Chinese Pharmaceutical Companies Enter the Arena of Long-Acting Ophthalmic Therapies Amid Intensifying Competition

The Fundus Therapy Market Is Breeding a Major Transformation.

In late May, new anti-VEGF drugs from Bayer and Novartis were successively approved in China, bringing a fresh dynamic to the market after a decade of dominance by traditional anti-VEGF therapies in the treatment of fundus diseases.

In recent years, with the successive introduction of dual-target drugs (faricimab), long-acting formulations (brolucizumab), and gene therapies (such as AAV vector-based drugs), the treatment cycle for fundus diseases has extended from “monthly injections” to “quarterly injections.” This revolution in efficacy and patient adherence is reshaping clinical standards. Coupled with support from medical insurance coverage, this trend has enabled the continuous release of incremental market growth.

The competition in the fundus drug market, driven by the three dimensions of technology, price, and distribution channels, is shifting from cutthroat “red ocean” rivalry to value reconstruction. Only companies that break through the paradigm of “follow-on innovation” can secure the commanding heights of the market.

Ranibizumab, on the market for over a decade, is beginning to show signs of fatigue.

Relying on the advantages of being the originator and a first-mover, Novartis’s ranibizumab had firmly held the top position in China’s fundus disease treatment market. However, the market landscape has shifted with the continuous emergence of competitors. From Kanghong (conbercept) and Bayer (aflibercept) to the entry of Roche (faricimab), approved in 2024, and Qilu Pharmaceutical (biosimilars of aflibercept and ranibizumab), ranibizumab is now struggling to cope.

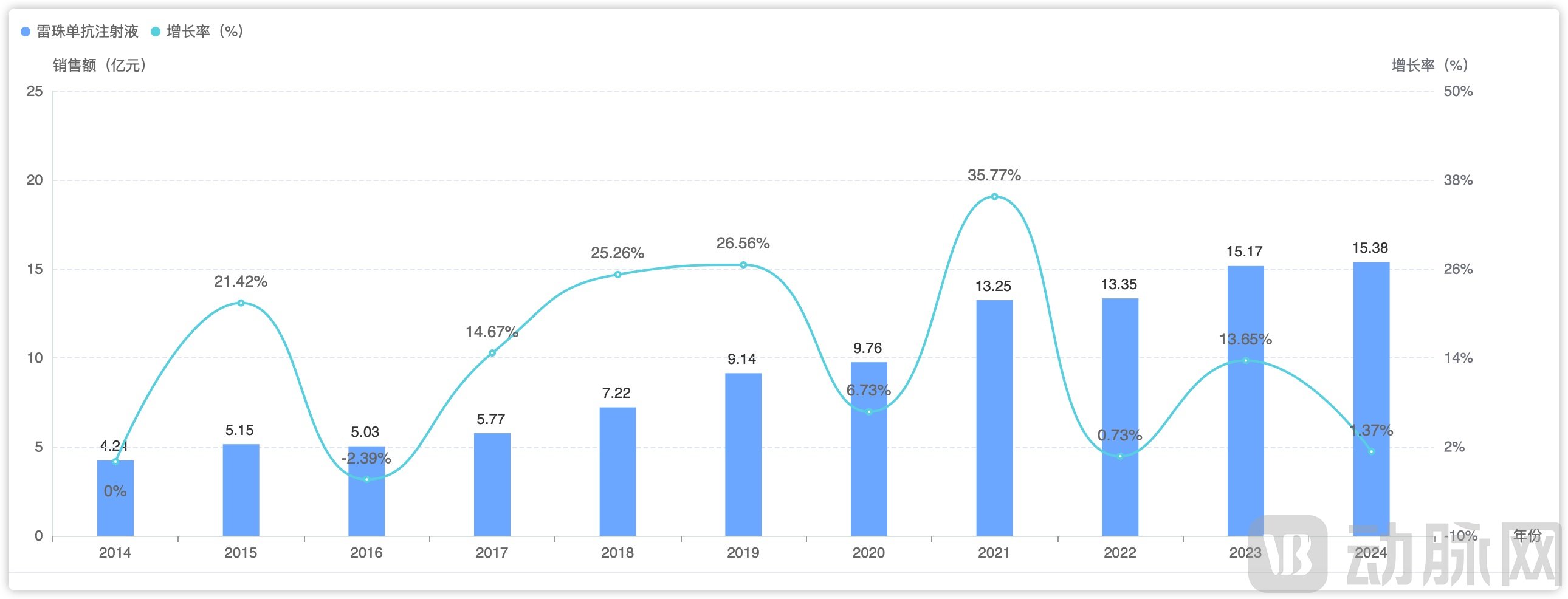

Ranibizumab’s Sales Performance and Growth Rate Over the Past Decade, Source: Minseng Pharma

According to data from PharmCube, the sales growth of ranibizumab has begun to slow after a decade of rapid expansion. Although it still achieved a year-on-year increase of 1.37% in 2024, this rate represents a significant decline compared to the previous growth rates of 20–30%. In addition to competition from external rivals, ranibizumab is facing pressure from biosimilars. Qilu Pharmaceutical’s ranibizumab injection has already received approval, while Huadong Medicine’s product is currently under review. The entry of these competitors is expected to further erode its market share.

Novartis’s market dominance with ranibizumab has begun to weaken.

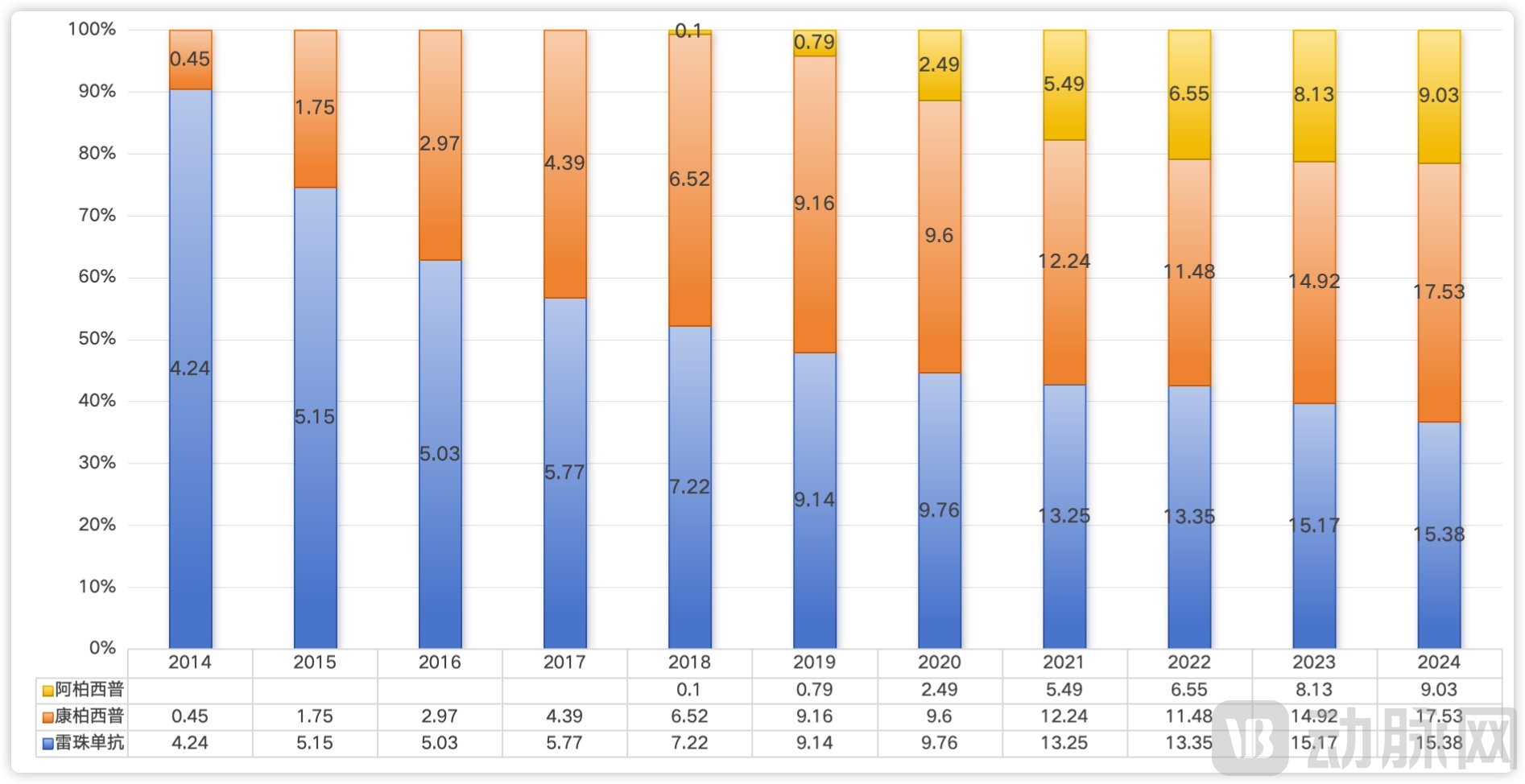

On the other hand, competitors have also delivered strong performance. Kanghong Pharmaceutical’s conbercept has maintained a high growth rate, with a year-on-year increase of 17.53% in 2024. Compared with ranibizumab, conbercept is priced lower; initially launched at approximately RMB 6,800 per vial, its price has been reduced continuously, falling to less than 50% of the initial launch price after being included in the National Reimbursement Drug List. In addition, conbercept requires fewer injections per year than ranibizumab, which has enabled its rapid gain in market share in China, ultimately surpassing ranibizumab.

Changes in Market Share of Three Drugs, Data Source: Menet Pharma

Subsequently, the entry of Bayer’s aflibercept has intensified competition to a fever pitch. Since receiving domestic approval in 2018 and being included in the National Reimbursement Drug List in 2019, aflibercept’s sales have surged dramatically, exceeding RMB 900 million in 2024. Of greater note is that, with the expiration of aflibercept’s patent, numerous Chinese companies have laid out plans for biosimilars, among which Qilu Pharmaceutical has made the fastest progress, obtaining approval at the end of 2023.

In 2024, Qilu Pharmaceutical’s aflibercept was officially launched. Although its overall sales volume was not particularly high, its quarter-on-quarter growth rate was quite remarkable. Moreover, it is not only Qilu Pharmaceutical that is active in this space; the aflibercept intravitreal injection solution, jointly developed by Ocumension Therapeutics and Boan Biotech, has also entered the approval stage. Meanwhile, related biosimilars from Mabwell Bioscience and Jingze Biopharma are in Phase III clinical trials, with several other domestic biosimilars currently under development. The market entry of biosimilars typically leads to lower prices, which will inevitably further intensify competition.

In addition to domestic pharmaceutical companies, MNCs are also entering this competitive landscape.

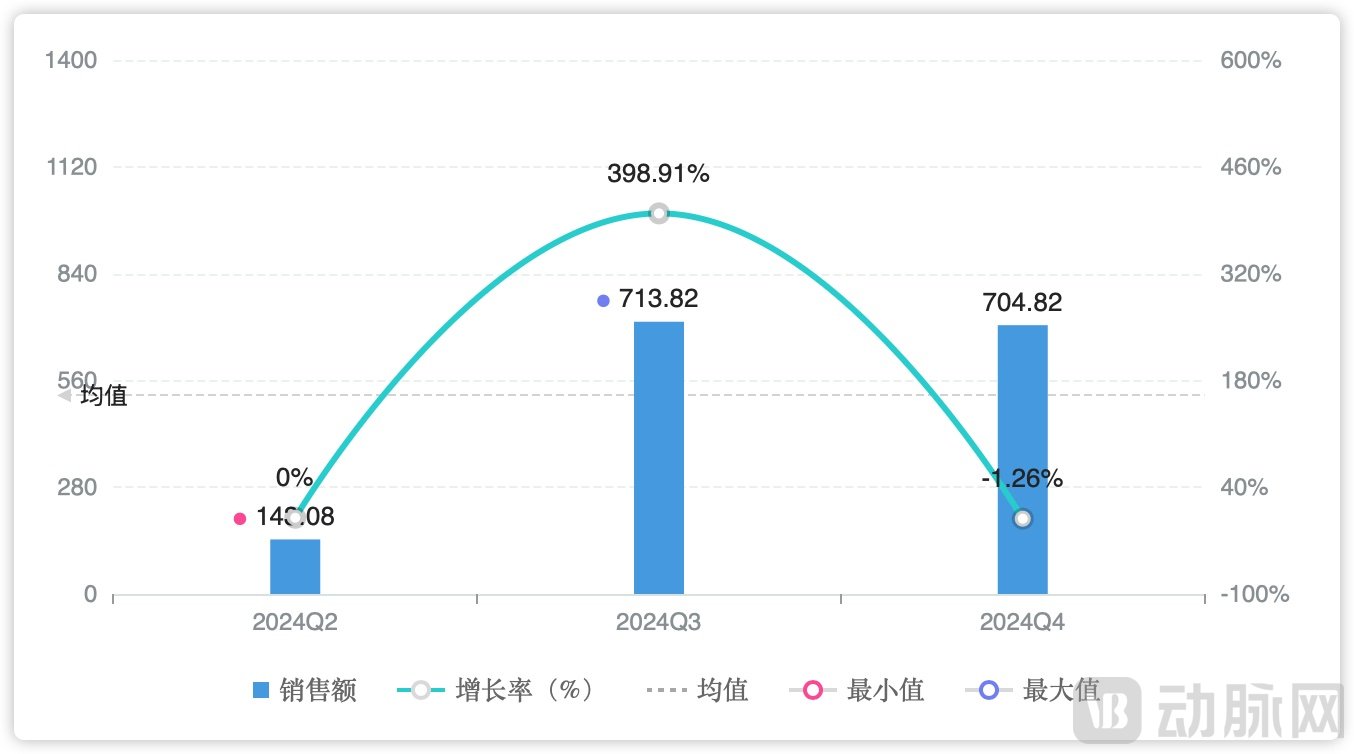

Roche’s faricimab is the world’s first dual-antibody drug for retinal diseases. After receiving approval in the United States in 2022, it was approved in China at the end of 2023. Since its launch, faricimab has rapidly gained market traction, with global sales exceeding $4 billion in 2024. Although its market share in China remained relatively low during the first year post-launch, its quarter-over-quarter growth rate has been remarkably impressive, even at a unit price of RMB 9,000 per dose.

It is worth noting that, starting in 2025, faricimab has been included in the National Reimbursement Drug List, with its price reduced to RMB 3,608. This means that a rapid surge in the volume of faricimab prescriptions this year is inevitable, and the existing market landscape will undoubtedly face significant disruption.

Faricimab’s First-Year Sales Performance; Source: Mordor Intelligence

Overall, after years of prominence, ranibizumab has lost momentum and its market dominance has significantly waned. Drugs such as conbercept and aflibercept have posed substantial challenges, particularly with the launch of more aflibercept biosimilars and the inclusion of faricimab in the national reimbursement drug list, which will further reshape the market landscape.

Amidst this period of profound transformation, companies are making their moves to cope with increasingly fierce competition.

Differentiating from existing drugs to become the preferred choice for pharmaceutical companies.

May was a particularly dynamic month for the fundus treatment market. On May 22, the National Medical Products Administration (NMPA) approved Bayer’s aflibercept (8 mg) for the treatment of neovascular (wet) age-related macular degeneration (nAMD). Compared with the previous 2 mg formulation, the higher-dose version is approved for initial monthly injections over three months, after which the dosing interval may be extended to once every four months, based on the physician’s judgment.

On May 23, Roche’s Susvimo (ranibizumab) 100 mg/mL was also approved by the FDA for marketing. Its distinguishing feature is a treatment regimen for diabetic retinopathy that requires only one refill every nine months.

In response to the waning market competitiveness of ranibizumab, Novartis has introduced brolucizumab, which received approval in China in late May. Novartis aims to reshape the treatment landscape for diabetic macular edema (DME) and usher in a new era of high-efficacy therapy by leveraging the unique properties conferred by its small-molecule structure and the advantage of an ultra-long dosing interval.

Comparison of Drug Dosing Intervals, Compiled from Publicly Available Data

Currently, the molecular weights of aflibercept, which is based on a fusion protein structure comprising the extracellular domain of VEGF receptors and the human IgG1 Fc fragment, and faricimab, which is developed using a bispecific antibody technology platform, are 115 kDa and 150 kDa, respectively. Studies have shown that the maximum molecular weight for free diffusion in the human retina is approximately 76.5 kDa. In other words, these large-molecule drugs face certain intractable challenges, such as limited penetration into deep retinal tissues due to the retinal tissue barrier, resulting in insufficient effective concentrations at the target site; increased cardiovascular risk when Fc fragments bind to receptors on the surface of intraocular immune cells and enter systemic circulation; and the mechanism of action of the Ang-2 pathway in the dual-pathway inhibition strategy remains not fully elucidated.

A competitor's weaknesses are, of course, an excellent entry point for differentiation.

Novartis’s brolucizumab consists solely of the antibody heavy-chain variable region (VH) and light-chain variable region (VL) connected by a flexible peptide linker, forming an ultra-compact protein structure with a molecular weight of only 26 kDa.

Unlike the Fc fragments of traditional antibodies, which may trigger immune-related side effects, this design retains only the minimal functional unit required for antigen recognition while maintaining full target-binding capacity. Its ultra-low molecular weight facilitates rapid penetration, enabling efficient crossing of the retinal pigment epithelium barrier and the internal limiting membrane barrier, thereby offering a new avenue for ophthalmic therapy.

In simple terms, through its specialized structural design, brolucizumab addresses three key dimensions—penetration capability, concentration control, and high affinity. In comparison with aflibercept and faricimab, it achieves both a faster onset of action and a prolonged duration of effect, thereby positioning itself strongly for future market competition.

In the realm of long-acting pharmaceuticals, not only multinational corporations (MNCs) but also domestic pharmaceutical companies are continuously intensifying their efforts to accelerate R&D processes.

Chinese pharmaceutical companies are starting to take their seat at the table.

Historically, domestically produced anti-VEGF drugs have been primarily focused on the development of biosimilars, particularly as key patents for aflibercept have successively expired, attracting numerous pharmaceutical companies to enter the field. However, not all enterprises are content to merely play catch-up. A growing number of companies recognize that to capture a share of the retinal disease treatment market, they need products with breakthrough value and truly innovative mechanisms of action.

At the ARVO 2025 (Association for Research in Vision and Ophthalmology) Annual Meeting, Innovent Biologics and RemeGen Co., Ltd. respectively delivered oral presentations on significant advancements in their respective drug pipelines, marking a new phase for domestically produced anti-VEGF ophthalmic drugs—from imitation and follow-on development to innovative competition.

At the annual meeting, Innovent announced the Phase II clinical trial data (NCT05403749) for its global first-in-class dual-target drug targeting VEGFR and C1, emovoprod (IBI302). The study lasted 52 weeks, with the primary endpoint being the change from baseline in best-corrected visual acuity (BCVA) score of the study eye at Week 40. IBI302 incorporates a C-terminal complement-binding domain in addition to the conventional VEGF-binding domain, thereby inhibiting inflammation mediated by mild complement activation. This design enables simultaneous inhibition of VEGF-mediated neovascularization and the complement activation pathway.

Overall, the study achieved its primary objectives. In terms of dosing intervals, more than 80% of subjects in the IBI302 group were able to maintain visual acuity benefits with a Q12W dosing regimen (compared to Q8W for aflibercept). The magnitude of visual acuity improvement was comparable to that of aflibercept, and anatomical efficacy endpoints showed improvement. More importantly, regarding the trend toward benefit in preventing geographic atrophy, the incidence of new-onset geographic atrophy at one year was 4.9% in the IBI302 group versus 8.3% in the aflibercept group. This represents a 40% reduction in the incidence of new-onset cases with IBI302 treatment compared to the aflibercept group, demonstrating its potential to inhibit geographic atrophy.

Shortly after its debut at the ARVO conference, Innovent announced that the first patient had been dosed in the Phase II clinical study of IBI302 for diabetic macular edema. The company stated that it aims to challenge the current highest global treatment standard in this field by conducting a head-to-head clinical trial against Roche’s faricimab, another dual-target innovative drug. This move underscores Innovent’s confidence in IBI302.

Following Innovent, RemeGen also unveiled its independently developed, first-in-class dual-target fusion protein drug RC28, which targets VEGF and FGF, at the annual conference. By simultaneously inhibiting the vascular endothelial growth factor (VEGF) and fibroblast growth factor-2 (FGF-2) pathways, RC28 has demonstrated superior clinical efficacy. Additionally, the humanized design of RC28 effectively extends its half-life, reduces dosing frequency, and alleviates patient discomfort.

Currently, RC28 is undergoing Phase 3 head-to-head trials against aflibercept for the indication of diabetic macular edema (DME). Additionally, a Phase 3 clinical trial comparing RC28 head-to-head with aflibercept for age-related macular degeneration (AMD) is also underway. According to public information, RemeGen plans to submit marketing authorization applications for these two indications in the second half of 2025 and the first half of 2026, respectively. RemeGen has previously stated its intention to out-license the rights to RC28. Given the current progress, the transaction is expected to be completed prior to the New Drug Application (NDA) submission.

Furthermore, Hengrui Medicine’s HR19034 also warrants attention. This anti-VEGF bispecific antibody has entered Phase III clinical trials and efficiently blocks the VEGF signaling pathway by simultaneously targeting two distinct epitopes of VEGF, thereby inhibiting neovascularization to treat wet age-related macular degeneration (AMD).

Overall, domestic companies have clear objectives in designing dual-target drugs: first, to significantly reduce treatment frequency and improve patient adherence; second, to provide additional ancillary benefits, such as the anti-fibrotic effects of RC28 and the anti-vascular leakage properties of IBI302, both of which effectively enhance overall therapeutic efficacy.

Although gene therapy has cooled in other areas, it remains exceptionally hot in the treatment of retinal diseases.

According to data from Molecule Pharma, there are currently more than 300 gene therapy drugs using AAV as a viral vector in clinical development worldwide, with over 80 of them in the field of ophthalmology.

This is because gene therapy in ophthalmology is relatively safe. On one hand, the relatively enclosed ocular environment confers immune privilege, and the small volume of the eye requires low viral vector doses, resulting in minimal systemic impact. On the other hand, retinal cells do not regenerate or divide, and many ophthalmic diseases are caused by single-gene mutations, making them ideal targets for gene therapy.

During the treatment of age-related macular degeneration (AMD), anti-VEGF therapy can slow disease progression and improve vision in some patients, but it requires frequent intravitreal injections, resulting in poor patient compliance and limited efficacy in certain individuals. Gene therapy can transduce ocular tissues with viral vectors expressing anti-VEGF agents, enabling long-term endogenous expression of therapeutic proteins, thereby addressing the challenges of frequent injections and poor long-term treatment adherence.

Taking ABBV-RGX-314, an ophthalmic gene therapy with advanced global development (currently in Phase 3 clinical trials), as an example, previous Phase 2 clinical data showed a 97% reduction in the need for anti-VEGF injections during a 9-month observation period. Furthermore, all patients required zero or only one supplemental anti-VEGF injection, with 78% of patients completely free from supplemental therapy. This means that the majority of patients, after receiving a single dose of ABBV-RGX-314, do not require frequent anti-VEGF injections for an extended period, significantly reducing the treatment frequency.

Notably, AbbVie acquired this pipeline from ReGenXBio in September 2021 through a deal valued at up to $1.752 billion. This demonstrates AbbVie’s commercial confidence in gene therapy’s potential to break through the limitations of traditional treatments and capture a substantial market share.

Gene Therapy Pipelines for AMD Indications in Clinical Stage in China, Data Sourced from Miotuan Pharma

Currently, R&D in the field of ophthalmic gene therapy in China is also quite active. Although none of the gene therapy pipelines for the two major fundus diseases—wet age-related macular degeneration and diabetic retinopathy—have reached Phase III clinical trials, there are currently nearly 10 gene therapy pipelines in China that have entered the clinical stage.

The next three years may become a critical window for the development of gene therapy in ophthalmology. If AbbVie’s RGX-314 successfully launches, it will significantly stimulate the global market. With Chinese pipelines lagging by approximately two years, they are well-positioned to catch up with this wave. Amidst the profound transformation in the fundus treatment market, Chinese pharmaceutical companies are bound to become key players at the table.