The Battle of Aesthetic Materials Heats Up: Who Will Emerge Victorious?

2025: The Battle for Aesthetic Medicine Materials Officially Begins.

Agarose and hydroxyapatite, two highly anticipated new materials, have each received their first Class III medical device certification. Notably, within a single month, hydroxyapatite saw the consecutive approval of one domestically produced product and one imported product.

Among high-profile developments, recombinant type III humanized collagen gel has received approval, becoming the third Class III medical device certificate for Jinbo Bio and indeed for the entire recombinant collagen sector. Meanwhile, Sihuan Pharmaceutical and Lepu Medical have successively obtained approvals for their “Girl Needle” and “Youth Needle” products. To date, seven “Youth Needle” products and three “Girl Needle” products have been approved in China.

Animal-derived collagen, a relatively niche category in recent years, has also made a comeback—recently, Keruikang Biotechnology’s injectable facial collagen implant was approved.

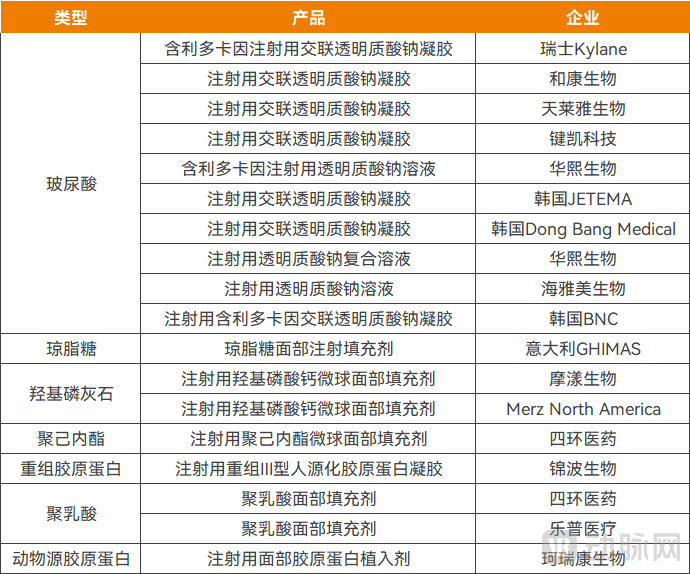

Approval Status of Class III Certificates for Major Medical Aesthetic Materials in 2025, Source: High-End Medical Device Institute Data Center

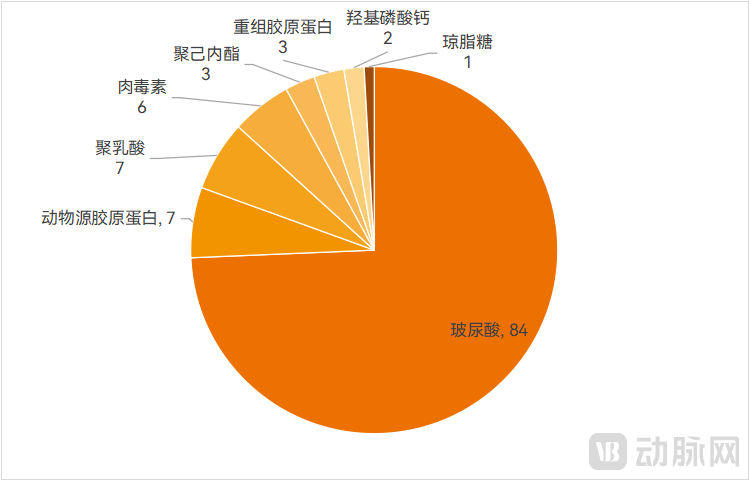

Overall,To date, more than 110 injectable filler products for medical aesthetics have been approved in China (the vast majority are Class III medical devices, while botulinum toxin products hold drug approval numbers). The main materials include seven types such as hyaluronic acid, animal-derived collagen, recombinant collagen, and botulinum toxin. With emerging materials like PDRN, ECM, and chitosan still racing for their initial approvals, the range of medical aesthetic materials is becoming increasingly diverse. As new and existing products compete side by side, a fierce market battle is imminent.

Number of Approved Medical Aesthetic Injectable Filler Products, Source: High-End Medical Device Institute Data Center

As new products continue to roll out, both startups and publicly listed companies are actively positioning themselves in the field of novel materials for medical aesthetics.

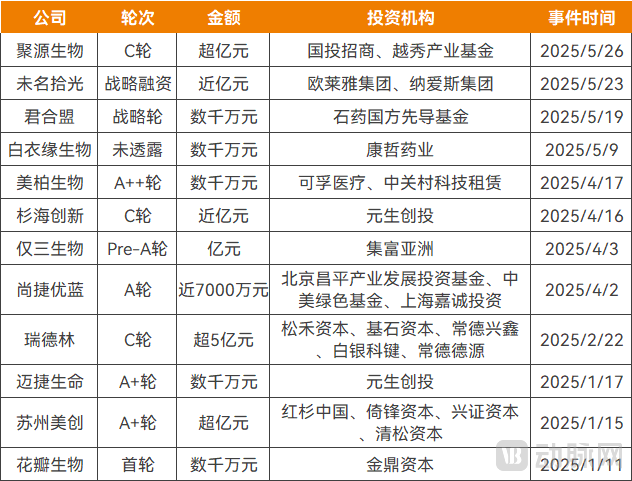

Over the past two years, companies developing new materials for medical aesthetics have been highly favored by investment institutions. In the first five months of 2025 alone, 12 such companies secured financing, primarily in the fields of injectable fillers and functional skincare materials.

Medical Aesthetics Material Companies That Have Secured Financing Since 2025, Source: Public Reports

Among them, Baiyiyuan Biotech has focused on porcine small intestinal submucosa extracellular matrix (SIS-ECM) to research, develop, and manufacture products for tissue repair, wound healing, and regenerative medical aesthetics, with ECM-based solutions currently under development for dermal fillers and skin boosters. Meibo Biotechnology, meanwhile, has established a human-derived ECM platform technology to position itself in the field of regenerative aesthetic materials.

Maijie Life adopts a natural hydroxyapatite technology platform, and clinical trials for multiple indications of its medical aesthetic injectable filler raw materials are currently underway.

In terms of agarose materials, while imported products have received regulatory approval, domestically produced alternatives have also seen significant progress. The injectable agarose gel developed by Huaban Bio entered the clinical trial phase in early 2025.

Publicly listed companies with established products and market channels are also aggressively expanding into new materials.

In 2024, Bloomage Biotech invested in Rigiming Biotech, whose core products are pharmaceutical-grade biological PDRN and PN, the primary ingredients of “salmon injections.” In the same year, Jiangsu Wuzhong made a strategic investment in Lilai Technology, securing exclusive rights to Lilai Technology’s PDRN solution.

Huadong Medicine is advancing the development of KIO015, a novel medical aesthetic filler whose core component is chitosan, a highly purified polysaccharide. Haohai Biological Technology has developed a medical-grade cross-linked chitosan gel, in which the medical chitosan is carboxymethylated chitosan with water-soluble properties.

In 2024, Imeik conducted a total of 21 cross-sectional research projects with medical institutions at all levels in China. In addition to covering existing products, these projects also involved new materials such as PLLA, PDDO, PCL, PVA, and HPMC.

From a functional perspective, the primary applications of numerous new materials focus on: pursuing enhanced safety and reducing the incidence of adverse reactions, with the aim of addressing the “pillow face” phenomenon; achieving superior contouring results to flexibly meet filling needs across different anatomical areas; and exploring more diverse efficacies, such as tissue repair, anti-inflammatory, and antioxidant effects.

Li Chunyan, an investment manager at Jinding Capital, stated that the primary applications of medical aesthetic materials can be summarized into two main categories: one focuses on facial plastic surgery, where rational use enables subtle adjustments to facial contours; the other targets anti-aging, emphasizing the maintenance of a youthful appearance. “New materials and concepts rarely deviate from these two broad categories, with innovations primarily centered on achieving safer and more natural filling effects, or delivering more cost-effective anti-aging benefits.”

It is worth noting that these new materials did not emerge out of nowhere; most have already been applied in medical aesthetic products abroad, or are classified as Class III medical devices in the field of conventional medicine.

For example, PDRN salmon injections have been approved in South Korea for use in medical aesthetic injections; the first imported calcium hydroxyapatite product—Radiesse, under Merz Aesthetics—has been used in medical aesthetics globally for over 20 years and is currently marketed in more than 80 countries and regions. Algeness VL, the first agarose-based product in China, previously obtained EU CE certification and has entered more than 40 countries and regions worldwide.

In China, medical-grade chitosan has been utilized in products such as viscosupplements for intra-articular injection in orthopedics and anti-adhesion agents. In the field of extracellular matrix (ECM), absorbable biological membranes and dural/spinal meningeal biological patches have received regulatory approval. Similarly, silk fibroin-based products, including membrane dressings and hernia repair meshes, have also been approved.

The aforementioned applications have validated the safety and efficacy of the materials, laying a foundation for the research and development pathways and regulatory submission processes of injectable dermal fillers in medical aesthetics.

Overall, new materials for medical aesthetics are emerging in a steady stream, promising to offer more choices for both physicians and consumers.

Products used for medical aesthetic filler injections must obtain a Class III medical device certification, which involves a rigorous research and development approval process.Similar to other sectors, securing the first Class III medical device certification serves as the foundation for a company to gain a first-mover advantage in the market; therefore, product speed—from materials to applications—has become critical.

Since 2021, Jinbo Bio has nearly monopolized the medical aesthetic injection market for recombinant collagen by securing the first Class III medical device certification for such products in China. This achievement has driven rapid growth in the company’s performance, making it a typical case of benefiting from first-mover regulatory approval.

Among new materials in medical aesthetics, calcium hydroxyapatite received its first two Class III medical device approvals in 2025. In February, Moyang Biotech’s Aphranel (Youfulan) was approved, becoming the first compliant calcium hydroxyapatite microsphere facial filler for aesthetic injections in China. In March, another imported calcium hydroxyapatite microsphere facial filler gained approval.

The first agarose-based product also received approval in 2025. In January, Algeness VL, the first agarose-based facial injection filler approved in China, manufactured by Italy’s GHIMAS and distributed by Lanzhou Biological Products, was granted marketing authorization.

Currently, multiple companies are racing to secure the first Class III medical device certification in other new material fields or striving to rank among the top players.

According to information released by Shengzhi Runhe in 2024, its first decellularized matrix bio-gel has completed clinical trials and will be primarily applied in the field of regenerative medical aesthetics. Baiyiyuan Biology’s SIS-ECM-based filler product is nearing the completion of clinical R&D, with the product registration application expected to be submitted in 2025.

Huadong Medicine’s chitosan-based dermal injection filler, KIO021, obtained ethical approval from the lead study site in December 2024 and is expected to receive EU CE certification in 2025, positioning it to become the world’s first non-animal-derived chitosan-based aesthetic filler.

In March 2025, Jiangsu Wuzhong announced that enrollment of all clinical trial participants for its PDRN composite solution product had been completed. The company expects to submit a marketing authorization application in the second half of the year, with approval anticipated within 2026, aiming to secure the first compliant Class III medical device product containing PDRN in China.

On June 5, 2025, the National Medical Products Administration (NMPA) accepted Xingyue Bio’s marketing application for its silk fibroin-containing product. Based on currently available public information, it is poised to become China’s first Class III medical aesthetic injection containing silk fibroin approved for facial indications.

Li Chunyan believes that the current explosive power of the “first certificate” is not as strong as before. “In the past two years,As more companies enter the market, with clear pathways for product development and registration, similar progress timelines, and shortened approval periods, it is becoming increasingly difficult for the “first approved certificate” to enjoy a prolonged period of market exclusivity.“Of course, even if a company is not the first to obtain approval but among the first few, significant market opportunities still exist. Companies must remain vigilant, continue to advance R&D milestones as planned, and avoid delays in their development pipelines or other underperformance.”

From another perspective, the value of being the first approved product is not limited to a specific material field. Previously, Imeik’s “Hearty” (compound sodium hyaluronate solution for injection), the first Class III medical device approved in China for correcting moderate to severe neck wrinkles, also benefited from market advantages. Therefore,Expanding into new indications based on existing materials has become another major strategy in the race to secure the first approval.

Currently, among the approved medical aesthetic injectable fillers, the vast majority of compliant indications are for the nasolabial region, intended for injection into the mid-to-deep dermal layers of the face to correct moderate-to-severe nasolabial folds (i.e., smile lines). A minority of products are indicated for neck lines, glabellar lines, forehead lines, or crow’s feet. Volumizing and contouring products are used for the nose, lips, and chin/jawline.

In the medical aesthetics market, there is already a demand for temporal (i.e., temple) augmentation. However, the complex anatomy and extensive area of the temporal region pose greater challenges to product safety and injection techniques. Achieving a natural and smooth transition requires exceptionally high supporting capacity and moldability from the filler. To date, no product has been approved for compliant use in temporal augmentation.

Huadong Medicine is advancing the expansion of indications for its marketed product, Ellansé (the “Girl’s Needle”), to include the temporal region. In January 2025, the National Medical Products Administration (NMPA) accepted the registration application for Ellansé M-type for the indication of improving temporal hollowing. According to the prospectus of Dongfang Yanmei, the company’s PLLA+HA injectable product XH311 is indicated for temporal hollowing and is currently in the clinical trial stage.

Stretch marks have also been included in the scope of injectable medical aesthetics. For example, Dongfang Yanmei’s investigational product XH312, primarily composed of PEG-PLLA and HA, is indicated for the treatment of stretch marks.

Huaban Biotech’s proprietary agarose injection, AG15, is primarily indicated for soft-tissue wrinkle filling in areas such as the face, neck, and hands, and is poised to become the first “multi-indication” agarose product to enter the market.

Materials can also form differentiated and complementary combinations, with some companies adopting the joint application of materials as a research and development direction to achieve stronger product competitiveness.

Furthermore, innovative drug delivery methods represent another avenue for capturing new markets.In 2025, among the botulinum toxin products jointly developed by Haohai Biological Technology and Eirion (USA), the topical botulinum toxin product entered Phase III clinical trials, with plans to initiate Phase III trials in China and the United States simultaneously. This product reduces injection pain and lowers the barrier to administration by combining microneedle-based skin pretreatment with an emulsion formulation.

Furthermore, according to data from the National Medical Products Administration (NMPA), in addition to the materials mentioned above, a growing number of new medical aesthetic materials have completed master file registration over the past two years.This includes Meishangjie’s injection-grade recombinant humanized type XVII collagen and injection-grade recombinant humanized type I collagen, Huaqing Zhimei’s injectable 3D bioprinted human-derived acellular extracellular matrix material, and Aipurui Nano’s β-tricalcium phosphate for cosmetic injection, which has also accelerated the approval of Class III medical device registrations in these respective niche sectors.

Undoubtedly,Future competition in the medical aesthetics market will not merely be a battle for market share between two specific materials; rather, it will involve intertwined competition among multiple materials, across different companies specializing in niche materials, and between various product variants indicated for the same clinical application.

Obtaining regulatory approvals for various materials is merely the beginning; post-launch, products still face marketing challenges, which are even more daunting for startups.

Medical aesthetic injectable fillers are characterized by high unit prices and significant impacts on facial appearance, leading to prolonged consumer decision-making cycles. New products based on novel materials require extensive, long-term market education and brand promotion to build consumer trust. Additionally, it is essential to collaborate with medical institutions to conduct large-scale physician training programs that standardize injection techniques and establish criteria for evaluating treatment outcomes.

“While early-stage projects in the current medical aesthetics market tend to prioritize R&D, building capabilities in marketing and sales is equally crucial. High-quality marketing resources come with a high barrier to entry; companies need to integrate such resources at key junctures through strategies like offering competitive salaries or supporting independent operations,” remarked Li Chunyan.

In her view,For individual materials, a trend of bidirectional integration between medical aesthetics and cosmetic skincare applications is likely to emerge, similar to past patterns. For instance, after injectable medical aesthetic products receive regulatory approval for use, the material’s concept can drive the popularity of consumer-facing skincare products; conversely, as cosmetics companies further expand the influence of these materials, they channel consumer demand back into the medical aesthetics market.“Once a positive feedback loop is established between medical aesthetics and consumer demand, the market size for specific materials will expand rapidly. Alongside this market growth, in addition to leading enterprises represented by listed companies, mid-sized firms with certain R&D capabilities or channel resources may enter through niche scenarios, thereby building differentiated competitiveness. As technologies in the medical aesthetics industry continue to advance and solutions undergo continuous iterative innovation, we look forward to the emergence of more high-quality products in the market!”

It is understood that various new materials, including PDRN, hydroxyapatite, and silk fibroin, are currently being explored for applications in medical aesthetic injections, functional skincare, and even personal health care.

In any case, safety and efficacy remain the perennial themes in medical aesthetic materials and products.In the competitive landscape where established and novel materials coexist, legacy materials benefit from prolonged application histories and more extensive clinical validation. While new materials offer fresh options driven by innovative functionalities, the advantages demonstrated in clinical trials require further substantiation through real-world application.

Ultimately, who will dominate the market? Only time will tell, as true product strength speaks for itself.