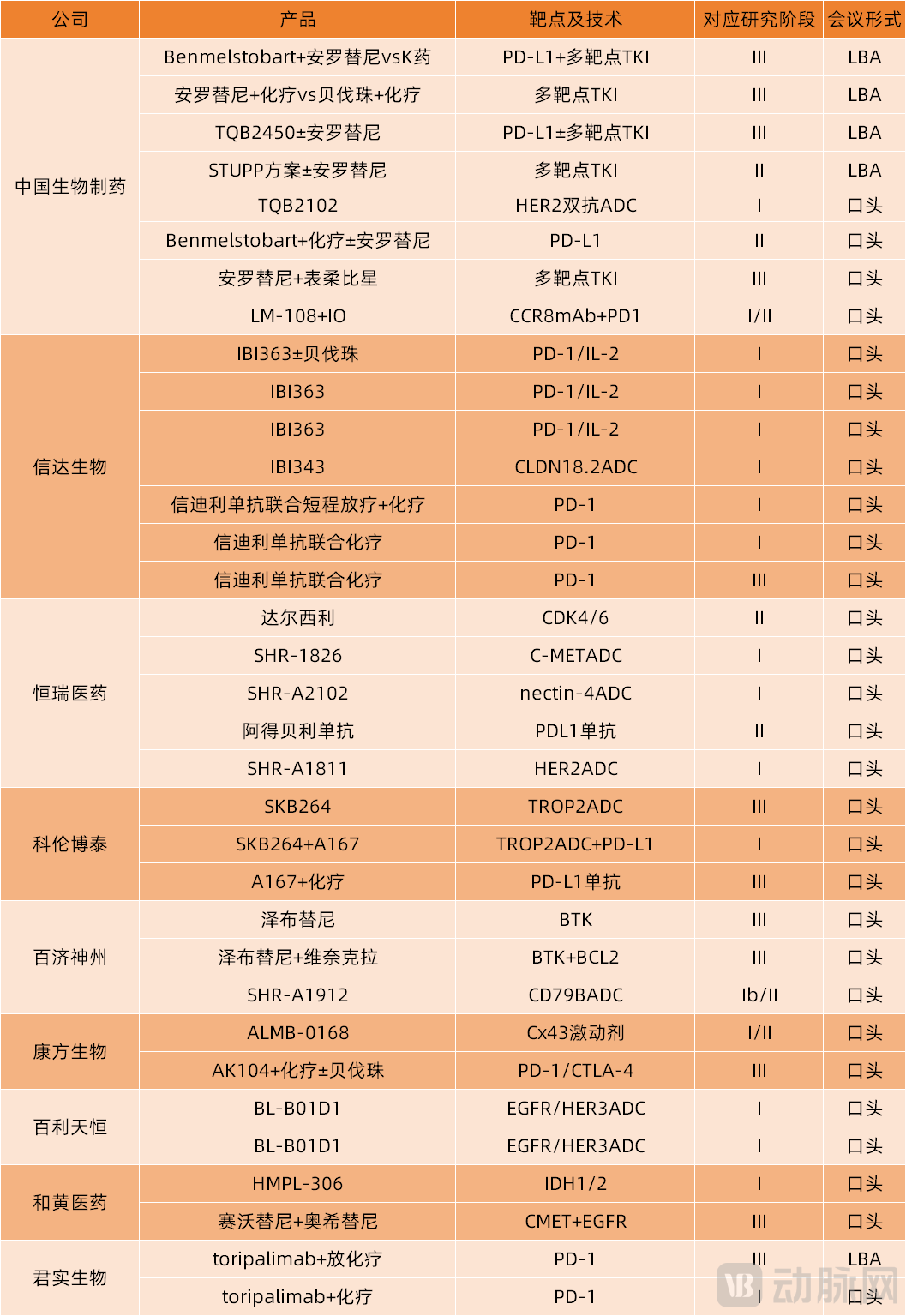

(Selected Chinese Studies, Related Companies, and Innovative Drugs at ASCO)

Among them, China Biopharmaceutical, a pharmaceutical giant, set a new record for Chinese pharmaceutical companies at ASCO with 12 oral presentations. Additionally, four of its studies were selected as “Late-Breaking Abstracts.” Including poster presentations and abstract acceptances, more than 40 studies were showcased.

Beyond a breakthrough in quantity, ASCO has also witnessed the rise in quality of Chinese research and innovative drugs.In the past, the most common refrain from Chinese teams at ASCO meetings was, “We have also conducted similar studies.” But today, the voice of Chinese pharmaceutical companies and clinical research teams at ASCO has shifted toWorld's First, First Announcement。

For example, the DIAMOND study, in which Junshi Medical participated, titled “A Multicenter, Non-inferiority, Phase III Randomized Controlled Trial of Toripalimab Combined with Induction Chemotherapy and Radiotherapy with Concurrent or Non-concurrent Cisplatin for the Treatment of Locally Advanced Nasopharyngeal Carcinoma,” isWorld's FirstPhase III study confirming that concurrent cisplatin chemotherapy can be omitted when PD-1 inhibitors are combined throughout the course of chemoradiotherapy.

LBL-007, an LAG-3 antibody under Weilizhibo, isOne of the top three globally advanced clinical-stage monoclonal antibodies targeting LAG-3 (excluding the only approved LAG-3-targeted drug), and the first antibody in its class proven effective against nasopharyngeal carcinoma.. The Phase II data presented in this poster showed that patients receiving combination therapy with LBL-007, tislelizumab, and chemotherapy achieved an objective response rate of 83.3%, compared to those treated with tislelizumab plus chemotherapy aloneincreased by nearly 20%. Meanwhile, the median progression-free survival in the LBL-007 combination therapy group reached 15.8 months, compared with tislelizumab plus chemotherapy> 70% increase。

Today, breakthroughs in China’s innovative drugs have drawn the attention of the U.S. industry.On May 29, Time magazine published an article titled “The U.S. Can’t Lose the Biotech Race With China,” stating that although the United States has long held a position as the global leader in biotechnology, it now faces the risk of losing this status.

It is worth noting that, leveraging the most cutting-edge global advancements, the ASCO Annual Meeting has given rise to the “ASCO Effect,” wherein the stock prices of relevant pharmaceutical companies experience significant short-term volatility in response to clinical data presented at the conference. Historically, the ASCO Effect was primarily observed in the U.S. stock market. However, over the past two years, as Chinese innovative drugs have increasingly become a prominent feature at ASCO, the “ASCO Effect” has also begun to manifest in China’s domestic stock market.

For example, after the full texts of selected study abstracts from the 2025 ASCO Annual Meeting were released, Chinese innovative pharmaceutical companies—particularly those that reported impressive clinical data—experienced significant stock price surges. As of May 30, the share prices of Chinese biopharmaceutical firms actively participating in ASCO, such as Sino Biopharmaceutical, RemeGen, and Innovent Biologics, had shown sustained upward momentum over several days. With the upcoming release of high-impact data from late-breaking abstracts, the stock prices of relevant domestic pharmaceutical companies are expected to receive further catalysts for continued growth.

ASCO Witnesses the Rise of China’s Innovative Drugs.

Among these, ADCs, bispecific antibodies, and cell therapies represent areas of strength for China’s innovative drugs, with domestic pipelines holding a leading position in the global market.

From the ASCO conference, it is evident that domestically produced ADCs are clearly in the global first tier.

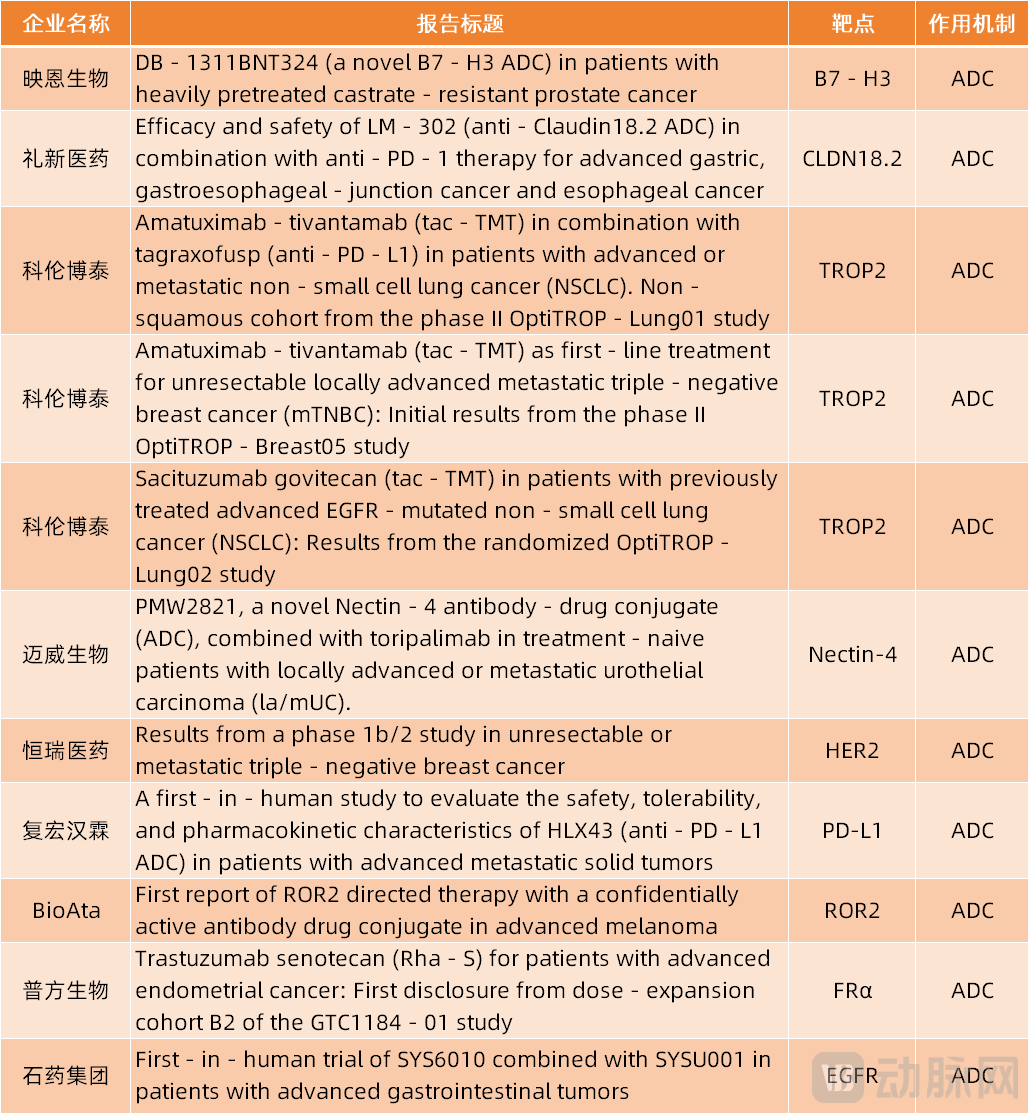

First, there is a large number of domestically developed ADC pipelines.At the ASCO Annual Meeting, 184 studies related to ADC pipelines were selected, of which 89 originated from China, accounting for approximately 48.4% of the total ADC-related reports—nearly half.

(Selected Chinese-Made ADCs at ASCO 2025)

Furthermore, expanding the view to the global market, data from the Insight database reveals that there are 519 R&D projects for domestically produced antibody-drug conjugate (ADC) new drugs, accounting for more than 40% of the global ADC pipeline. For popular targets such as HER2, TROP2, and CLDN18.2, Chinese pharmaceutical companies have captured 63.6%, 76.5%, and 85.7% of the global number of drugs under development, respectively.

Secondly, domestically developed ADC drugs are at the forefront of global R&D progress.For example, RemeGen’s disitamab vedotin is the first ADC drug approved globally for patients with HER2-positive advanced breast cancer with liver metastases; Kelun-Biotech’s sacituzumab tirumotecan is the first TROP2-targeting ADC drug approved globally for lung cancer indications...

On May 29, Hengrui Medicine’s self-developed HER2 antibody-drug conjugate (ADC) was approved for marketing. It is indicated for the treatment of adult patients with unresectable locally advanced or metastatic non-small cell lung cancer (NSCLC) harboring activating HER2 (ERBB2) mutations who have previously received at least one systemic therapy.

In addition, ADC products such as Lepu Biopharma’s vebicoritamab and Kelun-Biotech’s bodotrituzumab have already been submitted for marketing approval. The progress of other domestic ADC pipelines is also at a global leading position; for instance, the ADC pipelines developed by pharmaceutical companies including DualityBiologics, Mabwell Bioscience, Henlius, and CSPC Pharmaceutical Group are all at the forefront of the field.

Finally, the clinical data for domestically produced ADC drugs are excellent.At the ASCO meeting, multiple studies on domestically developed ADC drugs were selected for oral presentations due to their outstanding clinical data.

For example, a study reported preliminary results of 9MW2821, an antibody-drug conjugate (ADC) developed by Mabwell Bioscience, in combination with toripalimab for the treatment of previously untreated patients with locally advanced or metastatic urothelial carcinoma (la/mUC): as of December 19, 2024, the objective response rate was 87.5%, the disease control rate was 92.5%, the 6-month median progression-free survival rate was 79.1%, and the 3-month duration of response rate was 100%.This indicates that treatment-naïve patients with locally advanced or metastatic urothelial carcinoma (la/mUC) across different subgroups can benefit from the combination therapy of 9MW2821 and toripalimab.。

Leveraging these advantages, Chinese-made ADCs have become the most competitive ADC pipelines globally. Consequently, multinational pharmaceutical companies are more inclined to engage in transactions involving domestic ADC pipelines. Statistics show that since 2021, the total value of outbound business development (BD) deals in China’s ADC sector has exceeded $40 billion; from 2022 to 2023, China became the country with the highest number of ADC deal licensors worldwide.

Bispecific Antibodies (BsAbs) are a class of artificial antibodies constructed through genetic engineering or chemical methods, featuring two distinct antigen-binding sites that can simultaneously bind to two different antigens or to different epitopes of the same antigen.

The core advantage of bispecific antibodies lies in their "dual-targeting" capability. Taking bispecific antibody-drug conjugates (BsADCs) as an example, compared with monoclonal antibody-drug conjugates (mAb-ADCs), BsADCs leverage two antigen-binding sites to enhance tumor cytotoxicity by engaging both tumor cells and immune cells. Binding to two distinct cell surface epitopes can reduce off-target effects and associated adverse reactions. Furthermore, dual targeting enables the blockade of two different signaling pathways, thereby enhancing cytotoxic potency and overcoming drug resistance.

China’s innovative drugs are also at the global forefront in the field of bispecific antibodies.

First, China's bispecific antibody pipeline accounts for nearly 50% of the global bispecific antibody pipeline.According to the NextPharma database by PharmaCube, as of September 2023, there were over 1,300 bispecific/multispecific antibody pipelines under development globally, with 46% developed by Chinese companies and more than 150 projects in clinical development or on the market.

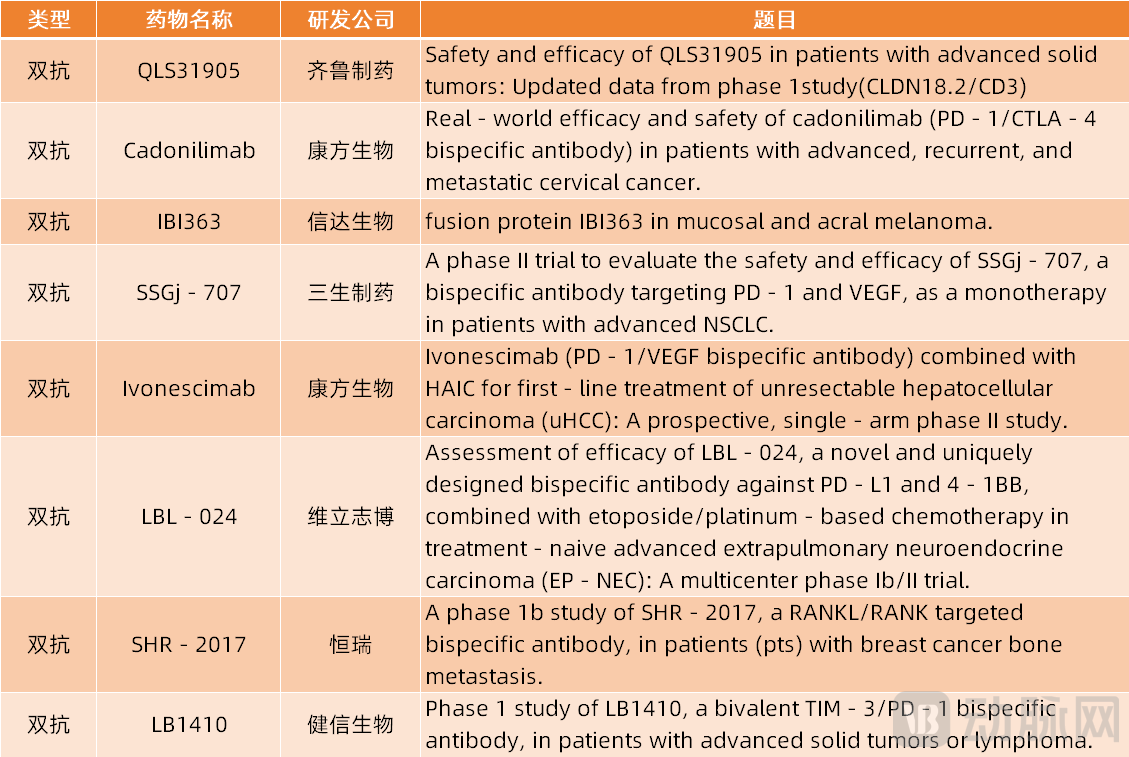

At the ASCO conference, companies including Qilu Pharmaceutical, Akeso, Innovent Biologics, 3SBio, WeLiBio, Hengrui Medicine, Henlius, Jianxin Biologics, Zeltex Pharmaceuticals, and Chia Tai Tianqing will present approximately 34 studies related to bispecific antibodies, accounting for about 49% of all bispecific antibody research at ASCO.

(Selected Studies on Chinese-Made Bispecific Antibodies Accepted at ASCO 2025)

Second, China’s bispecific antibody pipeline is at the forefront globally.As of August 2024, there were 24 bispecific antibody products globally in the marketing application or Phase III stage, including seven domestically produced drugs.

Third, clinical data from domestic bispecific antibody pipelines have demonstrated robust performance.For example, at the 2025 ASCO Annual Meeting, 3SBio presented Phase II clinical data on SSGJ-707, a PD-1/VEGF bispecific antibody, as monotherapy in patients with advanced non-small cell lung cancer (NSCLC), in poster format. Among the 76 patients who completed at least one efficacy assessment, the objective response rate (ORR) and disease control rate (DCR) were 29.6% and 85.2%, respectively, at the 5 mg/kg Q3W dose; 61.8% and 97.1% at 10 mg/kg Q3W; 54.5% and 90.9% at 20 mg/kg Q3W; and 25% and 75% at 30 mg/kg Q3W.

Possibly influenced by this clinical data, on May 20, 3SBio and Pfizer signed an agreement granting Pfizer exclusive global rights (excluding mainland China) to develop, manufacture, and commercialize SSGJ-707, a PD-1/VEGF bispecific antibody. 3SBio will receive a non-refundable, non-creditable upfront payment of $1.25 billion, as well as development, regulatory approval, and sales milestone payments totaling up to $4.8 billion. Additionally, 3SBio will receive tiered royalties in the double-digit percentage range based on product sales in the licensed territories.

Following Akeso’s $500 million upfront payment for ivonescimab, Lixin Pharma’s $588 million upfront payment for the overseas licensing of LM-299, and Promiscience Biotech’s $800 million upfront payment for PM8002, 3SBio’s $1.25 billion upfront payment for SSGJ-707 has once again set a new record for upfront payments in the overseas licensing of Chinese-developed bispecific antibodies.

In addition to 3SBio, pharmaceutical companies such as Keymed Biosciences, Tongrun Biopharma, Akeso Biopharma, Nona Biosciences, Bio-Thera Solutions, and Lixin Pharma have also achieved overseas business development (BD) deals for bispecific antibody drugs. According to incomplete statistics,Approximately 14 domestic bispecific antibodies went global in 2024(excluding bispecific antibody-drug conjugates), covering targets such as CD3/CD19, CD3/CD20, PD-(L)1/VEGF, and TSLP,Total transaction value surpassed $10 billion, with upfront payments exceeding $2 billion, setting a new historical record.。

In 2025, multinational pharmaceutical companies (MNCs) continued to pursue business development (BD) opportunities for bispecific antibody pipelines from Chinese pharmaceutical firms. For instance, Quxin Biologics and 3SBio recently finalized BD collaborations with MNCs for their bispecific antibody drugs within the past two months. With data from various domestic bispecific antibody studies being presented at ASCO, BD transactions involving Chinese-made bispecific antibodies are expected to become even more vigorous.

Beyond ADCs and bispecific antibodies, China’s innovative drugs are also in the global first tier in fields such as cell therapy and oncolytic viruses.

In the field of cell therapy, for instance, the report “Trends in Technological Innovation and Industrial Development of Immune Cell Therapy,” jointly released in January 2025 by authoritative institutions such as the Shanghai Center for Life Sciences Information of the Chinese Academy of Sciences and the School of Medicine at Shanghai Jiao Tong University, indicates that:As of the end of 2024, China had registered 489 cell therapy clinical trial projects, accounting for 47% of the global total and ranking second worldwide., further narrowing the gap with the United States (48.3%).

From the perspective of pipeline distribution, Chinese companies are primarily focused on CAR-T therapies. However, domestic innovative enterprises are also accelerating their deployment of emerging technologies such as CIK, TCR-T, CAR-NK, and TIL therapies. For instance, Gracell Biotechnologies reported at the conference that its TIL therapy demonstrated preliminary efficacy in patients with recurrent or metastatic cervical cancer.

Overall, in emerging fields such as antibody-drug conjugates (ADCs), bispecific antibodies, trispecific/multispecific antibodies, and cell therapy, Chinese innovative pharmaceutical companies are leveraging their advantages in talent, technology, clinical resources, and policy support to secure a leading position globally.

With the rise of China’s innovative drugs, business development (BD) deals for domestic innovative drugs are also becoming increasingly active.

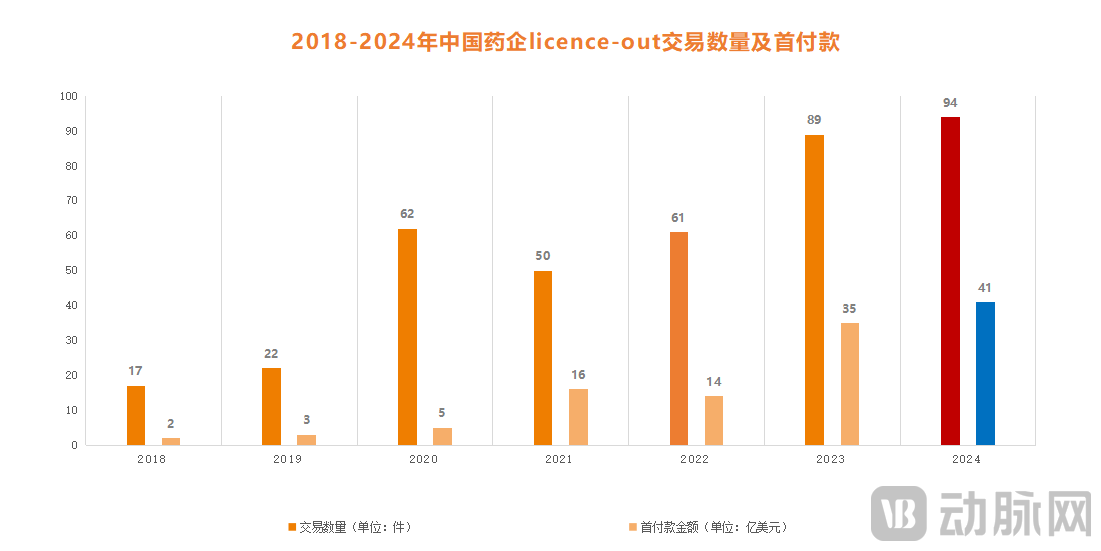

According to data from PharmaCube, the number of license-out transactions by Chinese pharmaceutical companies has increased from 17 in 2018 to 94 in 2024; the upfront payments for these license-out deals have grown from approximately USD 200 million in 2018 to around USD 4.1 billion in 2024.

Number of License-Out Deals and Upfront Payments by Chinese Pharmaceutical Companies, 2018–2024 (Data Source: PharmaCube)

In 2025, business development (BD) deals for innovative drugs remained highly active. In the first quarter alone, the total value of license-out transactions by Chinese innovative pharmaceutical companies reached $36.9 billion, representing a year-on-year increase of 222%.

However, recent BD transactions have undergone significant changes in form compared to previous deals.

In the past, license-out deals for innovative drugs in China largely followed a narrative of “high total deal value, low upfront payment,” with upfront fees typically accounting for only 2%–5% of the total transaction amount. However, given the high barriers and substantial risks associated with innovative drug development, the likelihood of achieving milestones and securing subsequent payments is relatively low. Data from SRS ACQUIOM shows that the milestone achievement rate for Chinese innovative drugs was only 22% in 2023, with success rates declining further in later stages.This has left domestic pharmaceutical companies able to secure only upfront payments in traditional business development (BD) deals.And this amount was precisely the lowest revenue figure.

Meanwhile, domestic pharmaceutical companies also face risks such as “product returns.” For instance, in February 2025, Novo Nordisk accused Henry Pharma of fraud and sought $800 million in damages. In March 2025, Clover Biopharmaceuticals received a written notice from Gavi, the Vaccine Alliance, unilaterally terminating the advance purchase agreement and demanding the refund of $224 million in upfront payments. When collaborations are terminated or “returns” occur, subsequent milestone payments for domestic pharmaceutical companies become mere illusions.

Undoubtedly, this is highly unfavorable for domestic pharmaceutical companies. Some overseas pharmaceutical firms even exploit the low upfront payment structure prevalent in business development (BD) deals involving Chinese companies to arbitrage profits: they acquire pipeline rights with minimal upfront costs and then resell them to multinational pharmaceutical corporations at a substantial premium.

With the rise of China’s innovative drugs and the growing influence in global discourse, the business development (BD) transaction models of domestic pharmaceutical companies have also evolved.

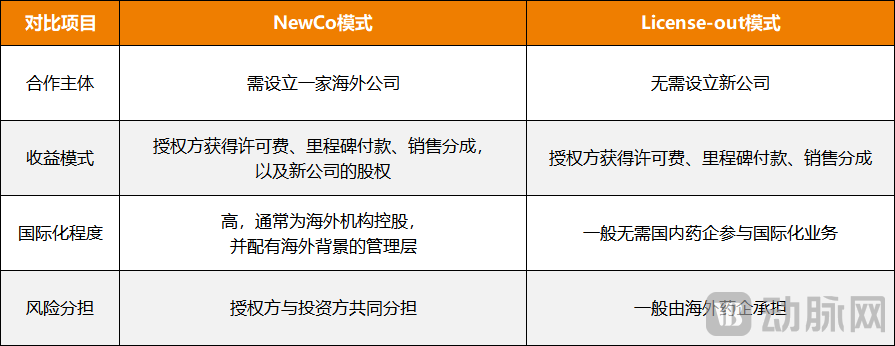

On one hand, BD transactions from the traditionallicense-outShift to the “NewCo” model.License-out involves directly selling pipeline rights to multinational pharmaceutical companies, whereas the NewCo model entails the buyer and seller jointly establishing a new company to manage the post-transaction pipeline.

Comparison Between the NewCo Model and the License-out Model

Compared with license-out deals, the most distinctive feature of the NewCo model is the deeper alignment between buyers and sellers. By leveraging the NewCo model, Chinese pharmaceutical companies and multinational pharmaceutical corporations can co-build an ecosystem, while Chinese firms retain decision-making influence, thereby maximizing and sustaining long-term benefits.

According to statistics, the total value of deals struck by Chinese innovative pharmaceutical companies through the NewCo model exceeded RMB 60 billion in 2024, representing a 54% increase from 2023. Entering 2025, the NewCo model has maintained its strong growth momentum, with five companies established via this model in January alone.

On the other hand, The proportion of upfront payments in BD transactions among Chinese pharmaceutical companies has significantly increased.In the past, upfront payment ratios in business development (BD) deals for innovative drugs in China were extremely low. However, driven by factors such as the NewCo model and the growing influence of Chinese innovative drugs, upfront payment ratios in domestic BD transactions have risen significantly.

For example, on May 20, 3SBio and Pfizer reached a collaboration agreement on the PD-1/VEGF bispecific antibody SSGJ-707, with an upfront payment of $1.25 billion, setting a new record for the highest upfront payment for Chinese innovative drugs going global; on May 27, EMBiologics entered into a NewCo partnership with Juri Biosciences, a portfolio company of TCG Labs Soleil, involving an upfront payment of $60 million, followed by up to $575 million in development, regulatory approval, and commercialization milestone payments, revenue sharing based on net sales, and partial equity in Vignette, with the upfront payment accounting for approximately 9.4% of the total deal value.

With the emergence of new models and the growth of BD transactions, the global expansion of China’s innovative drugs is expected to transition from the previous “asset licensing” approach to a new phase of “ecosystem co-creation.”

During the ASCO 2025 conference, the rise of innovative Chinese drugs was a prominent theme, as evidenced by the substantial number of abstracts selected for presentation.

However, the industry also needs another voice to cool down the market and bring it back to rationality.

As mentioned above, the ADC and bispecific antibody pipelines developed by Chinese pharmaceutical companies account for nearly 50% of the global pipeline in these categories. While characterized by both substantial volume and high quality, a significant challenge remains: severe homogenization among domestic pipelines. This necessitates that Chinese innovative pharmaceutical companies move beyond existing, well-known targets and make contributions in other novel targets and emerging fields.

The same applies to BD (Business Development) deals. While BD transactions are currently booming, they are not a “master key.” BD deals leverage the strength of multinational corporations (MNCs) to facilitate the global expansion of domestically developed innovative drugs. This indirectly highlights that most Chinese pharmaceutical companies have shortcomings in their commercialization capabilities in other global regions and lack sufficient experience in autonomous globalization. To enhance their international competitiveness and reduce reliance on MNC distribution channels, Chinese pharmaceutical companies must build global commercialization teams alongside achieving technological advancements and breakthroughs in new drug development.

We believe that with the development of innovative drugs in China, domestic pharmaceutical companies will gradually address their weaknesses, strengthen their influence, and become a significant force in the global pharmaceutical industry.