State Capital as Lifeline: 822 Direct Investments in Two Years Reshape China's Medical Sector

Akeso

Innovative Antibody Drug Developer

One in Every Three Healthcare Companies Receives Direct Investment from State-Owned Institutions。

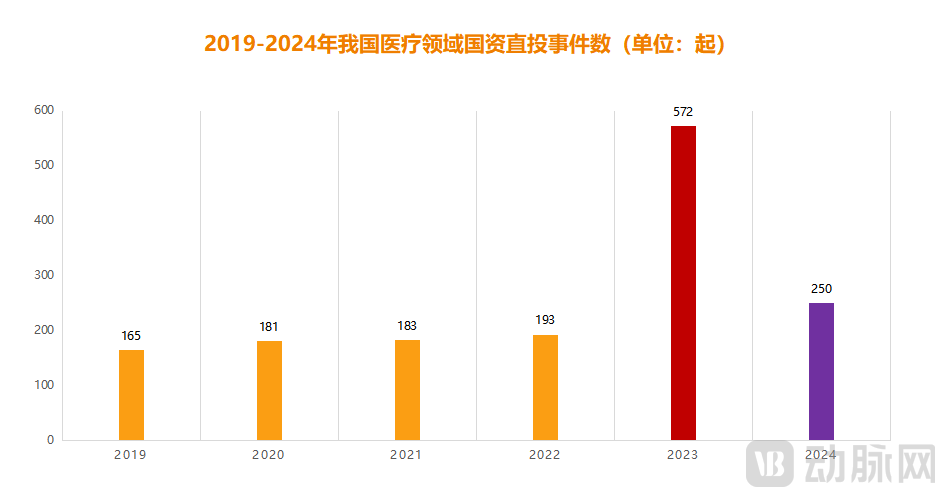

Figure 1. Number of State-Owned Direct Investment Events in China’s Healthcare Sector, 2019–2024 (Chart by VCBeat)

Figure 1. Number of State-Owned Direct Investment Events in China’s Healthcare Sector, 2019–2024 (Chart by VCBeat)

This is not an exaggerated description, but a true reflection of the data. According to incomplete statistics from the VCBeat Orange Database,From 2023 to 2024, state-owned capital completed a total of 822 direct investments in the healthcare sector, accounting for 32.8% of the total number of investments.It is worth noting that these figures are based solely on publicly available data; since a portion of direct investments by state-owned capital has not been disclosed, the actual proportion may be even higher, potentially exceeding 50%. A founder currently in the midst of fundraising round has deep personal insight into this reality, “"Over the past six months, we have primarily engaged with state-owned enterprises; it has been extremely difficult to identify any non-state-owned institutions."。”

Following the aggressive increase in state-owned capital investment, the industry has already witnessed some positive changes, with a number of healthcare companies achieving rapid growth thanks to state-owned involvement. A typical case is Akeso, which received RMB 500 million in funding from Guangzhou High-Tech Industrial Development Zone Investment Group in December 2022 to support the commercialization of Cadonilimab and expand its approved indications. The following year, Akeso delivered its “strongest financial performance in history,” with annual revenue surging by 440.35% and achieving profitability for the first time. In fact, during the capital winter of the past two years, there have been many similar cases of state-owned capital stepping in to rescue companies.

However, everything has two sides. As state-owned capital gradually becomes the sole source of fresh water in the healthcare industry, negative information related to it is also constantly emerging.The foremost issue is the “impurity” of state-owned capital., as they are linked to local investment promotion targets, this practice artificially extends the lifespan of projects that should have been gradually phased out by the market, thereby severely disrupting industry order;Secondly, state-owned capital faces the challenge of “struggling alone” in the capital market., taking the recently heated discussion on “the inability to find a lead investor this year” as an example, it is essentially the excessive participation of state-owned capital that has caused some private capital to withdraw, resulting in the absence of key industry players;Finally, the most challenging issue for state-owned capital is its exit., with narrowing IPO pathways compounded by fund maturities, the exit of state-owned capital has become increasingly urgent.

It is evident that the “era of comprehensive state-owned capital” has already arrived with great fanfare and will persist for a considerable period in the future. However, for the vast majority of healthcare professionals, despite their intricate ties to state-owned capital and frequent discussions on the topic over the past two years, most still hold only a vague impression and lack access to comprehensive information. In light of this, VCBeat has systematically reviewed 822 direct investments made by state-owned capital in the healthcare sector, aiming to clarify the underlying investment logic.

What Types of Healthcare Projects Do State-Owned Capital Prefer to Invest In?

Since the establishment of “Shenzhen Investment Management Company” in 1987, China’s state-owned asset development has a history of nearly 40 years; however, for a long period in the past,State-owned capital in the healthcare sector primarily targets mid-to-late-stage projects., the market certainty for this segment of projects is generally strong, with state-owned capital playing more of a complementary role.

The shift occurred in 2023. Impacted by the market downturn, US dollar funds withdrew successively, leaving state-owned capital as the sole source of fresh liquidity in the capital market. Meanwhile, China’s innovative drug and high-end medical device sectors entered a critical transition period, urgently requiring substantial early-stage fund allocation. Thus,The investment logic of state-owned capital in the healthcare sector has shifted from pursuing broad certainty to focusing on “investing early, investing in small ventures, and investing in innovation.”。

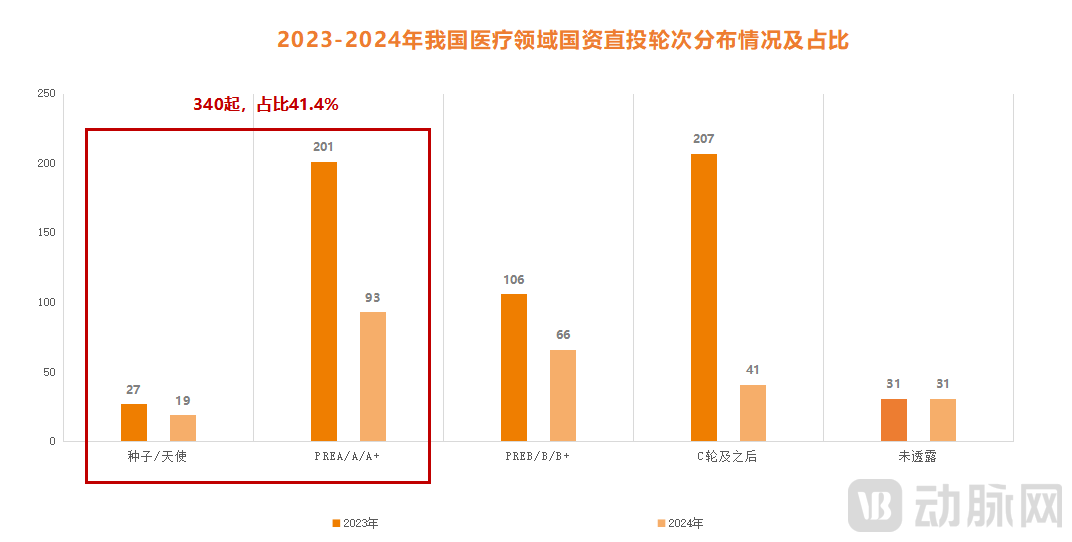

Figure 2. Distribution and Proportion of State-Owned Capital Direct Investment Rounds in China’s Healthcare Sector, 2023–2024 (Chart by VCBeat)

Figure 2. Distribution and Proportion of State-Owned Capital Direct Investment Rounds in China’s Healthcare Sector, 2023–2024 (Chart by VCBeat)

The data precisely validates this point. According to incomplete statistics from the Artery Orange database, among the 822 direct investments by state-owned capital in the healthcare sector over the past two years,The financing proportion for Series A and prior rounds reached 41.4%.. To further break it down, this proportion stood at 39.8% in 2023 and rose to 44.8% in 2024, clearly indicating that state-owned capital is increasingly favoring early-stage medical projects.

In this regard, a head of a Shenzhen state-owned asset management firm stated, “The consensus among state-owned capital to ‘invest early and invest in small ventures’ stems first from an industry perspective. China’s healthcare sector has reached a critical stage that demands ‘genuine innovation,’ and state-owned capital has an obligation to identify and incubate a batch of cutting-edge projects with high potential. Furthermore, from the standpoint of fund returns, as exit channels narrow, the investment yields for mid- to late-stage projects have significantly declined. Moreover, for certain state-owned investors, investing in very late-stage projects offers little competitive advantage.”But with early-stage investments, as long as one or two projects succeed, the overall return of the fund is secured.。”

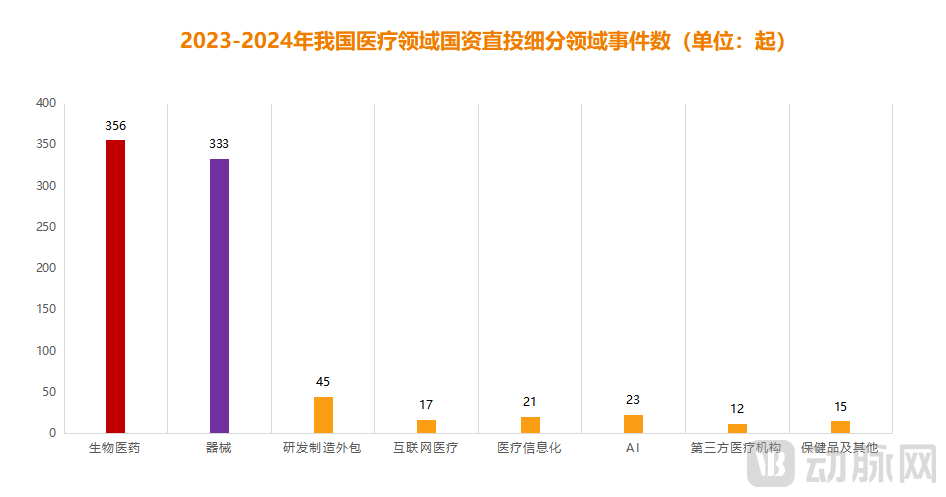

Figure 3. Number of State-Owned Direct Investment Deals in Subsectors of China’s Healthcare Industry, 2023–2024 (Chart by VCBeat)

Figure 3. Number of State-Owned Direct Investment Deals in Subsectors of China’s Healthcare Industry, 2023–2024 (Chart by VCBeat)

Compared with “investing early and in small ventures,” “investing in innovation” is more prominently reflected in the statistical data. It is reported that among 822 direct investments made by state-owned capital,A total of 689 deals were concentrated in the biopharmaceutical and high-end medical device sectors, accounting for 83.8% of all financing transactions.. So, which industrial sectors have actually received investment?

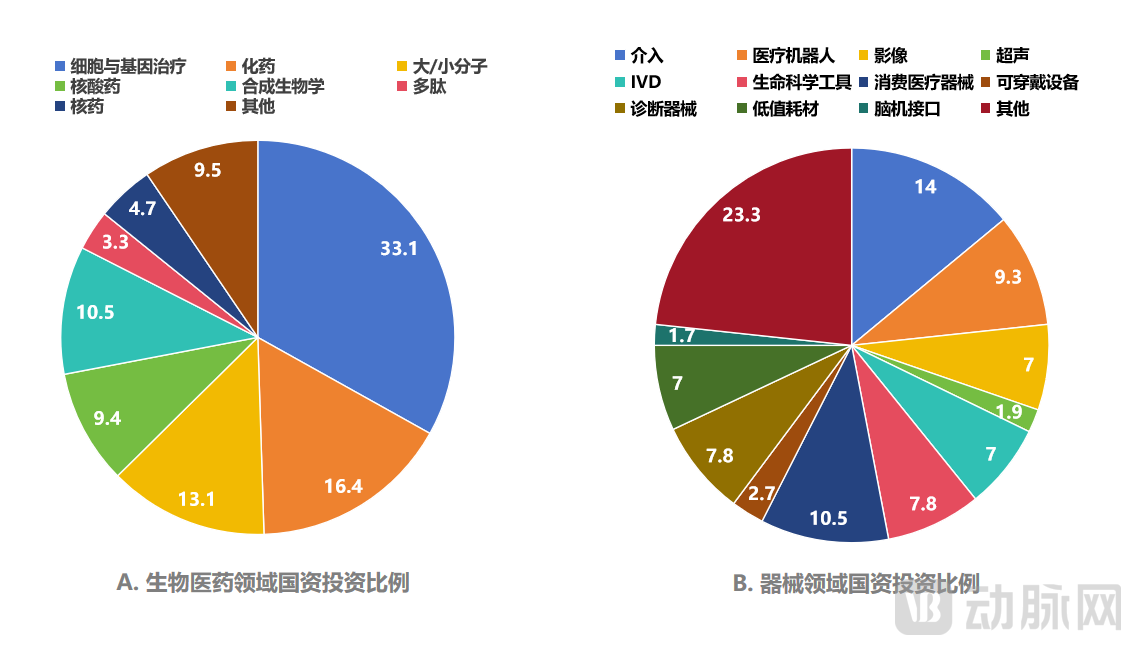

Figure 4. State-owned Capital Investment in the Biopharmaceutical and Medical Device Sectors (Chart by VCBeat)

Figure 4. State-owned Capital Investment in the Biopharmaceutical and Medical Device Sectors (Chart by VCBeat)

Taking the biopharmaceutical industry as an example,State-owned capital investment targets are primarily concentrated in niche sectors such as cell and gene therapy, large and small molecules, nucleic acid drugs, and synthetic biology.These fields generally exhibit strong technological innovation and correspond to substantial market demand for their respective diseases. For instance, synthetic biology is regarded as a groundbreaking technology from a technical perspective, enabling the leap from “understanding life” to “designing life” through engineering approaches. In terms of market demand, synthetic biology primarily targets major diseases such as cancer and autoimmune disorders, which affect hundreds of millions of people. Following this logic, state-owned capital has completed 38 direct investments in the synthetic biology sector over the past two years, with representative cases including Weigou Factory, Baifu’an Biotechnology, Danqing Pharmaceuticals, and Bio-Rock Regenerative Medicine.

In addition to combining innovation with widespread market demand, the rapid development of domestically produced innovative drugs in recent years has naturally garnered increased favor from state-owned capital. It is reported that Chinese innovative drugs currently not only hold significant R&D advantages in multiple key targets, but the business development (BD) trading market is also exceptionally active. According to incomplete statistics from VCBeat,From 2023 to 2024, Chinese pharmaceutical companies completed a total of 183 license-out deals, with upfront payments alone reaching $7.6 billion.. Behind the surge in business development (BD) deals lies an urgent need for working capital among a large number of pharmaceutical companies, and state-owned capital, as a vital source of liquidity in the capital market, naturally steps forward to meet this demand.

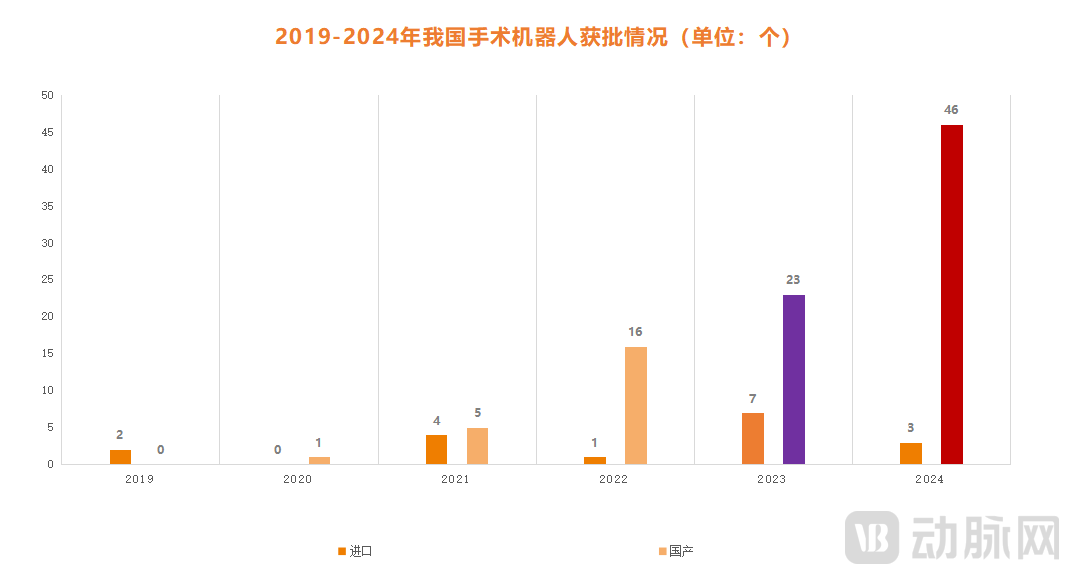

Figure 5. Approval Status of Surgical Robots in China, 2019–2024 (Chart by VCBeat)

Figure 5. Approval Status of Surgical Robots in China, 2019–2024 (Chart by VCBeat)

Unlike innovative drugs,State-owned capital’s investment in medical devices is primarily based on the underlying logic of “domestic substitution.”Focusing on surgical robots as a key example, data from the National Medical Products Administration (NMPA) shows that between 2014 and 2020, only 10 domestically produced surgical robot products from 8 companies were approved in China. However, by the end of 2024, a total of 115 surgical robot products from 64 companies had gained approval across China, comprehensively covering subfields such as laparoscopy, orthopedics, neurosurgery, and puncture procedures. Among these, 94 approved brands were domestically produced, accounting for a significant 81.7% of the total approvals. This growth is clearly inseparable from the promotion by state-owned capital, which completed 31 direct investments in the medical robotics sector over the past two years, successively increasing stakes in leading enterprises such as Tinavi, Pangce, Ruilong Nuofu, Shurui Technology, and Lancet Robotics.

In fact, in addition to surgical robots,Key areas for domestic substitution, including interventional medicine, medical imaging, diagnostics, ophthalmology, and life science tools, have also attracted significant attention from state-owned capital over the past two years, with numerous large-scale financing events occurring.。

In this regard, a state-owned asset executive remarked, “Compared with pharmaceuticals, investing in medical devices is better suited for state-owned capital. On one hand, the market offers greater certainty and entails relatively lower investment risk; on the other, the sector is more ‘tangible,’ as it can rapidly drive local employment and effectively integrate upstream and downstream industrial chains. Coupled with the overarching trend of domestic substitution, state-owned investment in medical devices fully possesses the essential success factors of ‘favorable timing, geographical advantage, and human harmony.’”

State-Owned Capital Invests in Healthcare: Which Company Stands Out?

Over the past two years, nearly all first- and second-tier cities across China have officially announced “industrial fund clusters” with scales ranging from tens of billions to hundreds of billions of yuan. Driven by this momentum,As of 2024, the total scale of China’s government guidance funds for industrial investment and venture capital has exceeded RMB 10 trillion.. As a key sector for state-owned capital investment, the healthcare industry has naturally attracted substantial funding. Behind this trend lies the urgent desire of local governments across China to establish or upgrade their healthcare industries.

So, from the current perspective, who has achieved more significant results in healthcare investment? Through data analysis,VCBeat believes that “Beijing, Shanghai, Guangzhou, Shenzhen, and Suzhou” are undoubtedly in the first tier.。

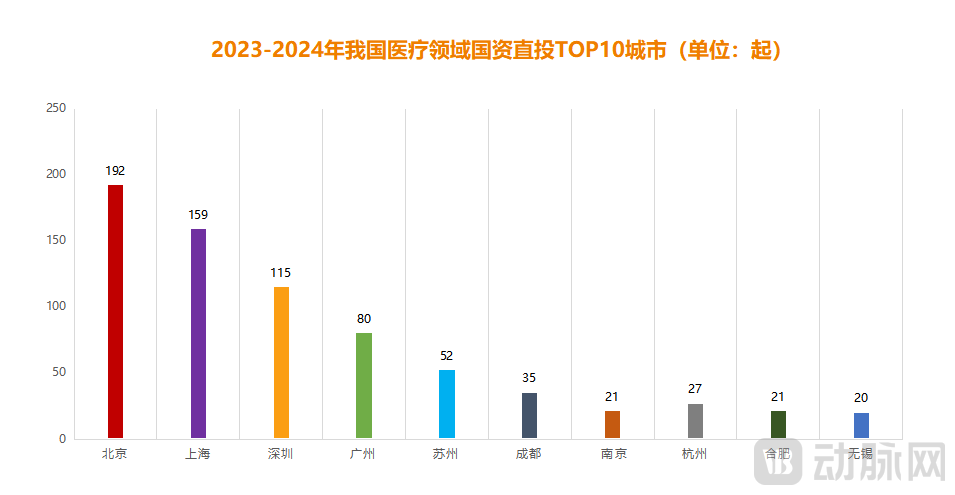

Figure 6. Top 10 Cities in China by Direct State-Owned Capital Investment in the Healthcare Sector, 2023–2024 (Chart by VCBeat)

Figure 6. Top 10 Cities in China by Direct State-Owned Capital Investment in the Healthcare Sector, 2023–2024 (Chart by VCBeat)

From the perspective of investment volume, Beijing, Shanghai, Shenzhen, Guangzhou, and Suzhou rank among the top five nationwide, having completed 192, 159, 115, 80, and 52 direct state-owned capital investments in the healthcare sector, respectively, over the past two years. From the perspective of project returns, as of April 2025,“Among the nearly 500 healthcare companies directly invested by state-owned capital in Beijing, Shanghai, Guangzhou, Shenzhen, and Jiangsu, 55 have successfully gone public, a figure that far exceeds the combined total of all other regions.”。

Of course, this is not something that can be achieved overnight. First, as a super-tier-1 city,“Beijing, Shanghai, Guangzhou, Shenzhen, and Suzhou” possess inherent advantages in healthcare investment, boasting well-developed industrial chains and abundant talent pools., which can provide substantial support for the rapid development of healthcare enterprises. In addition, as one of the earliest pioneers in China to adopt the state-owned capital model,“Beijing, Shanghai, Guangzhou, Shenzhen, and Suzhou” are also more market-oriented overall, taking Shenzhen Capital Group as an example, on its very first day of establishment, it selected Kan Zhidong, one of the “three godfathers of China’s securities industry,” as its helmsman due to his “extensive market-oriented experience.” Over the subsequent 25 years, the firm has consistently adhered to market-driven operations, having invested in nearly 200 companies in the healthcare sector and facilitated the successful IPOs of 24 of them.

Also worth mentioning is Yuanhe Holdings, which was established on the groundbreaking day of BioBAY and invested in the first 10 medical enterprises to settle there the following year. As the earliest state-owned capital platform established for BioBAY, Yuanhe Holdings accounted for up to 70% of the investment in early-stage medical enterprises settling in the park, all of which were long-term investments. Driven by this support, BioBAY has risen rapidly, helping Suzhou’s medical industry double its scale within just five years. In 2023, the industrial output value of enterprises above designated size exceeded RMB 200 billion, firmly establishing it as a significant force in China’s medical industry.

In response, a senior investor stated, “For the vast majority of healthcare enterprises today, state-owned capital in the Beijing-Shanghai-Guangzhou-Shenzhen-Suzhou region remains their top priority, as it offers richer industrial resources and a higher degree of market orientation—advantages that are difficult for other regions to match at this stage.。”

However, this does not mean that latecomers have no opportunities at all; cities like Chengdu and Hefei have found their own paths to breakthrough through practical experience.

Let's start with Chengdu.Over the past two years, backed by a cohort of local state-owned capital investors—including Ceyuan Capital, Tianfu International Bio-Town Investment, and the Sichuan Mass Entrepreneurship and Innovation Fund—Chengdu has completed 35 direct investments in the healthcare sector. These efforts have not only incubated and nurtured leading healthcare enterprises such as Keymed Biosciences, Qitan Technology, Ucell Therapeutics, and Yafei Biologics, but also facilitated successful investment promotion for the Tianfu International Bio-Town. Within just two years, the bio-town grew from having no tenants to hosting 300 healthcare companies, directly driving the counter-trend growth of Chengdu’s healthcare industry.

Figure 7. Representative Medical Companies Listed in Chengdu in Recent Years (Graphic by VCBeat)

In response, a head of a state-owned enterprise (SOE) in Chengdu remarked, “In fact, Chengdu’s medical industry started earlier than Suzhou’s. However, its development has been relatively slow due to a greater focus on the IT sector and a long-term lack of commitment from leading funds and enterprises. The rise of Chengdu’s SOEs has undoubtedly revitalized this stagnant landscape. They have targeted a batch of frontier technology companies, providing them with continuous and significant support to foster their growth, which then radiates out to benefit other innovative targets.”

Compared with Chengdu, the rise of Hefei’s state-owned assets carries a more legendary hue.. In fact, Hefei’s state-owned assets gained nationwide prominence as early as 2020, when the Hefei municipal government injected RMB 7 billion to rescue NIO from the brink of collapse. Since then, Hefei’s state-owned capital has sought to replicate this success in the healthcare sector. Over the past two years, state-owned investment entities represented by Hefei Venture Capital, Hefei Industrial Investment, and Hefei High-Tech Investment have completed 21 direct investments in healthcare, increasing their stakes in a number of high-potential companies such as Tongyi Medicine, Zhongsheng Suyuan, Jitong Medical, and Shanhai Semiconductor. Meanwhile, these efforts have attracted leading investment firms including Sequoia Capital, Hillhouse Capital, and Legend Capital to establish a presence in the city, resulting in a particularly notable upward momentum.

In this regard, Hefei state-owned asset personnel attributed their success to the correct strategic path chosen. “Hefei’s medical industry started late, and with major industrial hubs like Suzhou and Shanghai nearby, it is unrealistic to expect rapid, large-scale growth overnight. At our current stage, it is also challenging to attract and secure leading enterprises. Under these circumstances,In recent years, Hefei State-owned Assets has focused on cultivating its own healthcare industry ecosystem, nurturing promising startups within this ecosystem to become chain leaders, thereby integrating the upstream and downstream segments of the industry.。”

Figure 8. Top 10 Direct State-Owned Capital Investments in China’s Healthcare Sector, 2023–2024 (Chart by VCBeat)

Overall, whether for the first-mover cities of Beijing, Shanghai, Guangzhou, Shenzhen, and Suzhou, or the rising stars Chengdu and Hefei, state-owned capital must possess three key elements to truly deliver results in the healthcare sector:First, we must ensure sufficient market orientation, fully respect industry dynamics, and maintain openness. Second, we should prioritize the cultivation of “chain leader” enterprises to build competitive industrial chains and foster synergy between upstream and downstream sectors. Third, we need to fully leverage the industrial guidance role of local state-owned assets and provide resource support to portfolio companies with the utmost sincerity.。

How to Break the Deadlock as State-Owned Capital Enters a Critical Phase of Exit?

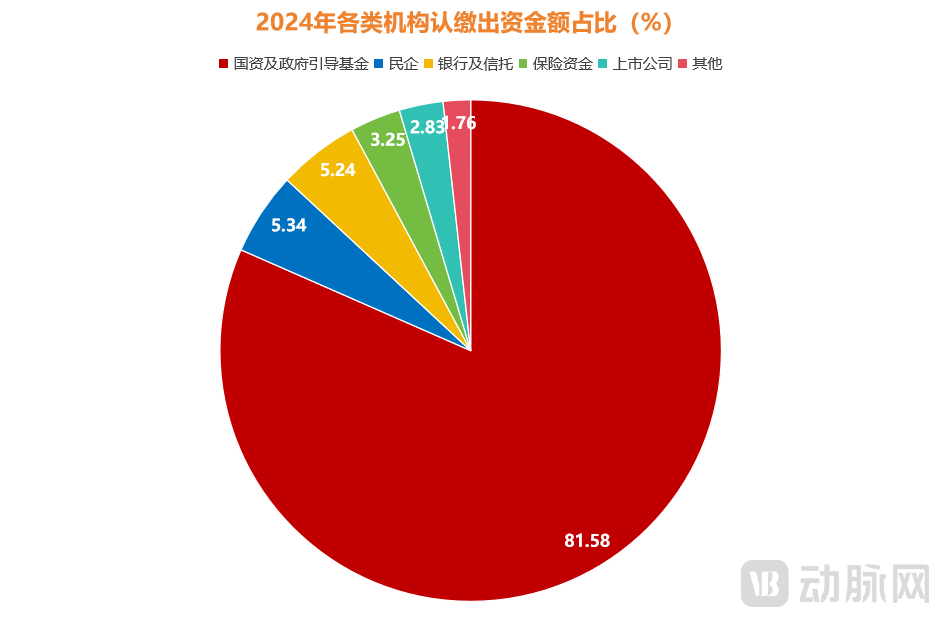

When things reach an extreme, they inevitably reverse; even state-owned capital is not exempt from this law. In the current market landscape, where state-owned investors dominate Series C, D, and even up to Series F funding rounds, accounting for nearly 90% of total fund size, industry-wide issues stemming from state-owned capital have gradually begun to come to the fore.

Figure 9. Proportion of Subscribed Capital Contributions by Institution Type in 2024 (Chart by VCBeat)

The foremost concern is the disruption of natural market selection., the substantial involvement of state-owned capital has delayed the market clearance of certain healthcare projects that should have been eliminated, resulting in significant "ineffective investment."The second is that it has disrupted the equilibrium of the capital market., excessive state-owned capital participation has significantly compressed the survival space of some market-oriented institutions, leading to insufficient enthusiasm among them, and the leveraging function of state-owned capital—“using minimal resources to achieve maximal impact”—has gradually weakened.

The last factor is the “impossible trinity” of state-owned capital, which has increased the difficulty of exit; many state-owned entities are currently facing significant pressure in recovering funds.Specifically, the “impossible triangle” of state-owned capital refers to the inability to balance investment, investment promotion, and risk management. Taking target selection as an example, if a healthcare project lacks significant growth potential but can generate substantial local employment, creating a mismatch between the demands of investment promotion and those of financial investment, how should state-owned capital make its decision? Furthermore, regarding exit horizons, early-stage investments typically have an exit cycle of around 10 years. However, state-owned capital generally requires an exit within 6–8 years, with some even compressing this timeframe to 3–5 years. This discrepancy directly intensifies the pressure on funds to achieve exits.

According to VCBeat's observations, starting from the second half of 2024,News of state-owned capital “blowing up” has been emerging endlessly. Moreover, as some state-owned funds have entered a critical phase of exit, the state-owned capital that was originally intended to fill the void left by USD-denominated funds is now being pushed to the forefront of controversy like never before.。

Fortunately, state-owned capital is already proactively seeking change.

Figure 10. Detailed Rules on Loss Tolerance for State-Owned Capital in Selected Regions (Chart by VCBeat)

Figure 10. Detailed Rules on Loss Tolerance for State-Owned Capital in Selected Regions (Chart by VCBeat)

The first item is “deregulation.”. In July 2024, the Chengdu High-Tech Zone officially released its full-lifecycle investment fund operational system, explicitly setting loss tolerance rates ranging from 30% to 80% for policy-oriented funds such as seed, angel, venture capital, industrial investment, and M&A funds. This marked the first move toward establishing liability exemptions for state-owned capital. Subsequently, regions including Beijing, Shanghai, Guangdong, Zhejiang, and Henan have also made significant efforts regarding “fault tolerance rates,” with continuous emergence of“Up to 100% Loss Tolerance”attempts. The well-intentioned rationale behind this is easy to understand: it aims to break the current dilemma of state-owned capital being “reluctant to invest.”

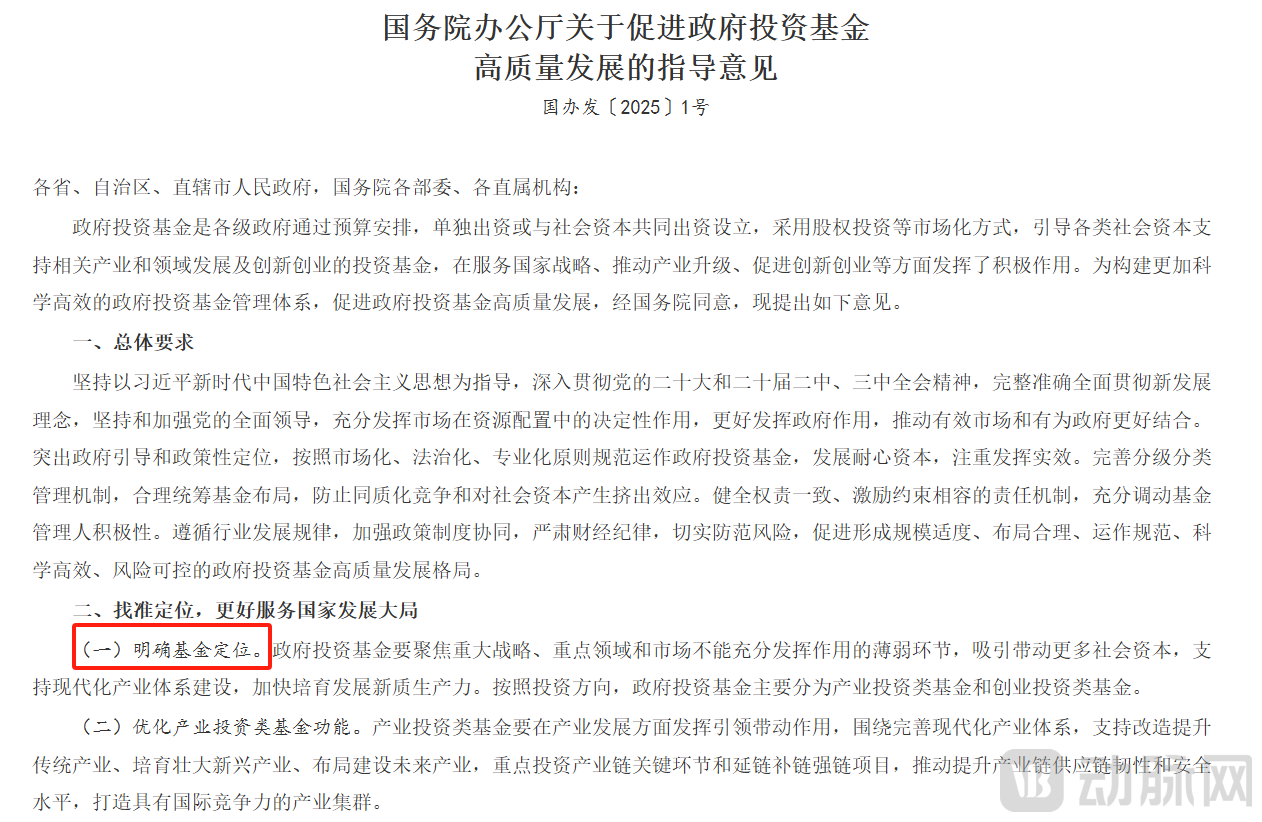

Figure 11. “Guiding Opinions on Promoting the High-Quality Development of Government Investment Funds” (Source: Official Website)

Figure 11. “Guiding Opinions on Promoting the High-Quality Development of Government Investment Funds” (Source: Official Website)

Next, further solidify market positioning and strive to become “patient capital.”At the beginning of 2025, the General Office of the State Council issued the “Guiding Opinions on Promoting High-Quality Development of Government Investment Funds,”This is the first important document issued at the national level to promote the development of government investment funds.. In this document, the first detailed rule is to "clarify the positioning of funds," and subsequent articles also mention tasks such as "tiered classification," "differentiation," and "integration and optimization," directly addressing the drawbacks of state-owned assets, including "overlapping positioning, redundant functions, and fragmented resources."

In this regard, a practitioner who frequently interacts with state-owned assets remarked, “It is not difficult to discern from a recent series of government statements that state-owned capital is currently clarifying its role within the overall equity investment pool, namely, to guide, regulate, and facilitate.”State-owned capital should not be the central protagonist in the primary market, but rather an important regulator and guiding force, effectively directing key funds and core resources toward high-potential enterprises capable of driving structural changes in the industry.。”

Figure 12. Establishment of State-Owned M&A Funds in 2025 (Chart by VCBeat)

Figure 12. Establishment of State-Owned M&A Funds in 2025 (Chart by VCBeat)

The final major change is reflected in exit strategies, with a surge in the popularity of “buyout funds” and “S funds.”. According to data from PharmaCube, by the end of November 2024, the number of M&A transactions involving innovative drugs in China had surpassed the combined total of the previous two years, while the total transaction value exceeded the sum of the preceding three years, reaching as high as $5.882 billion, indicating a highly active M&A market in the country. State-owned capital has clearly recognized this trend and has consequently established numerous “M&A funds.” It is reported that,In the first four months of 2025 alone, the total scale of merger and acquisition (M&A) funds in China approached RMB 1 trillion, facilitating the successful exit of multiple healthcare projects.。

Compared with buyout funds, the establishment of “S funds” is more focused on revitalizing state-owned assets. These funds primarily take over existing local government-guided funds to unlock the liquidity of capital from local fiscal authorities, banks, and other entities—in short, exchanging fund interests for time. According to incomplete statistics from VCBeat, since the second half of 2024, Shanghai, Zhejiang, Anhui, Sichuan, Fujian, Henan, Jiangxi, and other regions have successively announced the establishment of their first S funds, garnering strong industry response.

It is not difficult to see that,State-owned assets are currently undergoing a critical process of self-correction, on one hand paying the price for earlier irrational behavior, and on the other, rapidly clearing out inherent weaknesses such as impure ownership structures, low market orientation, and weak risk resilience.. A frontline employee at a state-owned enterprise also noted this significant change, stating, “Investment promotion personnel used to focus only on their own narrow domains, but now they are beginning to pay attention to companies’ commercial demands and even team building.”

A head of a leading institution predicts that state-owned capital will continue to play a dominant role in the capital market for at least the next five years. This means that, whether for investment institutions or healthcare enterprises,All parties should proactively embrace state-owned capital, avoiding the dead end of fearing it while remaining unable to change the status quo, and instead seek complementary coexistence with the state-owned capital system.Only in this way is it possible to survive the harsh winter and achieve growth against the trend.

Note: All references to “the past two years” in this article collectively refer to 2023 and 2024.

1. “Revisiting ‘Wang Ran’ and ‘State-Owned Capital’ in the Primary Market” – TMTPost;

2. “State-Owned LPs Are Growing Increasingly Confident” – ChinaVenture;

3. “Where Is the Bold State Capital?” — 36Kr