Behind the Surge: Hidden Crises in China's Booming Surgical Robot Market

From January to May 2025, 150 surgical robots were awarded in bids in China,+82.9% YoY. After a year of slowing growth, the surgical robotics market has finally resumed its rapid surge.

However, amid the booming market, there have also been reports of “voluntary divestitures and bankruptcy liquidations.”

In early June, UK surgical robotics company CMR Surgical announced that it was “seeking sale opportunities.” Just two months prior, the company had closed a new funding round of more than $200 million to support the global market rollout of its core product, the Versius surgical robot.

Almost simultaneously, a Chinese vascular interventional surgery robotics company was auctioned off in bankruptcy proceedings. It is reported that the company had previously secured tens of millions of yuan in financing, and its developed vascular interventional surgery robot had completed animal studies and initiated clinical trials in early 2023.

Amidst a Market Surge and Bankruptcy Liquidations, What Is Happening to the Surgical Robotics Industry? What Crises Lurk in the Surgical Robotics Market?

After years of development, the crisis in the surgical robotics industry has begun to gradually emerge.

First, the surgical robotics industry is characterized by intense competition.To date, a large number of domestic companies are competing in each segment of the surgical robot market. For instance, approximately 16 laparoscopic surgical robots have received regulatory approval in China, more than 50 orthopedic surgical robots have been approved, and over 10 needle-insertion surgical robots have gained approval...

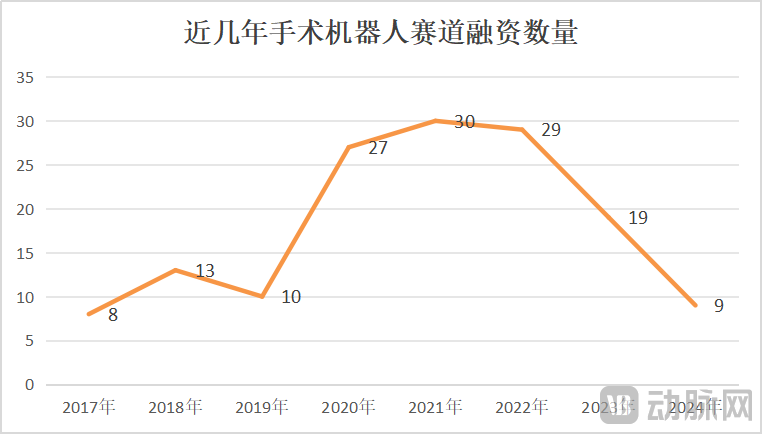

Second, the amount and number of financings have sharply declined, and some surgical robotics companies that have not yet generated commercial revenue will face a funding crisis.From 2020 to 2022, China’s surgical robotics industry completed 27, 30, and 29 financing deals, respectively. The influx of substantial capital and the entry of numerous innovative enterprises have intensified competition in this high-barrier sector.

However, the capital market has returned to rationality. In 2024, the surgical robotics industry completed only nine financing rounds. It is foreseeable that as funding dries up and investor activity declines, surgical robotics companies that have yet to generate commercial revenue will face a liquidity crisis. As a result, more surgical robotics companies may fade from the scene.

Third, some surgical robots are only suitable for simple lesions, and their clinical value has yet to achieve a breakthrough.Recently, the peer-reviewed medical journal JSCAI, published by the Society for Cardiovascular Angiography and Interventions (SCAI), released a study. This study aggregated clinical research findings on two generations of the CorPath vascular interventional surgical robots, encompassing a total of 1,734 robot-assisted percutaneous coronary intervention (PCI) procedures. The results indicated that procedural success rates for both generations of surgical robots exceeded 96%, while technical success rates were approximately 89%.

Zhang Yi, Director of the Pan-Vascular Disease Center and the Hypertension Center at Shanghai Tenth People’s Hospital, commented on the study, stating, “In clinical practice behind the data,”Currently, the symbolic significance of coronary intervention surgical robots in coronary procedures outweighs their practical value, as these systems are still far from capable of handling complex coronary interventions. In robot-assisted procedures for simple lesions, 11% require conversion to manual operation.。”

Director Zhang Yi also stated, “Interventional surgical robots represent a key strategic field. Following future technological breakthroughs, the advantages of robotic arms can be leveraged to assist operators in performing specific lesion interventions. While this may require further research, continued practice and exploration are essential.”

Fourth, the surgical robot market is engaged in a price war.Currently, surgical robots launched by companies such as MicroPort MedBot, Tinavi, Sizrui, Edge Medical, Yida Health, and Jianjia Medical have all achieved commercial installation. To accelerate market penetration, some of these companies have even engaged in price wars.

Previously, Sizrui’s SR1000 laparoscopic surgical robot won a bid at RMB 5.38 million; laparoscopic surgical robots from companies such as Edge Medical and MicroPort MedBot were awarded contracts at prices ranging from RMB 14 million to RMB 17 million. In contrast, the da Vinci Surgical Robot, which holds the largest market share, has an average price of approximately RMB 23 million.

Even amid a price war, the da Vinci Surgical System’s market position remained unshaken. In 2024, 58 new da Vinci units—with an average price exceeding RMB 20 million—were installed in China, keeping it at the top of the domestic laparoscopic surgical robot sales rankings. By contrast, domestically produced surgical robots, with an average price below RMB 10 million, recorded combined sales of 33 units, while models priced at around RMB 15 million achieved sales of approximately 29 units.

This indicates that domestic hospitals in China are less price-sensitive toward surgical robots than previously assumed. Low-priced products do not necessarily achieve high sales volumes, nor do high-priced ones inevitably suffer from low sales; instead, hospitals prioritize the performance and quality of surgical robotic systems. The orthopedic surgical robot market further validates this perspective. For instance, Tinavi’s orthopedic surgical robots are priced 19% above the market average, yet the company still commands a 50% market share.How to Break Through the Market Remains a Tough Challenge for Some Companies。

Fifth, the commercialization of surgical robots is significantly influenced by policy and macroeconomic factors.In 2024, the domestic surgical robot market in China experienced phased performance pressure due to factors such as anti-corruption campaigns in the pharmaceutical and medical sectors and a slowdown in tendering and bidding processes. For instance, Tinavi’s orthopedic surgical robots saw sales drop by nearly 50% in 2024, with total revenue declining by 14.9% to RMB 179 million.

However, with the growth in the number of robot-assisted surgeries, Tinavi’s revenue from supporting equipment and consumables and from technical services increased by 28.52% and 104.26% year-on-year, respectively. In 2024, the annual surgical volume of Tinavi’s Tiangji series orthopedic surgical robots exceeded 39,000 cases, representing a 62.5% year-on-year increase.

Additionally,Since 2025, with the resumption of bidding processes and a surge in market demand, the surgical robot market has also demonstrated rapid growth. For instance, Tinavi Medical Technologies reported Q1 2025 revenue of RMB 58.58 million, representing a year-on-year increase of over 102.40%.。

Overall, some surgical robotics companies have entered bankruptcy and liquidation, primarily due to intense competition and product homogenization. The lengthy R&D cycle for surgical robots means that even after securing financing during peak capital availability, these companies struggle to rapidly transition to commercialization and generate revenue. In particular, following Siemens Healthineers’ announcement of its exit from the coronary interventional surgical robotics business, investment and financing in this niche market have nearly stalled. This has forced surgical robotics companies that have lost access to funding and failed to achieve commercial revenue into bankruptcy and liquidation.

Surgical robotics companies that have obtained product approvals and secured commercial orders—including those specializing in vascular intervention surgical robots—are poised to leverage their first-mover advantage, strengths in marketing and distribution channels, and product differentiation to generate commercial revenue early on. This will enable them to validate their business models, garner greater support from investors, and utilize financing proceeds to accelerate market expansion and enhance overall competitiveness.

While companies can only react passively to the industry landscape, investment trends, and policy directions, they are actively addressing operational challenges—such as product value, market promotion, and development strategy—through a variety of measures.

First is technological innovation.Currently, surgical robots are innovating in the following directions:

First, robotics technology is being integrated with AI technology.AI technology applied to surgical robots can drive robot-assisted surgery toward being less invasive, more intelligent, and increasingly autonomous. At present, companies such as Allpeth Medical, MicroPort MedBot, Tinavi, Edge Medical, and Zhuoye Medical have all deployed AI technologies or integrated AI into their existing surgical robot products.

Taking Jingfeng Medical as an example, its CP1000 Jingfeng Bronchoscopy Robot is a fully flexible bronchoscopy robot equipped with AI navigation, ultra-flexible robotic arms, and robotic control technology. It enables operators to guide the robotic bronchoscope along preoperatively planned paths to peripheral targets using a control joystick, thereby achieving precise diagnosis and treatment of lesions deep within the lungs.

Meanwhile, some enterprises and institutions are also considering partnerships with companies possessing leading AI technologies to develop AI-powered surgical robots. For instance, Tuodao Medical has signed a cooperation agreement with Huawei Cloud to engage in in-depth collaboration on surgical robots and jointly promote technological innovation in smart healthcare. Wuhan Central Hospital is partnering with Infervision to develop AI surgical robots and establish a demonstration base for digital and intelligent surgery.

Second, reduce product costs,Making surgical robots more “affordable to purchase and operate” for hospitals. For instance, Ruilong Surgical independently developed the Haishan Yi endoscopic surgical robot, the first modular surgical robot in China approved for full indications across four major specialties. Its split-type structure and modular design allow hospitals to select the number and models of console carts according to their needs, enabling rapid deployment without site modifications. The robot is also compatible with conventional laparoscopic instruments, reducing reliance on proprietary consumables and lowering procurement costs.

Third, 5G + remote technology.Tele-robotics helps facilitate the decentralization of high-quality medical resources and promotes tiered diagnosis and treatment. To date, companies such as MicroPort MedBot, Tinavi Medical Technologies, Edge Medical, ShuRui Medical, and Zhuoye Medical have all explored remote robotic surgery. For instance, the Toumai surgical robot has completed nearly 400 remote robotic procedures on human patients; the Jingfeng multi-port surgical robot conducted nearly 200 exploratory remote surgeries in 2024; and Tinavi Medical has cumulatively performed over 1,000 remote orthopedic robotic surgeries.

Among these, MicroPort MedBot’s Toumai remote surgical robot received the world’s first regulatory approval for market launch in April 2025. Reportedly, the Toumai robot has established the first and only intercontinental remote surgery network system, covering six continents and 103 countries and regions, with transmission distances approaching 800,000 kilometers. There are over 120 active remote surgical robot sites, with nearly 400 remote robotic surgeries performed on human patients, alongside hundreds of animal experiments and surgical procedure validations completed.

In September 2024, Edge Medical also launched the Jingfeng Cloud Remote Surgery System and fully initiated the “Thousand-Member Medical Alliance Program,” establishing a new intelligent remote surgery network platform featuring real-time multi-point interconnectivity.

Fourth, expand indications to increase the volume of robotic surgeries.Previously, a surgical robot was mainly applicable to one department or one indication, with a limited scope of clinical application, which greatly restricted the willingness to purchase. However, at present, the application range of individual surgical robot devices is continuously expanding.

For example, in May 2025, the indicated uses for the ShuRui single-port laparoscopic surgical robot were updated to “for use in urological, gynecological, general surgical, and thoracic pulmonary laparoscopic procedures,” making it the first and only single-port surgical robot in China to cover all four major surgical specialties.

The Jingfeng multi-port surgical robot has also gradually expanded into multiple fields, including urology, gynecology, thoracic surgery, and general surgery, and is applicable to nearly 340 types of surgical procedures.

Additionally, Lancet Robotics, which has just completed a financing round worth tens of millions of yuan, plans to use the funds to drive innovation and localization in cross-departmental surgical robots. Currently, several of its cross-departmental surgical robot products, including those for minimally invasive tumor intervention and neurosurgery, are undergoing registration with the NMPA and FDA.

Fifth, surgical robots are being utilized for more complex surgical procedures.In clinical practice, Level 4 surgeries are the most difficult, complex, and highest-risk procedures among surgical operations, imposing extremely high requirements on surgeons. Currently, innovative enterprises have gradually expanded the application scope of surgical robots to include Level 4 surgeries, helping surgeons reduce operational difficulty, enhance surgical safety, and increase the clinical value of surgical robots.

For example, by the end of May 2025, the cumulative number of procedures performed using the Jingfeng multi-port surgical robot had exceeded 8,000, with 7,760 being Level 4 high-difficulty surgeries, accounting for as high as 97%. The remaining procedures were all Level 3 surgeries.

Furthermore, a growing number of innovative enterprises are collaborating with medical institutions to explore more complex surgical procedures. For instance, Professor Zhang Yixin’s team at Shanghai Ninth People’s Hospital, Shanghai Jiao Tong University School of Medicine, performed the world’s first robot-assisted radical resection and reconstruction for complex elbow tumors using the Kai microsurgical robot developed by Ontai Weijing. Additionally, Professor Wu Wenhan’s team at Peking University First Hospital successfully completed a robot-assisted pancreaticoduodenectomy using the Kangduo Robot (pancreaticoduodenectomy is one of the most complex surgeries for treating diseases such as pancreatic head cancer)...

Secondly, to cope with intense domestic competition and expand market opportunities, an increasing number of surgical robotics companies are accelerating their global expansion.

For example, against the backdrop of a slowdown in China’s surgical robot market in 2024, MicroPort MedBot achieved revenue of RMB 257 million, a year-on-year increase of 146%, by pursuing a dual-pronged strategy targeting both domestic and overseas markets. Its laparoscopic surgical robot, Toumai, secured 39 new orders, including more than 20 commercial orders from international markets. These international orders provided strong momentum for its performance growth.

Edge Medical is also accelerating its international strategic layout. In March 2025, Edge Medical partnered with Meden-Inmed, a long-established medical group in Poland, to establish its first surgical robot training center in Europe in Warsaw, Poland. The center will undertake three core functions: technical training, clinical demonstration, and academic exchange.

Meanwhile, Edge Medical has partnered with Dornier MedTech, a global leader in urological medical devices. Leveraging Dornier MedTech’s mature network channels and support systems, Edge Medical is promoting its multi-port laparoscopic surgical robot system in Spain and Portugal.

Previously, Edge Medical Robotics had also reached a cooperation agreement with the Egyptian Healthcare Authority in multiple areas, including the application and training of surgical robots, as well as the development and utilization of robotic telesurgery systems.

In addition, multiple surgical robot companies, including Huiwei Kang (Platon), Shurui Robotics, Tinavi, and Gerui Technology, are accelerating their global expansion.

Finally, surgical robot companies are beginning to penetrate county-level hospitals.Declining costs have alleviated the financial burden on county-level hospitals, while the integration of AI and remote surgery technologies has addressed the shortage of physicians skilled in operating surgical robots. Under these circumstances, some county-level hospitals have begun procuring surgical robots.

For example, county-level hospitals such as the First People’s Hospital of Xiushui County, Jingxing County Hospital, and Guangning County People’s Hospital have procured laparoscopic surgical robots; Cengong County People’s Hospital, Huidong County People’s Hospital, Xianju County People’s Hospital, and the Affiliated Traditional Chinese Medicine Hospital of Chongqing Three Gorges Medical College have procured orthopedic surgical robots; Yunyang County People’s Hospital has procured neurosurgical surgical robots, among others.

Among them, county-level hospitals such as Huidong County People's Hospital and Guangning County People's Hospital have procured surgical robots equipped with remote surgery technology and have successfully completed their first local remote robotic surgeries. Through this technology, patients at county-level hospitals can access high-quality medical resources from thousands of miles away. For instance, the first "5G + orthopedic surgical robot" remote total knee arthroplasty performed in Huidong County was assisted by Professor Sheng Puyi’s team from the First Affiliated Hospital of Sun Yat-sen University. The first remote surgery in Guangning County was conducted by a team from Zhujiang Hospital of Southern Medical University.

As surgical robots are deployed at the grassroots level, county-level hospitals can perform more complex procedures, enhancing their medical service capabilities and allowing patients to receive treatment locally without traveling to distant cities. For instance, after introducing the da Vinci Surgical System, Dazu District in Chongqing has gradually mastered high-difficulty procedures such as heart valve replacement, mediastinal tumor resection, radical lung cancer surgery, and radical esophageal cancer surgery. Complex cases that previously required referral to higher-tier hospitals can now be diagnosed and treated within Dazu District, reducing the burden on patients from the local area and surrounding districts and counties.

Driven by initiatives such as product innovation, accelerated global expansion, and deployment at the primary care level, domestic surgical robot manufacturers are expected to further raise the market ceiling and accelerate market growth.